For many drivers, especially those financing a new car, gap insurance isn't just an add-on; it's a financial lifeline. The answer to whether it's worth it is often a resounding yes. Think of it as an inexpensive safety net that can save you from a multi-thousand-dollar headache if your car is ever totaled.

What Is Gap Insurance and Why You Might Need It

You know that amazing feeling of driving a brand-new car off the lot? Unfortunately, a harsh financial reality tags along for the ride: depreciation. The second your new tires hit the pavement, your car's value starts to plummet. This instant drop in value is the very reason gap insurance exists.

It all boils down to two key numbers. First, there's the amount you still owe on your auto loan. Second, there's your car's actual cash value (ACV), which is what it's worth right now, not what you paid for it. For the first few years of most car loans, what you owe is almost always higher than what the car is worth.

The difference between what you owe on the loan and what your car's ACV is—that's the "gap." If your car is totaled, your standard auto insurance policy only pays out the ACV, leaving you to cover that gap yourself.

The Financial Risk of Depreciation

This isn't just a tiny crack you can step over; it's a deep financial hole. When your insurance company declares your car a total loss, they cut you a check for its current market value, factoring in all that depreciation.

Let's say you still owe $25,000 on your loan, but your car's ACV is only $20,000 after an accident. Your insurance payout will leave you with a $5,000 bill for a car you can't even drive anymore. This is where gap insurance swoops in to save the day, as it's designed specifically to pay off that remaining loan balance.

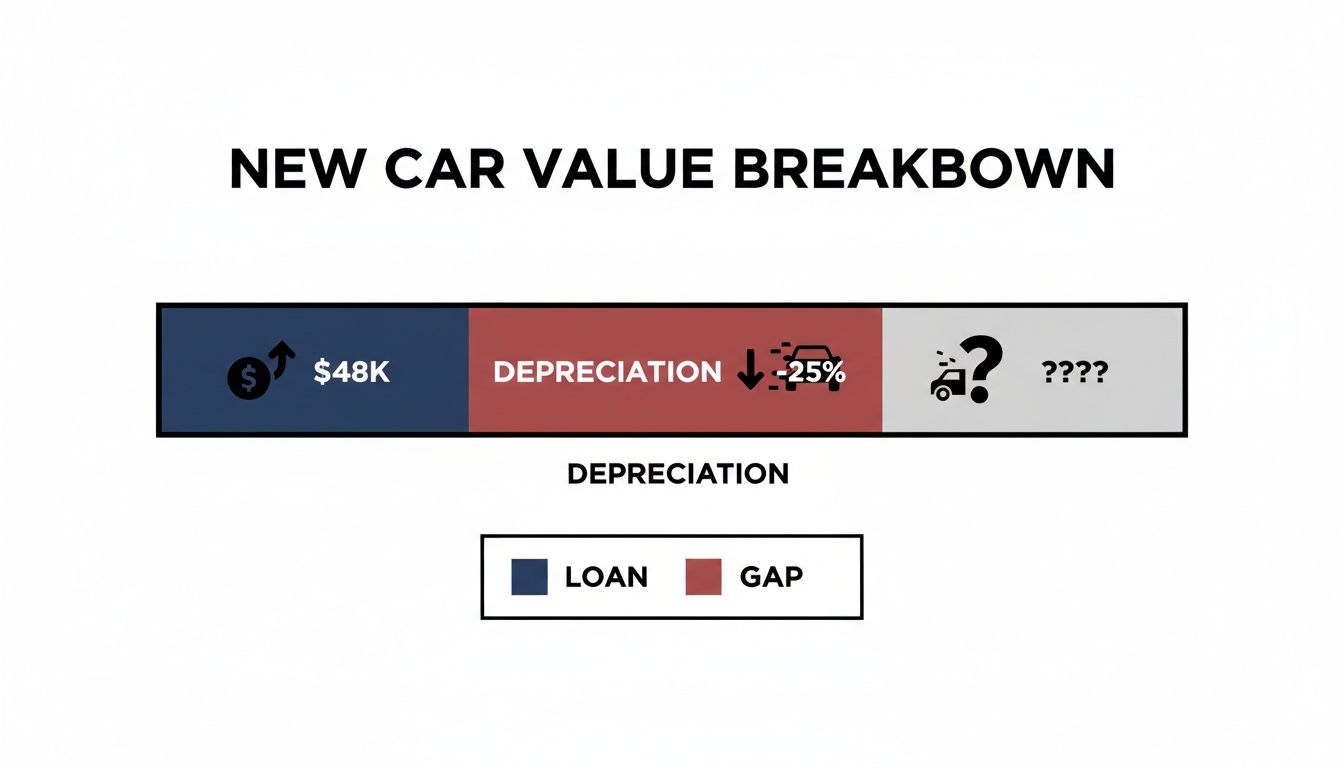

And this situation is more common than you'd think. With new car prices recently averaging around $48,000, aggressive depreciation can wipe out 20-30% of a vehicle's value in the first year alone. Data from the Guaranteed Auto Protection insurance market shows that roughly 25% of all insured vehicles involved in a total loss are financed or leased, putting those owners squarely in this risky position. This protection is especially crucial if you have:

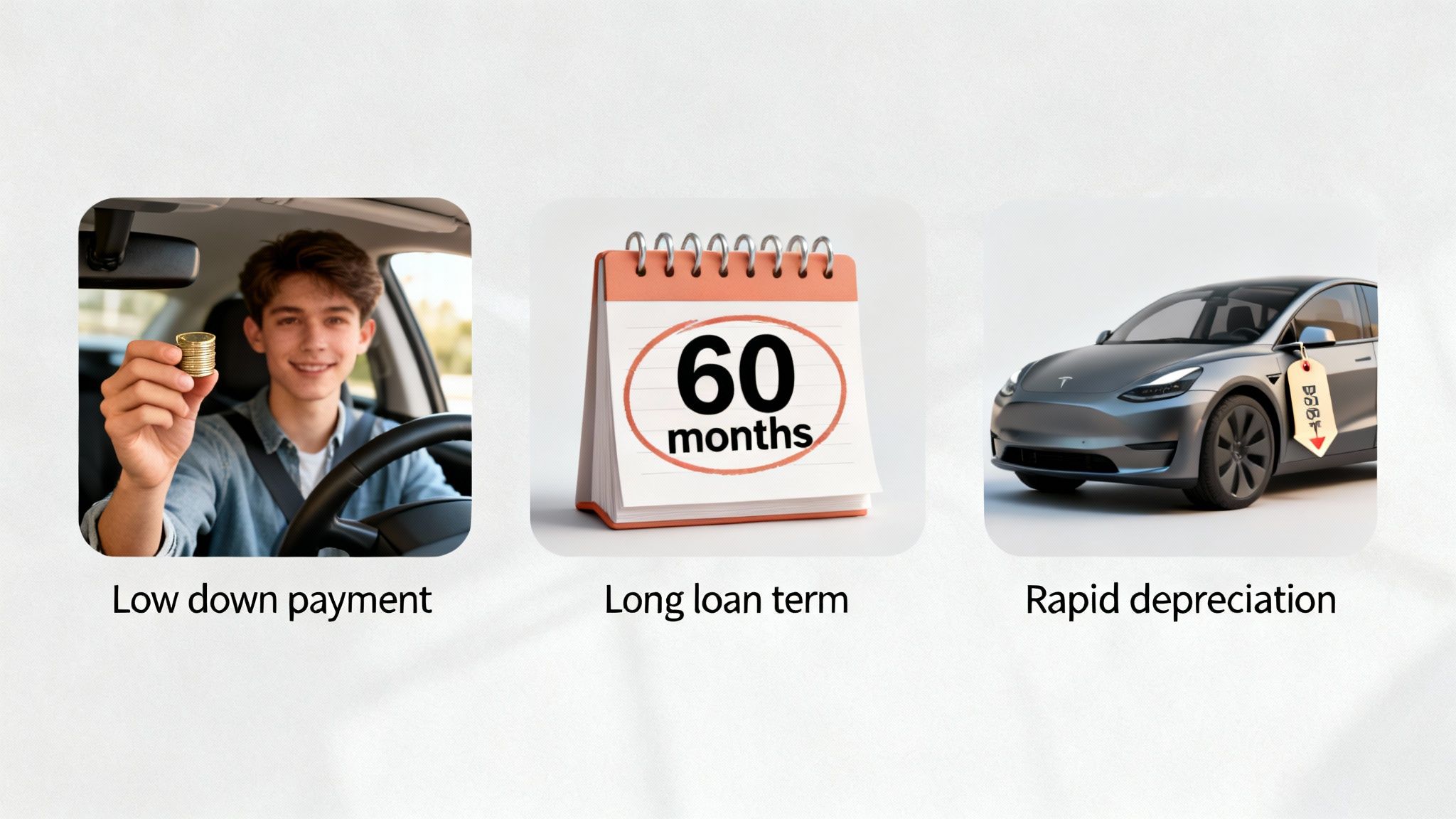

- A Small Down Payment: Putting less than 20% down on a new car almost guarantees you'll be "upside down" from the start.

- A Long Loan Term: Spreading payments over 60 months or more means your loan balance shrinks much more slowly than your car's value.

- Rolled-Over Debt: If you traded in a car that had negative equity, that old debt gets tacked onto your new loan, inflating it from day one.

Quick Guide to Deciding If Gap Insurance Is Worth It

Still on the fence? This table gives you a quick snapshot to help you see if your financial situation makes you a prime candidate for gap insurance.

| You Should Strongly Consider Gap Insurance If… | Why It Creates a Financial Risk |

|---|---|

| Your down payment was less than 20% | A small down payment means you owe much more than the car is worth immediately. |

| Your auto loan term is 60 months or longer | Your loan balance will decrease very slowly, while depreciation happens quickly. |

| You rolled negative equity from a trade-in | You started your new loan already "upside down" by owing more than the car's price. |

| You drive more than 15,000 miles per year | High mileage accelerates depreciation, widening the gap between value and loan balance. |

| You bought a vehicle that depreciates quickly | Luxury cars and certain models lose value faster, creating a bigger potential gap. |

| You are leasing your vehicle | Most lease agreements actually require you to carry gap insurance. |

Ultimately, the table highlights common scenarios where the "gap" between your loan balance and your car's value is likely to be significant. If you check off one or more of these boxes, gap insurance is probably a smart move.

How Vehicle Depreciation Creates a Financial Gap

So, to really get a handle on gap insurance, we need to talk about the one thing that makes it necessary in the first place: depreciation. It's a fancy word for a simple, brutal fact—your brand-new car starts losing value the second you drive it home. This isn't a slow process; it's immediate and steep, and it's the root cause of a major financial risk.

Let's put some real numbers to this. Picture yourself buying a new car for $40,000. You want to keep the monthly payments low, so you put down $2,000 and finance the rest over a 72-month (6-year) term. That leaves you with a $38,000 loan. You're thrilled with your new ride, but behind the scenes, its value is already plummeting.

In that first year alone, it’s not uncommon for a new car to lose 20% of its value, sometimes more. At the same time, your loan balance barely budges. Why? Because in the early days of a loan, most of your payment is just covering interest, not paying down the actual amount you borrowed.

An 18-Month Total Loss Scenario

Now, let's jump forward a year and a half. You've been making every payment on time, but then the worst happens—an accident totals your car. This is where the rubber meets the road, financially speaking.

Here’s what your situation looks like:

- Original Loan Amount: $38,000

- Loan Balance After 18 Months: Roughly $30,500

Next, we figure out what the car is actually worth. After 18 months, that shiny $40,000 vehicle has depreciated quite a bit. Its Actual Cash Value (ACV)—what it’s worth right before the crash—might only be around $28,000.

This is the moment of truth. Your auto insurer is going to cut you a check for the car's ACV, which is $28,000. After they subtract your $1,000 deductible, you’re left with a $27,000 payout.

See the problem?

- You Still Owe: $30,500

- Insurance Payout: $27,000

- The Financial Gap: $3,500

Even though your car is gone, you are still on the hook for that remaining $3,500. Without gap insurance, that money has to come straight from your savings. You’re left with no car and a hefty bill for something you can't even drive anymore.

This is exactly what people mean when they talk about being "upside down" or "underwater" on their car loan.

The infographic above really drives the point home. Your loan balance goes down slowly and predictably, but the car's value drops off a cliff. That space between the two lines is the financial gap—the exact risk gap insurance is built to cover.

Why Your Insurer’s ACV Matters

Everything in this equation hinges on the Actual Cash Value your insurance company assigns to your totaled car. If they come in with a lowball valuation, that gap gets wider, and your out-of-pocket cost gets bigger.

That’s why it’s so important to understand what is actual cash value of my car and how it’s determined. In our scenario, every dollar the insurer undervalues your car is another dollar you're stuck paying back to the bank.

Who Really Needs Gap Insurance? Here's Who Benefits Most

Gap insurance isn't for everyone, but for some drivers, it's a financial lifesaver. Certain situations almost guarantee you'll be "upside down" on your car loan, owing more than the car is actually worth. If you see yourself in any of the scenarios below, gap insurance shifts from a "maybe" to a "must-have."

Think of it this way: you're in a race. On one side, you have your loan balance slowly ticking down. On the other, you have your car's value dropping like a rock. If your car’s value is winning the race to the bottom, that’s when you're at risk.

Drivers with Small Down Payments

This is the big one. If you make a down payment of less than 20%, you’re starting the loan already in a vulnerable position. With very little money down, your loan amount is almost the full price of the car, but its value plummets the moment you drive it off the lot. That creates an immediate, and sometimes massive, gap.

Let's say you buy a $35,000 car and only put 5% down ($1,750). You’re now financing $33,250. If that car loses 10% of its value ($3,500) in the first month alone, you already owe $1,750 more than it's worth. A total loss at that point would be a financial nightmare without gap coverage.

The gap insurance market is booming for a reason. Valued at USD 4.25 billion in 2024, it's expected to hit USD 11.78 billion by 2033. This isn't surprising when you see car prices and loan terms getting higher, making it harder for people to keep up with depreciation. You can read more about these global GAP insurance market trends.

Car Buyers with Long Loan Terms

Stretching a car loan out to 60, 72, or even 84 months is another major red flag. Sure, it makes the monthly payment more manageable, but it also means your loan balance shrinks at a snail's pace. For the first few years, most of your payment is just covering interest, barely touching the principal.

This slow-motion payoff schedule simply can't compete with how fast a car loses value. The gap between what you owe and what the car is worth can stay wide open for years. You might be three years into a 72-month loan and find you still owe more than the car's market value. A shorter loan, like 48 months, helps you build equity much faster and often eliminates the need for gap insurance altogether.

Owners of Rapidly Depreciating Vehicles

Let's be honest: not all cars are created equal when it comes to holding their value. Some vehicles, particularly certain luxury sedans and models with a poor resale reputation, depreciate far more quickly than others. If you’ve got your eye on one of these, you’re at a higher risk of being upside down, even if you made a decent down payment.

Do your homework before you sign the papers. A quick search on your desired model’s depreciation rate can tell you a lot. If you learn it's known for dropping in value quickly, gap insurance acts as a vital financial backstop. It’s also a good idea to understand how much your totaled car is worth to see just how low an insurance payout could be, making that gap even wider.

When Can You Safely Skip Gap Insurance?

While gap insurance can be a real financial lifesaver for many drivers, it's definitely not for everyone. In some cases, buying it is like paying for an umbrella on a perfectly sunny day—it's an extra cost for protection you just don't need. Knowing when to pass on it is just as crucial as knowing when to buy it.

The whole decision boils down to one simple question: do you owe more on your car than it's actually worth? If your loan balance is less than your car's actual cash value (ACV), you're in a good spot. This means if your car were totaled, your standard insurance check would be more than enough to pay off the loan. You might even have some cash left over.

So, when does that happen? Here are a few common scenarios where you can confidently skip the gap coverage.

You Made a Large Down Payment

Putting a hefty chunk of cash down upfront is one of the fastest ways to make gap insurance irrelevant. A down payment of 20% or more immediately builds a solid equity buffer between your car's value and your loan amount.

Think about it: if you buy a $30,000 car and put down $6,000 (20%), you're only financing $24,000. Even with that initial drop in value the moment you drive off the lot, the car is almost certainly still worth more than what you owe. That initial equity means a "gap" is highly unlikely to ever open up.

Your Loan Term Is Short

Opting for a shorter loan term—say, 48 months or less—is another smart move. Why? Because with a shorter loan, more of each payment attacks the principal balance instead of just chipping away at interest. You build equity much, much faster.

It's like a race between your loan balance and your car's depreciation. With a short-term loan, your balance shrinks so quickly that your car's value simply can't drop fast enough to create a gap.

You Purchased a Used Car

Buying a vehicle that's already a few years old often means you can skip gap insurance altogether. New cars take their biggest depreciation hit in the first one to three years. When you buy used, you're letting the original owner take that massive financial blow.

Your loan is starting much closer to the car's stabilized value, making the risk of becoming "upside down" significantly lower from day one.

Finding Your Breakeven Point: This is the magic moment when your loan balance finally dips below your car's actual cash value. Once you reach this point, gap insurance is no longer doing anything for you. Keep an eye on your loan statement and check your car's current value on a site like Kelley Blue Book. The second you're "right-side up," it's time to call your provider and cancel the policy.

Where to Buy Gap Insurance and How to Get the Best Price

Alright, you've decided gap insurance might be a smart move. So, where do you actually get it? This is where a little bit of shopping can save you a whole lot of money. You generally have three places to turn, and the difference in what you'll pay between them can be shocking.

The first time you'll likely hear about gap insurance is from the finance manager at the car dealership as you're signing stacks of paperwork. They make it incredibly easy to say yes, but that convenience comes at a steep price.

Dealerships typically sell gap insurance as a single, lump-sum product. You'll see a flat fee, often ranging from $500 to $700, tacked onto your final bill. The real kicker? They usually roll that cost right into your auto loan. That means you’re not just paying for the coverage—you’re paying interest on it for years, making an already expensive option even pricier.

Comparing Your Options

A far better route is to get gap coverage straight from your auto insurance company. Most major insurers offer it as a simple endorsement—an add-on—to your existing comprehensive and collision policy. This is almost always the cheapest way to go, typically adding only $60 per year to your premium. That's a massive difference.

You might also be able to buy coverage from the third-party lender that’s financing your car, like your local credit union or bank. Their rates can be more competitive than the dealership's, but it’s still crucial to see how they stack up against your auto insurer's offer.

The takeaway here is simple: never take the first offer. The convenience of buying at the dealership is tempting, but a couple of quick phone calls to your insurer and lender can get you the exact same protection for a fraction of the cost.

Getting the Best Price for Gap Coverage

So, how do you make sure you don't overpay? It's easier than you think. Just follow these simple steps to lock in the best rate.

- Call Your Insurer First: Before you even set foot in the dealership, give your car insurance agent a call. Ask them for a quote to add gap coverage to your policy. This number is your baseline—your "don't-pay-more-than-this" price.

- Get the Dealership's Price: When the finance manager inevitably offers you their gap insurance plan, ask for the total, one-time cost. Don't be shy about mentioning the quote you already have from your insurer.

- Compare and Choose: With both numbers in hand, the choice is usually crystal clear. The savings are often so significant that it makes the decision for you.

To make this even clearer, let's break down the key differences between these sources.

Comparing Gap Insurance Providers

The table below gives you a side-by-side look at your options, highlighting why it pays to shop around.

| Provider Type | Typical Cost Structure | Pros | Cons |

|---|---|---|---|

| Car Dealership | $500 – $700 flat fee | Extremely convenient | Most expensive option; often rolled into the loan, accruing interest. |

| Auto Insurer | ~$60 per year add-on | Most affordable; easy to manage with your existing policy. | You must carry comprehensive and collision coverage to qualify. |

| Third-Party Lender | Varies (often a flat fee) | Can be cheaper than the dealer. | Requires an extra step; may not be as cheap as your insurer. |

As you can see, the dealership offers a one-stop-shop experience, but your wallet pays for it. Your insurance company, on the other hand, provides the most cost-effective path to the same peace of mind.

Why Gap Coverage Is Only Part of Your Total Loss Strategy

Gap insurance is a fantastic safety net, but it's important to understand what it actually does. It’s not a standalone solution; its effectiveness hinges on one critical number determined by your primary auto insurer: your vehicle’s Actual Cash Value (ACV).

Think of the ACV as the starting line for your entire total loss claim. It’s the amount your insurance company says your car was worth the moment before it was wrecked. Your gap insurance payout is calculated after this number is set.

So, what happens if your insurer's ACV offer is too low? A lowball offer creates a bigger financial hole for your gap insurance to fill. This puts more pressure on the gap policy and can complicate your claim, leaving you in a tough spot. It feels like the insurance company holds all the cards, but they don't.

You Don't Have to Accept a Low ACV Offer

Many drivers don't realize their auto policy has a built-in tool for fighting back. In states like Washington and Oregon, this is called the Appraisal Clause. This provision gives you the legal right to challenge your insurer's valuation.

How does it work? You can hire an independent, state-licensed appraiser to conduct their own valuation of your totaled vehicle.

Invoking the Appraisal Clause shifts the power dynamic. It forces the insurance company to justify its offer against a fair, market-based appraisal from an unbiased expert, not just rely on the internal software that often benefits them.

Getting a professional appraisal can completely change the game. A detailed, evidence-based report forces the insurer to the negotiating table and often results in a significantly higher ACV payout. This process is covered in our guide to calculating total loss vehicle value.

By successfully increasing the ACV, you directly impact the "gap." A higher settlement from your primary insurer might shrink that gap considerably—or even eliminate it entirely. This ensures you get the money you're truly owed and lets your gap coverage work as the simple safety net it was meant to be.

Common Questions About Gap Insurance

Even after you've got a good handle on the basics, a few specific questions always seem to pop up about gap insurance. Let's tackle those common head-scratchers so you can make a fully informed decision.

Can I Cancel Gap Insurance Whenever I Want?

You bet. In almost every case, you can cancel your gap insurance policy at any time.

The best time to do this is when your loan balance finally dips below your car's actual cash value. Once you're no longer "upside down" on the loan, the coverage has done its job and isn't needed anymore.

A nice little bonus: if you paid for the whole policy upfront when you bought the car, you'll likely get a prorated refund for the unused portion. Just get in touch with your provider to kickstart their cancellation process.

Does Gap Insurance Also Cover My Deductible?

This is a big one, and the answer is… it depends. Some of the more comprehensive (and expensive) gap policies will indeed cover your collision or comprehensive deductible if your car is totaled. However, many standard, bare-bones policies will not.

Don't get caught by surprise. Always read the fine print of your policy before you sign on the dotted line. If deductible coverage isn't explicitly included, you'll still be on the hook for that amount, even if gap insurance pays off the rest of the loan.

What Happens If I Skip Gap Insurance and My Car Is Totaled?

If you don't have gap coverage and your car is declared a total loss, the financial responsibility falls squarely on your shoulders. You are legally obligated to pay the entire difference between what your insurance company gives you (the car's ACV) and what you still owe on the loan.

This can be a really tough spot to be in. You'd be stuck making monthly payments on a car you can no longer drive, potentially for years. Without that protection, a single accident can leave you with a surprise bill for thousands of dollars.

If you've been in an accident and feel your insurance company is undervaluing your vehicle, don't accept a lowball offer. Total Loss Northwest specializes in total loss and diminished value appraisals in Washington and Oregon. We fight to get you the fair settlement you're legally owed. Learn more about protecting your investment at https://totallossnw.com.