Ever heard the term "fair market value" and wondered what it actually means? At its heart, it’s simply the price an asset would sell for on the open market. But there's a crucial catch: it assumes both the buyer and seller are willing, knowledgeable, and not under any pressure to make a deal.

Think of it like selling a classic car. It’s not about the price you’d take if you were desperate for cash, nor is it the pie-in-the-sky number you dream of. It’s that realistic sweet spot where an informed buyer and an equally informed seller can shake hands, both feeling good about the price.

Defining Fair Market Value Without The Jargon

While the idea seems straightforward, "fair market value" (or FMV) is a heavyweight term in the worlds of finance, law, and especially insurance. It’s the bedrock number used to figure out what your vehicle is worth after a total loss or the value of a property for tax purposes. To really get a handle on it, you need to understand the conditions that make a transaction truly "fair."

To better illustrate this, let's break down the essential components that must be present for a price to be considered the true FMV.

Core Components of Fair Market Value

| Component | Description | Real-World Implication |

|---|---|---|

| Willing Parties | Both the buyer and seller are participating by choice. Neither is being forced into the transaction. | A court-ordered liquidation isn't FMV because the seller is compelled to sell, often leading to a lower price. |

| Reasonable Knowledge | Both sides understand the asset, its condition, and current market trends. No one is operating in the dark. | If you sell your car without knowing it's a rare model, the price you get probably isn't its true fair market value. |

| No Undue Pressure | Neither party is acting out of desperation. The timing is neutral, not driven by an emergency. | Selling your truck for quick cash to pay a sudden bill means you'll likely accept less than what it’s actually worth. |

This framework isn't just a good idea—it's so important that the U.S. government has a formal definition for it. The concept of a willing buyer and seller, both reasonably informed and free from compulsion, is the legal standard. You can read more on the official definition from the International Society of Appraisers to see how these ideas are set in stone.

Key Takeaway: Fair Market Value is not the sticker price, what someone hopes to get, or what it costs to buy a brand-new replacement. It's the realistic, negotiated price that comes from a balanced, informed, and unforced sale.

Getting this concept right is everything. Whether you're dealing with an estate, donating to charity, or—most critically for this guide—arguing with an insurance company over a total loss settlement for your car, these principles are your best tool. They give you the power to push back on a lowball offer by asking a simple question: "Does this number truly reflect what a knowledgeable buyer and seller would agree on in today's market?"

Of course. Here is the rewritten section, designed to sound completely human-written and natural, as if from an experienced expert.

Why Fair Market Value Actually Matters to You

It’s one thing to read a definition of “fair market value” in a glossary, but it's another thing entirely to see how that number plays out in your own life. This isn't just some abstract term for accountants and lawyers to toss around. FMV has a direct, and often surprisingly large, impact on your wallet.

Suddenly, it stops being a theoretical concept and becomes a hard number that can define the outcome of some of life's most significant financial moments. From insurance claims to tough family situations, fair market value is the yardstick used to put a dollar figure on your most valuable possessions.

Where You'll Encounter Fair Market Value

Let’s get practical. Picture this: your reliable car gets into a bad wreck, and your insurance company declares it a total loss. The check they're about to write isn't for what you originally paid, nor is it enough to buy a brand new replacement. Their offer is based on the car's fair market value an instant before the accident happened.

This value is a cocktail of factors—the car's age, its mileage, its overall condition, and what similar vehicles have recently sold for right in your local area.

Here are a few other common scenarios where FMV becomes the most important number in the room:

- Charitable Donations: Thinking of donating a car, a piece of art, or even real estate to a good cause? If it's worth more than $5,000, the IRS will want to see a formal appraisal that establishes its FMV before you can claim that tax deduction.

- Estate Settlements: When an estate is being settled after a loved one passes, assets must be valued at their FMV. This is a crucial step for the IRS to accurately calculate any estate taxes that might be owed.

- Divorce Proceedings: In a divorce, assets acquired during the marriage—the house, cars, investment accounts—have to be valued at their FMV to ensure they can be divided fairly between both parties.

In any of these situations, getting the valuation wrong can be a costly mistake. It could mean accepting thousands less from an insurance payout or walking away from a divorce with an unfair settlement.

The Bedrock of a Fair Number

So, how do we know the number is fair? The process for determining FMV isn't just a wild guess; it’s built on principles that have been tested in courtrooms and financial institutions for decades.

For instance, the IRS didn't just invent these rules. They rely on a framework that has evolved over time.

A cornerstone for appraisers in the United States is Revenue Ruling 59-60. It codifies the whole idea of a "willing buyer and a willing seller," making it clear that neither party can be forced into the deal and both must have all the relevant facts about the asset and the market.

This isn't just bureaucratic nonsense. It's a system designed to keep valuations grounded in reality and prevent someone from just pulling a number out of thin air. These principles ensure the final figure truly reflects what’s happening in the market. If you're interested in the nitty-gritty, you can explore detailed insights on the real-world application of FMV.

Ultimately, having a solid grasp of what fair market value is—and just as importantly, what it isn't—is empowering. It gives you the confidence to scrutinize an insurance settlement, challenge an appraisal you think is off, and stand up for your own financial well-being. Without it, you’re basically forced to take whatever number you're given, and that’s a vulnerable place to be.

How Professionals Pinpoint Fair Market Value

So, how do appraisers and insurance companies actually arrive at that final number for your car or any other asset? It's not magic, and it's certainly not a random guess. Professionals use a set of well-established methods to calculate fair market value, making sure the price is based on solid data and sound reasoning.

These valuation techniques provide a clear, defensible framework. While the best method depends on the asset in question—a 2019 Honda Civic is valued differently than a commercial warehouse—the goal is always the same: to determine a realistic price for a no-pressure, open-market transaction.

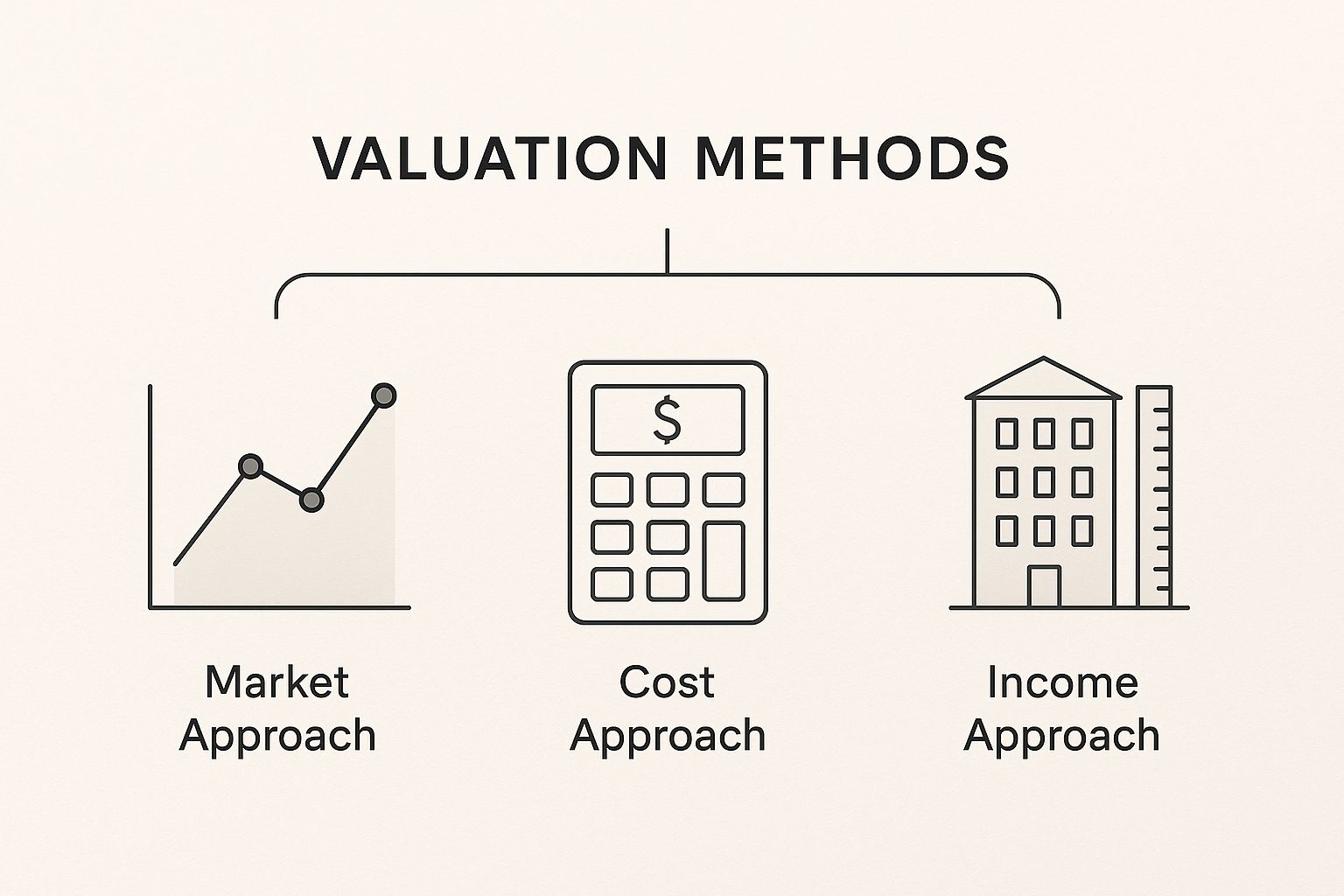

This image neatly summarizes the three main approaches appraisers have in their toolkit.

As you can see, professionals don't just pick one at random. They choose between market, cost, and income-based strategies to build a complete and accurate picture of an asset's worth.

The Three Core Valuation Methods

Let’s dig into the three main ways professionals determine FMV. Each one offers a unique perspective, and the right choice is dictated by the nature of the asset itself.

-

Market Approach: This is by far the most common and intuitive method. It answers the question, "What are similar things selling for right now?" For a car, this means an appraiser scours dealer listings and private sale records for vehicles of the same make, model, year, and condition in your specific region. It's the real-world evidence of what buyers are actually paying.

-

Cost Approach: This method works from a different angle, asking, "What would it cost to replace this item brand new?" It calculates the price of constructing an identical asset from the ground up and then subtracts value for depreciation—things like age, wear, and tear. You'll see this used for one-of-a-kind assets, like a custom-built machine or a historic building, where there are no direct "comparables" to analyze.

-

Income Approach: This one is all about the money-making potential. An asset's value is determined by the cash flow it's expected to generate over its useful life. It’s the standard for valuing investment properties, apartment buildings, and operating businesses.

Expert Take: The choice of valuation method is strategic, not arbitrary. It hinges on the type of asset and the quality of available data. A car appraisal almost exclusively relies on the Market Approach, while a commercial property appraisal will lean heavily on the Income Approach.

Comparing Valuation Methods

To make it even clearer, here’s a simple breakdown of how these three approaches stack up against each other.

| Valuation Method | How It Works | Best For |

|---|---|---|

| Market Approach | Analyzes recent sales of comparable assets. | Cars, residential homes, publicly traded stocks. |

| Cost Approach | Calculates replacement cost minus depreciation. | Unique assets, insurance purposes, new construction. |

| Income Approach | Projects future cash flow the asset will generate. | Commercial real estate, businesses, rental properties. |

Understanding these methods gives you the power to read and question any appraisal report you're handed, especially after an accident.

This isn't just a niche business practice; it's a concept that underpins global commerce. Fair Market Value is a critical metric for everything from taxation and financial reporting to mergers and acquisitions. The IRS, for instance, relies on precise FMV calculations for estate taxes, a process that affects billions of dollars annually.

Even in the digital world, the same principles apply. Professionals use tools like a domain name value estimator to assess the worth of online assets.

Ultimately, having this knowledge is crucial when you've suffered a loss. For example, knowing how your vehicle is valued is the first step in recovering its lost worth after an accident. To see how this applies in a real-world scenario, check out our guide on how to file a diminished value claim in Washington.

How to Navigate a Total Loss Car Insurance Claim

For most people, a total loss claim is their first real, and incredibly stressful, introduction to the concept of fair market value. It’s a harsh lesson. When the insurance company declares your car a "total loss," they're saying the repair costs are more than the vehicle was worth right before the accident.

The settlement check they offer isn't for a new car. It's for your old car's Fair Market Value (FMV), which they'll often call Actual Cash Value (ACV). Understanding this is the first step, but dealing with the process, especially when their initial offer feels way too low, can be a real battle. To protect your finances, you need to know how they got their number so you can effectively push back.

How Insurers Calculate Your Car's Value

Insurance adjusters don't just pull a number out of a hat. They rely on powerful third-party valuation software, with names like CCC Intelligent Solutions or Mitchell International, which crunches a massive amount of market data to spit out a detailed report. This report becomes the foundation for their settlement offer.

Here’s a look at what their systems analyze to pin down that ACV:

- Vehicle Specifics: The basics—year, make, model, and trim.

- Mileage: A straightforward factor. Lower miles usually mean higher value.

- Overall Condition: This is where things get subjective. The adjuster grades your car’s pre-accident condition (e.g., clean, average, rough), and this is a frequent point of disagreement.

- Recent Upgrades: Did you just drop money on new tires, a premium sound system, or major engine work? These can add significant value, but you absolutely have to prove it with documentation.

- Local Market Comparables: The software scours your geographic area for recent sales of cars just like yours to set a market baseline.

The final number is a mix of all these data points. But here’s the problem: these automated reports are far from perfect.

Crucial Point: Think of the insurer’s valuation report as their opening bid in a negotiation, not the final word. It's incredibly common for these reports to miss key features, undervalue your car's condition, or use "comparable" vehicles that simply aren't, leading to a lowball offer.

What to Do if the Offer Is Too Low

There are few things more gut-wrenching than getting a settlement offer that won't even pay off what you still owe on the car. Don’t panic, and don't accept it. You have every right to dispute their valuation and present your own evidence to get a higher, fairer payout.

Start by combing through their valuation report, line by line. Look for mistakes—is the mileage wrong? Are they missing options or features your car had? Are the comparable vehicles they used base models in poor condition?

Next, gather your own ammunition. Pull together all your maintenance records, find receipts for any recent upgrades, and search for online listings of truly comparable cars for sale in your area.

If presenting your own facts and figures doesn't make them budge, you have a powerful tool built into most auto policies: the Appraisal Clause. This provision gives you the right to hire your own certified, independent appraiser to conduct a completely separate valuation. A professional can build a comprehensive report that captures your vehicle's real worth. If you find yourself in this fight, you can learn more about how a professional total loss vehicle appraisal can give you the leverage you need for a fair settlement.

Fair Market Value Versus Other Valuations

Once you start dealing with assets like homes or cars, you'll find a whole dictionary of valuation terms being thrown around. It’s incredibly easy to mix up "fair market value" with "assessed value" or "insurable value," but getting them wrong can be a costly mistake.

Think of these different values as specific tools for specific jobs. You wouldn't try to saw a board with a screwdriver, and you shouldn't rely on your property tax assessment to price your home for sale. Let's break down what each one really means and where it applies.

Assessed Value for Taxes

Your local government calculates your property’s assessed value for one reason and one reason only: to figure out your property tax bill. This number is almost never what your home would actually sell for on the open market.

Why the difference? Assessors typically use a mass appraisal system, valuing entire neighborhoods at once with broad strokes. On top of that, many places use an "assessment ratio," meaning the assessed value is deliberately set at a fraction—say, 80%—of its estimated market value. This is why the value on your tax statement usually looks disappointingly low compared to what a real buyer would pay.

Insurable Value for Replacement

Now, let's talk about insurable value. This figure is all about a worst-case scenario. It represents the cost to rebuild your home from scratch if it were completely destroyed, perhaps by a fire or a tornado.

Crucially, insurable value excludes the value of the land itself—after all, the land will still be there after a disaster. It focuses purely on the current cost of materials and labor needed for a total reconstruction. Depending on the construction market, this number can sometimes be higher or lower than the fair market value.

Key Difference: Fair market value is what your entire property, land and all, is worth to a buyer today. Insurable value is the cost to rebuild only the structure, excluding the land.

Actual Cash Value for a Total Loss

When your car is declared a total loss, the insurance company will bring up Actual Cash Value (ACV). In the world of auto insurance, ACV is essentially the same concept as fair market value. It’s what your vehicle was worth on the open market in the moments right before the accident happened.

To calculate ACV, an insurer starts with the replacement cost for a similar vehicle and then deducts for depreciation based on its age, mileage, wear and tear, and overall condition. Understanding this is absolutely vital to getting a fair settlement check. If you find yourself in this situation, you can learn more about how to determine the actual cash value for your car to make sure you're getting what you're owed.

Common Questions About Fair Market Value

https://www.youtube.com/embed/ZQ8wODESzhs

Even when you've got the basics down, fair market value can still feel a bit tricky in the real world. It's one of those concepts that sits at the intersection of legal definitions, tough negotiations, and everyday situations, so a few questions are bound to pop up.

Let's clear the air and tackle some of the most common ones. These are the practical details that help you connect the dots, whether you’re talking to an appraiser, negotiating with an insurance adjuster, or just trying to figure out what something is really worth.

Can Fair Market Value Be a Range?

Yes, absolutely. In fact, it’s almost never a single, concrete number. It’s far more accurate to think of fair market value as a defensible range of values.

Think of it this way: two highly qualified appraisers can look at the exact same vehicle and come to slightly different conclusions. They’re both using legitimate market data, but their interpretations might vary. One appraiser might find three comparable cars that recently sold for $18,500, $19,000, and $19,200. The other might find a different set of comps that sold for $18,800, $19,300, and $19,600.

Neither is wrong. They've just established a reasonable FMV that falls somewhere between $18,500 and $19,600. There's no single magic number.

Is Asking Price the Same as Fair Market Value?

Not at all, and this is a crucial point to understand. An asking price is simply what a seller hopes to get. It’s the sticker price, the starting point for a conversation—not a reflection of what the market has proven it will bear.

Fair market value, on the other hand, is built on the foundation of actual sold prices. When an appraiser values a totaled car, for example, they can't just look at what dealers are listing similar cars for online. They have to use data from real, completed sales.

A simple way to keep it straight: asking prices are what people want, while fair market value is what people have actually paid. This is a fundamental rule in any professional appraisal.

How Does Condition Affect the Value?

Condition is a huge factor—and often the most subjective one. For a vehicle, appraisers use a grading scale (think excellent, clean, average, or rough) to describe its state right before the accident. It makes sense: a garage-kept car with a perfect interior will be worth much more than the same model with dings, stains, and worn-out tires, even if the mileage is identical.

This is where many insurance claims get messy. Adjusters who haven't seen the car might automatically classify it as "average" condition, which could undervalue it by thousands. This is precisely why your own evidence—like recent photos and detailed maintenance records—is so powerful. It helps you prove your car's true, pre-accident condition and fight for the value you're rightfully owed.

If you're dealing with a total loss claim and the insurance company's offer feels low, remember that you don't have to take it. Total Loss Northwest specializes in independent auto appraisals for clients in Washington and Oregon, giving you the solid evidence needed to secure a truly fair settlement. Visit us at https://totallossnw.com to get the expert valuation you deserve.