So, how long does it actually take to get a car accident settlement? The honest answer is: it depends.

While some straightforward claims wrap up in just a few months, more complicated cases can easily stretch out for over a year. There's no one-size-fits-all timeline. The specifics of your crash, the severity of your injuries, and even the insurance companies you're dealing with will all play a huge role.

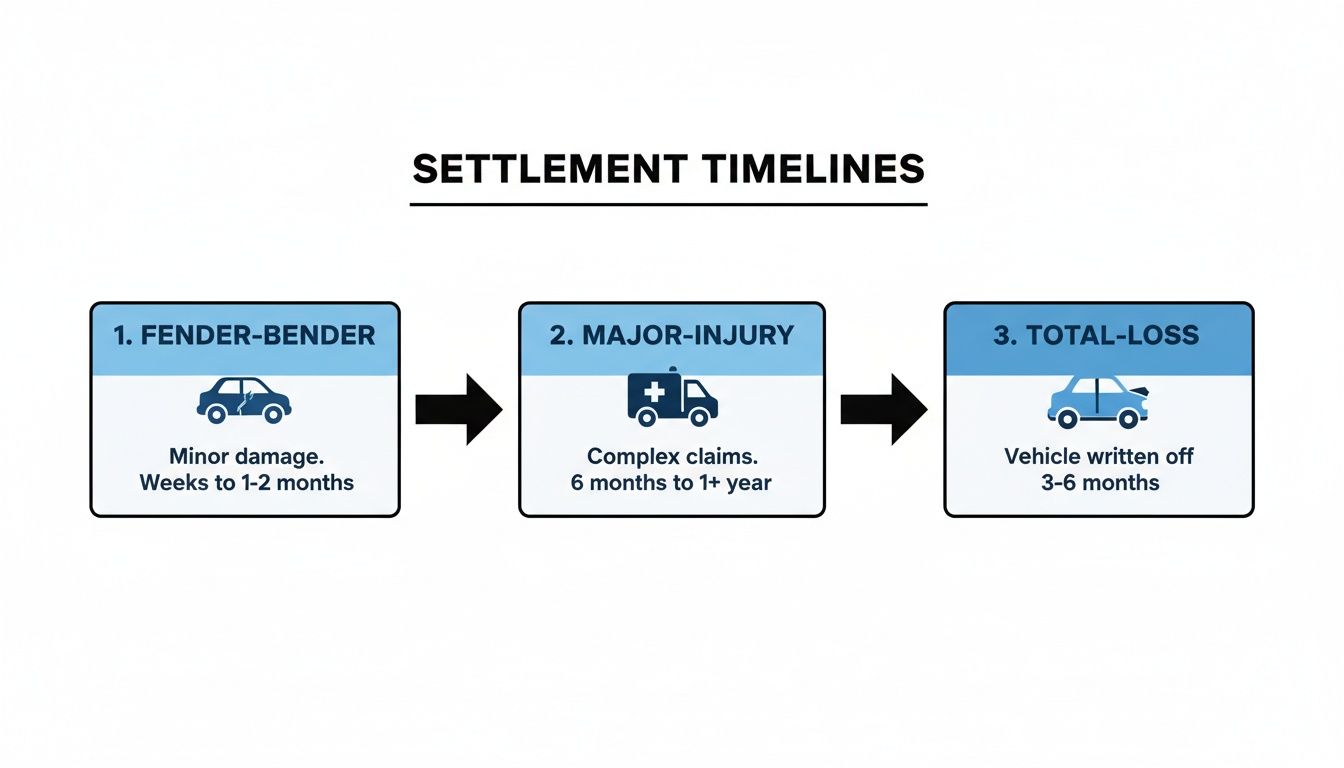

What Is a Realistic Car Accident Settlement Timeline?

Getting into an accident is jarring enough. The last thing you need is to be left in the dark about the settlement process, which can often feel confusing and drawn out. Think of this guide as your roadmap—it’s here to set clear, realistic expectations from the very beginning.

A minor fender-bender with a dented bumper and no injuries? That might get sorted out in a couple of months. But if you're dealing with serious injuries or your car is a total loss, the timeline naturally gets longer. For a deeper look at all the moving parts, this resource on how long it takes to settle a car accident claim in Texas is incredibly helpful.

Comparing Simple vs. Complex Claims

The single biggest factor dictating your settlement timeline is the complexity of your case. Knowing where your claim likely falls on the spectrum can help you mentally prepare for the road ahead.

The table below gives you a quick snapshot of what to expect based on common accident scenarios.

Estimated Settlement Timelines by Accident Complexity

This table provides a quick reference for settlement timelines based on the severity and complexity of the car accident.

| Accident Scenario | Typical Settlement Timeline |

|---|---|

| Minor Fender-Bender (Clear fault, vehicle damage only) | 1 to 3 months |

| Moderate Injuries (Whiplash, broken bones) | 6 to 12 months |

| Serious or Catastrophic Injuries (Disputes over liability) | 12+ months |

Let's break down what those timelines really mean.

H3: Minor Fender-Benders

- Timeline: 1–3 months

- These are the quickest claims to resolve. If everyone agrees on who was at fault and the only issue is fixing your car, the process is pretty straightforward. It’s mostly about getting a few repair quotes and having the insurance company cut a check.

H3: Claims with Moderate Injuries

- Timeline: 6–12 months

- This is where things start to slow down. If you’ve suffered injuries like whiplash or a broken arm, you can't even begin to talk settlement until you've reached what's called Maximum Medical Improvement (MMI). This is the point where you've healed as much as you're going to. Why wait? Because you need to know the full, final cost of your medical care before you can demand fair compensation.

H3: Serious Injury or Total Loss Cases

- Timeline: 12+ months

- When catastrophic injuries are involved or there's a major fight over your vehicle's value, you're in it for the long haul. These claims demand a mountain of paperwork, reports from medical experts, and intense back-and-forth negotiations with the insurer.

Here's the most important thing to remember: rushing to settle is almost always a mistake, especially if you're injured. If you accept a quick offer before understanding your long-term medical needs, you could be left paying for future treatments out of your own pocket. Patience is key to getting what you truly deserve.

The Four Main Stages of Every Car Accident Claim

Every car accident claim, no matter how big or small, tends to follow the same four-stage path. Getting a handle on this journey can take a lot of the mystery out of the process and give you a realistic idea of the average time for car accident settlement. It’s less of a straight line and more of a sequence of crucial milestones.

The clock really starts ticking the moment the crash happens, as the steps you take here lay the groundwork for everything else.

Stage 1: The Immediate Aftermath and Reporting

This first phase is all about acting quickly to preserve evidence and get the ball rolling. Right after an accident, the priority is always safety, but your next move should be gathering key information. That means snapping photos of the scene, getting contact details from any witnesses, and making sure a police report is filed.

This is also when you'll give your insurance company a heads-up, which officially kicks off your claim. This whole stage can be over in a few hours or might take a couple of days to wrap up.

Stage 2: Investigation and Medical Assessment

Once the claim is filed, the insurance adjuster steps in. Their job is to dig into the details of the accident to figure out who was at fault. They’ll pour over the police report, witness statements, and any photos you have.

At the same time, your focus needs to be on your health. It's critical to see a doctor and stick to the treatment plan they give you. This phase is often the longest and most unpredictable, stretching from weeks to months, especially if you have serious injuries. You can't really move forward until you've reached what's known as Maximum Medical Improvement (MMI)—the point where your doctor says you've recovered as much as you're going to.

As you can see, a simple fender-bender resolves much faster than a case involving major injuries or a totaled vehicle, which can easily add months to the timeline.

Stage 3: The Demand and Negotiation Dance

This is where things get serious. Once you’ve hit MMI and all your damages—medical bills, lost wages, vehicle repairs—have been tallied up, it’s time to negotiate. You or your lawyer will send a formal demand letter to the insurance company, laying out the full extent of your costs and arguing for compensation for your pain and suffering.

The adjuster will almost always come back with a lowball offer. Don't be surprised by this; it's just the opening move in a back-and-forth negotiation that can take anywhere from several weeks to a few months.

The negotiation stage is a strategic dance. The insurer’s goal is to minimize their payout, while your goal is to secure fair compensation. Having all your documentation in order is your strongest leverage.

Understanding the legal rules that govern these discussions is also key. For example, knowing the basics of Ontario's Car Accident Law can give you a much clearer picture of how these negotiations are framed.

Stage 4: Reaching a Resolution

The final stage is all about crossing the finish line. If negotiations go well, you’ll agree on a settlement amount, sign a release form (which officially closes the claim), and get your check. If the dispute is over your vehicle's value, you might need to use an appraisal clause in your policy.

But what if you can't agree? If you reach a stalemate, the next step is often filing a lawsuit. This moves the claim into the legal system and will dramatically extend the timeline, sometimes by years.

Key Factors That Can Drag Out Your Settlement

While every accident claim is different, a few common roadblocks can really stretch the average time for a car accident settlement. Think of the settlement process as a highway journey. These factors are the unexpected pileups and construction zones that can bring everything to a grinding halt. Knowing what they are is the first step to finding a way around them.

The most frequent holdup is a fight over fault. If the other driver's insurance company insists you were partly or even entirely to blame, the timeline gets longer right away. What could have been a simple claim becomes a messy debate that demands more evidence, witness interviews, and a whole lot of back-and-forth.

Where you live also makes a huge difference. In "at-fault" states, you have to prove the other driver was liable, but their insurer will almost always push back. This can force you to send a formal demand letter (adding 2-4 weeks), which then kicks off months of tense negotiations. If you have to file a lawsuit, you could be looking at another 9-18 months, if not more.

The Waiting Game for Medical Recovery

Honestly, one of the most critical delays is your own physical healing. You simply can't, and shouldn't, finalize a settlement until you've reached what's called Maximum Medical Improvement (MMI). This is the official point when your doctor says you've recovered as much as you're going to, and they can clearly outline any medical care you might need down the road.

Why is MMI such a big deal? Because settling before you hit that point is a huge gamble. You won't have a final tally of your medical bills, you won't know if you'll need future surgeries, and you won't have a full picture of long-term needs like physical therapy.

If you jump on an early offer, you could be stuck paying for all that future care yourself. This wait, while frustrating, is essential to make sure the final settlement number actually covers the true cost of your injuries—now and in the future.

An insurance adjuster's job is to close your claim for as little money as possible. Delay tactics are part of their playbook. They're hoping the financial pressure will wear you down and make you accept a lowball offer out of desperation.

Insurance Company Tactics and Valuation Disputes

Let's be clear: insurance companies are businesses, and their adjusters are trained negotiators. They have a whole arsenal of tactics designed to slow things down. A classic move is to throw out a ridiculously low initial offer that doesn't come close to covering your damages, forcing you into a drawn-out negotiation battle.

They also love to use their own biased software to undervalue your car, especially if it's a total loss or has lost value after repairs. When you're fighting over your vehicle's actual worth, it just adds another layer of conflict to resolve. Fighting for what your car was really worth is crucial, but it requires solid proof and takes time. Our guide on diminished value after a car accident shows you exactly how to push back against these low valuations.

These delays aren't just annoying; they're a calculated strategy. The longer the process drags on, the more likely you are to get tired and just accept less than you deserve. Being ready for these games is the key to standing your ground and getting a fair outcome.

How Total Loss and Diminished Value Claims Affect Your Timeline

Things get a lot more complicated when your car is declared a total loss or takes a serious hit to its resale value even after repairs. Suddenly, the process isn't just about covering a repair bill. You're now in a direct dispute with the insurance company over what your car was actually worth.

At the heart of these delays is a battle over the Actual Cash Value (ACV)—the fair market value of your vehicle moments before the accident. Insurance companies often lean on valuation software that tends to spit out lowball numbers. This creates a frustrating gap between their offer and what it would genuinely cost you to replace your car, and that disagreement is why these settlements can drag on for so long.

The Battle Over Your Vehicle's True Value

Let's say your well-maintained daily driver in Portland gets totaled. The insurance adjuster comes back with an offer for $12,000, citing a report from their go-to software. But you’ve done your homework, and similar models in your area are consistently selling for around $16,000. That $4,000 difference is where the fight begins, and it can easily add weeks or even months to your claim.

This problem gets even worse with unique or specialized vehicles.

- Classic Cars: A vintage car's value isn't just about its make and model; it’s about its condition, rarity, and provenance. Standard valuation tools completely miss this. An insurer might peg a classic Ford Mustang at $25,000, while a professional appraisal shows it's really worth $45,000 on the open market.

- High-Value Vehicles: For a luxury car in Washington, an accident can tank its resale price, a loss known as diminished value. Proving just how much value was lost requires a specialized report, and you can bet the insurance company will push back hard, stretching out the negotiations.

An insurer’s first offer on a total loss or diminished value claim is rarely their best. It's an opening bid in a negotiation they hope you'll be too tired to fight. Contesting their low valuation is not just your right—it's essential for a fair outcome.

Why These Claims Take Significantly Longer

The timeline for these claims is just naturally longer because the burden of proof falls on you. You have to prove a value that the insurance company has a strong financial incentive to downplay. It's a completely different ballgame than just submitting repair estimates. You’re essentially building a case to establish your vehicle's true market worth.

For a deeper look into the nuts and bolts, our guide on how a total loss car valuation is determined is a must-read.

With total loss claims, the timeline can really blow up if there's any dispute over fault (12-24 months) or if you need an independent appraisal to challenge the insurer's biased software. While the general average for a car accident settlement is about 10.7 months, claims involving diminished value—like a custom truck that loses 20-30% of its value after an accident—almost always take longer as you fight to be compensated for that real-world loss.

In the end, fighting for what you're rightfully owed is a critical part of the process. It's time-consuming, yes, but it’s the difference between accepting what they want to give you and getting the funds you actually need to be made whole.

Proactive Steps to Help Speed Up Your Settlement

While you can't control every single part of the claims process, you are far from powerless. Taking a proactive approach from the very beginning can shave off significant delays and stop the insurance company from dragging its feet. Your actions can directly influence the average time for a car accident settlement by helping you build a stronger, more organized case from day one.

Think of it like this: your claim is a construction project. If you don't have a solid blueprint and all your materials lined up, the build will be slow, messy, and full of problems. Meticulous documentation is your blueprint.

You can streamline everything by:

- Creating a Central File: Keep every single piece of paper—the police report, all medical bills, repair quotes, and every email—in one designated spot.

- Maintaining a Communication Log: Jot down the details of every single call and email with the adjuster, including the date, time, and a summary of what you talked about.

- Responding Promptly: When the insurer asks for information, get it back to them as quickly and accurately as you can. This prevents them from using "waiting on you" as an excuse for delays.

Taking Control of the Valuation Process

One of the biggest holdups is the endless back-and-forth over your vehicle’s value. Insurance companies often use this negotiation as a stalling tactic, knowing that the longer it takes, the more likely you are to accept a lowball offer out of sheer frustration. But there's a powerful tool written right into your policy to cut through this nonsense: the Appraisal Clause.

Invoking this clause brings in a certified, independent appraiser to determine your vehicle’s actual pre-accident market value. This isn't just someone's opinion; it's a professional valuation based on real-world data, not the insurance company’s self-serving software. Taking this single step can often bypass months of frustrating haggling.

"Don't let the insurer's stalling tactics cost you time and money. Invoking the Appraisal Clause early with a certified appraiser provides bulletproof market data that can slash delays and secure a fair settlement faster, often halving the negotiation timeline."

This proactive move forces a real, market-based valuation onto the table that is incredibly difficult for the insurer to argue against. In my experience, this is often the key that unlocks a much faster resolution.

Knowing How to Communicate Effectively

Clear, consistent communication is absolutely essential. While being proactive is great, it’s just as important to know what to say—and, more importantly, what not to say. Remember, insurance adjusters are professionally trained to use your own words against you to reduce your payout. Getting a firm handle on how to deal with insurance adjusters can keep you from making very costly mistakes during those calls.

By staying organized, using your policy’s appraisal rights, and communicating with purpose, you can take meaningful control over your claim’s timeline. You go from being a passive victim waiting for things to happen to the one driving the process forward toward a fair and timely resolution.

Common Questions About Settlement Timelines

When you're dealing with the fallout from a car accident, it's completely normal to wonder how long it's all going to take. The uncertainty can be one of the most stressful parts of the whole ordeal.

Let's walk through some of the questions we hear most often to give you a clearer picture of the road ahead.

How Long Is Too Long for a Settlement?

There's no magic number, but your gut feeling is probably right—some timelines are just too long and should set off alarm bells. If you have a simple, clear-cut claim where fault isn't in dispute, it shouldn't be dragging on past a year. For more serious accidents with major injuries, a claim pushing past the 18 to 24-month mark without any real, understandable progress is a big problem.

The real test isn't a date on the calendar; it's momentum. Are you getting regular updates, or just radio silence? Are the adjuster's reasons for the delay legitimate, or are you getting vague, circular excuses?

If communication has completely broken down and your claim feels like it’s stuck in neutral for no good reason, you might be dealing with bad faith insurance tactics. Unreasonable delays are a classic sign that it's time to get a professional involved to force the issue.

Does Hiring an Appraiser or Lawyer Slow Things Down?

This is a huge misconception. People often worry that bringing in help will just add more time to the process, but it's often the exact opposite. Insurance companies know that unrepresented individuals can get frustrated and are more likely to accept a lowball offer just to be done with it. Delay is a strategy they sometimes use.

When you hire an independent appraiser for your car, you're sending a clear signal: you know your rights and you have the facts on your side. A good appraiser can slash months off the negotiation by delivering a solid, market-based valuation that an insurer can't easily poke holes in. It often gets the property damage part of your claim settled much faster.

The same goes for a good attorney. They cut through the red tape, make sure every document is filed on time, and handle all the back-and-forth with the insurer, which can light a fire under a slow-moving adjuster.

Can I Get a Partial Payment During the Process?

Yes, this is definitely possible and sometimes a good option. For instance, the insurance company might agree to pay for your vehicle repairs or a rental car while you're still getting medical treatment for your injuries. This happens a lot when the property damage is straightforward but the full extent of your injuries isn't known yet.

A word of caution here: be incredibly careful with any paperwork you sign. Never, ever sign a document labeled "final payment" or "full and final release" without being 100% certain it only applies to one specific part of your claim (like just your car). Get it in writing that accepting payment for your vehicle does not in any way prevent you from pursuing your injury claim for medical bills, lost wages, or pain and suffering.

What if the Final Insurance Offer Is Still Too Low?

First and foremost, remember this: you never have to accept an offer that isn't fair. If you've negotiated and the insurance company’s "final" number is still way off, you aren't out of options. The next step is to circle back with a firm counter-offer that's backed by every piece of evidence you have.

Make sure your counter-offer includes:

- A complete file of your medical bills and treatment records.

- Clear documentation of any time you missed from work.

- A professional, independent appraisal report detailing your vehicle's true value.

If they still won't budge, you can invoke the Appraisal Clause in your insurance policy, which is a powerful tool for settling a dispute over your vehicle's value. For the claim as a whole, your next steps might be mediation or, if all else fails, filing a lawsuit. A lawsuit takes more time, of course, but sometimes it's the only way to make an insurer take your claim seriously and pay what you're rightfully owed.

Don't let an insurance company's lowball offer dictate your financial recovery. At Total Loss Northwest, our certified appraisers fight to get you the true market value for your vehicle. We provide the data-driven reports you need to challenge unfair valuations and secure a fair settlement, faster. Learn how we can help at https://totallossnw.com.