Even after a top-notch repair job, a car that's been in an accident is worth less than one that hasn't. That loss in market value is what we call diminished value. It's the permanent financial hit your vehicle takes simply because an accident is now part of its official history.

Think about it from a buyer's perspective. An accident history is a red flag, making them wary and giving them a reason to offer you less money.

Understanding the Real Cost of an Accident

Let's say you're shopping for a used car. You find two that are exactly the same—same make, model, year, and mileage. The only difference? One has a clean vehicle history report, while the other was in a major collision last year, though it was repaired by a certified shop.

Which one are you going to buy? And if you did consider the one with the accident, you’d expect a pretty hefty discount, right?

That discount is the very essence of what is diminished value. It's the invisible damage that sticks around long after the dents and scratches have been fixed, directly impacting your wallet.

Why Perfect Repairs Aren't Enough

The best body shop on the planet can make a car look brand new, but they can't erase its past. That accident will be permanently stamped on vehicle history reports from services like CARFAX and AutoCheck.

This public record creates a stigma. It immediately makes your car less desirable to potential buyers and reduces what a dealer will offer on a trade-in. This isn't just a theoretical drop in value; it's a real, measurable financial loss you'll face down the road.

The moment a vehicle is in an accident, its value drops. This immediate loss is based on public perception—a repaired car is simply less desirable than one with a pristine record.

This is exactly why filing a diminished value claim is so crucial. You have a legal right to be compensated for this loss by the at-fault party's insurance. The entire point of an insurance settlement is to make you "whole" again, and that includes restoring the market value your car lost, not just fixing the physical damage.

The Financial Impact by the Numbers

Just how much are we talking about? The loss can be surprisingly large, often shaving a significant percentage off your car’s pre-accident value.

Multiple studies have shown that a vehicle with an accident on its record can lose anywhere from 10% to 25% of its market value. For a car that was worth $20,000 before the crash, that could mean an instant loss of $5,000, no matter how great the repairs look.

For a quick overview of these concepts, take a look at the table below.

Quick Guide Diminished Value at a Glance

| Concept | Explanation |

|---|---|

| Definition | The reduction in a vehicle's resale value after it has been damaged and repaired. |

| Primary Cause | The permanent negative stigma associated with a vehicle's accident history. |

| Financial Impact | A typical loss of 10% to 25% of the car's pre-accident market value. |

| Your Right | To be compensated for this loss by the at-fault driver's insurance company. |

This table helps break down why diminished value is a real financial loss that you shouldn't have to absorb.

You can get a rough estimate of your potential loss by using a diminished value claim calculator as a starting point. The type of vehicle also plays a big role. Compact cars, for instance, can lose up to 25% of their trade-in value, while SUVs might see a more modest 10-15% drop.

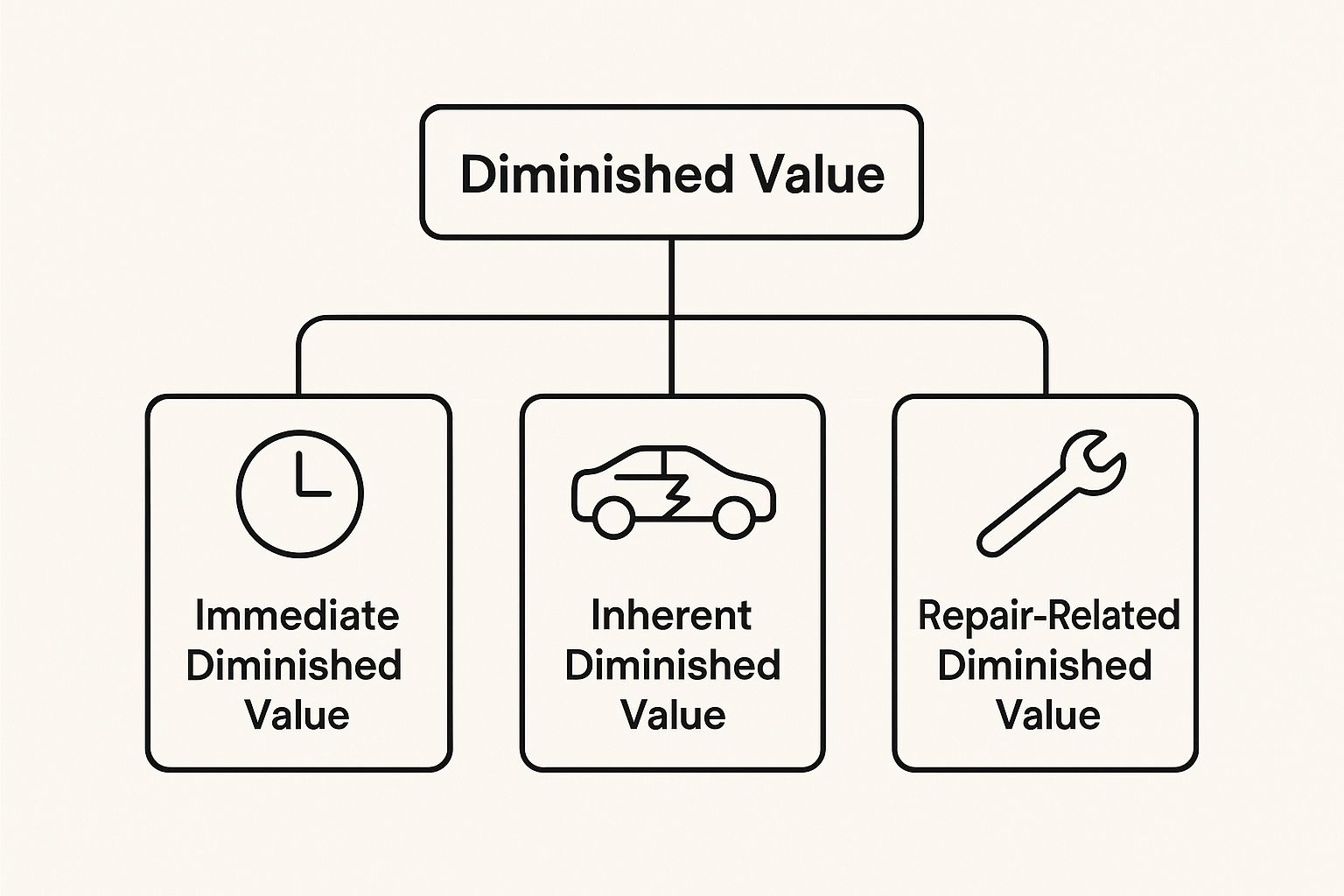

Understanding the Three Types of Value Loss

When your car gets hit, the drop in value isn't just one simple number. It's actually broken down into three different types, and knowing which one applies to your situation is the key to getting the compensation you deserve. Each type of loss happens for a different reason and at a different stage of the process.

Let's break them down.

As you can see, the loss in value starts the moment of impact and can even be made worse by a bad repair job.

Inherent Diminished Value

This is the big one—the most common and unavoidable type of loss. Inherent diminished value is the automatic hit your car's resale price takes simply because it now has an accident on its record.

Think about it from a buyer's perspective. You have two identical cars, but one has a clean CARFAX report and the other shows a collision history. Even if the repaired car looks perfect, which one would you choose? Most people would pick the one without the accident history, or at the very least, they’d expect a steep discount for taking the "branded" vehicle. That discount is inherent diminished value.

This is the fundamental loss you're entitled to claim from the at-fault driver's insurance.

Repair-Related Diminished Value

Now, let's say the repairs weren't perfect. Repair-related diminished value is the additional loss in value caused by shoddy workmanship. When a body shop cuts corners, you're not just left with a bad repair job; your car's value plummets even further.

Some classic signs of poor repair work include:

- Mismatched paint that you can spot a mile away in the sun.

- Cheap aftermarket parts used instead of factory OEM parts.

- Uneven gaps between body panels that weren't there before.

- New rattles or strange noises that started after you got the car back.

This extra layer of value loss exists because any future buyer will see these flaws and know they'll have to spend their own money to fix them, driving down what they're willing to pay you.

The quality of repairs directly impacts your vehicle's final value. Poor workmanship not only looks bad but also actively subtracts more money from your car's worth, compounding the initial inherent loss.

Immediate Diminished Value

Finally, we have immediate diminished value. This is a more theoretical concept, but it's important. It represents the difference between your car's value right before the crash and its value immediately after the crash, but before a single repair has been made.

Essentially, it’s what your car is worth in its wrecked, damaged state. While you probably won't file a claim for this specific type (since most people get their cars fixed), it helps establish a crucial point: the financial loss happens the instant the collision occurs, not weeks later when the repairs are finished.

How Insurance Companies Calculate Your Claim

When you file a diminished value claim, the at-fault driver's insurance company isn’t just guessing what your car has lost in value. They pull out a specific, and often controversial, formula to generate their initial offer. Knowing how their math works is the first step to pushing back on a lowball number.

Most insurers lean on a calculation called the "17c formula." This method isn't some gold standard of appraisal; it came out of a 2001 Georgia court case and was quickly adopted by the industry for one simple reason: it consistently produces low payouts. It's a structured system, but one that’s deliberately designed to limit what the insurer has to pay.

The formula kicks off by immediately capping the maximum possible diminished value at 10% of your vehicle's pre-accident value, typically based on a source like the NADA guide. This is the first red flag. An arbitrary 10% cap completely ignores the reality that a car with significant frame damage could lose far more of its resale value.

The Problematic "Modifiers"

Once that 10% ceiling is in place, the insurer applies two "modifiers" to whittle the number down even further. Think of these as deductions designed to penalize you for the extent of the damage and your car's mileage, ensuring the final offer is just a fraction of that initial capped amount.

First up is the damage modifier. This is a subjective multiplier based on the adjuster's interpretation of the damage severity.

- 1.00 Multiplier: Reserved for severe structural damage.

- 0.75 Multiplier: Applied for major damage to panels.

- 0.50 Multiplier: Used for moderate damage to panels.

- 0.25 Multiplier: For minor damage to panels.

- 0.00 Multiplier: Assigned if there's no structural damage or panel replacement.

Next, they apply the mileage modifier. This second deduction reduces the amount again based on the odometer reading at the time of the wreck. Higher mileage means a bigger cut from your claim.

A common misconception is that the insurance company's calculation is the final word on your claim. In reality, their formula is just a starting point for negotiation—one that is heavily weighted in their favor.

Seeing the Flawed Formula in Action

Let's walk through a real-world example. Say your car was worth a solid $30,000 before the accident. The 17c formula immediately limits your potential claim to just $3,000 (10% of the car's value).

Now, let's say the adjuster labels the damage as "major," applying a 0.75 multiplier. Your car also has 60,000 miles, which might trigger a mileage multiplier of 0.60. Suddenly, your offer shrinks dramatically.

The final calculation looks like this: $3,000 x 0.75 x 0.60 = $1,350.

The real-world loss in market value might easily be $5,000 or more, but their internal formula spits out an offer of only $1,350. This is precisely why their first offer should never be taken at face value. It’s a number generated to protect their bottom line, not to make you financially whole again, and it's the single best argument for getting an independent appraisal to prove your true loss.

Here's the rewritten section, designed to sound completely human-written and natural.

Why Your Car's Identity and Market Whims Can Make or Break Your Claim

Figuring out a car’s diminished value isn’t just about plugging numbers into a formula. Far from it. The real-world loss you’ve suffered is powerfully shaped by two things that have nothing to do with the accident itself: the kind of vehicle you own and what’s happening in the used car market right now. This is precisely why those generic online calculators often miss the mark by a mile.

Think about it this way. A pristine Porsche 911 or a high-end Mercedes has a certain reputation to maintain. An accident, even a minor one, puts a permanent black mark on its history—a much bigger deal than a similar fender-bender on a ten-year-old Honda Civic. Buyers in that luxury space are paying for perfection, and any hint of past damage makes them extremely hesitant, causing the car's value to plummet.

On the other hand, a super common car like a Toyota Camry might see a smaller drop in its percentage value, but it's a loss nonetheless. Its value is tied more to reliability than prestige, but that accident history still gives a potential buyer all the leverage they need to haggle the price down.

Riding the Waves of the Auto Market

Beyond what’s sitting in your driveway, the entire automotive market is a living, breathing thing. Supply and demand, consumer confidence, and broader economic trends are constantly shifting, and these currents directly pull your car's value—and your diminished value claim—along with them.

Things like inflation, rising interest rates, or even a spike in gas prices can completely change what people are willing to pay. If the used car market is red-hot and everyone is desperate for a vehicle, that accident history might not hurt as much. But when the market cools down and buyers have plenty of options, they get a lot pickier. Suddenly, that "clean CarFax" becomes a non-negotiable, and your repaired vehicle gets left on the lot.

The used car market is the ultimate judge of diminished value, and its verdict changes from state to state and month to month. In 2024, global car production hit 75.5 million units, but where those cars were built and sold created massive regional imbalances. These supply-and-demand shifts are a huge piece of the puzzle. You can dive deeper into these market factors that impact diminished value on diminishedvalueofgeorgia.com.

Location, Location, Location… and Season?

You’d be surprised how much your zip code and the calendar can influence your claim. A big 4×4 truck is a hot commodity in a place with heavy winters, so an accident on one in Colorado will likely cause a bigger value drop than the same accident in Florida, where it's just another large vehicle.

Seasonal demand is a real thing, too:

- Convertibles and sports cars: Everyone wants one when the weather gets nice. Their value (and the potential loss after a wreck) peaks in the spring and summer.

- SUVs and trucks: Demand for these often climbs in the fall and winter as people start thinking about snow and slick roads.

Smashing up a convertible in April, right at the start of its prime selling season, could result in a much higher diminished value than if the same thing happened in November.

A true professional appraiser knows all of this. They don't just look at a book value; they dig into local sales data, track seasonal trends, and build a case grounded in the reality of your specific market. That’s how you prove your actual financial loss and get the settlement you deserve.

Here is the rewritten section, crafted to sound human-written and natural.

How an Independent Appraisal Strengthens Your Claim

Let's be blunt: after an accident, you and the insurance adjuster are on opposite teams. Your goal is to be made whole again—to recover every penny you lost. Their job, plain and simple, is to pay out as little as possible. This conflict of interest is why an independent appraisal isn't just a good idea; it's your most powerful tool.

An independent appraisal isn't just a second opinion. It's a detailed, evidence-backed report from a certified professional who works for you, not the insurance company. This is a crucial distinction. The appraiser’s assessment is based on real-world market data, a world away from the insurer’s self-serving internal formulas (like the infamous 17c method) that are specifically designed to spit out low numbers.

The Anatomy of a Powerful Appraisal Report

A real appraisal is much more than a number on a piece of paper. Think of it as the expert testimony that proves your case. It’s a detailed, defensible document that serves as concrete proof of your car’s lost market value and becomes the foundation for your entire negotiation.

A rock-solid report will always contain a few key elements:

- Detailed Vehicle Information: A complete breakdown of your car—make, model, year, trim, mileage, and its specific condition before the accident.

- Local Market Analysis: This is critical. The valuation must be based on sales data from your actual area, not some generic national average that doesn't reflect your local market.

- Comparable Vehicle Sales: The appraiser will pull "comps," showing real-world examples of similar cars without an accident history selling for more than those with one.

- Professional Valuation Methodology: It won’t just give you a number; it will show the math. The report clearly explains how the appraiser calculated the final diminished value figure.

This isn't just a request for more money; it’s a professionally supported demand backed by hard facts.

An independent appraisal completely flips the script. The burden of proof is no longer on you to argue against their lowball offer. It's now on the insurance company to try and poke holes in a report written by a certified expert.

An Investment, Not an Expense

It’s easy to look at the cost of an appraisal and hesitate, but that's the wrong way to think about it. See it as a strategic investment. The fee you pay for a professional report is almost always a tiny fraction of the thousands of dollars in value it helps you get back.

When you hand the at-fault insurer an unbiased, expert-backed report, you’re taking the negotiation off their home field and moving it to neutral ground. You're no longer just another claimant they can push around. You're armed with a professional assessment that can stand up to scrutiny, giving you both the evidence and the confidence to demand what you're legally owed.

Your Step-By-Step Guide To Filing a Claim

Knowing your car has lost value is one thing, but actually getting the insurance company to pay up is a whole different ballgame. The process can seem daunting, but it's really just a matter of building a solid case. If you approach it methodically, you’ll be in a much stronger position to get what you're rightfully owed.

Before you do anything else, you need to confirm you're eligible. Here's the key: diminished value claims are filed against the at-fault driver's insurance, not your own policy. So, if someone else hit you and their carelessness caused the accident, you have a clear path to pursue compensation for your car's lost market value. This is the first and most important box to check.

Assembling Your Evidence

Once you've confirmed you can move forward, your mission is to gather the proof. Think of yourself as a detective building a case file. Every document you collect strengthens your position and makes it harder for the insurance adjuster to deny or lowball your claim.

To make your claim undeniable, you'll need to create a complete file with all the critical paperwork.

Here is a quick checklist of the essential documents you'll need to build a rock-solid diminished value claim. Having these organized and ready to go will make the entire process smoother and significantly increase your chances of a successful outcome.

Essential Documents for Your Diminished Value Claim

| Document | Why You Need It |

|---|---|

| Official Police Report | This is the official record that proves who was at fault for the accident. It's non-negotiable. |

| Itemized Repair Invoices | You need a detailed breakdown of every single repair, part, and labor hour. This documents the severity of the damage. |

| Before & After Photos | Visual proof is powerful. Photos of the initial damage and the completed repairs tell a clear story. |

| Independent Appraisal Report | This is your expert witness. It's the professional, data-backed report that calculates your exact financial loss. |

Gathering these documents puts you in control of the narrative, proving not just that the accident happened, but exactly how it impacted your vehicle's value.

A huge mistake people make is trying to file a claim without getting their own appraisal. Relying on the insurance company’s assessment is like letting the opposing team’s coach be the referee. You need an unbiased expert in your corner.

With your evidence in hand, it's time to make your move. You'll officially start the process by sending a formal demand letter to the at-fault party's insurance adjuster. This isn't just a casual email; it’s a professional document that clearly states your intent, lays out the facts of the case, and includes copies of your appraisal and all your supporting evidence.

This letter kicks off the negotiation. From this point on, stay professional, keep a record of all communication (preferably in writing), and use your independent appraisal as the anchor for your arguments. For a more detailed walkthrough, our guide explains exactly how to file a diminished value claim from start to finish. Armed with the right proof and a confident strategy, you can successfully navigate the process and recover the money you're owed.

Common Questions About Diminished Value

When you start digging into a diminished value claim, a lot of questions pop up. It’s totally normal. Getting straight answers is the first step to feeling in control of the situation. Let's tackle some of the most common things people ask.

Can I File If the Accident Was My Fault?

This is a big one, and the answer is usually no. Diminished value is something you claim against the at-fault party's insurance company.

Your own collision coverage is there to pay for the repairs—to get your car back on the road and looking like it did before the wreck. It isn't designed to compensate you for the hit your car’s resale value takes.

The one major exception is in Georgia. There, you might be able to file a diminished value claim under your own Uninsured/Underinsured Motorist (UM) policy if the person who hit you doesn't have enough insurance.

Is There a Time Limit to File?

Yes, and this is a deadline you can't afford to miss. Every state has a legal time limit for filing property damage claims, known as the statute of limitations. Diminished value falls squarely into this category.

This window can be anywhere from two to five years, depending on your state. It's really important to look up the specific deadline for where you live and get the ball rolling as soon as your repairs are done.

Does My Car’s Age or Mileage Matter?

It matters a lot. A brand-new car with only a few thousand miles on the odometer has a ton of value to lose, so its diminished value claim will naturally be higher.

An older car with 150,000 miles has already seen most of its depreciation, so the added loss from an accident history will be smaller. That said, even older cars, especially classic, rare, or impeccably maintained models, can still have very legitimate and significant claims.

For a deeper dive, check out our guide on understanding diminished value after an accident.

Don't let the insurance company dictate what your vehicle is worth. At Total Loss Northwest, our certified appraisers provide the expert, data-backed reports you need to fight for a fair settlement. Whether it's a diminished value claim or a total loss, we ensure you recover what you're truly owed. Get your certified appraisal today.