When an insurance company talks about your car's Actual Cash Value (ACV), they're talking about what it was worth on the open market right before it was damaged. It's the real-world price a buyer would have realistically paid for your specific vehicle in its pre-accident state.

This isn't what you originally paid for the car, and it's definitely not what a brand-new one costs today. Instead, ACV accounts for all the life your car has lived—its age, the miles on the odometer, and any dings, scratches, or wear and tear it had.

Your Car's Actual Cash Value Explained

Getting a handle on your car's ACV is crucial, especially when you're in the middle of an insurance claim. If your vehicle is declared a total loss, the settlement offer you get from the insurer is built entirely around this number. Their goal is to compensate you for the exact value of the asset you lost—not to buy you a new replacement.

Think of it like a smartphone. The moment you unbox it, it’s worth the full retail price. A year later, it has a few scuffs, the battery doesn’t last quite as long, and a new model is already out. Its value has dropped. ACV is that lower, present-day value. You can dive deeper into the nuts and bolts of how insurers determine this figure at: https://totallossnw.com/what-is-actual-cash-value/

Depreciation and Market Factors

The biggest force driving down your car’s value is depreciation. It's the natural, unavoidable loss of value that happens over time. But depreciation doesn’t hit all cars equally; a lot depends on where you live and what you drive.

For instance, a car in the United States depreciates by an average of 32.36% in its first three years. Across the pond in the UK, that same car would lose value a bit faster, dropping by 38.72%. So, a $30,000 car might be valued at $20,292 in the US after three years, but only $18,384 in the UK.

Your vehicle's ACV also matters in other financial situations, like the auto loan pre-approval process. A higher, well-documented ACV can often lead to better loan terms because the lender sees it as a more valuable asset.

Key Takeaway: Actual Cash Value is what your car was worth moments before an accident. It is calculated by taking the replacement cost of a similar vehicle and subtracting depreciation for age, mileage, and condition.

To really understand ACV, it helps to see how it stacks up against other common types of insurance coverage. Not all policies are created equal, and the type of valuation you have makes a huge difference at claim time.

Insurance Valuation Types at a Glance

The table below breaks down the three main ways insurance companies value your vehicle. Knowing which one applies to your policy is key to managing your expectations.

| Valuation Type | What It Covers | Best For |

|---|---|---|

| Actual Cash Value (ACV) | Pays the market value of your car at the time of the loss, minus depreciation. | Standard on most auto policies; suitable for most used vehicles. |

| Replacement Cost Value (RCV) | Pays the cost to replace your totaled vehicle with a brand new, similar model. | Owners of brand-new cars who want full replacement coverage. |

| Agreed Value / Stated Value | Pays a pre-determined amount that you and the insurer agreed upon when the policy started. | Owners of classic, custom, or high-value specialty vehicles. |

As you can see, an "Agreed Value" policy offers the most predictability for a unique vehicle, while RCV is great for new car owners. ACV, however, is the default for the vast majority of drivers on the road.

The Core Factors That Determine a Car's ACV

Figuring out your car's actual cash value isn't some secret art; it's a straightforward assessment based on a handful of key factors. Think of it like putting together a puzzle—each piece helps form the final picture of what your car is worth right now. The biggest pieces of that puzzle are what we often call the "big three."

These are the pillars of any vehicle valuation and give us a starting point:

- Age: It's no surprise that the older a vehicle gets, the more it depreciates. Time takes its toll on materials, technology becomes obsolete, and shiny new models hit the showrooms, all pushing down the value of an older car.

- Mileage: The number on the odometer is a direct reflection of how much life the car has lived. Higher mileage means more wear and tear on everything from the engine to the suspension, which naturally lowers its ACV.

- Condition: This is all about the physical state of your car, inside and out. We're talking about the quality of the paint, the state of the body panels, the cleanliness of the interior, and even the tread on the tires.

But while these three factors create the foundation, they don't paint the complete picture. A few other critical details can really move the needle on that final number.

Beyond the Basics of Vehicle Valuation

To get a truly accurate ACV, you have to look past the obvious and dig into the car's specific story. An insurance adjuster won't just glance at the surface; they'll investigate the vehicle's entire history.

A major piece of this is the vehicle history report. A clean, one-owner history is the gold standard. On the flip side, a report showing several owners or, worse, previous accidents, will almost certainly drag the ACV down. Even minor fender-benders can create hesitation for a potential buyer, which directly impacts its market value.

Then you have the car's specific trim level and any optional features it came with from the factory.

Key Insight: A factory-installed sunroof, a high-end sound system, or advanced safety features all add real, provable value. Aftermarket modifications, however, rarely increase the ACV and can sometimes even hurt it.

Finally, where you live actually matters quite a bit. Demand for certain types of vehicles changes from one region to another. A convertible, for instance, will likely fetch a higher price in sunny Florida than in snowy Alaska. In contrast, a rugged 4×4 truck is worth a lot more in a place with tough winters.

Insurers pore over local sales data for comparable vehicles (known as "comps") to dial in the value based on these regional market trends. Every one of these elements plays a role in the complex equation of a fair valuation. Getting familiar with all the inputs can help you understand why different valuations might come back with different numbers, and digging into the actual cash value formula can shed even more light on the process.

How Depreciation Lowers Your Vehicle's Value

Depreciation is the single biggest factor chipping away at your car's Actual Cash Value. Think of it as an invisible clock that starts ticking the second you drive a new car off the lot. The value drop is steepest in the first couple of years, then thankfully, it starts to level off a bit.

But here's the thing: not all cars depreciate at the same speed. Some models are champions at holding their value, while others seem to shed worth like a golden retriever sheds fur. This difference is a huge piece of the puzzle when figuring out what your car is worth right now.

A tough, in-demand pickup truck, for example, might only lose a small percentage of its value each year. On the flip side, a discontinued sedan or a high-end luxury car with a reputation for pricey repairs could lose a massive chunk of its value in that same year. Brand reputation and reliability scores from outfits like Consumer Reports play a massive role here—cars known for going the distance tend to depreciate much more slowly.

Why Some Cars Lose Value Faster

Ultimately, depreciation comes down to what the market thinks your car is worth. It’s all about supply and demand. If a specific model is known for eye-watering repair bills, fewer people will want to buy it used, and that drives its resale price down.

On the other hand, a car celebrated for its stellar gas mileage and cheap maintenance will always have buyers lined up, which helps keep its value strong.

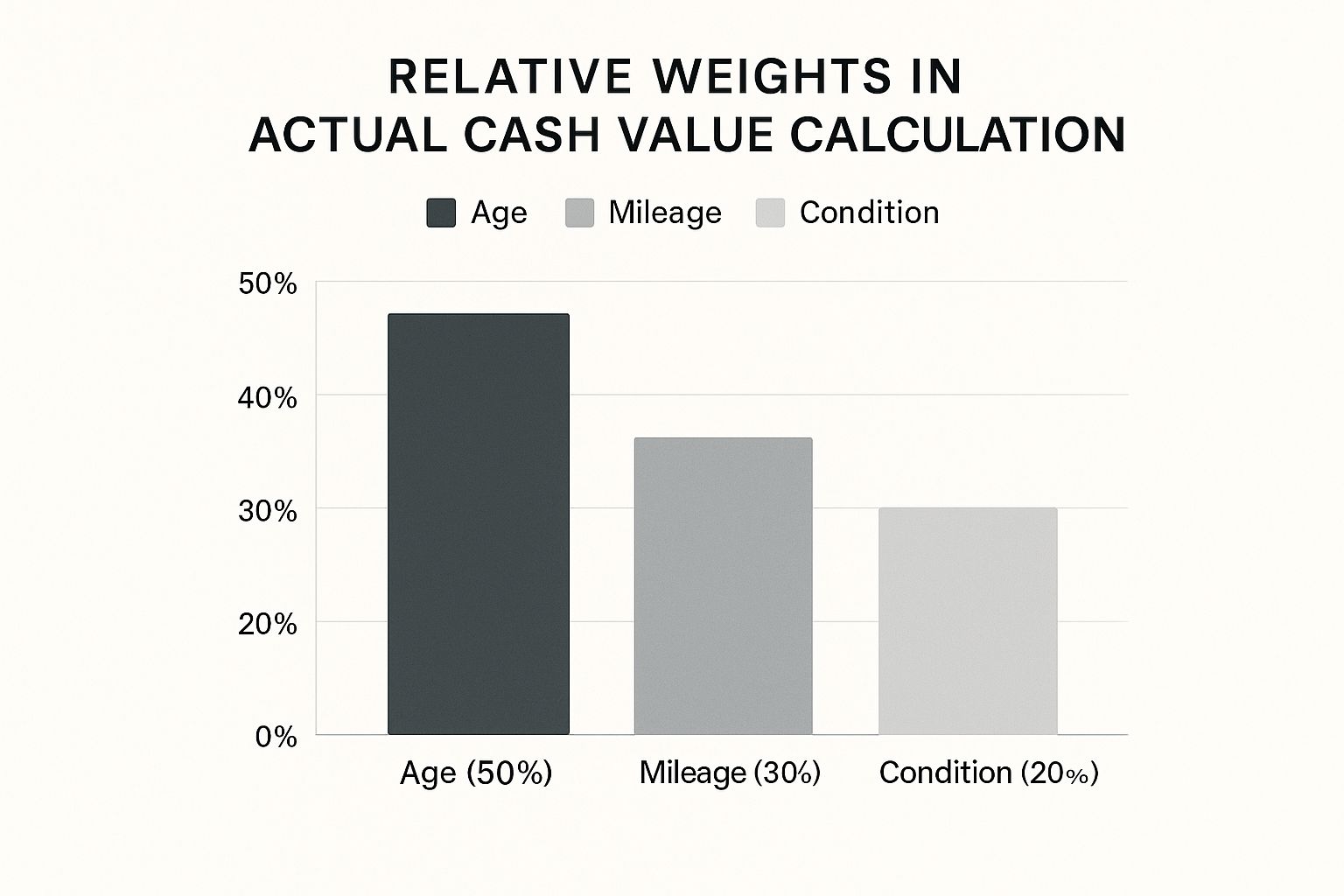

This chart breaks down the weight of the big three factors—age, mileage, and condition—that go into a typical ACV calculation.

As you can see, while mileage and condition are major players, the car's age is often the single most dominant factor pushing its value down over time.

Real-World Depreciation Examples

To really get a feel for how this works, let's look at some numbers. Certain types of vehicles are notorious for taking a huge hit early on. For example, some mainstream sedans can see their value plummet by around 50% from the original sticker price in just a few years. A car like the Volkswagen Passat has been known to lose about 40% of its value in its first year alone.

Luxury SUVs aren't immune, either. The Cadillac Escalade ESV can depreciate by roughly 50% early in its life, and the Infiniti QX80 often sees a similar drop. You can dive deeper into these trends and see how vehicles lose resale value with data from sources like Motus.com.

Key Takeaway: Depreciation is never one-size-fits-all. The make, model, and public demand for your specific car are the critical variables that dictate how quickly its ACV will fall.

At the end of the day, depreciation is a cocktail of age, wear-and-tear, and public perception. Once you understand how these forces work together, you'll be in a much better position to understand the ACV an insurer offers and argue why your well-maintained car might just be an exception to the rule.

Estimating Your Car's Actual Cash Value

So, how do you figure out your car's ACV before the adjuster even calls? It’s actually pretty straightforward, and knowing how the insurance company arrives at their number is your first and best line of defense. It gives you a solid baseline to work from and prepares you for the settlement negotiation.

Insurance companies don’t just pull a number out of thin air. They lean on sophisticated third-party data services that aggregate a mountain of sales data. These services zero in on recent sales of vehicles that are practically identical to yours—same make, model, year, and trim—right in your local area.

These matching vehicles are called "comparables," or "comps," and they are the foundation of any professional valuation. The adjuster will look at the final sale prices of these comps, not the asking prices you might see online, to calculate a fair market value for your car just before the incident.

Using Online Tools for Your Own Estimate

The good news is, you don't have to be in the dark. You can access many of the same types of tools the pros use to get a very reliable estimate of your own. Spending a few minutes on a few free online platforms can arm you with the data you need to have a productive, informed conversation with your insurer.

Some of the most well-known and trusted resources are:

- Kelley Blue Book (KBB): The household name for a reason. KBB gives you different values for trade-in, private party sale, and even what a dealer might ask for it.

- Edmunds: This site calculates a "True Market Value" (TMV®), which is designed to reflect what people are actually paying for cars like yours in your city.

- NADAguides: This is the guide many banks, credit unions, and dealerships use. It's considered an industry benchmark and provides straightforward value estimates.

To get a number that’s actually useful, you have to be completely honest about your car's condition. That means selecting the exact trim package, entering the correct mileage down to the last digit, and being upfront about every last scratch, dent, or weird noise the engine makes.

Expert Tip: Your honesty here is crucial. If you gloss over your car's flaws, you’ll get an inflated, unrealistic number that an adjuster's report will quickly poke holes in. An objective self-assessment gives you a figure you can actually stand behind.

Comparing Popular Online Car Valuation Tools

Not all valuation tools are created equal. Each one crunches data a little differently and focuses on a slightly different piece of the market. Getting estimates from a couple of them gives you a much richer, more complete picture of your car's real-world value.

Here's a quick look at the big three and what they do best.

Comparing Popular Online Car Valuation Tools

| Tool | Primary Use | Pros | Cons |

|---|---|---|---|

| Kelley Blue Book (KBB) | A great starting point for consumers looking at trade-in or private party prices. | Very user-friendly and widely recognized; provides multiple value scenarios. | Can sometimes run a bit higher than what cars actually sell for on the open market. |

| Edmunds | Calculating a "True Market Value" based on actual, recent sales in your area. | Backed by hard data; gives you a real-time pulse on your local market. | The website isn't quite as simple to navigate as KBB for newcomers. |

| NADAguides | The go-to valuation source for many lenders and financial institutions. | Seen as an industry standard; its numbers carry weight in official transactions. | Often provides more conservative (and sometimes lower) values than consumer sites. |

By gathering numbers from two or three of these services, you can establish a credible value range for your vehicle. This simple step is the most powerful thing you can do to make sure the settlement offer you receive truly reflects what your car's actual cash value is.

What to Do When You Disagree With an ACV Offer

Getting a settlement offer for your totaled car that feels like a lowball can be a real gut punch. It’s frustrating, but don't panic. The first number the insurance company throws out is just that—a first offer. It's a starting point for a negotiation, not the final say.

Your right is to question their math and push for a settlement that actually reflects what your vehicle was worth. The secret is to stay calm, be professional, and come prepared with solid evidence.

The very first thing you should do is ask the adjuster for a complete copy of their valuation report. This document is their playbook; it shows you exactly which "comparable" vehicles they used to land on their offer price. Go through it with a fine-tooth comb. Are the cars they listed really comparable to yours?

Building Your Counter-Offer

Now that you have their report, it’s time to build your own case. A strong counter-offer isn’t about what you feel your car was worth; it’s about what you can prove. Your mission is to use hard data to show them exactly where their valuation went wrong.

Here’s how you can tackle it:

-

Run Your Own Numbers: Start by using online valuation tools like KBB and Edmunds to establish a realistic value range for your car. This gives you an immediate sanity check.

-

Find Better Comps: Hop on local online marketplaces and dealer sites. Your goal is to find vehicles for sale that are a much closer match to your own in make, model, year, trim, mileage, and overall condition. Screenshot every single one.

-

Gather Your Proof: Dig up all your service records, receipts for recent work (like those new tires you just bought), and any documentation for factory upgrades or special features your car had.

Key Takeaway: An organized folder full of evidence is infinitely more powerful than an emotional phone call. Lay out all your findings in a clear email to the adjuster, explaining point-by-point why their offer is too low.

What if you've presented your case and the insurance adjuster still won't budge? You have another powerful tool at your disposal, likely written right into your policy: the appraisal clause.

Invoking this clause lets you hire your own certified, independent appraiser to conduct a fresh, unbiased valuation. This professional assessment often provides the final push needed to get a fair payout. You can learn more about how to navigate auto insurance appraisals to make sure you get every dollar you're entitled to.

Got Questions About Your Car's ACV? We've Got Answers.

When your car is totaled, the term "Actual Cash Value" suddenly becomes very important. It can also be incredibly confusing. Let's break down some of the most common questions people have when they're trying to figure out what their car is truly worth.

ACV vs. Replacement Cost

This is a big one. People often assume their insurance will pay for a brand-new car, but that's rarely the case unless you have a specific type of coverage.

Actual Cash Value (ACV) is the standard. It pays you what your car was worth the moment before the accident. Think of it as the market value of your vehicle, taking into account its age, mileage, and wear and tear. The payout is meant to be enough to buy a similar used car.

Replacement cost coverage is a different beast entirely. It's a premium add-on that pays enough to buy a brand-new model of your car, minus your deductible. It costs more for a reason, so it's crucial to know which policy you have to set the right expectations.

Do My Upgrades and Modifications Count?

It’s natural to wonder if the money you put into your car will be reflected in its ACV. The short answer? Probably not as much as you'd hope.

A factory-installed sunroof or a premium sound system might add a little value. But most aftermarket modifications—that custom wrap, the new rims, or the engine tune—often don't increase the ACV. Sometimes, they can even hurt it by making the car less appealing to the average buyer.

Pro Tip: Always keep receipts for any professional upgrades. While they won't revolutionize the valuation, solid documentation for high-quality, professionally installed equipment can give you a bit of leverage to argue for a slightly higher number.

Why Is the Insurance Offer So Much Lower Than Dealer Prices?

This is probably the most frustrating part of the process. You look up cars just like yours on a local dealer's lot and see them listed for thousands more than what your insurer is offering. What gives?

It all comes down to a difference in valuation. Car dealers list vehicles at retail prices. That price tag has to cover their overhead, the cost of reconditioning the car, and, of course, their profit.

Insurers don't use retail value. They base their ACV on the private-party value—what a regular person would reasonably pay another regular person for that same car. Their data comes from actual sale prices of similar vehicles, not the inflated asking prices you see on websites, which are almost always just a starting point for negotiation.

If you're staring at a lowball offer for your totaled vehicle, you don't have to accept it. At Total Loss Northwest, our certified independent appraisers are here to fight for the fair market value you're owed. We're experts at invoking the Appraisal Clause in your policy to ensure you get a fair shake. Learn how we can help you get a fair settlement.