When an insurance company lowballs their settlement offer, a professional, third-party insurance car appraisal is your most powerful tool. It’s an independent valuation that establishes your vehicle’s true market value, giving you the evidence needed to fight back after a total loss or diminished value incident.

What an Insurance Car Appraisal Really Means for You

After a wreck, your insurance company will send you a settlement offer based on their own internal math. Let's be clear: this isn't a friendly suggestion. It's a number calculated to protect their bottom line. An independent insurance car appraisal is your formal, evidence-backed counteroffer.

Think about it like selling a house. You would never let the buyer's agent set the final price without getting your own appraisal, right? The same principle applies here. In a total loss claim, the insurance company is effectively buying your wrecked car, and their primary goal is to pay as little as possible.

Why Your Insurer's Offer Is Just a Starting Point

Insurance companies aren't evil, but they are for-profit businesses. That simple fact shapes every step of the claims process. Recent market trends, which saw many insurers paying out more in claims than they collected in premiums, have only made them more aggressive about controlling costs.

This financial pressure means adjusters often rely on automated valuation tools that can miss the unique details of your vehicle. These computer systems frequently overlook recent upgrades, regional market conditions, or the true impact of diminished value. For a deeper dive into the market forces at play, the 2025 U.S. P&C Insurance Market Report offers some great insights.

To put it simply, there's a fundamental conflict of interest between what your insurer wants to pay and what your car is actually worth. The table below breaks it down.

Insurer Appraisal vs Your Goal: A Quick Comparison

| Aspect | Insurance Company's Goal | Vehicle Owner's Goal |

|---|---|---|

| Primary Motivation | Minimize claim payout to maintain profitability. | Maximize settlement to be made financially whole. |

| Valuation Method | Use automated tools and averages that favor a lower value. | Document the vehicle's true, fair market value with real-world comparables. |

| Outcome Focus | Settle the claim as quickly and cheaply as possible. | Receive enough money to replace the vehicle or cover the loss in value. |

This table highlights why you can't just take their first offer at face value. Their goal is fundamentally different from yours.

An insurer's valuation is designed to serve their financial interests. An independent appraisal is designed to serve yours by documenting the actual cash value you are rightfully owed.

When an Independent Appraisal Becomes Essential

So, when is it time to stop arguing and bring in a professional? Two situations almost always call for an expert second opinion:

- Total Loss Claims: This is the big one. Your car is declared a total loss, and the insurer offers you a check for its "Actual Cash Value" (ACV). If that number feels low—and it often is—an appraisal is your official path to disputing it.

- Diminished Value Claims: Your car is repaired, but it now has an accident on its record. That permanent loss in resale value is called diminished value. An independent appraisal calculates this loss so you can claim it from the at-fault driver's insurance.

In either case, the objective is the same: to make sure you get the money you're truly owed. The insurer's offer is just an opening bid. An independent appraisal gives you the ammunition to negotiate from a position of strength.

2. Understanding the Different Types of Car Appraisals

When you hear the word "appraisal" tossed around during an insurance claim, it's easy to think all valuations are the same. But they're not. Far from it. Knowing the difference between the various types is the first step toward taking control of your claim and getting the money you're actually owed.

Let's be clear: not all appraisals are created equal. The most important distinction to grasp is the one between what your insurance company does behind the scenes and what a certified, independent professional does on your behalf.

The Insurer's Valuation: A Starting Point, Not the Final Word

Right after an accident, your insurer will perform what they call a valuation. Honestly, it’s less of a true "appraisal" and more of a quick calculation. They typically plug your car's details into third-party software like CCC ONE or Mitchell, which spits out a number based on broad market data.

While this system is fast and cheap for them, it's often a raw deal for you.

- It’s Automated: The software can’t see the new tires you just bought, the meticulous service records you kept, or the high demand for your specific trim package in your local area. It misses the details that add real value.

- It’s a Black Box: You almost never get to see the full report or the "comparable" vehicles they used. This makes it incredibly difficult to argue with their math because you can't even see how they got there.

- It’s Inherently Biased: Let’s face it, the system is built to serve the insurer's bottom line, which means producing a conservative value that minimizes their payout.

You have to treat the insurance company's initial number as what it is: their opening offer. It's not the final word on what your car was worth.

Independent Car Appraisals: Your True Advocate in the Fight

This is where you turn the tables. An independent insurance car appraisal is a detailed, evidence-based valuation performed by a certified, unbiased expert that you hire.

Unlike the insurer's automated estimate, an independent appraisal is a comprehensive report built from the ground up. It’s designed to reflect your car’s actual pre-accident condition and fair market value. An independent appraiser digs deep into the details that the insurance company’s software glosses over.

An independent appraiser works for you, not the insurance company. Their only job is to determine and document the true, fair market value of your vehicle using solid evidence and professional expertise.

This process gives you the powerful documentation needed to formally dispute a lowball settlement offer and negotiate from a position of strength. Within this category, there are two main types of appraisals you might encounter.

Total Loss Appraisal: Determining Your Car’s Pre-Accident Value

A total loss appraisal comes into play when the insurance company declares your car a "total loss," meaning the repair costs are more than the vehicle is worth. The entire goal of this appraisal is to pin down your vehicle's Actual Cash Value (ACV) the moment before the crash happened.

A certified appraiser will:

- Conduct a Thorough Inspection: They’ll physically examine the vehicle (if possible) or use extensive photos to document its precise condition, options, and mileage.

- Find Real-World Comps: They hunt down actual, local sale listings for vehicles of the same make, model, year, and condition to prove what it would really cost to replace your car in your market.

- Adjust for the Details: They make specific value adjustments for things like aftermarket upgrades, major recent maintenance (like a new transmission), and its overall pristine condition.

The final product is a robust report that presents a realistic, defensible replacement value for your vehicle. It's the hard evidence you need to push back against the insurer's low offer.

Diminished Value Appraisal: Calculating Your Car’s Lost Resale Worth

A diminished value appraisal is for a different, but equally frustrating, situation. This is for when your car is repaired after an accident that wasn't your fault. Even with flawless repairs, your car is now saddled with an accident history that permanently damages its resale value.

That loss in value is called inherent diminished value. An appraiser calculates the difference between what your car was worth right before the accident and what it's worth now with that accident on its record. This report becomes the foundation of your claim against the at-fault driver's insurance to compensate you for that very real financial hit.

Trying to recover diminished value without this kind of expert documentation is next to impossible.

How Repair Costs and Valuations Affect Your Claim

Ever wondered why your insurance company seems so eager to total your car, even when the damage doesn't look that bad? It all comes down to the skyrocketing cost of fixing modern vehicles. This trend has a huge impact on how your claim is handled and, more importantly, how much you get paid.

Today's cars are essentially computers on wheels. All those great safety features—lane-keep assist, adaptive cruise control, automatic braking—run on a complex network of sensors, cameras, and computers. They keep you safe, but they also make repairs incredibly expensive.

What used to be a simple bumper replacement after a minor fender-bender is now a major operation. It requires recalibrating sensitive electronics, running deep diagnostic scans, and hiring specialized technicians. These hidden costs can easily make a repair bill balloon out of control.

The New Math of Total Loss Claims

For your insurance company, the decision to repair your car or call it a total loss isn't emotional; it's pure math. They weigh the estimated repair bill against your car's Actual Cash Value (ACV). Once the repair costs hit a certain percentage of the ACV—a threshold that varies by state—they'll cut their losses and write you a check.

You can learn more about how insurers determine this number in our guide on what is actual cash value of my car?.

This creates a powerful, and frankly lopsided, incentive for the insurance company. As repair costs for tech-heavy cars climb, it becomes cheaper for them to just declare the car a total loss. This move caps their payout at the ACV, protecting them from a potentially massive repair bill.

The real kicker? The ACV they offer is often a lowball figure spit out by their own software. So, they get to use high repair costs to justify totaling your car, and then turn around and offer a low valuation for that very same car. It's a one-two punch that can leave you with a settlement that's nowhere near enough.

This is precisely why an independent insurance car appraisal is so critical. It shifts the conversation back to your vehicle’s true pre-accident market value, not just the number that works best for the insurer's bottom line.

This trend is fueled by the advanced driver-assistance systems (ADAS) now standard in most vehicles. A staggering 87% of appraisals coming from insurer-preferred body shops now include diagnostic scans. On top of that, complex electronic calibrations are needed in 32% of all claims. These aren't just minor add-ons; they dramatically inflate repair estimates, pushing more and more cars over the total loss finish line.

How Technology Complicates Valuations

The very same technology that drives up repair costs also makes getting an accurate insurance car appraisal more challenging—and more necessary than ever. The automated valuation tools that insurance companies rely on are notorious for missing the details that add real value to a modern car.

Think about what their software often overlooks:

- Advanced Driver-Assistance Systems (ADAS): A premium tech package can add thousands to a car's original price, and that value doesn't just disappear overnight.

- Customizations and Upgrades: Whether it's a performance tune, a high-end sound system, or custom wheels, these modifications add real-world value that generic databases ignore.

- Pristine Condition: If you’ve meticulously maintained your car, it commands a higher price in the used market. A standard valuation tool simply can't see that.

If you don't fight back with your own appraisal, these value-adding features get wiped off the books, and you're left with a settlement offer that won't come close to replacing what you lost. As the industry leans more on technology like automated claims processing solutions, the risk of these nuances getting lost only grows.

An expert appraiser makes sure your high-tech, well-cared-for, or customized vehicle is valued for what it truly is, not just another generic entry in a spreadsheet.

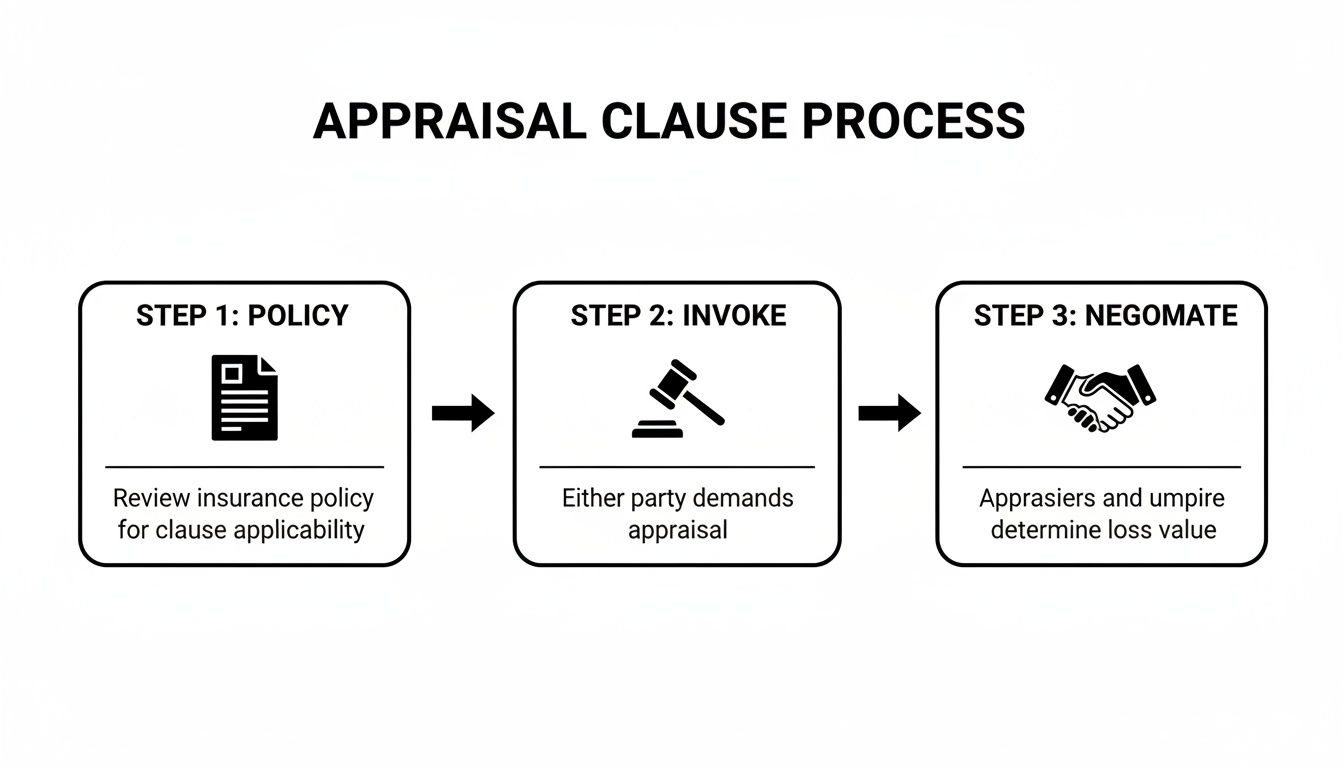

Using the Appraisal Clause in Your Policy

Tucked away in the fine print of your auto insurance policy is a powerful tool most people don't even know they have: the Appraisal Clause. This isn't just a bunch of legal gobbledygook; it's your contractual right to formally challenge an insurance company's lowball offer.

Think of it as the official "tie-breaker" clause. When you and your insurer are stuck in a stalemate over what your car is worth, invoking this clause takes the decision-making power away from them. It kicks off a structured process designed to land on a fair number based on real evidence, not just the insurer's software.

What Is the Appraisal Clause?

The Appraisal Clause lays out a specific game plan for settling valuation disputes. When you trigger it, both you and the insurance company have to hire your own independent appraiser to determine the vehicle’s actual cash value. In short, it forces a professional-level negotiation.

This is your ace up the sleeve. Instead of going back and forth with an adjuster whose job is to settle claims for as little as possible, you’re bringing in an expert who works for you. Their only goal is to argue for your car’s true market value. Getting a handle on how the insurance appraisal clause works is the first step to leveraging it.

How the Process Functions as a Tie-Breaker

Once both sides have an appraiser, the two experts first try to work it out and agree on a value. If they can shake hands on a number, that amount becomes the binding settlement. Simple enough.

But what happens if they can't agree? This is where the real magic happens.

The two appraisers then have to agree on a neutral third party, called an umpire. The umpire acts as a referee, reviewing the reports and evidence from both appraisers. A final, binding decision is made when any two of the three parties—your appraiser, the insurer's appraiser, or the umpire—sign off on a value.

This structure is a game-changer because it takes the final say completely out of the insurance company's hands. The outcome is decided by a majority vote among experts, which is a far cry from a one-sided negotiation where they hold all the cards.

Of course, this isn't free. You'll have to pay for your own appraiser and usually split the cost of the umpire with the insurer. While that's an upfront investment, the return—a significantly higher settlement—often makes it more than worth it, especially if your car was in great shape or had unique features. When the insurer’s offer feels wrong, knowing how to reject an insurance settlement offer and activating the appraisal clause is your path forward.

Invoking this clause completely changes the dynamic. It sends a clear signal to your insurance company that you mean business and you’re ready to prove your vehicle's worth with hard evidence. This one little provision is often the key that unlocks the fair settlement you deserve.

How to Get an Independent Appraisal Step by Step

That sinking feeling you get from a lowball settlement offer is awful, but it's not the final word. Think of it as the starting pistol for taking back control. Getting an independent insurance car appraisal is a clear, methodical way to arm yourself with expert evidence and fight for what your car was actually worth.

Let's walk through exactly how it's done.

Step 1: Formally Dispute the Insurer's Offer in Writing

Your first move is simple but non-negotiable: you have to formally reject the insurance company’s offer in writing. A phone call won't cut it. You need to create a paper trail.

Your letter doesn't need to be aggressive or long-winded. You just need to state clearly that you don't accept their valuation, you believe it doesn't reflect your vehicle's fair market value before the accident, and that you intend to get an independent appraisal. This puts them on notice and officially preserves your rights.

This is also the moment you’ll typically invoke the Appraisal Clause in your policy, kicking off the formal dispute resolution process laid out in your contract.

Step 2: Find and Hire a Certified Independent Appraiser

This is easily the most critical decision you'll make in this entire process. You need a genuine expert—someone who is certified, has years of experience, and truly understands the local car market. Be wary of generic, nationwide services that often miss the crucial details of your specific region.

When you're looking for the right person for the job, focus on these key qualifications:

- Certifications: Are they certified by a recognized professional appraisal organization?

- Specialization: Do they focus specifically on total loss and diminished value claims? A general appraiser might not have the niche expertise needed to win.

- Local Market Knowledge: An appraiser who knows the Washington and Oregon markets will find much stronger, more relevant comparable vehicles to build your case.

- Real Reviews: Look for testimonials from people who were in your exact situation.

If you’re not sure where to begin, the goal is to find a certified and experienced independent auto appraiser near you who specializes in fighting lowball insurance offers.

Step 3: Gather All Your Documentation

While your appraiser handles the expert analysis, you can give your claim a massive boost by providing them with every piece of paper you have on your car. You're essentially building a case file that proves your vehicle's history and condition. The more evidence you have, the stronger the final report will be.

Your vehicle is more than just a year, make, and model. Maintenance records, photos, and receipts are the hard evidence that proves its unique value and separates it from the generic, run-of-the-mill examples the insurer wants to use.

Pull together everything you can find, including:

- Maintenance and Service Records: This is proof that you took great care of your car.

- Receipts for Recent Major Work: Did you just put on new tires or have the transmission serviced? Those receipts add real value.

- Photos of the Vehicle Before the Accident: If you have any, these are absolute gold. They visually document the car’s excellent pre-loss condition.

- Original Window Sticker: This is often overlooked, but it lists all the factory options and packages that can add thousands to the value.

This paperwork allows your appraiser to make specific, justifiable adjustments that push your vehicle’s value well above the baseline.

Step 4: Cooperate with the Appraisal and Review the Report

Once you’ve hired your expert, they’ll get to work. This involves a meticulous inspection of the vehicle (when possible) and deep research into the local market. The final product is an incredibly detailed report, often 20-30 pages long, that breaks down your car’s features, its condition, and a list of true comparable vehicles for sale in your area.

This level of detail is why a rushed, software-generated valuation is so frustrating for owners. In fact, a recent J.D. Power study found that only 51% of customers with high-value vehicles are likely to stick with their insurer, partly because they feel the unique aspects of their car are completely ignored by generic tools.

Once the report is ready, sit down with your appraiser and go through it. They’ll explain exactly how they determined the value and answer all your questions. This is key—you need to understand the evidence before it goes to the insurance company.

The infographic below gives you a bird's-eye view of the process that begins once you invoke the Appraisal Clause.

This simple, three-step framework transforms your claim from their take-it-or-leave-it offer into a structured negotiation between experts.

Step 5: Submit the Appraisal and Negotiate

Armed with your comprehensive appraisal report, you submit it to the insurer as your official counteroffer. This completely changes the conversation. It's no longer just your opinion against theirs; it’s your expert's detailed, evidence-backed report against their automated software.

From here, your appraiser typically takes the lead, negotiating directly with the insurance company's appraiser. If the two experts can agree on a number, that value becomes binding. If they can't, the umpire process kicks in to break the deadlock. This structured, methodical approach is your best shot at getting the fair settlement you deserve.

Common Questions About Car Appraisals

Even after getting the basics down, you probably still have a few questions rolling around in your head. That’s completely normal. This whole insurance appraisal process can feel a bit overwhelming, but clearing up the common sticking points can give you the confidence you need to move forward.

Let's break down some of the most frequent questions people ask when they're staring down a lowball offer from their insurance company.

How Much Does an Independent Appraisal Cost?

This is usually the first thing people want to know, and for good reason. For a high-quality, independent appraisal on a total loss or diminished value claim, you can expect to pay somewhere between $300 and $750.

I know that might sound like a lot of money to spend out of pocket, but it’s best to think of it as an investment. A solid, well-documented appraisal from a certified pro can boost your final settlement by thousands, sometimes even tens of thousands, of dollars. The return on that initial cost is often huge.

Put it this way: spending a few hundred bucks to potentially get back several thousand is a smart, calculated move. The real key is to steer clear of "bargain" appraisers. A cheap report that gets tossed aside by the insurer is just wasted money; a quality report that wins your case is an investment in getting what you’re truly owed.

Is an Appraisal Worth It for My Car?

The next logical question is whether the potential payout makes sense for your specific car. While every situation is unique, getting an independent appraisal is almost always the right call if you believe the insurance company's offer is off by $1,000 or more.

Here are a few times when an appraisal really pays off:

- Well-Maintained Vehicles: If you have a stack of service records and kept your car in pristine shape, an appraisal can prove that superior condition—something automated valuation tools completely miss.

- Vehicles with Upgrades: Did you add custom wheels, a killer sound system, or recently shell out for a new transmission? An appraiser can quantify that added value.

- High-Demand Models: If your specific car, truck, or SUV is a hot item in your local area, an appraiser can pull real-world sales data to prove it’s worth a premium.

At the end of the day, if there's a big gap between the insurer's offer and what it would actually cost you to buy a similar car today, an appraisal is your strongest weapon to prove it.

What Is the Timeline for the Appraisal Process?

Patience is a virtue here, because a proper appraisal doesn't happen overnight. It's a methodical process built for accuracy, not speed. From the day you officially invoke the Appraisal Clause until you have a check in hand, the timeline can vary quite a bit.

Here’s a general roadmap of what to expect:

| Stage | Typical Duration | Notes |

|---|---|---|

| Hiring an Appraiser & Gathering Docs | 1-3 Business Days | You can get a head start by having your documents ready to go. |

| Appraiser's Inspection & Research | 5-7 Business Days | This is where the real work happens—finding comps and building your case. |

| Negotiation Between Appraisers | 7-14 Business Days | This part depends on how complex the case is and how quickly the insurer's appraiser responds. |

| Umpire Process (If Needed) | 14-21 Additional Days | If the two appraisers hit a wall, bringing in an umpire adds another layer to the process. |

All told, a straightforward case might be wrapped up in three to four weeks. But if things get complicated and an umpire is needed, it could stretch to six weeks or more. It definitely takes longer than just cashing the first check, but the wait often leads to a much, much fairer settlement.

What Happens If the Appraisers Cannot Agree?

This is where the Appraisal Clause really shows its teeth. If your appraiser and the insurance company’s appraiser can't see eye-to-eye, the process doesn't just grind to a halt. It’s specifically designed to break a stalemate.

The two appraisers are required to agree on a neutral, third-party expert called an umpire.

Here’s how the umpire system works to get to a final number:

- Selection: Both appraisers have to agree on a qualified, impartial umpire to act as a tie-breaker.

- Review: The umpire then reviews all the evidence and reports submitted by both sides.

- Final Decision: A binding settlement amount is locked in as soon as any two of the three parties (your appraiser, the insurer’s appraiser, or the umpire) sign off on a value.

This "majority rules" setup is brilliant because it prevents the insurance company from just digging in its heels and saying "no." The final decision is taken out of their hands and put into the control of a panel of experts. You typically split the cost of the umpire with the insurer, making it a structured and fair way to finally cross the finish line.

Don't let an insurance company's lowball offer be the final word on what your vehicle was worth. At Total Loss Northwest, we specialize in providing the certified, evidence-backed appraisals that force insurers to pay what you're rightfully owed. If you're in Washington or Oregon and ready to fight for a fair settlement, we’re here to help.