When an insurance adjuster tells you your car is a "total loss," what they're really saying is that it's cheaper for them to pay you for your car than it is to fix it. This decision starts a process where they have to figure out your car's Actual Cash Value (ACV)—basically, what it was worth on the open market moments before the crash.

From that ACV number, they'll subtract your deductible and cut you a check. That's the simple version, but the details are where things can get complicated.

Understanding Your Next Steps

Hearing your car is "totaled" is a gut punch, no doubt about it. But once you get past the initial shock, you'll find the path forward is a series of clear, manageable decisions.

At its heart, the insurance company is essentially buying your wrecked car from you. The big question, and the main point of negotiation, is the price. That price is the ACV. It’s not what you paid for it, and it has nothing to do with what you still owe on your loan. It’s all about what someone would have realistically paid for your exact car—same make, model, year, and condition—right before the accident. Getting a firm grip on this concept is your first and most important step toward getting a fair deal.

One of the very first things you'll need to do is learn how to file an auto insurance claim correctly. Getting this right from the start can make the entire process much smoother.

Why Cars Are Totaled More Often Now

If it seems like you’re hearing about more totaled cars these days, you’re not wrong. It's a real trend. Today, a staggering 30% of U.S. auto claims end up as total losses. For perspective, that’s way up from just 17.3% in 2014.

What’s going on? Two things: soaring repair costs and the incredible complexity of modern cars. With all the sensors, cameras, and computers packed into new vehicles, even a minor fender bender can lead to thousands in repair bills. Most states have a "total loss threshold," usually around 70-80% of the car's value. If the repair estimate crosses that line, the insurer declares it totaled.

Your Immediate Choices

Once the insurance company makes the call, the ball is in your court. You have a few main paths you can take, and your choice here sets the stage for everything that follows.

Here’s a quick breakdown of your options:

Your Initial Choices After a Total Loss Declaration

| Your Option | What It Means | Key Consideration |

|---|---|---|

| Accept the Settlement | You take the insurer's ACV offer, sign the title over, and they send you a check (minus your deductible). | This is the fastest and simplest path, but only if you're confident the offer is fair. |

| Negotiate the Settlement | You disagree with their ACV and present your own evidence (like ads for similar cars) to argue for a higher value. | This takes more work but is often necessary to get what your vehicle was truly worth. |

| Keep Your Car (Retain Salvage) | You decide to keep the damaged vehicle. The insurer pays you the ACV minus your deductible and the car's salvage value. | You'll get a salvage-branded title, which makes the car difficult to insure, register, and sell. |

Each path has its own pros and cons, so it's worth taking a moment to think about what makes the most sense for your situation.

Key Takeaway: Never forget that the insurer's first valuation is just an opening offer. You absolutely do not have to accept it if you feel it's too low. To get ready for that conversation, it's a good idea to understand what to do when your car is totaled so you can advocate for yourself effectively.

How Insurance Companies Calculate a Total Loss

When an insurance adjuster tells you your car is "totaled," it's not a gut feeling—it's cold, hard math. The decision boils down to a simple business calculation: are they better off paying to fix your car, or paying you its pre-accident value and selling the wreck for scrap?

The entire process hinges on what’s known as the Total Loss Formula. It’s the simple equation that determines whether your car gets a second chance or a one-way ticket to the salvage yard.

The Formula: If the Cost to Repair + the Salvage Value of your damaged car is more than its Actual Cash Value (ACV), it's officially a total loss.

Let's break that down. The Actual Cash Value (ACV) is what your car was worth right before the crash. The salvage value is what a company like Copart or IAA would pay for the wreckage. If the repair bill plus the scrap value is higher than the car's pre-accident worth, the insurance company will always choose to cut a check for the ACV. It just doesn't make financial sense for them to do anything else.

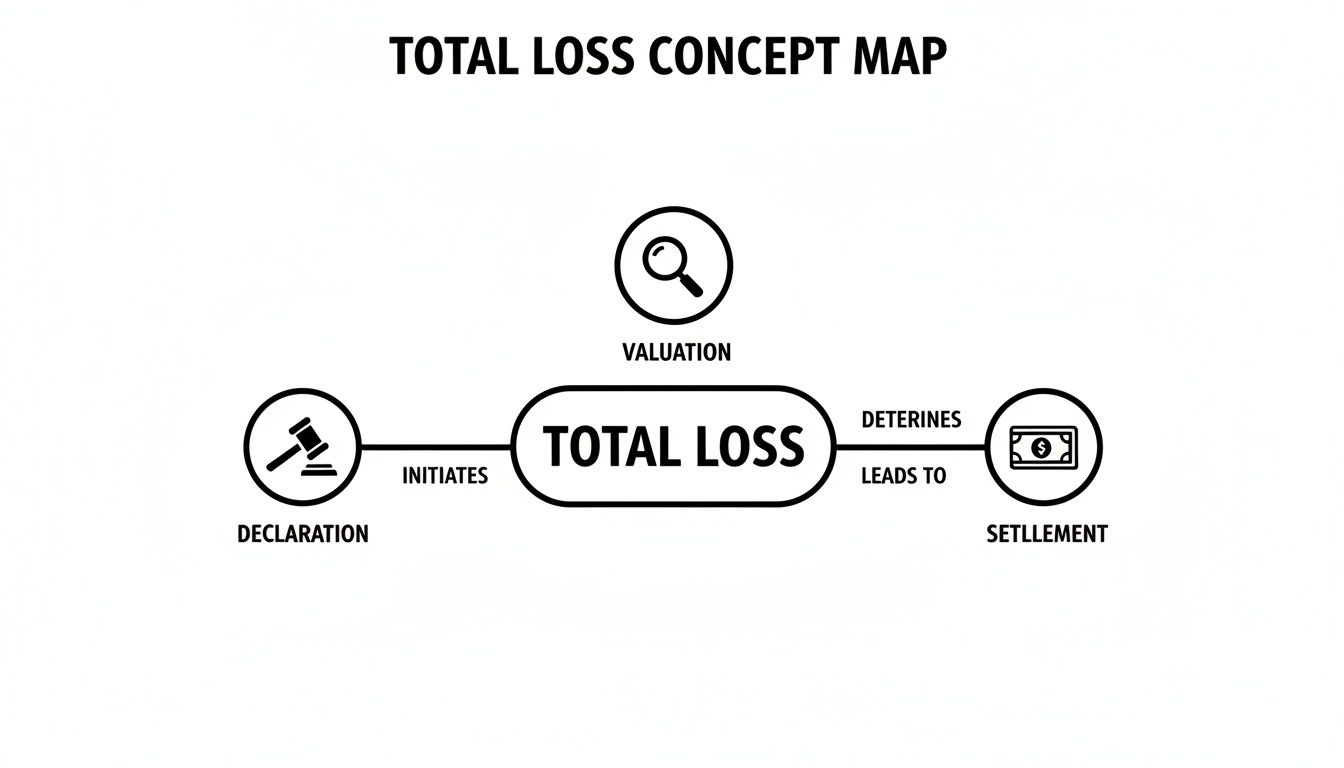

This flowchart lays out the journey from the initial accident to the final payout, showing how that crucial valuation step sits right in the middle of everything.

As you can see, that valuation is the most critical (and often the most disputed) part of the entire process. It directly controls the amount of money you end up with.

The Total Loss Threshold: Making It Official

To keep things consistent, states like Washington and Oregon have a Total Loss Threshold (TLT) written into law. This is a set percentage that acts as a tripwire. If the estimated repair costs exceed this percentage of your car's ACV, the insurer must declare it a total loss.

For instance, if your state has a 75% TLT and your car’s ACV is $20,000, any repair estimate over $15,000 means it’s automatically totaled. This rule prevents an insurance company from spending $19,000 to fix a car that was only worth $20,000 in the first place, only to hand you back a vehicle with a permanent accident history.

And it’s happening more and more. Recent industry data shows total losses made up 22.6% of claims, a huge jump from 18.0% just a year before. With cars on the road getting older and modern repairs getting more complex (and expensive), this trend isn't slowing down.

How They Decide What Your Car Was Worth

The entire settlement you're offered comes down to one number: the Actual Cash Value. This is where you, as the vehicle owner, are at a huge disadvantage.

Insurers don't pull up Kelley Blue Book and call it a day. They rely on powerful third-party valuation platforms—most commonly one called CCC ONE—to generate a report. In theory, this software scans databases for "comparable" vehicles that recently sold in your area to determine your car's value.

The problem is, the system is far from perfect, and the data adjusters work with can be seriously flawed. It's shockingly common for these reports to be built on faulty comparisons that conveniently lead to a lower ACV for you and a smaller payout from them.

Here are a few of the most common tricks and errors we see:

- Bad "Comps": Your low-mileage, fully-loaded vehicle gets compared to base models with twice the mileage and a shoddy history.

- Nitpicky Adjustments: They’ll dock you hundreds of dollars for "condition," citing tiny scratches or normal wear and tear that had zero real impact on your car's market value.

- Overlooked Value: The report completely ignores valuable options, like a premium sound system, a towing package, or high-end aftermarket wheels you added.

Getting a handle on how they build these reports is your first and best defense. When you know where to spot the mistakes, you can start fighting back for the fair settlement you actually deserve. For a deeper dive, read our guide on the complexities of calculating a total loss vehicle's value.

What Goes Into Your Final Settlement Payout?

After all the negotiation over your car’s Actual Cash Value (ACV), you finally have a number. But the check you get in the mail isn't just that ACV amount. It’s a final figure that comes from a bit of math—some additions and a few important deductions.

Think of the ACV as the starting line. From there, the insurance company starts adding and subtracting. Getting a handle on this formula is key to understanding what your final payout will really look like.

First, the Additions to Your Payout

Before they subtract anything, your insurer often has to add certain costs back into your settlement. These are meant to help make you "whole" by covering the unavoidable expenses that come with buying a replacement car.

A lot of people don’t realize this, but in states like Oregon and Washington, insurers are required to reimburse you for these specific costs. You’ll want to double-check your settlement breakdown for them:

- Sales Tax: The company should add the state and local sales tax you'd have to pay on a similar replacement vehicle.

- Title and Registration Fees: The cost to title a new car and transfer the registration is another common expense you're entitled to.

These might seem small, but they can easily add up to hundreds, sometimes thousands, of dollars. Always comb through that settlement letter to make sure they haven't been missed. If they’re not there, you have every right to ask for them to be included.

Next, the Deductions From Your Payout

Once the pluses are tallied, the insurer will make a couple of significant deductions that lower the amount of the check you'll actually hold in your hand. The first one is pretty straightforward and expected.

The second deduction, though, is where many car owners get a nasty financial surprise.

- Your Deductible: This is the amount you agreed to pay out-of-pocket when you signed up for your policy. If you have a $500 deductible, the insurer will simply subtract that from the total.

- Your Loan Payoff: If you still owe money on your car, the insurance company pays your lender first. The check goes directly to the lienholder, and you only get what's left over—if anything.

This brings up a huge, and often painful, question: what if you owe more on the loan than the car is worth?

The "Upside-Down" Loan and Why GAP Insurance Is a Lifesaver

Being "upside-down" or "underwater" on a car loan is a tough spot to be in, and it's surprisingly common. It just means your loan balance is higher than your car’s ACV.

Let's say you owe $22,000 on your loan, but the insurance company settles on an ACV of $18,000. They'll send that $18,000 straight to your lender, but you are still legally on the hook for the remaining $4,000. And you don't even have a car anymore.

This exact scenario is why GAP insurance exists. GAP, which stands for Guaranteed Asset Protection, is an optional policy that covers the "gap" between what your car is worth and what you still owe.

In our example, your GAP coverage would step in and pay that $4,000 difference to your lender. It saves you from having to pull that money out of your own pocket for a car that’s sitting in a salvage yard.

Without it, you'd be stuck making payments on a totaled vehicle while simultaneously trying to figure out how to afford a new one.

Should You Keep Your Totaled Car?

When the insurance adjuster delivers the news that your car is a total loss, it feels final. Most people assume the insurance company simply cuts a check and hauls the vehicle away. But there's another path you might not know about: you can actually choose to keep the car.

This is called "owner retention" or "retaining the salvage," and it’s an option in most states.

It sounds straightforward, right? Instead of the insurer taking your wrecked car to sell at auction, you hang onto it. But making this choice changes how they calculate your final payout. The adjuster will start with the car's Actual Cash Value (ACV), subtract your deductible, and then subtract one more crucial number: the salvage value. This is the amount they expected to get for the car at a salvage auction.

So, your payment formula looks like this: ACV – Deductible – Salvage Value = Your Payout. You end up with a smaller check, but the car is still yours.

The Reality of a Salvage Title

Before you even think about keeping your car, you need to understand the immediate, permanent consequence: the DMV will issue a salvage title. This isn't just a minor footnote on the paperwork; it's a permanent brand that fundamentally changes the car's legal status and value forever.

A salvage title acts as a permanent red flag to any future buyer, insurer, or mechanic. It officially declares that a professional insurance company once decided the vehicle was too damaged or too expensive to be worth repairing properly. This brand sticks with the car for the rest of its life, even if you restore it to showroom condition.

This single piece of paper can turn what seems like a smart financial move into a long-term, expensive headache.

Key Insight: A salvage title fundamentally redefines your vehicle. It will never be just a "used car" again. From that moment on, it is a "salvage vehicle," a label that carries significant financial and logistical baggage.

Weighing the Pros and Cons

Is retaining your salvage a hidden gem or a financial trap? The answer depends entirely on your specific situation, skills, and the vehicle itself.

When Keeping the Car Might Make Sense

For most drivers, this is the wrong move. But in a few specific scenarios, it's worth considering.

- You Have Serious Mechanical Skills: If you're a mechanic or a serious hobbyist who can do the work yourself, you can slash the repair bill by eliminating labor costs. This is the biggest single reason it can sometimes pay off.

- The Damage is Purely Cosmetic: Sometimes a car is totaled by something like a severe hailstorm that leaves it mechanically perfect but covered in thousands of dollars of cosmetic damage. If you don't mind driving a "golf ball," you could pocket the payout and keep a perfectly functional car.

- It's a Rare, Classic, or Highly Customized Vehicle: Standard insurance valuation tools are terrible at pricing unique cars. They don't account for rare parts, custom work, or sentimental value. If your insurer's ACV offer is way too low, rebuilding the car yourself might be the only way to make yourself whole.

The Major Downsides You Can't Ignore

For the average person, the challenges of a salvage title almost always outweigh the benefits.

- The Insurance Nightmare: Good luck getting full coverage. Most mainstream insurance companies won't offer collision or comprehensive policies on a salvage-branded car. Even finding liability insurance can be more difficult and expensive.

- Plummeting Resale Value: The moment that salvage title is issued, your car's value tanks by 20% to 40%—or even more. A fully repaired, beautiful-looking car will always be worth significantly less than an identical one with a clean title.

- The Rebuilding Gauntlet: You can't just fix it and drive it. To make the car legal for the road again, you have to navigate a complex state inspection process to earn a "rebuilt" title. This involves meticulous paperwork, receipts for parts, and proving the vehicle is safe, which can be a bureaucratic nightmare.

Keeping vs. Surrendering Your Totaled Vehicle

This is a direct comparison to help you decide whether retaining your totaled car is the right financial move.

| Factor | Surrendering to Insurer | Keeping the Vehicle (Retaining Salvage) |

|---|---|---|

| Payout | ACV – Deductible | ACV – Deductible – Salvage Value |

| Vehicle Title | Title is signed over to the insurer. | A permanent salvage title is issued by the DMV. |

| Effort Required | Minimal. Sign paperwork, get your check. | High. You must arrange for repairs, inspections, and new title. |

| Future Insurance | No issues insuring your next vehicle. | Extremely difficult to get full coverage; liability may be costly. |

| Resale Value | Not applicable. | Drastically reduced (20-40% lower than a clean title). |

| Best For | The vast majority of drivers. | Mechanics, experts, or owners of unique classic/custom cars. |

For owners of high-value or specialized vehicles, the algorithms insurers use often fail to capture the true market price, as detailed in this auto insurance trends report. They overlook unique modifications, rarity, and regional demand. When you're facing a lowball ACV offer, the idea of keeping the wreck can be tempting.

However, you have to weigh that reduced payout against the guaranteed headaches of a salvage title. For nearly everyone, surrendering the vehicle to the insurer is the cleaner, simpler, and financially safer decision.

How to Dispute a Lowball Settlement Offer

When the settlement offer from your insurance company finally arrives, that number can feel final. Like it or not, this is what they're paying. But what if the offer is just plain wrong?

The truth is, their first offer is just that—an offer. It's their opening bid in a negotiation you probably didn't even realize you were in. You are not stuck with it. If the amount feels low, you have every right to push back and fight for what your car was actually worth. The secret is to stop arguing and start proving your case with hard data.

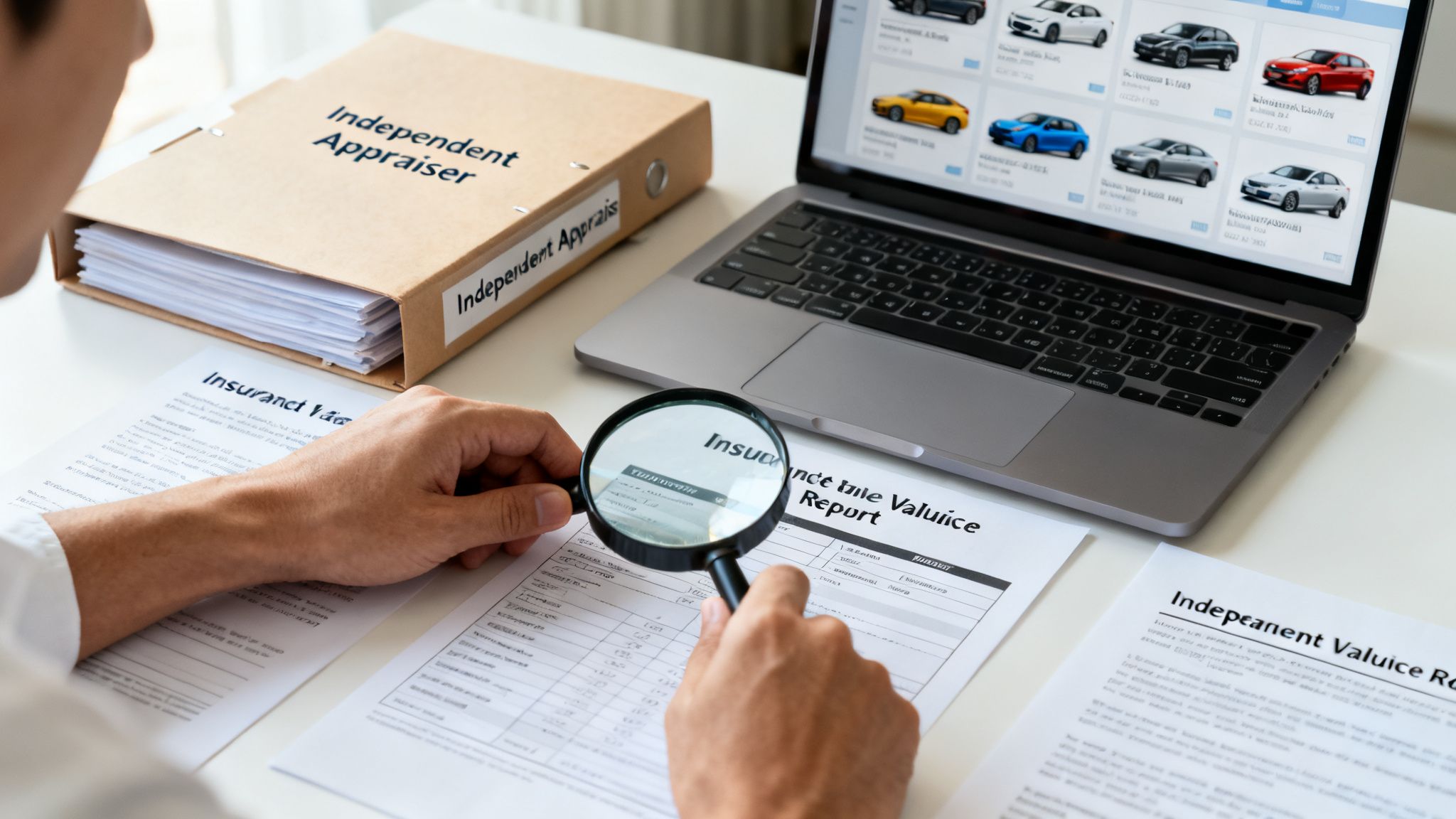

Your First Move: Scrutinize Their Report

Before you fire off an angry email, take a breath and ask the insurer for a complete copy of their valuation report. This document, often generated by third-party software like CCC ONE, is the "proof" behind their lowball number. Your job is to pick it apart.

Treat it like a detective at a crime scene. Look closely at the "comparable" vehicles they used to justify their price. Did they compare your pristine, low-mileage sedan to a beat-up former rental car with 50,000 more miles? Did they forget to add value for your premium sound system, sunroof, or brand-new tires? Every error, big or small, is money they've unfairly taken off your settlement.

Introducing Your Most Powerful Tool: The Appraisal Clause

Buried deep in the fine print of your insurance policy is a provision you've likely never heard of, but it’s the single most powerful tool you have: the Appraisal Clause.

This clause gives you the contractual right to hire your own certified, independent appraiser to come up with their own valuation. Invoking this clause takes the insurance company's biased software out of the picture. It forces them to deal with a real-world market analysis from an expert who is working for you, not them.

Key Takeaway: The Appraisal Clause is your contractual right to a second opinion. It legally requires your insurer to consider a valuation from an independent expert, leveling the playing field and putting power back in your hands.

A good independent appraiser doesn't just pull a number out of thin air. They build a rock-solid case for your car's true value.

Here’s how they do it:

- Finding True Comparables: They dig into the local market—not just a national database—to find vehicles that are a genuine match for yours in year, model, trim, mileage, and condition.

- Accounting for Uniqueness: They properly credit you for every option, every recent repair, and the overall excellent condition of your vehicle.

- Creating a Data-Backed Report: You get a comprehensive, professional report that systematically proves your car’s higher Actual Cash Value. This is what you’ll submit to the insurance company.

For a deeper dive into the process, check out our guide on how to negotiate your total loss settlement like a pro.

Presenting a Counteroffer

Armed with an independent appraisal, you're no longer just a frustrated customer complaining about a low number. You're presenting a documented, evidence-based counteroffer. This completely changes the conversation. The burden of proof is now on the insurer to explain why their computer-generated number is more accurate than an expert's detailed report.

Most of the time, this is enough to get the insurance company to come back with a much better offer. It’s hard to ignore a professionally prepared document that highlights the actual market reality.

If the insurer still refuses to budge, you may have to explore your legal options. It might be time to ask, "Can I sue if someone totaled my car?" While it’s a bigger step, it’s a valid path if the company refuses to negotiate in good faith. By following these steps, you can confidently challenge a weak offer and secure the fair payment you’re owed.

Your Top Questions About Total Loss Claims, Answered

When your car is declared a total loss, it can feel like you've been dropped into a whole new world with its own confusing language and rules. You're going to have questions, and getting straight answers is the first step toward getting through this process with your finances intact.

Let's cut through the jargon and tackle the most common questions we hear from vehicle owners every single day. From how long this will all take to what happens with your rental car, here’s the straightforward information you need.

How Long Does a Total Loss Claim Usually Take?

This is usually the first thing on everyone's mind. While no two claims are exactly alike, you can generally expect the entire process—from the day of the wreck to having a check in your hand—to take about 30 days.

That timeline isn't just a random number; it covers several critical steps. First, there's the initial investigation and vehicle inspection, where the adjuster figures out just how bad the damage is. Then comes the valuation, where they run the numbers to calculate your car's ACV. The final piece is settling the claim and handling all the paperwork.

Of course, that 30-day figure is an average. The clock can definitely run longer if there's a dispute over who was at fault or, more often, a disagreement over your vehicle's Actual Cash Value. If you have to push back, negotiate, or bring in an appraiser, be prepared for a longer timeline.

What Happens If the Other Driver Was at Fault?

If another driver caused the accident, you've got a choice to make. You can either file the claim through your own insurance company (this is called a first-party claim) or go directly after the at-fault driver's insurer (a third-party claim).

Going through the other person's insurance means their company is on the hook for your settlement. But don't make the mistake of thinking this makes things easier. Their primary goal is exactly the same as any insurer: to settle your claim for the absolute minimum amount possible.

Crucial Point: Even when you're the claimant and not the policyholder, the at-fault party's adjuster is working to protect their company's money, not yours. You have to be just as ready to challenge their valuation and fight a lowball offer.

They'll use the same process and the same software, like CCC ONE, to come up with your car's value. Never assume they’ll be generous just because their driver was in the wrong. You still have to be your own best advocate.

Will I Get a Rental Car While My Claim Is Processed?

Losing your car throws your whole life into chaos, so getting a rental is often an immediate need. Whether you get one—and for how long—boils down to the specific insurance policies involved.

If you have rental reimbursement on your own policy, that's great, but it always has limits. A typical policy might cover $40 per day with a total cap of $1,200, for example. If the other driver was at fault, their policy should cover a "comparable" rental for a reasonable amount of time.

But here’s the catch you need to watch out for: rental coverage almost always stops the moment the insurance company makes a formal settlement offer. They aren't going to pay for your rental for weeks while you negotiate with them or shop for a new car. This tactic puts a lot of pressure on you to accept their first offer and move on.

What Happens to My Personalized License Plates?

Got custom or vanity plates? Make sure you grab them off your vehicle before it gets hauled away for good. The insurance company only cares about the car; the plates are your personal property.

In most states, including Washington and Oregon, you can easily transfer your personalized plates to your next vehicle. It usually involves a trip to the DMV and a small transfer fee, but it's much simpler than ordering brand new ones. The best time to remove them is right away, while the car is still at the body shop or tow yard.

Can I Make a Diminished Value Claim on a Totaled Car?

This is a very common question, but the answer is a hard no. A diminished value claim is specifically for compensating an owner for the loss in a vehicle's resale value after it has been in a crash and then repaired. It's all about the stigma—the market reality that a car with an accident history is worth less than an identical one with a clean record.

A totaled car, by its very definition, isn't being repaired. Its value hasn't been "diminished"; it's been wiped out. The insurance company is effectively buying the wreck from you for its full pre-accident ACV. Since you're being paid for the car's entire undamaged worth, there's no remaining loss of value to claim.

Staring down a lowball settlement offer after your car has been totaled can feel defeating, but you don't have to take it. At Total Loss Northwest, we build ironclad, data-driven independent appraisals that compel insurance companies to pay what you are rightfully owed. We fight for your vehicle's true market value so you can get back on the road without taking a financial hit. Visit us at https://totallossnw.com to see how we can help.