When your insurance adjuster delivers the news that your car is a "total loss," it’s not just about the crumpled bumper or shattered glass. It’s a purely financial decision. An insurer totals a vehicle when the cost to repair it plus its scrap value is greater than its pre-accident market value—what they call the Actual Cash Value (ACV).

This calculation is the bedrock of the entire total loss process.

What It Means When Your Vehicle Is Totaled

Hearing your car is totaled can feel jarring, especially if it seems like it could be fixed. From the insurer's perspective, though, looks don't matter. They're running a numbers game dictated by your policy and state law. The second the repair estimate hits a certain percentage of your car's value, the total loss process kicks into gear.

This isn't an uncommon scenario. In fact, total loss frequency has climbed to a staggering 22.8% of all crash-involved vehicles.

A big driver is the age of cars on the road. Believe it or not, over 72% of total loss valuations in 2025 are expected to involve cars that are seven years or older. This is made worse by today's complex technology; with 88% of repair appraisals now requiring diagnostic scans for advanced driver-assistance systems (ADAS), what looks like a minor fender-bender can quickly become a massive expense. You can dig into more of this data on rising repair costs over at Carscoops.com.

The Core Concepts You Need to Know

To make sure you get a fair shake, you first need to speak the insurance company's language. Getting comfortable with their terminology gives you the power to navigate the process and push back when their numbers don't add up.

Let's break down the jargon you'll hear over and over. This quick reference table translates the key terms into what they actually mean for your wallet.

Key Terms in a Total Loss Claim

| Term | What It Means for You |

|---|---|

| Actual Cash Value (ACV) | The market value of your vehicle the moment before the accident. This isn't the replacement cost or what you owe on your loan; it's what someone would have realistically paid for it. |

| Total Loss Threshold | A percentage set by state law or your policy. If repair costs cross this line (e.g., 75% of the ACV), the car must be totaled. It varies by state. |

| Salvage Value | The amount the insurer can get by selling your wrecked car to a salvage yard for parts or scrap. This is their money to recoup. |

Knowing these terms is your first step toward taking control of the situation. They form the basis of the insurance company's settlement offer and give you the knowledge you need to protect your financial interests.

The most important number in your entire claim is the Actual Cash Value. The insurer's settlement offer is based entirely on their determination of your vehicle's ACV, making it the most critical figure to scrutinize and, if necessary, challenge.

Once you understand this foundation, you can see past the initial shock and start preparing for the next steps in your claim.

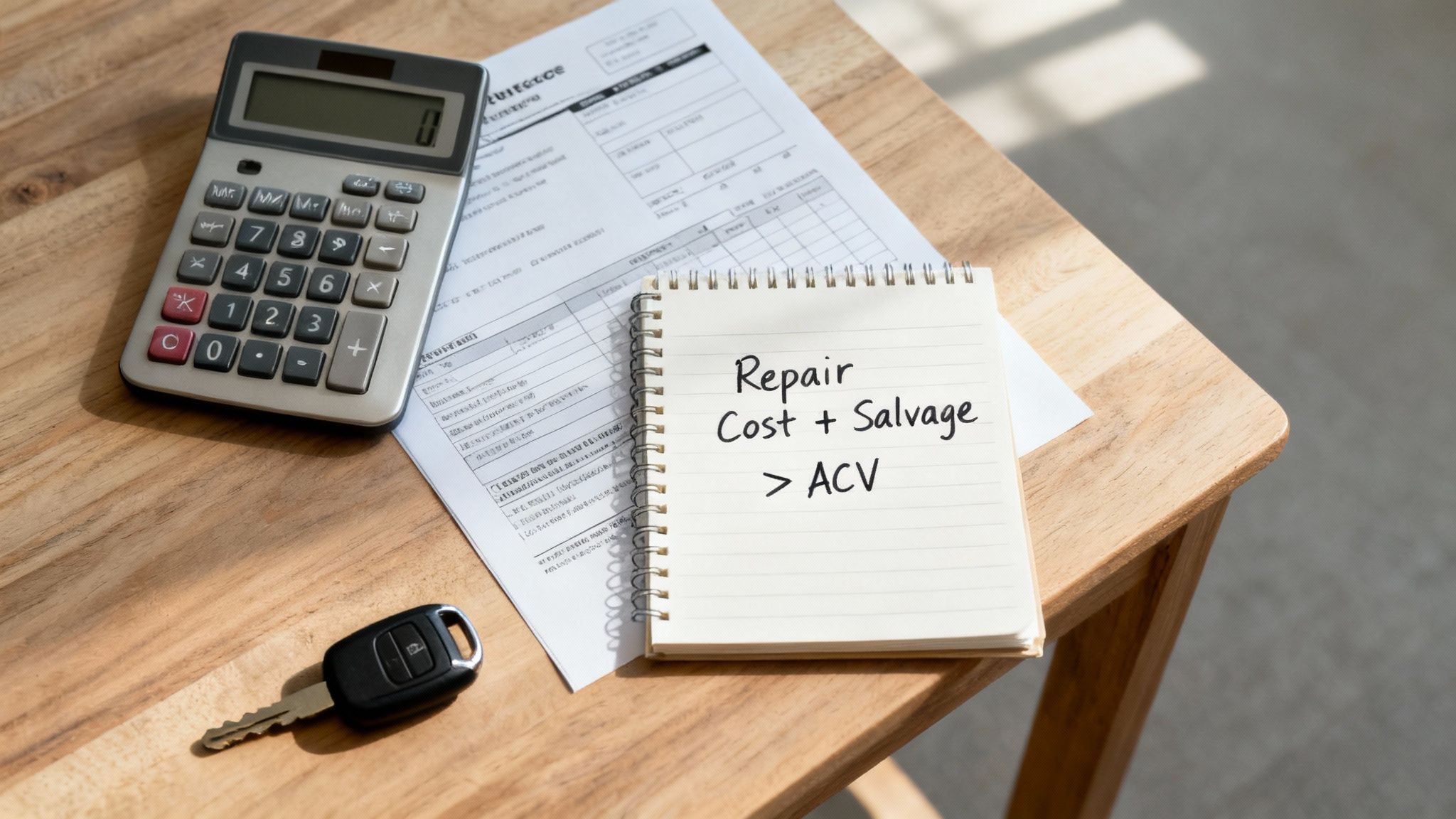

The Insurance Company's Total Loss Formula Explained

When an insurance adjuster looks at a wrecked car, they aren't just making a gut call based on the damage. Their decision to repair or total it comes down to cold, hard math.

It's all based on a surprisingly simple formula that seals your vehicle's fate:

(Cost of Repairs + Salvage Value) > Actual Cash Value (ACV)

If the sum on the left is greater than the value on the right, the insurance company will declare your car a total loss. To make sure you're getting a fair shake, you need to understand what each of these terms really means.

Decoding the Cost of Repairs

This is usually the biggest number in the equation. The "Cost of Repairs" isn't just a new bumper and a paint job; it’s a detailed estimate of every single thing needed to restore your car to its pre-accident condition.

A proper estimate includes:

- Parts: This is a classic battleground. Insurers love to spec cheaper aftermarket or used parts to keep their costs down.

- Labor: The number of hours a certified tech will spend on the job, multiplied by the shop's hourly rate.

- Hidden Expenses: Think about all the tech in modern cars. This includes things like recalibrating sensors for driver-assistance systems, which can add hundreds or even thousands to the bill.

The type of parts used can make or break the calculation. Understanding the difference between OEM vs aftermarket parts is crucial, as this one detail can easily push a repairable car over the total loss line.

Understanding Salvage Value and Actual Cash Value

While repair costs are the main event, the other two parts of the formula are just as critical. They represent your car's "before" and "after" value from the insurer's point of view.

Salvage Value is what your wrecked car is worth to the insurance company after they've paid you off. It's the price they expect to get by selling the car at a salvage auction to a rebuilder or parts yard. This amount basically reduces their net loss on the claim.

Actual Cash Value (ACV) is, without a doubt, the most important—and most disputed—number in this whole process. This is what your car was worth the moment before the crash happened. It is not what you paid for it, what a new one costs, or what you still owe on your loan.

The insurer’s ACV calculation is the starting point for their settlement offer. They typically rely on valuation software that uses broad national data, which often misses your vehicle's excellent condition, recent upgrades, or the realities of your local market.

This strict math is why more cars are being totaled now than ever before. Recent data shows total loss rates are nearing 24% of all estimates in mid-2025. With used car values cooling off and over 73% of totaled cars being seven years or older, it's just cheaper for insurers to write a check than to pay for complicated repairs. You can find more detail on what makes a car a total loss in different scenarios in our other guides.

Protecting Your Claim from the Moment of Impact

The minutes right after a car accident are a blur of adrenaline and stress. But the actions you take right then and there can have a massive impact on your total loss settlement down the road. This goes way beyond just swapping insurance info; it's your first—and best—chance to build a rock-solid case for your vehicle's real, pre-accident value.

Think of it this way: the insurance company is going to start from a baseline number, and it’s almost always lower than what your car was actually worth. Your mission, starting at the scene, is to gather the proof that your car was better than their average, cookie-cutter valuation.

Document Everything Before the Tow Truck Arrives

Your smartphone is your single most important tool in these first few minutes. Before your car gets hooked up and hauled away, you need to create a complete visual record of the damage, the car’s condition, and the scene itself. Don’t just snap a few quick pictures of the crumpled bumper. You need to think like a crime scene investigator documenting evidence for your own claim.

This detailed record creates an objective truth that’s hard to argue with later. It showcases the full scope of the impact and can be your best defense if an adjuster tries to minimize the severity of the crash.

Get photos and videos of everything:

- The Big Picture: Take wide shots of the entire scene. Get all the vehicles involved, any visible skid marks, and nearby road signs or traffic lights.

- Your Car's Condition: Walk around and capture your entire vehicle from all four sides. This is crucial for showing its overall pre-accident condition, including the parts that aren't damaged.

- The Damage Details: Now, get in close. Take detailed photos of every dent, scratch, and broken part. If you can safely do so, get pictures of damage underneath the car. Don’t forget the interior—deployed airbags are a key detail to capture.

- A Walk-Around Video: A slow, steady video as you walk around the car can provide incredible context. You can even narrate what you're seeing to add more detail that a static photo might miss.

Pro Tip: Your mind will be racing after a crash. That's why you should create a note in your phone right now with a simple photo checklist. If you're ever in an accident, you won't have to think—just open the note and follow your own instructions.

Your Pre-Settlement Documentation Checklist

Once you're safely away from the scene, it’s time to assemble your vehicle's "value portfolio." This isn't just a pile of paperwork; it's the hard evidence that proves your car was well-cared-for and worth more than the generic book value the insurer will try to use. Being proactive here shows the adjuster you mean business and can add hundreds, or even thousands, to your final payout.

Use this checklist to gather the essential evidence needed to support your vehicle's true value.

| Action Item | Why It's Critical | Pro Tip |

|---|---|---|

| Maintenance & Repair Receipts | Proves the vehicle was well-maintained. A $1,200 set of new tires adds real value. | Organize receipts chronologically in a folder or scan them to a single PDF for easy sharing. |

| Proof of Upgrades & Add-Ons | Documents aftermarket parts like stereos, remote starters, or custom wheels the insurer will otherwise ignore. | Find the original receipts. If you can't, take clear photos of the upgrades themselves. |

| Original Window Sticker | The best source for listing every factory-installed option, package, and special trim. | If you don't have it, try searching online for your vehicle's VIN to find a replica or build sheet. |

| Pre-Accident Photos | Shows the excellent cosmetic condition of your car before the crash. | Look through your phone's photo gallery for pictures from trips, holidays, or just a day it looked really clean. |

Putting this portfolio together is one of the most important things you can do. To see how it fits into the bigger picture, check out our complete guide on what to do when your car is totaled.

How to Talk to the Claims Adjuster

That first phone call with the insurance adjuster sets the tone for everything that follows. You need to be cooperative and honest, but you also have to be smart and strategic.

Stick to the undisputed facts of the accident. Don't volunteer extra information, and absolutely do not speculate on things you aren't sure about. Never, ever admit any fault or even say something as simple as "I'm so sorry." These phrases can be twisted and used against you later.

It's also wise to avoid giving a recorded statement right away. You are rarely required to provide one on the spot. Give yourself time to calm down, collect your thoughts, and gather your documents. Always remember: the adjuster's job is to settle the claim for as little as possible. Your job is to make sure you get the fair, full value you're owed.

How to Challenge and Negotiate a Low Settlement Offer

When that total loss settlement offer from the insurance company finally lands, it’s a make-or-break moment. Let's be clear: their first offer is almost never their best offer. Think of it as the starting point in a negotiation, not the final word.

If the number they gave you feels way off, trust your gut. It probably is. Insurers rely on third-party valuation reports that are notorious for errors, omissions, and bad data that consistently undervalue cars just like yours. Pushing back isn't just an option; it's often the only way to get the fair payout you're entitled to.

Dig Into Their Valuation Report

Your first move is to ask the adjuster for a complete copy of the valuation report they used. This document, often from providers like CCC ONE or Mitchell, is the "proof" behind their offer. Don't just skim it. You need to go through it line by line, looking for the mistakes that are costing you money.

I've seen the same errors pop up time and time again. Here's what to look for:

- Wrong Trim and Options: Did they list your top-tier Limited model as a base-level LE? It happens all the time. Adjusters often default to the most basic version of a car, completely ignoring valuable factory-installed features like a sunroof, premium audio system, or advanced safety package.

- Unfair Condition Rating: The report will grade your car's pre-accident condition (e.g., "average," "good," etc.). If you meticulously maintained your vehicle and it was in great shape, a generic "average" rating is a huge red flag. This is where your pre-accident photos and service records become your best evidence.

- Mileage Typos: It sounds simple, but a single misplaced digit can slash hundreds, even thousands, off your car's value. Double-check that the mileage on the report is exactly what was on your odometer when the accident happened.

Once you find these mistakes, make a list. Send it to the adjuster along with your proof—photos, window sticker, repair receipts. This isn't just complaining; it's a fact-based counter-offer that forces them to defend their numbers.

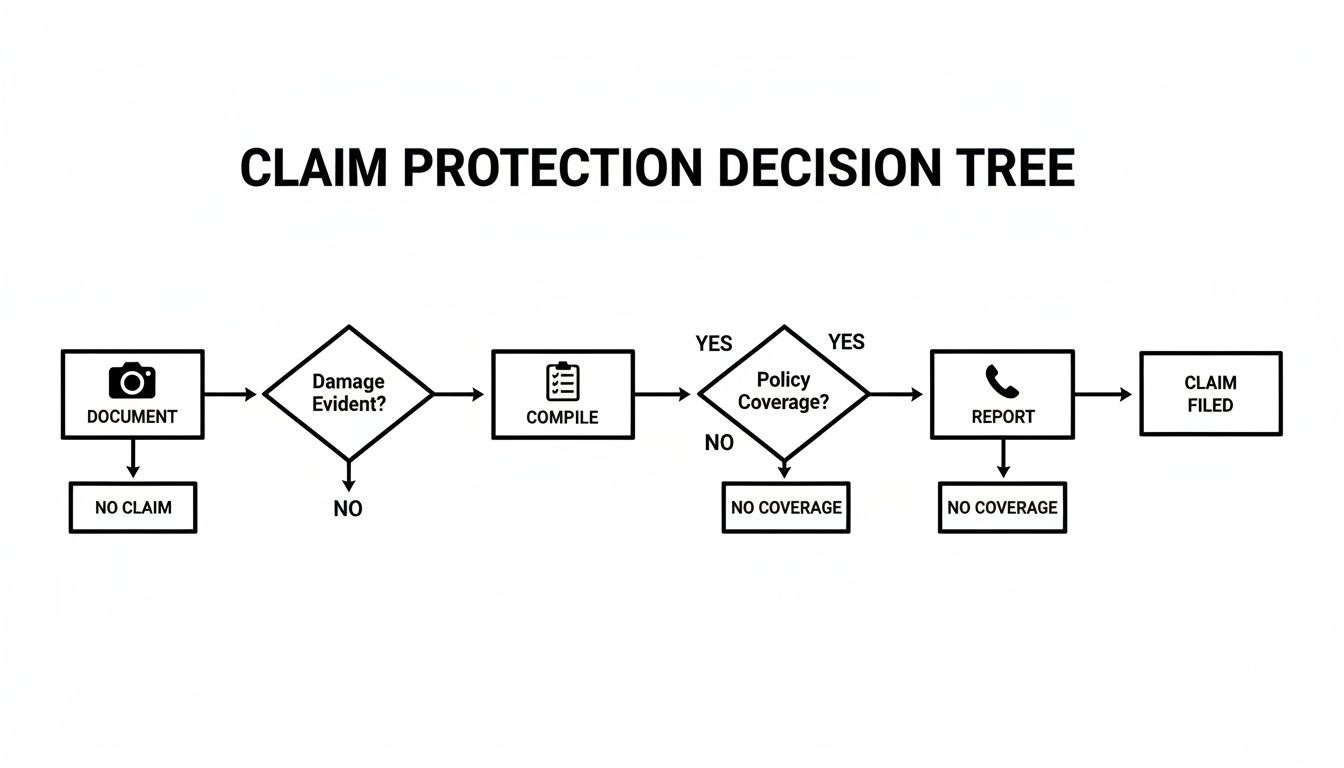

This flowchart breaks down the basic, but powerful, steps of building your case.

It really is that simple: methodical documentation turns a weak claim into a strong, well-supported argument for a higher payout.

The Appraisal Clause: Your Secret Weapon

So, what do you do when the adjuster digs in their heels and refuses to budge? You play the trump card hidden in your auto insurance policy: the Appraisal Clause.

The Appraisal Clause is a policyholder's right. It essentially takes the decision out of the insurance company's hands and puts it in front of independent experts. Two certified appraisers—one you hire, one they hire—are tasked with determining the vehicle's true Actual Cash Value.

Here’s a quick rundown of how it works:

- You hire your own certified, independent appraiser. This is an expert who will build a valuation from the ground up using real-world market data for your specific vehicle in your local area.

- The insurance company hires their own appraiser.

- The two appraisers then negotiate to land on an agreed-upon value. If they can’t reach an agreement, they bring in a neutral third-party "umpire" who makes a final, binding decision.

Suddenly, the playing field is level. The process forces the insurer to contend with an expert who knows value inside and out. The end result is almost always a settlement that's significantly better than that initial lowball offer. For a deeper dive, check out our complete guide on how to negotiate a total loss settlement.

Why an Independent Look Matters So Much Right Now

Insurers have more incentive than ever to undervalue totaled vehicles. Total loss claims are on the rise, and with 73% of valuations being done on cars that are seven years or older, it’s easier for them to justify low payouts.

On top of that, 26% of drivers now have deductibles of $1,000 or more, making a fair settlement absolutely critical. For those of us in places like the Pacific Northwest, their algorithms often use national data that doesn't reflect our stronger local car values. Hiring a local specialist who understands your market corrects that flaw and ensures the valuation is based on what your car was actually worth, right where you live.

So, What Happens After You Settle?

After all the phone calls, paperwork, and negotiation, you and the insurance company have finally landed on a settlement number. That's a huge step, but you're not quite done. You’ve hit a final fork in the road: what do you do with the wrecked car?

Your decision here boils down to two main paths. You can sign over the title, take the full check, and walk away. Or, you can choose to keep the car, a route known as retaining salvage. Each path has its own set of rules and consequences, so it's a decision you'll want to think through carefully.

Path 1: Surrendering the Vehicle

By far the most common and straightforward choice is to let the insurance company have the car. You sign the title over to them, they hand you a check for the full settlement amount, and they tow the car away. It's a clean break.

From there, the insurer will typically sell the car at a salvage auction to recoup a small portion of what they paid you. For you, the ordeal is over. You can take your settlement money and start shopping for a new ride without the headache of a mangled vehicle sitting in your driveway.

What if you still have a loan? The process is a bit different. The insurance company will pay your lender first. If the settlement is more than your loan balance, you get a check for the difference.

Heads Up: If you owe more on your loan than the car's ACV (a situation often called being "upside down"), you are still on the hook for that remaining loan balance. This is the exact scenario where Guaranteed Asset Protection (GAP) insurance becomes a lifesaver, as it’s designed to cover that very gap.

Path 2: Retaining Salvage

Your other option is to keep the damaged car. When you retain salvage, the insurance company still pays you, but they subtract the car's salvage value from your settlement check.

Let's say your car's ACV was agreed to be $15,000 and the insurer calculated its salvage value (what it would get at auction) at $2,000. If you choose to keep the car, they will cut you a check for $13,000. The car is now yours, but this is where a whole new chapter begins.

The Realities of a Salvage Title

The moment you decide to retain salvage, your car's title gets a permanent mark. The DMV will issue a salvage title (or a similar "salvage certificate"), officially branding it as a total loss.

This isn't just a piece of paper. A car with a salvage title is not street legal. You can't register it, you can't get insurance for it, and you certainly can't drive it on public roads. To bring it back to life, you'll have to jump through several hoops:

- Repair Everything: You’ll need to get the car fully repaired, which often means pouring a good chunk of your settlement money right back into the vehicle.

- Pass a State Inspection: A certified inspector will need to go over the vehicle with a fine-tooth comb to ensure all repairs meet safety and operational standards.

- Apply for a Rebuilt Title: Once it passes inspection, you can apply for a rebuilt title. This new title makes the car legal to drive, register, and insure again.

However, that "rebuilt" brand sticks with the car forever, which will drastically lower its resale value down the road.

Choosing to keep your totaled car is a serious commitment. It can make sense if you're a skilled mechanic or know someone who can do the work affordably. But for most people, the hassle, expense, and permanent hit to the car's value make surrendering it the much more practical option.

Common Questions After a Total Loss

Even when you know the steps, a total loss claim can throw some curveballs. It’s a confusing process, and it’s completely normal to have a lot of specific questions pop up along the way.

Let’s dig into some of the most frequent concerns people have. My goal here is to give you straight, practical answers based on years of experience dealing with these claims.

Will My Insurance Rates Go Up After a Total Loss?

This is probably the number one question on everyone's mind. The short answer is, it all comes down to who was at fault.

If another driver was 100% at fault, their insurance company foots the bill, and your rates shouldn't be affected. But if the accident was your fault, you can almost certainly expect your premiums to go up when your policy renews. How much? That varies wildly depending on your insurance company, your driving history, and where you live.

One thing to keep in mind: even if you weren't at fault, some insurers might view a total loss on your record as a minor risk factor down the line. It's not a guarantee, but it's something to be aware of.

How Long Do I Get a Rental Car For?

Most auto policies have rental car reimbursement, but the coverage is anything but unlimited. Your policy will spell out the limits, which usually look something like a $40 per day cap and a $1,200 total maximum.

Here’s the catch: the clock starts ticking once the insurance company makes a settlement offer. Most insurers will only cover your rental for a few days after that. This puts you in a tough spot, scrambling to get your settlement check, pay off any auto loan, and find a new car before the coverage runs out.

Expert Tip: Never let the rental car deadline pressure you into accepting a bad offer. A rushed settlement could cost you thousands. It's far better to pay for a few extra rental days out-of-pocket than to leave a huge chunk of your car's value on the table.

What Happens If My Totaled Car Is a Lease?

Totaling a leased car works a lot like totaling a financed one, but the money trail is different. The insurance settlement check goes straight to the leasing company—it never passes through your hands.

The leasing company applies that payment to what you still owe on the lease. If the settlement is more than the buyout amount (a rare but happy occasion), you might actually get a check back for the difference. More commonly, you’ll find that the car's value is less than what you owe, leaving you with a bill.

This is exactly why GAP insurance is so critical for a lease. In fact, most lease agreements make it mandatory for this very reason.

What Is Diminished Value and Can I Make a Claim?

Diminished value is the drop in a car’s resale value that happens after it's been in an accident, even if it’s repaired perfectly. A car with an accident on its record is simply worth less than the same car with a clean history.

However, you can't claim diminished value when your car is a total loss. Why? Because the entire concept is based on a repaired vehicle. A total loss settlement is supposed to pay you the car's full, pre-accident value, so there's no "repaired" value to be diminished.

The only scenario where this might be relevant is if you're in a third-party claim (the other driver was at fault) and you're arguing that your car should have been repaired instead of totaled. These are tough, complex cases that almost always require professional help to argue successfully.

If you're in Washington or Oregon and your insurer is digging in their heels with a lowball offer, don't just accept it. Total Loss Northwest provides independent, certified auto appraisals that force insurance companies to acknowledge real market data. We invoke the Appraisal Clause in your policy to fight for the fair settlement you're legally entitled to. Get an expert in your corner by visiting us at https://totallossnw.com.