When you hear that a car has been "totalled," it doesn't necessarily mean it's a twisted pile of metal that can't be fixed. It's actually a business decision made by the insurance company.

Simply put, a car is declared a total loss when the cost to repair it is more than what the vehicle is worth. It’s a purely financial calculation, not an emotional one about whether your beloved car can be put back on the road.

When a Fender Bender Becomes a Total Loss

It’s a situation that catches many drivers by surprise. You get into what seems like a minor accident—a rear-end collision or a side-swipe—and your car still looks okay, maybe it even drives. Then the phone rings, and it's your insurance adjuster with the news you weren't expecting: "Your car is a total loss."

How is this possible? It all comes down to a straightforward formula.

Insurance companies compare the total estimated cost of repairs to your car's Actual Cash Value (ACV)—that’s what your vehicle was worth on the open market just moments before the crash. If the repair bill climbs past a certain percentage of the ACV, they'll write it off. In the U.S., that magic number, or total loss threshold, is often between 70% to 80% of the car's value. You can find more data on these trends from industry sources like Claims Journal.

The Bottom Line: A "total loss" is an economic verdict. If it's cheaper for the insurer to pay you the car's value and sell the damaged vehicle for scrap, that's exactly what they will do.

The Adjuster's Calculation Checklist

The adjuster's decision isn't made on a whim. It’s a methodical process based on a few key financial data points. They’re looking far beyond that dented bumper to understand the full financial picture. Knowing what they're looking at is the first step to making sense of the process.

To help you understand their perspective, here’s a breakdown of what goes into the decision.

Key Factors in a Total Loss Decision

| Factor | What It Means for You | Why It's Critical |

|---|---|---|

| Repair Costs | The final estimate from the auto body shop, covering everything from parts and labor to paint and finishing. | This is the main number being weighed against your car's value. Modern cars with sensors and cameras can make this cost skyrocket, even from minor damage. |

| Actual Cash Value (ACV) | This is your car's market value right before the accident. It accounts for its age, mileage, overall condition, and any special features. | The ACV sets the financial bar. A lower ACV means it's much easier for repair costs to hit the "total loss" threshold. |

| Salvage Value | The cash your insurer can get by selling your damaged car to a salvage yard, which will then use it for parts or scrap metal. | This is a crucial part of the insurer's math. The salvage value is money they recoup, which reduces their total payout and can be the factor that tips a car into the total loss category. |

Ultimately, these three elements—repair costs, ACV, and salvage value—are the pillars of the insurance company's calculation.

Decoding the Total Loss Formula

When an insurance company declares a car a "total loss," it’s not really a judgment on whether the car can ever be driven again. It's a purely financial decision, a business calculation designed to keep them from spending more to fix a car than it's actually worth.

At the heart of this decision is what's known as the Total Loss Formula. It’s a simple but crucial equation:

(Cost of Repairs + Salvage Value) ≥ Actual Cash Value (ACV)

If the cost to fix your car plus the money the insurer can get for the wreckage equals or exceeds your car's value right before the crash, they'll write it off. Let's dig into what each of those terms really means.

The Key Components Explained

Understanding this formula is all about knowing its three main parts.

- Actual Cash Value (ACV): This is the single most important number. It's the market value of your vehicle moments before the accident happened. Think of it this way: it's not what you paid, but what it would cost to buy an identical car—same make, model, year, mileage, and condition—in your local area today.

- Cost of Repairs: This is the full estimate from the body shop. A detailed car repair cost estimator is used to figure out the price for all the parts and labor needed. It also has to account for any hidden damage or the cost of recalibrating modern safety systems, which can add up quickly.

- Salvage Value: This is the silver lining for the insurance company. It's the amount they can expect to get by selling your damaged car to a salvage yard, which will then either sell the usable parts or scrap the metal. This value is subtracted from the insurer's total payout, reducing their overall loss on the claim.

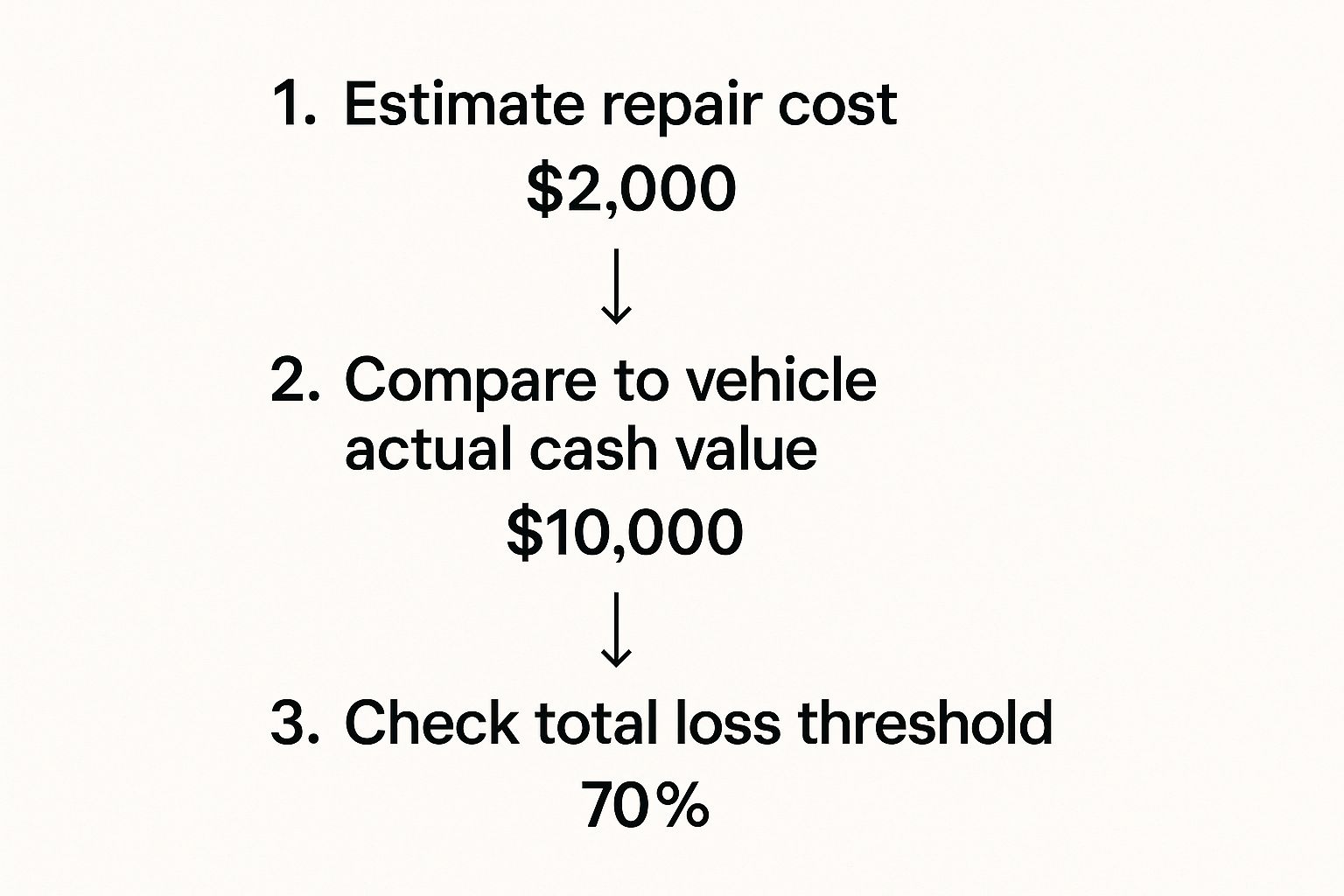

This image really helps visualize how all these pieces fit together in the decision-making process.

As you can see, the process flows from the initial repair estimate to comparing those costs against both the car's value and any specific rules set by the state.

Let’s put it into practice with an example. Say your car's ACV is determined to be $10,000. The body shop says repairs will run $7,000, and the insurer knows they can get $1,500 for the salvage.

Using the formula, we get ($7,000 + $1,500) ≥ $10,000. Since $8,500 is less than $10,000, the car would not be a total loss based on this formula alone. But, and this is a big but, if your state has a 70% threshold law, the $7,000 repair bill itself is enough to declare the car totalled, regardless of the salvage value.

How Insurers Calculate Your Car's Actual Cash Value

When your car is declared a total loss, everything hinges on one key figure: its Actual Cash Value (ACV). This isn't just a number plucked from thin air; it’s supposed to represent what your specific car was worth on the open market right before the accident happened. Getting this number right is the most critical—and often most debated—part of the entire claims process.

You might be tempted to look up your car's value on consumer websites, but insurers don't use those. They pull data from specialized third-party services that have access to a massive database of actual vehicle sales in your local area.

Think of it this way: the insurance adjuster is trying to determine the exact price a willing buyer would have paid a willing seller for your car, one minute before the crash.

Deconstructing the Valuation Report

An adjuster's valuation report goes deep. It's far more than just the year, make, and model. They are building a detailed profile of your exact vehicle to pinpoint its unique market value.

Several key factors will either raise or lower your car's ACV:

- Mileage and Trim Level: A low-mileage car with a top-tier trim package is naturally worth more than a basic, high-mileage version of the same model.

- Overall Condition: This is where the little things add up. The adjuster will account for pre-existing dings, scratches, interior wear and tear, and even how much life was left on your tires. A vehicle that was clearly well-maintained will fetch a higher value.

- Recent Upgrades: Did you just spend $800 on four new tires or recently install an upgraded stereo? Keep the receipts! These kinds of investments can boost your car’s value if you can document them.

- Local Market Data: Geography plays a huge role. The exact same truck might be more valuable in a rural community where it's in high demand than it would be in a dense urban center. The value is tied directly to what similar cars have recently sold for near you.

If the insurance company’s first ACV offer feels off, don't just accept it. You absolutely have the right to question their valuation. To prepare, check out our guide on how to determine the actual cash value for my car. By gathering your own evidence—like maintenance records and comparable vehicle listings from local dealerships—you can build a strong case to negotiate a settlement that truly reflects what your car was worth.

The Role of State Laws in Total Loss Claims

While your insurance company has its own way of calculating a total loss, it isn't the only rulebook in play. A huge factor in whether your car gets totaled is, quite simply, where you live.

Every state has its own department of insurance that sets the ground rules for the industry. A critical part of that is defining exactly when a vehicle must be declared a total loss. These state regulations act as a legal minimum, a line that insurers cannot cross. It’s why the same accident can have completely different outcomes depending on which side of a state line it happens on.

So, how do states actually do this? They generally use one of two methods: the Total Loss Threshold (TLT) or the Total Loss Formula (TLF).

The Total Loss Threshold (TLT) is a straightforward percentage set by state law. If the estimated repair cost climbs past this percentage of your car's actual cash value (ACV), the insurer is legally required to total it. For instance, in a state with a 75% TLT, a car valued at $10,000 is automatically a total loss if the repair bill is $7,501 or higher.

State Rules Can Vary Wildly

Some states are very strict, setting a firm, non-negotiable percentage. Others are more flexible and adopt the Total Loss Formula, which says a car is totaled if the repair costs plus the expected salvage value are greater than or equal to the car's ACV. This gives the insurance company a bit more wiggle room.

These differences are not trivial. Let's look at a few examples to see just how much the rules can change from one state to another.

Examples of State Total Loss Thresholds

Here’s a quick comparison that shows the different approaches states take. This is the legal framework your insurance adjuster has to work within.

| State | Threshold Type | Governing Rule |

|---|---|---|

| Iowa | Total Loss Threshold (TLT) | A vehicle is totalled if repair costs exceed 70% of its fair market value. |

| Texas | Total Loss Threshold (TLT) | A vehicle is a total loss if repair costs exceed 100% of its ACV (essentially, if the repair bill is more than the car is worth). |

| Colorado | Total Loss Formula (TLF) | Colorado uses the TLF, giving the insurer more discretion based on the specific repair costs and potential salvage value. |

Knowing your state's rule is a big advantage. It helps you understand whether the adjuster’s decision is coming from a state mandate or just your insurer's internal policy. A quick search for your state's "total loss threshold" can give you the information you need to have a much more informed conversation.

What Are Your Options After a Total Loss?

So, you've just been told your car is a "total loss." That news kicks off the next stage of your insurance claim. Once you and the insurance company have landed on a final number for your car's value, you’ve got a big decision on your hands.

Most people take the straightforward route. They accept the settlement check (minus their deductible, of course) and sign the car's title over to the insurer. It's clean, simple, and lets you move on. But that’s not your only choice. You might have the option of owner retention.

Keeping Your Car: What Owner Retention Really Means

"Owner retention" is just the industry term for keeping your totaled car. If you go this route, you essentially buy the wreck back from the insurance company. They'll determine its salvage value—what it's worth as a heap of parts—and subtract that amount from your final settlement payment.

This can sound tempting, especially if you're a mechanic, the damage doesn't look that bad, or the car just means a lot to you. But you need to know what you're getting into, because it's a path loaded with complications.

The Reality of Salvage Titles

Once you decide to keep the car, the state DMV gets involved. They will brand the vehicle's title, changing it to a salvage title. Think of this as a permanent black mark on the car's record.

A salvage title creates some serious headaches:

- Getting Insurance is Tough: Good luck finding a standard insurer willing to offer anything more than basic liability coverage. Comprehensive and collision are usually off the table.

- The Road to "Rebuilt": You can't just fix it and drive it. The car has to be professionally repaired and then pass a very strict state inspection before it can be legally registered with a "rebuilt" title.

- Resale Value Tanks: The car's value takes a nosedive. Trying to sell a vehicle with a branded title is a nightmare because most buyers (and dealers) will run the other way.

In some places, a car can be a total loss but still be considered repairable. If you find yourself in that situation, understanding how to deal with Cat N classifications is a must. At the end of the day, the smartest move is almost always a financial one, not an emotional one.

Why More Cars Are Being Totalled Than Ever Before

If it feels like you're hearing about more cars being "totaled" after an accident, you’re not just imagining it. There are some powerful forces at play in the auto industry that make it easier than ever for an insurance company to write off a vehicle, even if the damage doesn't look catastrophic. The two biggest culprits are the advanced technology in new cars and the simple economics of an aging vehicle fleet.

Think about what's in a modern car's bumper. It’s no longer just a piece of plastic and foam. Today, it’s a complex hub for sensors, cameras, and radar that run everything from adaptive cruise control to automatic emergency braking. A simple fender bender can easily damage these delicate systems, skyrocketing repair costs. A once $500 bumper fix can now turn into a $5,000 job that includes expensive parts and precise recalibration.

The Double Impact of Age and Value

At the same time, the average age of cars on the road keeps climbing. While an older car might run perfectly well, its Actual Cash Value (ACV)—what it was worth right before the crash—is much lower than a newer model's. This creates a collision course where a high repair estimate quickly overtakes a low vehicle value.

It's a straightforward but harsh equation for many owners.

An older car with a low ACV is far more likely to be declared a total loss. A repair bill that’s a minor percentage of a new car’s value could easily surpass 75% of an older vehicle's entire worth.

These issues are magnified by wider automotive market trends and their impacts. As new cars become more expensive due to technology and electrification, the gap between new and used vehicle values can widen, while repair costs for all cars continue to rise.

Add in occasional supply chain problems for parts, and you have the perfect storm for more frequent total loss declarations. If you find yourself in this situation, getting a professional total loss vehicle appraisal is one of the best ways to make sure the insurance company's settlement offer reflects what your car was truly worth.

Your Top Questions About Total Loss Answered

Even with a good grasp of the basics, seeing your car declared a total loss can throw you for a loop. It's a confusing and stressful time. Let's walk through some of the most common questions we hear from car owners in this situation.

Can I Fight the Insurance Company's Decision to Total My Car?

Yes, you can—but it’s usually more effective to challenge the numbers they used rather than the total loss label itself. You have two main points of leverage: the repair estimate and your car's valuation.

First, you can get an independent repair estimate. Take your car to a trusted body shop and see how their quote compares to the insurer's. If there's a big difference, you have a solid starting point for a discussion.

More often, the real battle is over the Actual Cash Value (ACV). If you feel the insurer’s offer is too low, you'll need to build a case. Pull together your maintenance records, receipts for recent work like new tires or a brake job, and find online listings for genuinely comparable vehicles for sale in your area. This evidence is your best tool for negotiating a fairer settlement.

What Happens If I Owe More on My Loan Than the Insurance Payout?

This is a tough spot to be in. If the insurance settlement is less than your outstanding loan balance, you are still on the hook for paying off the difference to your lender.

This exact scenario is why Guaranteed Asset Protection (GAP) insurance exists. If you added GAP coverage when you financed your car, it steps in to pay off that remaining loan balance for you.

This gap between what you owe and what the car is worth is often called being "upside down" on a loan. Without GAP insurance, that debt becomes your personal responsibility to settle.

Will My Insurance Rates Go Up After a Total Loss?

It really comes down to who was at fault for the accident.

- Not At-Fault: If another driver caused the crash and their insurance is paying, your rates shouldn't be affected. The same usually goes for comprehensive claims, like if your car was stolen or totaled by a falling tree.

- At-Fault: If the accident was your fault, you should unfortunately expect your premium to increase when your policy renews.

If you're in Washington or Oregon and staring down a lowball offer from an insurer after a total loss, remember you don't have to take it. At Total Loss Northwest, our certified appraisers use the Appraisal Clause in your policy to fight for the fair market value you deserve. Find out more about how we can help you at Total Loss Northwest.