When your insurance company says your car is a "total loss," they aren't just making a judgment call. It's a decision based on a straightforward, but often misunderstood, calculation.

This calculation, known as the total loss formula, boils down to comparing two key numbers: the estimated cost to repair your vehicle versus its value right before the accident, known as the Actual Cash Value (ACV).

If the repair bill hits a certain percentage of the car's ACV, the insurer will "total it out" and cut you a check instead.

So, What Does "Total Loss" Really Mean?

Think about it like this: your trusty old laptop suddenly dies. The repair shop quotes you $800 to fix it, but you know you could only sell it for about $900 as-is. Would you sink that much money into fixing it? Probably not. You'd take the loss and put that money toward a new one.

Insurance companies do the exact same thing with your car. It’s a simple business decision.

After an accident, an adjuster will meticulously estimate the cost of everything needed to bring your car back to its pre-crash condition—parts, labor, paint, you name it. They then stack that number up against the car’s ACV at the precise moment before the impact.

Your car's ACV isn't just a random number. It’s based on real-world data, including its:

- Make and model

- Year and mileage

- Overall condition (dings, scratches, and all)

- Recent sales of similar cars in your local market

When the repair estimate crosses a certain line—a percentage set either by state law or the insurer's own internal rules—the car is officially a total loss. This isn't about whether the car can be repaired; it's about whether it makes financial sense for the insurance company to do so.

The Bottom Line: A "total loss" is a financial decision, not a mechanical one. Your car is totaled when the cost to fix it is simply too high compared to what it's worth.

Getting a handle on this basic math is the first step in making sure you get a fair settlement. Many people are surprised by their insurer's first offer, and knowing how they got to that number gives you the power to push back.

To help you through this, our guide on what to do when your car is totaled walks you through the next steps you should take to protect yourself.

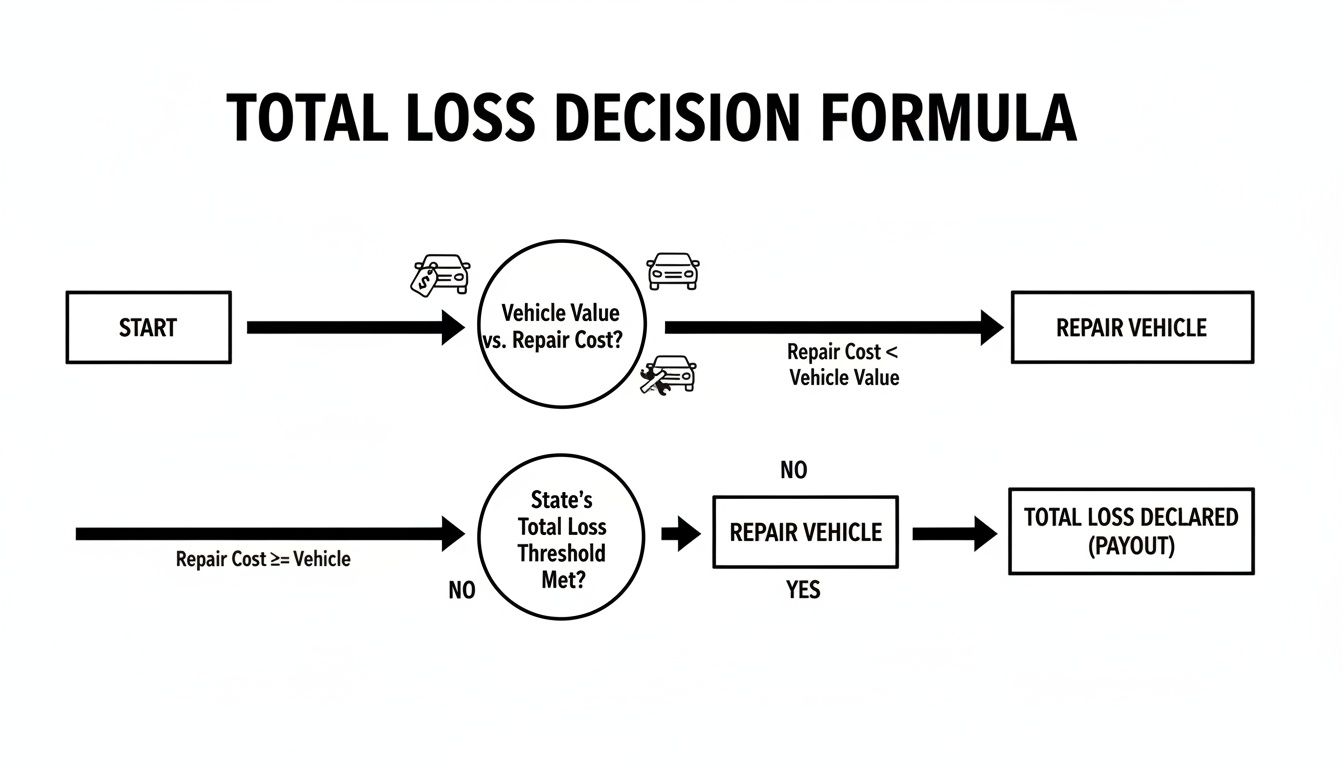

Understanding the Total Loss Threshold

So, what's the magic number that pushes a car from "repairable" to "totaled"? It all comes down to something called the total loss threshold, or TLT.

This isn't some arbitrary figure your insurance adjuster pulls out of thin air. The TLT is a specific percentage set by state law. It's the line in the sand. If the cost to fix your car goes over this percentage of its pre-accident value (the Actual Cash Value), your insurer is legally required to declare it a total loss.

Let's put that into real numbers. Say your state has a 75% threshold. If your car was worth $20,000 before the crash, any repair estimate that tops $15,000 ($20,000 x 75%) means it’s officially totaled. Simple as that.

This rule is there to create a consistent, unbiased standard. The flowchart below gives you a good visual of how this decision plays out.

As you can see, it's a straightforward comparison. If the repair bill meets or beats that state-mandated percentage, the car is a goner.

How Thresholds Vary by State

Here's where things get interesting—and potentially frustrating. These thresholds aren't the same everywhere. Every state makes its own rules, which means the exact same car with the exact same damage could be totaled in one state but considered repairable right across the border.

For example, a state like Washington uses a simple percentage-based TLT. But others, like Oregon, get a bit more complex with something called a "Total Loss Formula" (TLF), which adds another layer to the calculation.

The Total Loss Formula (TLF) is a common alternative where a vehicle is totaled if the Cost of Repair + Estimated Salvage Value ≥ Actual Cash Value. This means even if repair costs are below the threshold, a high salvage value can still tip the scales.

This little formulaic difference can have a huge impact on your claim. A car with moderate damage might seem repairable under a simple threshold system, but if its parts are valuable and it has a high salvage auction estimate, a TLF state could still write it off.

Let's look at a practical example. Imagine a car with a $20,000 Actual Cash Value (ACV) that needs $15,500 in repairs. Here’s how the outcome changes based on different state rules.

How State Thresholds Impact Total Loss Decisions

This table shows how different total loss thresholds affect whether a vehicle with a $20,000 Actual Cash Value (ACV) is declared a total loss.

| State Threshold Percentage | Repair Cost to Trigger Total Loss | Is a $15,500 Repair Bill a Total Loss? |

|---|---|---|

| 75% Threshold | > $15,000 | Yes |

| 80% Threshold | > $16,000 | No |

| 100% Threshold | > $20,000 | No |

As the numbers show, that $15,500 repair bill gets two very different results. The driver in the 75% threshold state gets a check for their totaled car, while the driver in the 80% state is headed to the body shop.

This is exactly why it's so important to know your state's specific rules. It's the first step in understanding what to expect from your insurance company and how to navigate your claim effectively.

How Insurers Calculate Your Car's Actual Cash Value

When your insurance company starts talking about the total loss formula, everything hinges on one key number: your car’s Actual Cash Value (ACV). This isn't what you paid for the car or what a brand-new one costs. It’s what your specific car was worth on the open market just moments before the crash.

Honestly, the ACV is the single biggest source of friction in most total loss claims, and for good reason. It’s a snapshot in time, and insurers follow a pretty standard recipe to figure it out.

They’ll start with the basics—year, make, and model—and then tweak that value based on a few critical factors:

- Mileage: More miles on the odometer usually means a lower value.

- Condition: They'll look at everything from old dings and scratches to interior wear and tear and even the depth of your tire treads.

- Options: That factory-installed sunroof, premium sound system, or advanced safety package you paid extra for? Those add value.

- Local Market Value: This is a big one. The final number is heavily swayed by what similar cars are actually selling for right in your area.

The process seems logical on the surface, but here’s where things can get tricky. Most insurance companies use third-party valuation software to pull all this data together. While that's efficient for them, these systems can sometimes spit out a low number if they’re using old sales data or don't properly account for a hot local market. A process that looks fair can easily end in a lowball offer.

The Two Sides of the Equation

Think of the total loss formula as a balancing act. On one side, you have the ACV. On the other, you have the estimated cost to fix your car.

The repair estimate is a line-by-line breakdown of everything needed to get your vehicle back to its pre-accident condition—parts, labor, paint, the whole nine yards. An initial estimate might not look too bad, but those costs can skyrocket once a body shop tears the car down and finds hidden damage to the frame or sensitive electronics, which is a huge issue in modern vehicles.

Let’s walk through a real-world scenario. Say you have a well-kept Subaru Outback that your insurer values at $22,000 (the ACV). The body shop says it will take $16,000 to fix it. If you live in a state with a 75% total loss threshold, your car is officially totaled because the repair cost ($16,000) is more than the $16,500 limit ($22,000 x 0.75).

But what happens if their ACV is just plain wrong?

This is where the fight often begins. If your research shows comparable Outbacks in your area are selling for $25,000, the 75% threshold is actually $18,750. Suddenly, your car is no longer a total loss based on that initial repair estimate.

The numbers can be nudged on both sides of the formula. A low ACV or an inflated repair estimate can easily push a perfectly repairable car over the total loss cliff. It's happening more and more—total loss claims jumped to 27% of all collision claims in 2022, up from 24% in 2021.

Your best defense against a bad settlement is to understand exactly what the actual cash value of your car is. This is especially true in fast-moving used car markets like we see in Oregon and Washington, where insurer valuations often lag weeks or months behind real-world prices, leaving you with a huge financial gap to cover.

The Hidden Role of Salvage Value

When your car is badly damaged, the insurance adjuster looks at two main numbers: what your car was worth (Actual Cash Value) and how much it’ll cost to fix it. But there’s a third, often overlooked, number that can completely flip the script on their decision: salvage value.

This is what the insurance company figures they can get for your wrecked car by selling it to a junkyard or at a salvage auction. Think of it as the car’s last gasp of value. Even a mangled wreck has parts that are worth something—an uncracked windshield, a solid transmission, or just the weight of its scrap metal. The insurer gets to subtract this amount from what they pay you, which reduces their overall cost for the claim.

How Salvage Value Completes the Formula

In states that use what’s called the Total Loss Formula (TLF), salvage value isn't just an afterthought; it’s a critical piece of the puzzle. They don't simply compare repair costs to your car's value. Instead, they add the salvage value into the equation.

The Total Loss Formula in Action:

A car is totaled if the numbers shake out like this:

Cost of Repairs + Salvage Value ≥ Actual Cash Value (ACV)

This little bit of math is what often tips a car over the edge from "repairable" to "totaled." You might think your car is safe because the repair bill doesn't meet your state's damage percentage, but a high salvage value can change everything. This happens a lot with newer cars or popular models where the parts are in high demand.

Let's walk through an example to see how this hidden number can totally change the outcome.

A Surprising Outcome

Let’s say your car has an ACV of $10,000. The body shop comes back with a repair estimate of $7,000. If you live in a state with an 80% total loss threshold, you'd need $8,000 in damage to total the car. At first glance, it looks like you’re in the clear and your car will be repaired.

But then the insurance adjuster factors in the salvage value. They determine that, even in its wrecked state, your car could fetch $3,500 at a salvage auction because of its pristine engine and high-tech electronics.

Now, let's plug those numbers into the Total Loss Formula:

- Repair Cost: $7,000

- Salvage Value: $3,500

- Total: $10,500

That combined figure of $10,500 is now more than the car’s $10,000 ACV. Just like that, your car is a total loss. It was the salvage value that sealed its fate, even though the repair bill alone wasn’t high enough. This is a perfect example of how the insurer's internal financial calculation, not just the physical damage you see, is what really decides if you get your car back.

Why Are So Many Cars Being Totaled These Days?

If you’ve noticed that insurance companies seem quicker than ever to label a car a "total loss," you're not just imagining things. It's a real trend, and the reason is likely sitting in your driveway: the very technology that makes your car safer and more convenient is also making it incredibly expensive to fix.

Think about a simple fender-bender. A decade ago, it was a straightforward bumper replacement. Today, that same bumper might be packed with sensors for parking assist, adaptive cruise control, and automatic emergency braking. A cracked windshield isn't just glass anymore; it often houses the camera for your lane-keeping assist.

These parts aren't just expensive to buy; they require specialized tools and highly trained technicians to calibrate them correctly. This new reality has completely changed the math for insurance companies, pushing more and more vehicles over the financial edge into a total loss.

It's All About the Tech (And the Cost)

The numbers don't lie. The percentage of collision claims ending in a total loss has been creeping up for years, and it's a direct result of eye-watering repair bills for modern cars.

Industry data paints a stark picture. By the second quarter of 2025, total losses made up a whopping 22.6% of all collision claims. That's a huge jump from just a few years ago and shows just how much repair complexity is tipping the scales. You can dig deeper into this data by reading about the surge in total loss claims.

So, what’s creating this perfect storm for insurers and car owners? It boils down to a few key factors:

- Pricey ADAS Parts: The sensors, cameras, and little computer modules that run your car’s safety features are both delicate and costly. Even a minor bump can damage these systems, triggering the need for a full replacement.

- Specialized Labor and Calibration: Fixing a modern car is no longer just a mechanical job. It requires technicians who understand electronics and software. The calibration process alone—ensuring all the sensors are aimed and working correctly—can add hundreds, if not thousands, to the final bill.

- Inflation Hits the Shop: On top of the tech, general inflation, supply chain issues for parts, and higher labor rates have driven up the cost of all car repairs.

- Our Cars Are Getting Older: The average age of vehicles on the road is at an all-time high. An older car naturally has a lower Actual Cash Value (ACV). This means it doesn't take a massive repair estimate to be more than the car is even worth.

When you mix these factors together, it becomes clear why insurers are more likely to just cut a check and write off a vehicle that would have been repaired without a second thought ten years ago. For you, this means knowing your car's true market value—and being ready to negotiate a fair ACV—is more important than ever. It's the only way to make sure you get enough money to actually replace what you've lost.

How to Negotiate a Better Total Loss Settlement

Getting that first settlement offer from your insurance company can feel like a punch to the gut, especially when the number is nowhere near what you know your car was worth. The most important thing to remember is this: their initial offer is just that—an offer. It’s the start of a conversation, not the final word.

You absolutely have the right to push back on their valuation. But to do it successfully, you can't just feel that your car was worth more; you have to prove it. The insurance company used their software and data to come up with a number, and now it's your turn to show them what they missed.

Gathering Your Evidence

To counter a lowball offer, you need to build a solid case backed by facts. Let's get organized and pull together everything that proves your vehicle’s true, pre-accident value.

Your negotiation toolkit should have a few key things:

- Comparable Vehicle Listings: This is your strongest ammo. Find at least 3 to 5 local listings for cars that are the same make, model, year, and trim as yours. These "comps" are real-world proof of what it will actually cost to buy a replacement.

- Maintenance Records: Did you keep up with every oil change and service interval? A thick stack of maintenance records proves your car was meticulously cared for, which directly translates to a higher value.

- Receipts for Recent Upgrades: Those brand-new tires you put on last month? That upgraded stereo system? Every recent investment you made needs to be documented. These aren't just features; they're value-adds that the insurer's system likely overlooked.

Key Insight: Don't forget about the "Appraisal Clause" buried in most auto policies. This is your ace in the hole. Invoking this clause means you and the insurer each hire an independent appraiser. They work to agree on the value, effectively taking the decision away from the company adjuster.

Hiring a certified independent appraiser can be a game-changer. Their unbiased, market-based report gives you professional leverage that’s hard for an insurance company to ignore. It’s a powerful way to challenge their initial number and fight for the fair payout you deserve.

If you want to go deeper on this topic, you can learn more about how to negotiate a total loss settlement right here on our blog.

Your Top Questions About the Total Loss Formula Answered

Going through the total loss process can be a real headache. But once you get a handle on how the insurance company runs the numbers, you'll feel much more in control. Let's break down some of the most common questions people have.

Can I Argue with the Insurance Company's Valuation?

Yes, you absolutely can. Think of the insurance company’s first offer for your car's Actual Cash Value (ACV) as their opening bid, not the final number set in stone. If that number feels too low, you have every right to push back.

The key is to come prepared with proof. To build a solid case for a higher value, you'll need to do a little homework:

- Find comps: Look for similar vehicles for sale in your local market. This shows the adjuster what it would actually cost to replace your car.

- Show your work: Gather up all your maintenance records. A well-cared-for car is worth more, and your records prove it.

- Document upgrades: Did you recently get new tires? A new stereo? Major engine work? Receipts for these upgrades can directly increase your car's value.

Handing this evidence to the adjuster gives you real leverage to negotiate a better settlement.

What if I'm Still Paying Off My Car?

This is a super common scenario, so don't panic. When your car is declared a total loss, the insurance company sends the settlement check directly to your lender first.

If the payout is more than your loan balance, the lender gets paid in full, and you get a check for the rest. But what if the settlement is less than what you owe? That's where it gets tricky. You're still on the hook for the remaining loan balance. This gap is precisely what Guaranteed Asset Protection (GAP) insurance is for—it's designed to cover that exact shortfall.

Crucial Point: The insurance payout is based on your car's market value, not what you owe on your loan. Without GAP coverage, you could end up making payments on a car that's already in a salvage yard.

How Long Does This Whole Process Take?

There's no single answer, but you can generally expect a total loss claim to take several weeks from start to finish. The timeline can get stretched out by a few common hiccups, like back-and-forth negotiations over the ACV, problems getting a clear title, or even just waiting for your lender to provide the final loan payoff amount.

At Total Loss Northwest, our entire focus is making sure you get a fair settlement based on your vehicle's true market value. If you're dealing with a lowball offer, we can step in and invoke the Appraisal Clause in your policy to fight for what you're rightfully owed. Find out more about how we help at https://totallossnw.com.