When your car is totaled, one term suddenly becomes the most important phrase in your insurance claim: auto insurance actual cash value (ACV). This is the number that determines how much your insurance company will pay you. It's supposed to represent the real-world market price of your vehicle the exact moment before the crash, after accounting for all the miles and wear and tear.

What Is Actual Cash Value in Auto Insurance?

Let's cut right to it. Think of your car’s actual cash value as what you could have reasonably sold it for right before it was damaged. It’s not the sticker price you paid years ago, and it's definitely not what a brand-new one costs today. It’s simply the fair market value of your specific used car.

This is a critical point because a standard auto policy isn't designed to buy you a new car; it's meant to compensate you for the value of the one you lost.

The Core Idea Behind ACV

Here’s a simple way to look at it. Say you bought a top-of-the-line laptop for $1,500 three years ago. Today, with newer models out and a bit of wear, you might only be able to sell it for $400. If it were stolen, an ACV-based policy would pay you that current $400 value, not the original $1,500.

Your auto insurance actual cash value works the exact same way. It's the replacement cost of a similar vehicle minus depreciation.

Key Takeaway: ACV is the foundation for any total loss claim. It’s supposed to reflect what your car was actually worth based on market data, mileage, and its condition just before the accident. The problem is, insurers often rely on valuation reports that can undervalue vehicles, potentially leaving you thousands of dollars short. You can explore more general auto insurance statistics and trends on III.org.

Why It Matters for Your Claim

Getting a handle on ACV is essential because it directly dictates the size of the check you'll get from the insurance company. Most people are shocked when the first offer comes in way lower than they expected. This often happens because the insurer's initial valuation might not have factored in your car's great condition, recent repairs, or valuable upgrades.

The physical damage portion of your policy—collision and comprehensive coverage—is almost always paid out on an ACV basis. This covers:

- Collision: Damage from a car accident, no matter who was at fault.

- Comprehensive: Things other than a crash, like theft, fire, hail, or a tree falling on your car.

Understanding what ACV really means is your first line of defense in making sure you get a fair settlement for your totaled car.

How Insurers Calculate Your Vehicle's Value

When an insurance company calculates your car’s auto insurance actual cash value, they aren’t just picking a number at random. It's a methodical, data-driven appraisal that weighs a handful of key factors to arrive at their settlement offer.

The process starts by establishing a baseline. Adjusters look at what similar cars have recently sold for in your local area. But that's just the beginning—from there, they start making adjustments based on your specific vehicle.

The Core Ingredients in the ACV Recipe

To come up with an initial number, insurers plug several critical data points into their valuation software. Knowing what they're looking at is the first step in figuring out if their assessment is fair.

The main factors that go into their calculation are:

- Year, Make, and Model: This sets the stage. A 2022 Honda CR-V obviously has a different starting value than a 2018 Ford F-150.

- Mileage: More miles mean less value. It's a simple rule. A car with 50,000 miles is worth a lot more than the exact same model with 150,000 miles on the odometer.

- Trim Level and Options: All those factory add-ons matter. A sunroof, a premium sound system, or advanced safety features all add to the car's value.

- Overall Condition: This is a big one. They assess all the pre-accident wear and tear—dents, scratches, interior stains, and even the condition of your tires.

- Location: Where you live makes a difference. Vehicle values can vary significantly by region due to local market demand and even weather-related wear.

Think of it like selling a house. Two homes on the same street might share a floor plan, but the one with the brand-new kitchen is going to command a higher price than the one with dated appliances. Your car is no different. You can dig deeper into the specific actual cash value formula insurers often use.

The Power of Depreciation

The single biggest factor that chips away at your vehicle's value is depreciation. It’s the unavoidable loss of value a car suffers over time from simple aging and use. This is the main reason an insurer's payout is almost always less than what you paid for the car in the first place.

Depreciation is steepest right at the beginning. In fact, most new vehicles lose 20-30% of their value in the very first year. This dramatic drop is why an ACV offer can feel so low, especially if your car was relatively new.

This harsh reality means that even a mint-condition, one-year-old car is worth substantially less than a brand-new one off the lot. Insurers use depreciation tables and sophisticated software to calculate this reduction precisely. Getting a handle on how these calculations work, including things like the impact of component replacement costs, gives you a much clearer picture of how an adjuster lands on a final number.

When you understand their playbook, you're in a much better position to spot a lowball offer and challenge a valuation that just doesn't seem right.

Here is the rewritten section, designed to sound completely human-written and natural.

Why Your First Settlement Offer Is Often Too Low

Getting that first settlement offer for your totaled car can feel like a punch to the gut. The number is almost always lower than you expected, and you're left wondering how you'll ever afford a replacement. But here’s something you need to remember: that first offer isn't the final word. It's the opening bid in a negotiation.

This lowball number doesn't necessarily mean your insurance company is trying to rip you off. More often, it’s just the output of an automated system that doesn't have the full story about your specific vehicle. Insurers lean heavily on valuation reports from third-party software, and those systems are notorious for getting the details wrong.

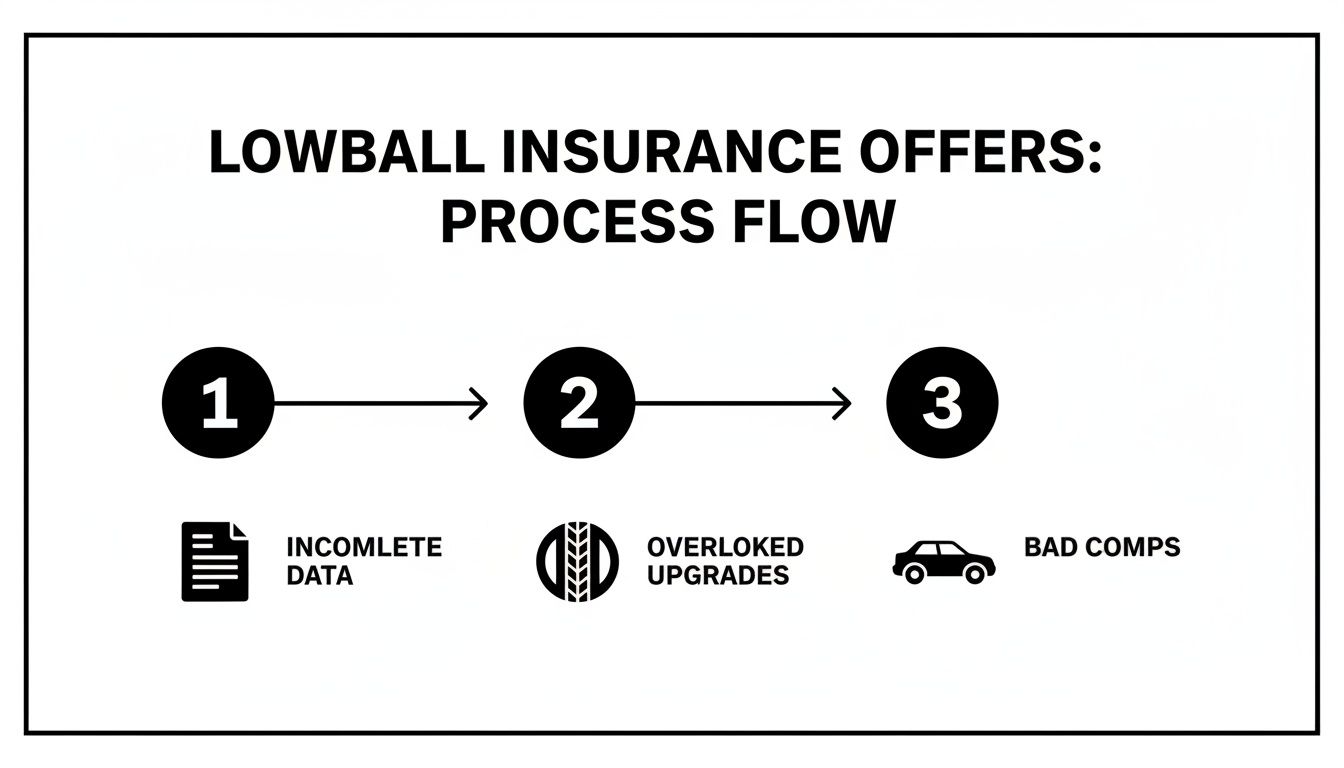

Inaccurate Data and Overlooked Details

The biggest culprit behind a low offer is simply incomplete or incorrect data. The software that spits out the valuation report might have pegged your car's condition incorrectly or missed key features entirely. These systems tend to default to an "average" or "fair" condition, completely ignoring the fact that you babied your car and kept it in pristine shape.

Think about it this way: the computer has no idea you dropped $1,200 on top-of-the-line tires last month. It doesn't know about the upgraded stereo you installed or that major service you just had done to keep the engine purring. It's up to you to fill in those blanks.

Some of the most common things these reports miss are:

- Recent Upgrades: Things like new tires, brakes, a battery, or even a recently replaced transmission.

- Condition Errors: Classifying your vehicle as “fair” when it was genuinely in “excellent” shape right before the crash.

- Missing Features: Forgetting to list a sunroof, leather seats, or that premium trim package you paid extra for.

In a total loss claim, everything comes down to the auto insurance actual cash value. The problem is, insurers' internal software can undervalue vehicles by 15-40% compared to what they’re actually selling for. This is a huge deal in a global market that's expected to hit $1,276.1 billion by 2035, as highlighted in research on the automobile insurance market by Fact.MR.

The Problem with "Comparable" Vehicles

Another huge issue is how they choose the "comparable" vehicles—or "comps"—to set your car's value. The report you get will list recent sales of supposedly similar cars in your area. The catch is, these comps are often not very comparable at all.

An adjuster might use a stripped-down base model as a comp for your fully-loaded, top-tier trim. Or they might pull comps from a different city where car values are lower, or even use examples with way more miles on the odometer than your car had.

Your job is to put on your detective hat and scrutinize these comps. Look for the mismatches. When you find them, you can push back with better, more accurate examples from your own local market. This is how you turn that initial frustration into a solid negotiation strategy.

Your Step-By-Step Guide to Disputing a Low Offer

Getting that lowball settlement offer can be frustrating, but it's not the end of the road. Think of it as the opening bid in a negotiation, not the final word. Don't ever feel pressured to take the first number they throw at you.

Instead, see this as your chance to build a strong case and fight for the fair auto insurance actual cash value you deserve. This isn't about getting into a heated argument; it’s a methodical process. If you stay organized and present clear, compelling evidence, you can successfully challenge the insurer’s math and get a much better outcome.

Start by Requesting the Valuation Report

First things first: ask the adjuster for a complete copy of their valuation report. This is the document they used to come up with their offer, and you have every right to see it. It will break down everything from the comparable vehicles they used to the adjustments they made for your car's condition.

Once you have that report, go through it with a fine-toothed comb. This is where you’ll find the cracks in their assessment. Look for simple mistakes like inaccurate mileage, listing the wrong trim package, or giving your car a lower condition rating than it deserved before the accident.

Build Your Counter-Offer with Solid Evidence

With their report in hand, it's time to gather your own proof. Your job is to build a case showing why their valuation is too low, using real-world market data to back it up. This isn't about what you feel your car was worth; it’s about what you can prove.

Your evidence file should include:

- Find Your Own Comps: Jump on auto listing sites and find vehicles for sale in your local area that are a genuine match for yours—same year, make, model, trim, and similar mileage. Screenshot everything.

- Document Your Car's Condition: Pull together all your service records, receipts for recent work, and any photos you have that show your car's great pre-accident condition. Put new tires on six months ago? Find that receipt.

- Get an Independent Opinion: Talk to a mechanic you trust. A written statement from them about the vehicle's condition and the value of recent maintenance can be incredibly powerful.

This is how you expose the common flaws in an insurer's valuation, which often boil down to incomplete data or just plain bad comps.

As you can see, low offers often come from the insurer overlooking recent upgrades or using poor-quality comparable vehicles to justify their number. Your documentation is the key to correcting this.

Invoke the Appraisal Clause

What if the adjuster won't budge? Your policy contains a powerful tool that most people don't even know exists: the Appraisal Clause. This provision gives you the right to hire your own certified, independent appraiser to determine your vehicle’s true value.

The Appraisal Clause is your ace in the hole. It forces the insurance company to consider a valuation from an unbiased, third-party expert, shifting the conversation away from their internal software and into the real world.

Typically, your appraiser and the insurer's appraiser will present their findings. If they still can't agree, they bring in a neutral "umpire" to make a final, binding decision.

Invoking this clause completely levels the playing field and ensures the final settlement is based on a fair market analysis. Once you've collected your evidence, you’ll want to present it all in a formal demand letter. To see how to put it all together, you can learn how to structure a strong insurance demand letter that makes your case impossible to ignore.

How an Independent Appraiser Can Maximize Your Payout

When your talks with the insurance adjuster stall out, it's easy to feel backed into a corner. But this is the exact moment an independent appraiser can become your most powerful asset. They are a certified professional you hire to provide an unbiased, real-world valuation of your vehicle, completely separate from the insurance company's interests.

Think about it: the insurer's adjuster works for them. An independent appraiser works for you. Their only job is to determine the true auto insurance actual cash value of your car using hard evidence and actual market data, not just whatever a generic software program spits out.

Going Beyond the Automated Report

The biggest difference comes down to the process. The insurance company's valuation often relies on automated data and "comparable" vehicles that might be hundreds of miles away or in worse condition. An independent appraiser, on the other hand, performs a hands-on, comprehensive market analysis.

Here’s what a real professional appraiser will do:

- Physically inspect your vehicle (or what's left of it) to get a true sense of its pre-accident condition, options, and unique features.

- Analyze your local market to find vehicles that are genuinely comparable and have sold recently, establishing a realistic baseline for its value.

- Account for all your documentation, including maintenance records, receipts for recent upgrades like new tires, and any custom work you’ve had done.

This methodical work results in a detailed, evidence-based report that carries serious weight when you go back to the negotiating table.

The Bottom Line: An independent appraisal isn't just a "second opinion." It’s a powerful tool that systematically breaks down the insurer's lowball offer by replacing their shaky data with a valuation grounded in reality.

The Power of an Unbiased Expert

Hiring an expert does more than just give you a new number—it changes the entire dynamic of your claim. The appraiser sees things the insurance company’s software will miss. They understand how local demand for your specific model, a premium trim package, or a history of meticulous maintenance adds real, tangible value.

This is why invoking the "Appraisal Clause" in your policy can be so effective. It forces the issue, taking the final decision away from the insurance company and placing it in the hands of qualified, neutral experts. The process is designed to ensure the settlement is based on a fair and thorough assessment.

Ultimately, an independent appraiser’s report gives you the leverage needed to get a payout that reflects what your vehicle was actually worth just before the accident. If you're fighting a low offer, it's worth looking into finding a certified independent auto appraiser near me to help your case. It’s a single step that can make a huge difference in the size of your final settlement check.

Got Questions About Actual Cash Value? We've Got Answers.

When your car is declared a total loss, "actual cash value" suddenly becomes the most important phrase in your vocabulary. It's also one of the most confusing. Let's break down some of the most common questions people have when they're staring down an insurance settlement.

Getting a handle on these details is the first step to making sure you're treated fairly.

Can I Actually Negotiate My Car's ACV?

Yes, you can. In fact, you absolutely should. The insurance company's first offer is just that—an offer. It's a starting point for a negotiation, not the final word. You have every right to see their full valuation report and point out anything that's wrong.

If their offer feels low, it's on you to prove it. Dig up receipts for that new set of tires or the sound system you installed. Find listings for comparable cars for sale right in your area—not 500 miles away. Document everything that made your car better than average. If you and the adjuster can't agree, invoking the Appraisal Clause in your policy is your next best move.

What's the Real Difference: Actual Cash Value vs. Replacement Cost?

This is a big one, and the distinction is crucial because it directly impacts your payout. They are two completely different ways of looking at your car's value.

-

Actual Cash Value (ACV): This is what your car was worth in the used car market the second before the accident. Think of it this way: what could you have reasonably sold it for? It’s calculated by finding the cost of a similar used car and then subtracting value for its age, mileage, and general wear and tear. Nearly all standard auto policies use ACV.

-

Replacement Cost Value (RCV): This type of coverage pays you enough to buy a brand-new version of your car. Because it ignores depreciation, RCV is much more expensive and pretty rare for auto insurance.

The Bottom Line: Most of us have ACV policies. That’s why the settlement check is almost never enough to walk into a dealership and buy a new car. The insurance is designed to pay you for the used car you lost, not upgrade you to a new one.

Does My Loan Balance Change the ACV?

Not one bit. Your car loan is a separate financial deal between you and your lender. It has absolutely no bearing on what the vehicle itself is worth on the open market. The insurance company's job is simply to pay you for the car's value, regardless of what you owe on it.

This is exactly where people get into financial trouble. If you owe more on your loan than the car's ACV—a situation often called being "upside down"—you are still on the hook for that difference. This is precisely the problem that GAP (Guaranteed Asset Protection) insurance was created to solve.

What About My Classic or Custom Car?

Standard insurance software is flat-out terrible at valuing unique vehicles. The programs adjusters use are built for common, everyday cars like Honda Civics and Ford F-150s. They will almost always undervalue a classic, collector, or heavily modified car—often by a shocking amount.

For these kinds of special vehicles, a standard ACV offer won't even be in the right ballpark. While the best-case scenario is having an "agreed value" policy from the start, it's not the end of the road if you don't. You'll need to hire an independent appraiser who lives and breathes classic or custom cars. It’s not just a suggestion; it's the only way to prove your car's true worth.

If you're dealing with a lowball offer on your totaled car, don't just accept it. Total Loss Northwest provides certified, independent auto appraisals that force insurers to look at real-world market data. We'll invoke the Appraisal Clause for you to make sure you get the fair settlement you deserve. Get an expert on your side by visiting us at Total Loss Northwest.