So, you've been in an accident that wasn't your fault. The other driver's insurance has covered the repairs, and your car looks as good as new. But here's the uncomfortable truth they won't tell you: your car is now worth significantly less than it was just before the crash. This loss in value is real, and you have the right to be compensated for it. This is where a diminished value claim comes in.

The goal is simple: to recover the inherent diminished value—the automatic drop in your car's market price simply because it now has an accident on its record.

What Is Diminished Value and Why Does It Matter?

When your car is repaired after a wreck, the insurance company pays to fix the physical damage. They'll put on a new bumper, straighten the frame, and match the paint. But what they can't do is erase the accident from your vehicle's history report.

That accident history creates a permanent stigma. This drop in what a buyer would be willing to pay for your car, even after perfect repairs, is called inherent diminished value.

Think about it from a buyer's perspective. If you're looking at two identical used cars on a lot, same year, same model, same mileage—but one has a clean history and the other was in a major collision—which one are you choosing? And if you do choose the wrecked one, you're definitely not paying the same price. That difference in price is its diminished value.

The Financial Reality of an Accident History

This isn't just a few hundred dollars we're talking about. The hit to your car's value can be massive. Depending on the car and the severity of the damage, vehicles often lose 15% to 30% of their pre-accident value. I've even seen cases involving high-end cars or severe structural damage where the loss climbed to 50%.

Don't expect the insurance company to bring this up. Their job is to settle claims for the least amount of money possible, and for them, that usually means just paying the repair bill and closing the file. It's on you to demand compensation for the full scope of your loss, which absolutely includes diminished value.

Key Takeaway: Quality repairs do not erase the accident from your vehicle's history. Filing a diminished value claim is the only way to be compensated for the guaranteed loss in resale value your car now carries.

Who Is Eligible to File a Claim?

Before you start the process, you need to make sure you have a legitimate case. Generally, you're in a good position to file a diminished value claim if you can check these boxes:

- You were not at fault for the accident. This is crucial. Your claim is made against the at-fault driver's insurance policy, not your own.

- The damage was significant. A few scratches or a minor door ding won't cut it. We're talking about damage that requires serious bodywork or structural repairs—the kind of stuff that shows up on a CARFAX report.

- Your car is newer or has high resale value. It’s much harder to prove diminished value on a 15-year-old car with 200,000 miles. The most successful claims are for vehicles that are just a few years old and have lower mileage.

State laws also play a big role. Each state has its own rules and, importantly, its own statute of limitations for filing. You'll want to review the specific state-by-state diminished value laws to understand the deadlines and regulations where you live.

Building an Unshakeable Case for Your Claim

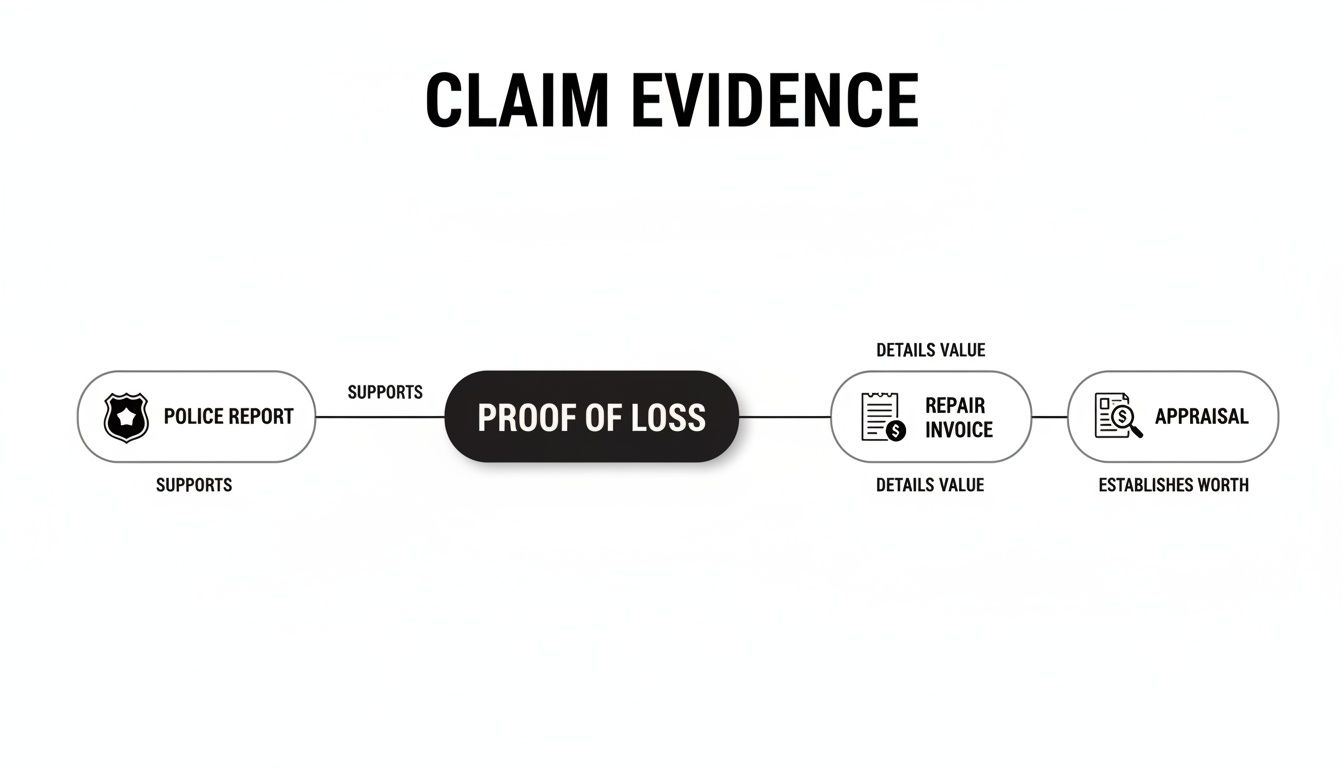

Before you even pick up the phone to call the insurance adjuster, your first job is to build an ironclad file of evidence. The whole point is to put together a case so logical and well-documented that the insurer has very little room to argue. This groundwork is everything when it comes to a successful diminished value claim.

Think of it like you're a detective building a case. Every single document adds another layer to the story and proves your financial loss. You can't just toss a few papers at them and hope for the best; you need a methodical, comprehensive collection of proof.

Assembling Your Core Documentation

First things first, let's get the essential paperwork in order. These documents establish the basic facts of the accident and the repairs that followed. They're non-negotiable and form the foundation of your entire claim.

Grab the official police report. This is your neutral, third-party account of what happened, who was at fault, and the initial damage seen at the scene. It immediately gives your claim credibility because it confirms the other driver was liable.

Next, you need to round up every document related to the repair work. I mean everything.

- Initial Repair Estimates: Get copies of all the estimates you received, not just from the shop that ultimately did the work. This shows that multiple professionals agreed on the extent of the damage.

- The Final Itemized Invoice: This is your holy grail of repair documents. It breaks down every single part that was replaced, every hour of labor, and the grand total. It paints a vivid picture of just how complex the repairs were. Make sure it notes whether any non-OEM (Original Equipment Manufacturer) parts were used, as that can hit your car's value even harder.

Creating a Clear Before-and-After Picture

Now that you've documented the accident and the repairs, it's time to show the direct hit to your vehicle's history. This is where a vehicle history report becomes your best friend.

Ideally, you’ll have a CARFAX or AutoCheck report from when you bought the car, showing its clean history. If you do, fantastic. Now, pull a brand-new report. Seeing that fresh "severe damage reported" entry creates an undeniable contrast.

My Experience: Showing an adjuster a clean, pre-accident history report right next to a post-accident one with a big red flag on it is incredibly effective. It's a powerful visual that makes the "stigma" on your car's VIN tangible. They can't argue with that.

The Cornerstone of Your Claim: The Independent Appraisal

The documents we've covered are crucial, but the single most powerful weapon in your arsenal is a professional, independent diminished value appraisal. This isn't just getting a second opinion from another body shop. This is a formal, detailed valuation report from a certified appraiser who specializes in this.

A good appraiser does a deep dive. They’ll physically inspect the quality of the repairs, pore over all your documentation, and analyze real-time market data for vehicles just like yours in your area—comparing prices for ones with and without accident histories.

The final report needs to be USPAP-compliant (Uniform Standards of Professional Appraisal Practice). This is key because it means the report meets strict federal standards, giving it serious credibility and legal weight. This document transforms your claim from your opinion against theirs into your expert's factual analysis versus their internal formula. It's how you turn a potential argument into a negotiation based on hard evidence.

Why a Professional Appraisal Is Non-Negotiable

If there’s one mistake that can tank your diminished value claim from the start, it’s trusting the insurance company’s valuation. Let's be clear: their internal process isn't designed to make you whole. It's built to close your file as cheaply as possible.

To do this, they often lean on a flawed, one-size-fits-all formula that works in their favor, not yours. This is precisely why getting your own professional, independent appraisal isn't just a good idea—it's the single most critical piece of evidence you’ll have. It’s not just a second opinion; it's the authoritative, fact-based foundation for your entire claim.

As you gather your documents, think of the appraisal as the final, powerful piece that ties everything together and puts a real, defensible number on your loss.

Each document you collect builds the story of what happened. The appraisal is what gives that story a price tag.

The Problem With the Insurer’s Math

Most insurance companies use a notorious shortcut known as the “17c formula” to calculate diminished value. Born out of a Georgia court case, this method is a quick-and-dirty way to produce a lowball offer.

It typically starts with your car's pre-accident value, applies an arbitrary cap (usually 10%), and then chips away at that number with "modifiers" for damage and mileage. The result is almost always an insultingly small figure. The formula’s biggest weakness? It completely ignores a physical inspection and real-world market data. It’s a generic calculation that produces conservative estimates, which is exactly why insurers love using it.

Real-World Scenario: A client came to us after their three-year-old SUV took a serious hit to the rear. The at-fault insurer offered a paltry $300 for diminished value, citing their internal formula. Our comprehensive appraisal, however, documented poor paint blending from the repair and analyzed local sales data, proving a true value loss of $4,500. Guess which number the final settlement was based on? Not theirs.

The gap between these two approaches is massive. One is a desk-based formula, while the other is a fact-based investigation.

Insurer's Formula vs Independent Appraisal

| Factor | Insurance 17c Formula | Independent USPAP Appraisal |

|---|---|---|

| Foundation | Generic, automated calculation | Hands-on physical inspection |

| Market Data | Ignores local market conditions | Based on real-time, local comparable sales |

| Repair Quality | Assumes repairs are flawless (sight unseen) | Meticulously inspects for imperfections |

| Credibility | Biased in favor of the insurer | Objective, third-party, and defensible in court |

This table makes it obvious—an independent appraisal is the only way to get a true picture of your financial loss.

What a Legitimate Appraisal Actually Involves

A true, USPAP-compliant appraisal is miles ahead of a simple formula. Here's what a certified professional delivers and why it gives you undeniable leverage:

-

A Detailed Physical Inspection: The appraiser gets hands-on, meticulously examining the quality of the repairs. They’re looking for things like mismatched paint, inconsistent panel gaps, and signs of non-OEM parts—details an adjuster will never spot from behind a desk.

-

Real-World Market Analysis: They dive into your specific local market to find out what identical vehicles—both with and without accident histories—are actually selling for. This isn't guesswork; it's hard data on buyer perception and value loss.

-

A Comprehensive Report: You don't just get a number. You get a detailed, multi-page report that explains the appraiser's methodology, shows the comparable vehicle data, and presents a clear, defensible dollar amount for your loss.

Investing in a professional vehicle appraisal service isn’t an expense; it’s the tool that gives you the power to negotiate effectively. It replaces the insurer’s opinion with an expert’s factual analysis. When you file a diminished value claim armed with this report, you're no longer just asking for money—you're presenting a documented, evidence-backed case for what you are rightfully owed.

How To Write And Submit Your Demand Letter

Now that you’ve got your professional appraisal and all your evidence lined up, it’s time to formally state your case. This is done with a demand letter. Think of it less as a letter and more as a professional, fact-based invoice for your car's lost value.

This isn't the place to rehash the accident or vent your frustrations. The tone should be firm and confident, but never angry. You're simply presenting a documented financial loss and asking to be compensated for it. This document kicks off the negotiation, so making it clear and professional is absolutely critical.

Structuring Your Demand Letter

Your demand letter needs to be a concise summary of your claim. The goal is to make it incredibly easy for the insurance adjuster to grasp your position in about 30 seconds. A strong letter gets straight to the point and includes a few essential pieces of information.

Here’s exactly what your letter needs to contain:

- Your Contact Information: Full name, address, and phone number.

- The At-Fault Party’s Details: The name of their insured driver.

- Critical Claim Identifiers: The date of the accident and the insurance claim number.

- The Demand Amount: This is the headline. State the specific dollar amount from your appraisal. For example: "My documented diminished value is $4,500."

Getting right to the point shows the adjuster you're organized, serious, and ready to back up your number. It tells them you’ve done the work. If you want a deeper dive, we have a complete guide on crafting an effective insurance demand letter with more examples.

Pro Tip: Keep it strictly business. The adjuster already has the accident report and knows the story. Your letter has one job and one job only: to formally present your financial loss and demand payment based on an expert's report.

Submitting Your Claim Package

Your letter is ready, but don’t send it alone. You need to assemble a complete package with every piece of evidence you've gathered. Sending the letter without the supporting documents is a rookie mistake that will only cause delays.

Here’s what your full submission package should include:

- The Demand Letter: This acts as your cover sheet and official request.

- The Full Appraisal Report: This is your expert evidence that justifies the dollar amount you’re demanding.

- The Police Report: This document officially establishes who was at fault.

- All Repair Invoices: These show the scope and severity of the physical damage that was repaired.

When you're ready to send everything, choose a method that gives you proof of delivery. Certified mail with a return receipt is a classic for a reason. If you're dealing with a company that prefers digital, using secure online fax services for legal documents can be a great way to ensure it arrives safely and you have a transmission record.

Whatever you do, make sure you can prove they received it.

Negotiating with the Insurance Adjuster Like a Pro

Alright, you’ve sent your demand letter. Now the real game begins. The ball is officially in the insurance adjuster’s court, and their response will kick off the negotiation.

Let's be clear about one thing: the adjuster's job is to protect their company's bottom line. That means paying out as little as possible on every single claim, including yours. Don’t take it personally; it’s just business.

Their first move will likely be an attempt to shut you down completely or throw a ridiculously low number at you. They are trained to control the conversation and see if you'll fold easily. Knowing their playbook ahead of time is your best defense.

Anticipating the Adjuster's Tactics

Insurance adjusters have a script they tend to follow, especially with diminished value claims. If you can see their moves coming, you can prepare calm, fact-based responses that keep the discussion focused on your evidence, not their talking points.

Here’s what you should be ready for:

- The Immediate Lowball Offer: They might toss out a few hundred dollars right off the bat, hoping you’ll see it as quick cash and go away. This is a classic test. Your response should be a polite but firm "no," explaining that the offer doesn't come close to the documented loss in your expert appraisal.

- Discrediting Your Appraisal: Get ready to hear things like, "Your appraiser is biased," or "We don't agree with their methodology." Don’t get defensive. Simply ask them to put their specific objections in writing. A great reply is, "My appraiser is a certified, independent expert, and their report is USPAP-compliant. Can you please provide a written critique of their findings?" This often stops that argument in its tracks.

- The "It Doesn't Exist" Defense: This one is a favorite. They’ll claim diminished value "isn't a thing" in your state or that your policy doesn't cover it. Calmly reiterate that inherent diminished value is a recognized component of property damage and that your claim is for the direct loss in market value caused by their insured’s negligence.

Your professional appraisal is your anchor. No matter what they throw at you, keep bringing the conversation back to the facts and figures in that report.

My Advice: Whatever you do, never accept the first offer. It's almost always a fraction of what your claim is actually worth. The real negotiation doesn't start until you've rejected that initial lowball amount.

Making a Strategic Counteroffer

After you turn down their initial offer, the adjuster will probably ask, "Well, what number are you looking for?" Don't just pull a number out of thin air.

Let's say your original demand was for $4,500 and they came back with a paltry $500. Dropping your number slightly, perhaps to $4,200, shows you’re willing to negotiate in good faith while still standing firm on your valuation.

When you make your counteroffer, tie it directly to the evidence. For example: "I'm willing to come down to $4,200, but as the appraisal details, the structural damage now listed on the CARFAX is the main reason for the $4,500 loss, and that is a permanent, documented issue."

Finalizing the Agreement

The back-and-forth will continue until you land on a number that feels fair. Once you and the adjuster verbally agree on a final figure, you’ve reached the most critical step of all: get it in writing.

Do not hang up the phone or consider the deal done until you have an email or a formal letter from the adjuster confirming the exact settlement amount. This document is your proof. Only after you have this confirmation in hand should you even think about signing any release forms.

Once that email arrives, you've officially navigated the diminished value claim process from start to finish.

Common Questions About Diminished Value Claims

Even with a clear roadmap, you probably still have a few questions about the nitty-gritty details of a diminished value claim. It’s totally normal. Every accident is different, and unique situations pop up all the time. Let’s tackle some of the most common questions I hear from clients.

Think of this as the FAQ for when you're in the trenches—your demand is sent, and you're navigating the back-and-forth with the insurance adjuster. Getting these points straight can make all the difference.

Can I File a Claim Against My Own Insurance Policy?

This is a big one, and the answer is a hard no almost every single time. Diminished value is what’s known as a third-party liability claim. In plain English, that means you have to file it against the insurance company of the driver who caused the accident.

Your own policy's collision coverage is there to pay for the direct cost of repairs to get your car back on the road. It isn't designed to cover the indirect financial hit your car takes to its resale value.

The only exception is incredibly rare. If you're hit by an uninsured or underinsured driver and your policy has a specific type of UIM property damage coverage that explicitly mentions diminished value, you might have a shot. But honestly, that’s almost unheard of in standard policies.

The Bottom Line: Your insurance fixes your car. Their insurance pays for the financial damage their driver caused, and that includes the drop in your car’s market value.

How Long Do I Have to File a Claim?

Don’t sit on this. Every state has a strict legal deadline for filing property damage claims, called the statute of limitations. This deadline absolutely applies to diminished value. If you miss it, you lose your right to claim that money forever, no matter how solid your case is.

The clock is different depending on where you live. For instance:

- In Washington and Oregon, the window is generally three years from the date of the wreck.

- Other states are less generous, sometimes giving you as little as two years.

My advice? Get the ball rolling as soon as your repairs are finished. Waiting not only puts you at risk of missing that legal cut-off, but it also makes it tougher to build a strong case with fresh evidence.

What if the Insurer Refuses to Pay?

So, what happens when the insurance company just says "no" or throws a lowball offer at you and calls it final? You’re not stuck.

Your first move is often to invoke the "Appraisal Clause" hidden in most auto insurance policies. This clause kicks off a formal dispute process. You hire an appraiser, they hire one, and the two work to reach a binding agreement on the value.

If that doesn't work out, your next stop is likely small claims court. This is where your professional appraisal report and all that organized paperwork become your best friend. You can walk in and present a powerful, well-documented case directly to a judge.

At Total Loss Northwest, we specialize in creating the certified, independent appraisals you need to build an unshakeable case. If you're getting stonewalled by an insurer, our USPAP-compliant reports provide the muscle to fight for every dollar you're owed. Don't leave their money on the table. Let us help you get the fair settlement you deserve. Learn more about how we can help.