It’s a phrase no car owner wants to hear from their insurance adjuster: "Your car is a total loss."

So, what does that actually mean? In the simplest terms, a car is "totaled" when the cost to fix it, plus what it's worth as scrap, is more than its value right before the crash. Forget how bad the damage looks—this is purely a numbers game for the insurance company. If fixing your car costs more than it's worth, they’ll cut you a check instead.

What It Means When Your Car Is Totaled

Hearing your car is "totaled" is jarring, but it doesn't mean it has been flattened into a pancake. It’s a business calculation. Insurance companies are simply trying to avoid a bad investment—spending more to repair a car than it would cost to replace it.

Think about it like this: imagine you have an old laptop that needs a $600 repair. If you could buy the exact same working model online for $450, would you pay for the repair? Probably not. You’d take the more financially sensible route. That's exactly what an insurer does when they total your car.

The Total Loss Formula

At the heart of this decision is a straightforward calculation that adjusters use to determine if a vehicle is a total loss. It's not based on emotion or guesswork; it's all about where the numbers land.

The Total Loss Formula:

Cost of Repair + Salvage Value ≥ Actual Cash Value (ACV)

Getting a handle on these terms is the first step to understanding your claim. Let’s quickly break down what each part of that equation means for your wallet.

Navigating a total loss claim means you'll run into some specific insurance jargon. Getting familiar with these terms will help you understand the process and advocate for yourself more effectively.

Understanding Key Total Loss Terms

| Term | Simple Definition | Why It Matters to You |

|---|---|---|

| Actual Cash Value (ACV) | What your car was worth in the open market the moment before the accident. | This is the most crucial number. It's the basis for your settlement check from the insurance company. |

| Cost of Repair | The total estimated price for parts and labor to fix the car. | If this number gets too high relative to the ACV, it pushes the car toward being a total loss. |

| Salvage Value | The amount the insurer can get by selling your damaged car to a salvage yard. | The insurer adds this to the repair cost. A higher salvage value can tip the scales and total a car even if repair costs seem manageable. |

Once the insurer does the math and the repair costs plus salvage value are equal to or more than the car's ACV, they'll officially declare it a total loss. They will then pay you the ACV (minus your deductible, of course) and take ownership of the vehicle to sell it to a salvage buyer.

State Rules and Thresholds

One last wrinkle to be aware of is that your state’s laws can play a big role. While many insurance companies use the formula we just discussed, some states have specific regulations that force an insurer's hand.

This is called the Total Loss Threshold (TLT). A TLT is a percentage set by state law that dictates when a car must be declared totaled. For example, if your state has a 75% TLT, any vehicle with repair costs hitting 75% or more of its ACV is automatically a total loss by law.

Knowing how this all works is your best defense. It empowers you to navigate the claims process, ask the right questions, and make sure you're getting a fair shake.

How Insurance Companies Calculate Your Car's Value

When an insurer declares your car a total loss, everything boils down to one critical number: its Actual Cash Value (ACV). This isn't what you paid for the car or what you still owe on the loan. It’s what your vehicle was worth in the open market the moment before the crash happened.

Think of it like this: if you had put your car up for sale one minute before the accident, what would a reasonable buyer have paid for it? That's the number the insurance company is trying to pinpoint. This figure will determine the size of your settlement check.

The whole valuation process can feel a bit mysterious, but it’s not random. Let's pull back the curtain on how they come up with that number, so you can make sure you’re getting a fair shake.

The Key Factors in Vehicle Valuation

Adjusters don't just guess a number. They rely on sophisticated software and a specific set of data points to build a valuation report for your exact car.

These are the primary ingredients that go into the ACV recipe:

- Year, Make, and Model: The basic DNA of your car.

- Mileage: This is a big one. Fewer miles generally mean more value.

- Overall Condition: The adjuster assesses the pre-accident state of the interior, exterior, and mechanicals. They're looking for things like dents, rust, tire tread depth, and upholstery wear.

- Trim Level and Options: A loaded-up trim package with a sunroof, leather seats, or a premium sound system is worth more than a base model.

- Geographic Location: Where you live matters. A 4×4 truck is often worth more in Colorado than in Florida due to regional demand.

The insurance company plugs all this information into a system that then scours databases for recent sales of nearly identical vehicles in your local area. These "comparables" (or "comps") are the foundation of their settlement offer.

Understanding the Valuation Report

Most major insurance carriers don't do this valuation in-house. They outsource it to third-party companies, with one of the biggest names in the industry being CCC Intelligent Solutions. So, your settlement offer will almost certainly arrive with a detailed report from a service like this.

This report is the insurance company's evidence. It’s their official argument for why they are offering you a certain amount. It will list the "comparable" vehicles they used and show adjustments they made for differences in mileage, condition, and features.

It is absolutely crucial that you review this report carefully. Don't just skip to the final number and accept it. You're looking for errors or unfair comparisons that could be artificially lowering your car’s value. If you want to learn more about dissecting these documents, you can get a clearer picture of the total loss estimate process and what red flags to watch for.

Building Your Case for a Higher Value

Remember, the insurer's first offer is just that—an offer. It's the start of a negotiation, not the final word. If you believe it's too low, you have the right to challenge it, but you'll need to come prepared with your own evidence.

Here’s how to build a strong counterargument:

- Gather Your Maintenance Records: Can you prove the car was meticulously maintained? Regular oil changes, new brakes, and other service records show its mechanical condition was better than average.

- List Recent Upgrades: Did you just put $800 worth of new tires on it a month before the crash? Find the receipt. Same for a new battery, stereo, or any other significant investment.

- Find Your Own "Comps": This is your most powerful tool. Hit the online classifieds (AutoTrader, Cars.com, even Facebook Marketplace) and find at least three examples of your exact car for sale in your area. Look for similar mileage and options to prove the true local market value.

When you present the adjuster with cold, hard facts, you change the dynamic. You’re no longer just complaining about the offer; you're presenting a well-researched case that they have to take seriously.

Why Are So Many Cars Being Totaled These Days?

https://www.youtube.com/embed/Cpwd_7C3Fis

If it feels like cars are being written off for less and less damage, you’re not wrong. That minor fender-bender that would have been a straightforward fix a decade ago might now get your car a one-way ticket to the salvage yard. The threshold for what it takes to total a car is definitely getting lower.

This isn't a random fluke. It's the result of a perfect storm of advancing technology and shifting economics that has completely changed the math for insurance companies. The decision to total your car isn't just about the crumpled bumper you can see; it’s about the staggering, often hidden, costs that lie just beneath the surface.

Your Car Is a Computer on Wheels

By far, the biggest reason more cars are being totaled is the sheer complexity of modern vehicles. A new car is less a piece of machinery and more a rolling supercomputer, packed with sophisticated systems that make it safer and smarter but also incredibly expensive to repair.

Think about all the technology that can get knocked out in a minor collision:

- Advanced Driver-Assistance Systems (ADAS): All those helpful features like adaptive cruise control, blind-spot monitoring, and automatic emergency braking depend on a network of delicate sensors, cameras, and radar units. They’re often hidden in places like bumpers, side mirrors, and windshields—the exact spots that get hit in an accident.

- Integrated Screens and Electronics: The massive touchscreen in your dash isn't just a radio anymore. It’s connected to everything. Damage to one small part can mean replacing an entire, very expensive, electronic module.

- High-Tech Headlights: Gone are the days of a simple bulb swap. Modern LED or Matrix headlight assemblies can easily cost $2,000 or more to replace. For just one headlight.

And here’s the kicker: after these parts are replaced, they have to be perfectly recalibrated with specialized, high-tech equipment. This process alone can add hundreds, sometimes thousands, of dollars in labor to the final bill. Even a simple cracked windshield can turn into a four-figure repair if it has ADAS cameras that need to be re-aligned.

Supply Chain Headaches and a Technician Shortage

It’s not just the technology itself. The entire repair ecosystem is under pressure. We're still feeling the effects of global supply chain disruptions, which means getting the right parts can take weeks or even months. Those delays add up, especially when the insurer is paying for your rental car.

At the same time, there’s a real shortage of technicians who have the training to work on these complex modern vehicles. With fewer qualified experts, labor rates go up, adding yet another layer of cost to every single repair job. When parts are hard to get and skilled labor is expensive, the repair estimate climbs fast.

Industry data from early 2025 shows just how common this has become. A full 22.6% of all U.S. insurance claims now result in a total loss. And a huge part of the reason why is that over 31% of repair estimates now require some form of specialized ADAS recalibration. You can dive deeper into these auto insurance industry trends and their impact.

The Rollercoaster of Used Car Values

The final piece of this puzzle is the value of your car itself. The Actual Cash Value (ACV) is the magic number that a repair estimate is measured against. While used car prices shot through the roof for a while, they've started to cool off.

As a car's market value drops, it takes far less damage to push it over the total loss cliff.

Let's say your car is worth $20,000 and needs $12,000 in repairs. That's a 60% damage-to-value ratio, so it's probably worth fixing. But if that same car's value dips to $15,000 a year later, that same $12,000 repair bill suddenly represents an 80% ratio. Now, it's a clear-cut total loss. As used car prices soften, the number of total losses will almost certainly keep rising.

Your Options After a Total Loss Declaration

Once the insurance company officially declares your car a total loss, the ball is in your court. The initial shock starts to fade, and you're left with a practical decision to make. You essentially have two main paths to choose from, and each one comes with a very different set of financial and logistical consequences.

The route you take will determine the fate of your damaged vehicle and how you receive your settlement money. It’s a big decision, so let's walk through exactly what each choice entails.

Option 1: Accept The Settlement and Surrender The Vehicle

This is, by far, the most common and straightforward path. You simply agree to the final settlement amount, which is your car’s Actual Cash Value (ACV) minus your policy's deductible.

Once you accept the offer, you'll sign over the title, hand over the keys, and complete some final paperwork. In exchange, the insurance company gives you a check for the settlement amount. They then take ownership of your wrecked car and usually sell it for parts or scrap at a salvage auction to recover some of their payout.

This option offers a clean break. It’s the quickest way to get paid and start shopping for a new car without the headache of a mangled vehicle sitting in your driveway.

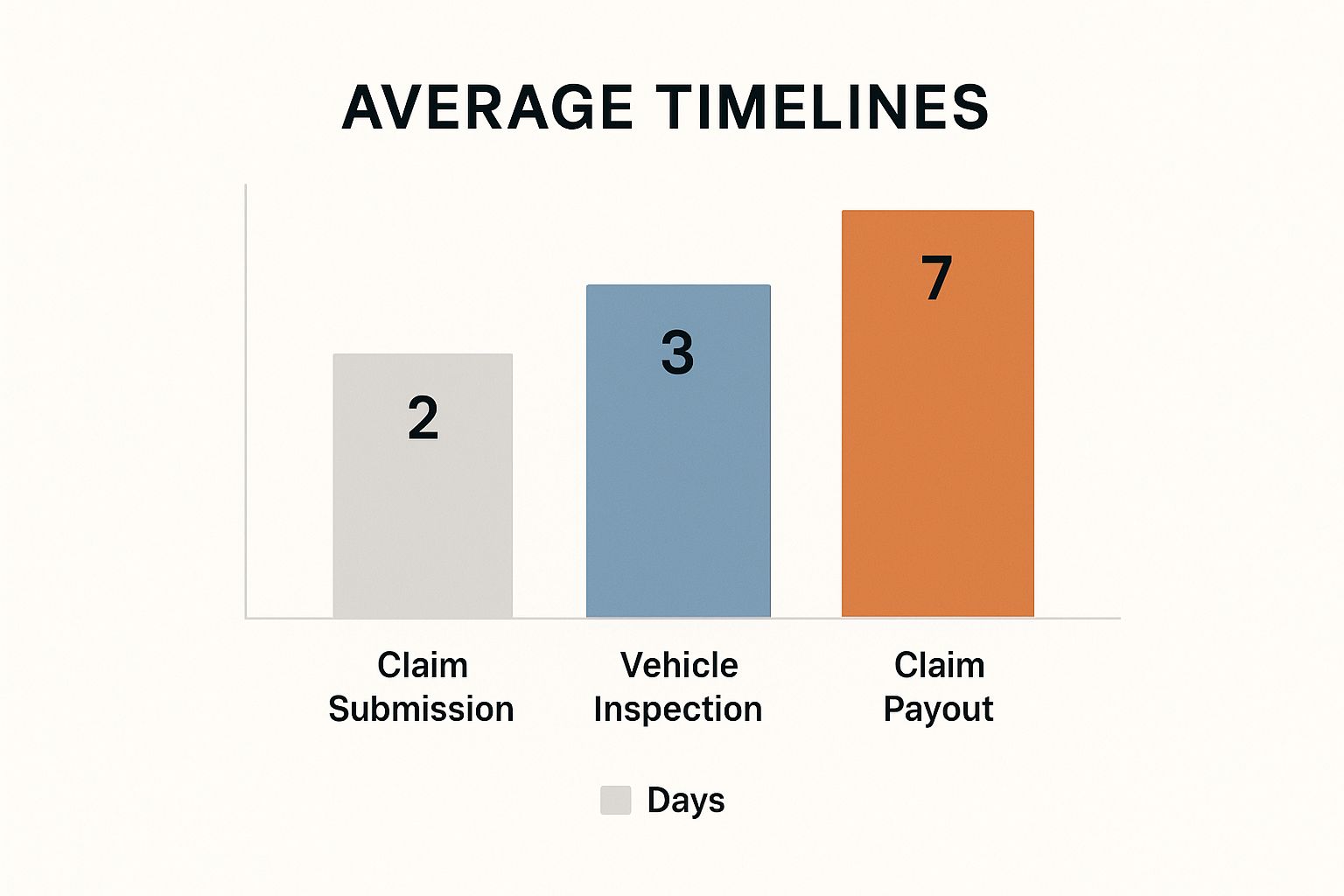

The timeline below gives you a good idea of how long the key stages of a claim take before you see that final payout.

As you can see, the whole process from filing the claim to getting paid usually wraps up in about two weeks, making it a pretty efficient way to move on.

Option 2: Keep The Car and Take a Reduced Payout

Your other choice is to keep the vehicle, a move the industry calls "owner retention." This path is much more complicated and is usually only a good idea for someone with serious mechanical skills or a deep sentimental attachment to their car.

If you choose to keep your totaled car, the insurance company changes how they calculate your payout.

Your payout becomes the car's Actual Cash Value (ACV), minus your deductible, and also minus the vehicle's salvage value. The salvage value is simply what the insurer expected to get for your car at auction.

Let's run the numbers. If your car's ACV is $10,000, your deductible is $500, and the salvage value is $2,000, your settlement check would only be $7,500. You get to keep the damaged car, but you're getting significantly less cash. If you're weighing this choice, our guide on what to do when your car is totaled can provide more detailed steps.

Choosing owner retention also means you're signing up for a whole new set of legal and logistical challenges:

- Salvage Title: Your local DMV will brand your car's title as "salvage" or "rebuilt." This is a permanent mark that tells every future buyer it was once a total loss, crushing its resale value.

- Mandatory Repairs: You can't legally drive the car until it's been repaired to meet strict state safety standards.

- State Inspection: After the repairs, the car has to pass a rigorous state inspection before it's considered roadworthy again.

- Insurance Headaches: Finding an insurance company willing to provide full coverage for a car with a salvage title is incredibly difficult. Most will only offer you the bare-minimum liability coverage.

This option isn't for everyone and requires a hard look at the costs, time, and effort involved.

Comparing Your Choices: Accepting The Settlement vs. Keeping The Car

To make the best decision for your situation, it helps to see the pros and cons of each option laid out side-by-side. This table breaks down the key differences in finances, effort, and long-term outcomes.

| Consideration | Accepting the Settlement | Keeping Your Totaled Car |

|---|---|---|

| Payout Amount | Full ACV (minus deductible) | ACV (minus deductible and salvage value) |

| Vehicle Ownership | You surrender the car to the insurance company | You keep the damaged car |

| Simplicity | Simple and fast process. Sign papers, get a check. | Complex process involving repairs, inspections, and DMV paperwork. |

| Future Costs | None. You use the settlement to buy a new car. | You are responsible for all repair costs to make it roadworthy. |

| Car Title | N/A (The insurer takes the title) | Receives a permanent "Salvage" or "Rebuilt" title. |

| Resale Value | N/A | Severely diminished due to the branded title. |

| Future Insurance | No issues; you're insuring a new vehicle. | Extremely difficult to get full coverage; liability is often the only option. |

| Best For… | Most people who want a clean break and cash for a new car. | DIY mechanics or those with a strong sentimental attachment. |

Ultimately, the right choice comes down to your personal finances, your mechanical ability, and how much time and effort you're willing to invest. For the vast majority of people, accepting the settlement is the most practical and financially sound decision.

How to Dispute an Unfair Settlement Offer

When the settlement offer for your totaled car lands in your inbox, it can feel like the end of a long, stressful road. But if that number makes your stomach drop, you need to know something crucial: the insurance company’s first offer is almost never their last.

Think of it as the opening bid in a negotiation, not a final verdict. You absolutely have the right to challenge an offer you believe is unfair. The key is to switch from being a passive victim of circumstance to an active, informed participant in determining what your car was really worth.

With a calm approach and solid proof, you can successfully argue for the money you're truly owed.

Step 1: Push Back with a Counteroffer

Before calling in the big guns, your first move is to present a well-documented counteroffer directly to the claims adjuster. This isn’t the time for an emotional appeal; this is business. You’re building a case to prove, with cold, hard data, that their valuation missed the mark.

Gather all the evidence you’ve collected. Your counteroffer should be built on:

- Real-World Comps: Find listings for 3 to 5 comparable vehicles for sale right in your area. You’re looking for the closest possible match in year, make, model, trim, and mileage.

- Proof of Upgrades: Did you just put on a brand-new set of tires? Upgrade the sound system? Find those receipts. Recent investments add real value.

- Maintenance History: A stack of service records is powerful. It proves your car was well-maintained and in better-than-average shape, which demands a higher value.

Package all of this into a polite but firm email. State the value you believe is fair, attach your proof, and make your case. More often than you’d think, a thoroughly researched counteroffer is all it takes to get the adjuster to come back with a better number. For a deep dive into this part of the process, our guide on how to negotiate a total loss settlement covers the most effective strategies.

Step 2: Bring in a Professional

What happens if the adjuster digs in their heels and refuses to budge? It’s time to bring in your own expert. You have the right to hire an independent auto appraiser to give you a second opinion.

This person works for you, not the insurance company. Their entire job is to determine the true, unbiased pre-accident value of your vehicle. They’ll do a deep dive, looking at your car's condition and researching the local market to produce a detailed report. This report is your new secret weapon.

An independent appraisal will typically cost between $300 and $600. It's an investment, but one that can easily pay for itself by adding thousands of dollars to your final settlement. A professional report from a certified appraiser carries serious weight and sends a clear message: you’re not backing down.

Handing this expert valuation to the adjuster changes the entire dynamic. Suddenly, they aren't just arguing with you anymore; they're arguing with another industry professional.

Step 3: Invoke the Appraisal Clause

So you’ve sent a counteroffer and a professional appraisal, but the insurance company still won't play ball. There's one more powerful tool at your disposal, and it's probably written right into your insurance policy: the Appraisal Clause.

Think of this clause as a built-in dispute resolution process, a sort of tie-breaker designed to settle valuation fights without going to court. When you invoke it, you force the issue into a structured, binding procedure.

Here’s a simple breakdown of how it works:

- You Hire an Appraiser: You choose and pay for your own certified, independent appraiser.

- They Hire an Appraiser: The insurance company does the same.

- The Appraisers Negotiate: The two experts present their cases to each other and try to agree on a fair value.

- An Umpire Decides: If they can't agree, the two appraisers select a neutral, third-party umpire. The umpire reviews everything and makes a final, binding decision. The cost for the umpire is usually split between you and the insurance company.

Invoking the Appraisal Clause takes the decision away from the adjuster and puts it in the hands of neutral experts. It’s an incredibly effective way to break a stalemate and make sure you get the fair settlement you deserve when your insurance totals your car.

Common Questions About Total Loss Claims

Even with a good grasp of the total loss process, a few nagging questions always seem to surface. The fine print in your policy and the unique details of your accident can leave you feeling a bit uncertain. Let's clear up the most common concerns people have when their car is totaled.

Think of this as your go-to FAQ. We’ll tackle everything from car loans to getting your sunglasses back, giving you the clarity you need to handle this situation with confidence.

What Happens If I Still Owe Money on My Car Loan?

This is easily one of the most stressful parts of a total loss. The hard truth is you're still responsible for the entire loan balance, even though the car is no longer driveable.

When the insurance company cuts the check, it won't be made out to you. It goes directly to your lienholder—the bank or finance company that holds your loan.

If the settlement amount is more than what you owe, the lender takes its cut, and you get the rest. But if you owe more on the car than its Actual Cash Value (ACV), you're what's known as "upside down" on your loan.

For example, let's say your settlement is $15,000, but you still have $17,000 left on your loan. You are still on the hook for that $2,000 difference. This is precisely where GAP (Guaranteed Asset Protection) insurance becomes a lifesaver, as it’s designed to cover that exact gap.

Can I Get My Personal Belongings From the Car?

Absolutely. Anything inside the car that isn't bolted down is your personal property. The insurance settlement doesn't cover your belongings, and you have every right to get them back before the insurer takes the vehicle.

You need to act fast, though. Once you agree to the settlement and prepare to sign over the title, the clock starts ticking. The insurance company will quickly arrange to have the car towed to a salvage yard, and retrieving your stuff after that point can be a real headache, if not impossible.

What to Grab Before They Tow It Away

- Personal Items: Don't forget sunglasses, phone chargers, important papers from the glove box, and anything else you keep in the car.

- License Plates: In most states, the plates belong to you, not the car. You'll need to either turn them in to the DMV or transfer them to your next vehicle.

- Toll Transponders: Grab your E-ZPass or any other toll device to avoid surprise bills in the mail.

Do a thorough sweep of the interior, trunk, and all the little storage compartments. You’d be surprised what you might leave behind.

How Long Does a Total Loss Settlement Take?

The timeline for a total loss claim can really vary depending on your insurance company and how quickly you get them the information they need. Still, there’s a general sequence of events you can expect.

All in, from the day of the accident to the day you get paid, the process usually takes about three to five weeks.

Here’s a rough breakdown of how that time is spent:

- Initial Claim and Inspection (3-7 days): After you report the accident, an adjuster will come out to inspect the vehicle and assess the damage.

- Total Loss Declaration (2-5 days): The adjuster's report goes back to the insurer, who then officially declares the vehicle a total loss.

- Valuation and Negotiation (7-14 days): This is often the longest step. The insurance company will present its ACV offer. If it feels low, this is when you'll negotiate.

- Paperwork and Payout (5-7 days): Once you agree on a settlement figure, you'll sign the title over. After they get the paperwork, the payment is usually sent out within a week.

Staying on top of your paperwork and responding quickly to the adjuster can definitely help speed things along.

What If the Other Driver Was at Fault?

If the accident was clearly someone else's fault, their liability insurance is on the hook for your car's ACV. This is called a "third-party claim," and it comes with one big perk.

The main advantage here is that you will not have to pay your deductible.

The downside? It can take a lot longer. The other driver’s insurance company has to conduct its own investigation and formally accept liability, which can drag the whole process out.

For that reason, you might want to consider another route: filing with your own insurance company through your collision coverage.

Using Your Own Coverage: When you file with your own insurer, they pay your settlement promptly (minus your deductible). Then, they go after the at-fault driver's insurance company for reimbursement in a process called subrogation. Once they get the money back, they refund your deductible to you. It's often the fastest way to get paid and get back on the road.

When your insurance company totals your car, their first offer is just that—an offer. If it feels unfair, you don’t have to take it. At Total Loss Northwest, we provide certified, independent auto appraisals that force insurers to look at real-world market data instead of their internal software. We fight to make sure you get the fair settlement you’re legally owed. If you're dealing with a lowball offer in Washington or Oregon, visit us at https://totallossnw.com to see how we can help.