So, what exactly is an independent car appraiser? Think of them as your personal expert, an unbiased professional you bring in to figure out your vehicle's true value, completely separate from the insurance company's influence. Their entire job is to be your advocate in a financial tug-of-war, making sure you get a fair shake after an accident.

This is crucial whether your car is a total loss or you're dealing with the diminished value of a repaired vehicle.

Your Advocate Against Unfair Insurance Offers

Let's be blunt: after a car accident, you and your insurance company are on opposite sides of the table. You want to be made whole again—to get back the full, pre-accident value of your car. The insurer, on the other hand, has a business to run, and their goal is to settle your claim for the lowest possible amount to protect their profits.

Their adjuster isn't a neutral referee; they are an employee of the insurance company. They typically rely on standardized software that spits out conservative, and often shockingly low, valuations. This is exactly where an independent car appraiser steps in. They work for you, and only you.

Leveling the Playing Field

An independent appraiser’s job is to challenge the insurance company's lowball number with a valuation grounded in objective, real-world evidence. They compile a detailed, comprehensive report that becomes your single most powerful tool in the negotiation.

This is a game-changer in two common situations:

- Total Loss Claims: If your insurer declares your car a "total loss," they'll cut you a check. An appraiser makes sure that check actually reflects what your car was worth on the open market right before the crash, not just some number from a cost-cutting algorithm.

- Diminished Value Claims: Your car might look perfect after repairs, but that accident on its history permanently lowers its resale value. An appraiser calculates this loss—the "diminished value"—so you can claim the compensation you're legally entitled to.

An independent appraiser doesn't just give you a "second opinion." They deliver a credible, market-supported valuation that an insurance company can't just brush aside. It shifts the conversation from your word against theirs to a serious negotiation based on documented facts.

An Unbiased Expert on Your Side

Hiring an appraiser isn't just about trying to get a bigger check; it's about ensuring the entire process is fair. They bring a level of expertise, local market knowledge, and an eye for detail that the insurer's adjuster—who might be juggling dozens of claims a day—simply can't match.

A true professional will conduct a hands-on inspection, dig into recent sales of comparable vehicles in your area, and factor in everything that made your car unique, from its pristine condition and regular maintenance to any special features or aftermarket upgrades.

In the end, an independent appraiser gives you the leverage you need. They build such a solid, undeniable case for your car’s true value that it forces the insurance company to either justify their low offer with hard evidence or come back to the table and negotiate in good faith. Without that expert in your corner, you're left arguing with a multi-billion dollar industry all by yourself.

The Difference Between Insurer Valuations and Independent Appraisals

When an insurance company values your car, they aren't sending out a team of market experts. Instead, they’re plugging a few basic details into proprietary software platforms like CCC ONE or Mitchell. The number that pops out is fast, cheap, and built to serve their financial interests, not yours.

Think of their software as a black box. It pulls data from a pool of vehicle listings that might be outdated, from a completely different region, or just too small to accurately reflect the market. The result is almost always a valuation that conveniently favors the insurer, leaving you with a lowball offer that simply doesn’t cover your car’s true pre-accident worth.

An independent car appraiser, on the other hand, performs a completely different kind of evaluation. It's a meticulous, hands-on investigation, not an automated guess. That's the real difference here—a thoroughly researched conclusion versus a quick calculation.

The Problem With Automated Systems

Automated valuation tools are everywhere in the auto industry. Across North America, over 56,000 dealerships process nearly 18 million used vehicles each year, with a huge number of them using software to set prices. This works fine for managing inventory, but it creates a massive conflict of interest in an insurance claim.

When these systems undervalue vehicles, it’s the accident victim who pays the price. This is exactly why an independent appraiser has become so essential for fighting back against these built-in biases. You can discover more insights about the automotive appraisal landscape and its heavy reliance on technology.

The insurer's valuation is an algorithm's opinion based on limited data. An independent appraisal is an expert's conclusion based on real-world evidence. The first serves the company; the second serves you.

An independent professional doesn't rely on a generic database. They dive deep into your vehicle's specifics and your local market, building a valuation that is both accurate and tough for an insurer to dismiss.

The table below breaks down these fundamental differences.

Insurer Valuation vs Independent Appraisal A Head-to-Head Comparison

| Factor | Insurance Company Valuation | Independent Appraiser Valuation |

|---|---|---|

| Primary Goal | Minimize claim payout for the insurer. | Determine the true, fair market value for the client. |

| Methodology | Automated software (e.g., CCC ONE, Mitchell). | Hands-on physical inspection and manual market research. |

| Data Sources | Proprietary databases of vehicle listings, which may be outdated or geographically irrelevant. | Real-time, local market listings of comparable vehicles ("comps"). |

| Key Focus | Basic vehicle details: year, make, model, mileage. | Comprehensive details: condition, maintenance, options, packages, and recent upgrades. |

| Objectivity | Inherently biased toward the insurer's financial interests. | Unbiased and neutral, advocating for factual accuracy. |

| Output | A one-page report with a computer-generated number. | A detailed, evidence-based report (often 20+ pages) justifying the final value. |

As you can see, one process is designed for speed and cost savings for the company, while the other is built on thoroughness and accuracy for you.

A Deeper Dive Into True Market Value

So, what does this hands-on process actually look like? An appraiser goes miles beyond the basic VIN and mileage that the insurance software relies on. They conduct a comprehensive, multi-point investigation.

This includes:

- Physical Inspection: The appraiser personally examines your vehicle's pre-accident condition, documenting its maintenance history, cleanliness, and unique features. They look for everything that made your car better than the "average" example on the road.

- Local Market Research: Instead of using a national database, they hunt for genuinely comparable vehicles for sale in your specific geographic area. This crucial step ensures the valuation reflects what local buyers are actually paying for cars just like yours.

- Detailed Adjustments: They apply specific value adjustments for your car’s trim level, optional packages, recent upgrades (like new tires or a stereo), and its overall pristine condition. Insurer software often ignores or downplays these critical details.

This methodical approach results in an evidence-based report that tells the complete story of your vehicle’s value. It transforms the negotiation from a frustrating argument into a factual discussion, giving you the leverage to demand a fair settlement backed by undeniable proof.

When to Hire an Appraiser: The Two Times It’s Absolutely Critical

Knowing when to bring in a professional is the single most important step in protecting your wallet after a car accident. While every crash is different, my experience shows there are two specific moments when hiring an independent car appraiser is non-negotiable. It's the only way to ensure you get a fair shake.

These two situations are Diminished Value and Total Loss.

Both scenarios are different fights, but they start from the same place: the insurance company’s first offer is almost always designed to save them money, not to make you whole again. Let's dig into exactly when you need an expert in your corner.

Scenario One: The Fight for Diminished Value

Even after your car is perfectly repaired by the best shop in town, it’s lost value. This is called inherent diminished value, and it's a real, permanent financial loss. Why? Because a car with a collision in its history is simply worth less to the next buyer than the exact same car with a clean record.

Think about it. You're at a dealership looking at two identical used trucks. One is squeaky clean, and the other has a history of significant accident repairs. Even if that repaired truck looks brand new, which one are you going to buy? A smart shopper will always pick the one with no history or demand a massive discount to take on the risk. That discount is your diminished value, and the at-fault driver's insurance owes you that money.

We’re not talking about a few hundred dollars here. Depending on your car’s age, model, and how bad the damage was, this loss can easily run into the thousands.

Insurers almost never volunteer to pay for diminished value. Their first offer will be $0 or a ridiculously low number, banking on the hope that you don't know your rights. An independent appraisal is the only way to prove precisely how much value your vehicle has lost.

An independent appraiser does the hard work of calculating this loss. We analyze real-world market data, the quality of the repairs, and the simple fact that the public is wary of cars with an accident history. The result is a detailed report that puts a real number on your financial loss, giving you the solid proof you need to demand what you're owed. You can learn more about this process in our guide on how to navigate a diminished value claim after a car accident.

Scenario Two: The Battle Against a Total Loss Lowball

The second critical moment happens when the insurance company declares your vehicle a total loss. This just means they’ve decided it would cost more to fix your car than it’s worth. Instead of paying for repairs, they’ll cut you a check for what they claim is the car’s Actual Cash Value (ACV).

Here's the catch: their ACV offer is often shockingly low. It’s spit out by a computer program that uses questionable data, frequently lowballing your vehicle's worth to protect their bottom line.

You should immediately think about hiring an appraiser if you see these red flags:

- The offer just feels wrong. You know what cars like yours are selling for in your area. If their number seems way off, it probably is.

- Their "comparable" vehicles aren't comparable at all. Insurers love to use examples from hundreds of miles away, with more mileage, in worse condition, or with fewer options than your car had.

- The valuation report ignores what made your car special. Did you have a premium sound system, brand-new tires, or a rare trim package? The insurer’s software often misses these important, value-adding details.

In a total loss situation, an independent appraisal report is your single most powerful tool. It completely replaces their flawed, computer-generated number with a real, heavily researched valuation based on your car's true condition in your local market. While your appraiser focuses on getting the vehicle's value right, an experienced Austin Car Accident Lawyer can manage the legal side, creating a powerful team to fight for your claim.

An appraiser's report gives you the undeniable proof you need to reject their lowball offer and negotiate for the settlement you actually deserve.

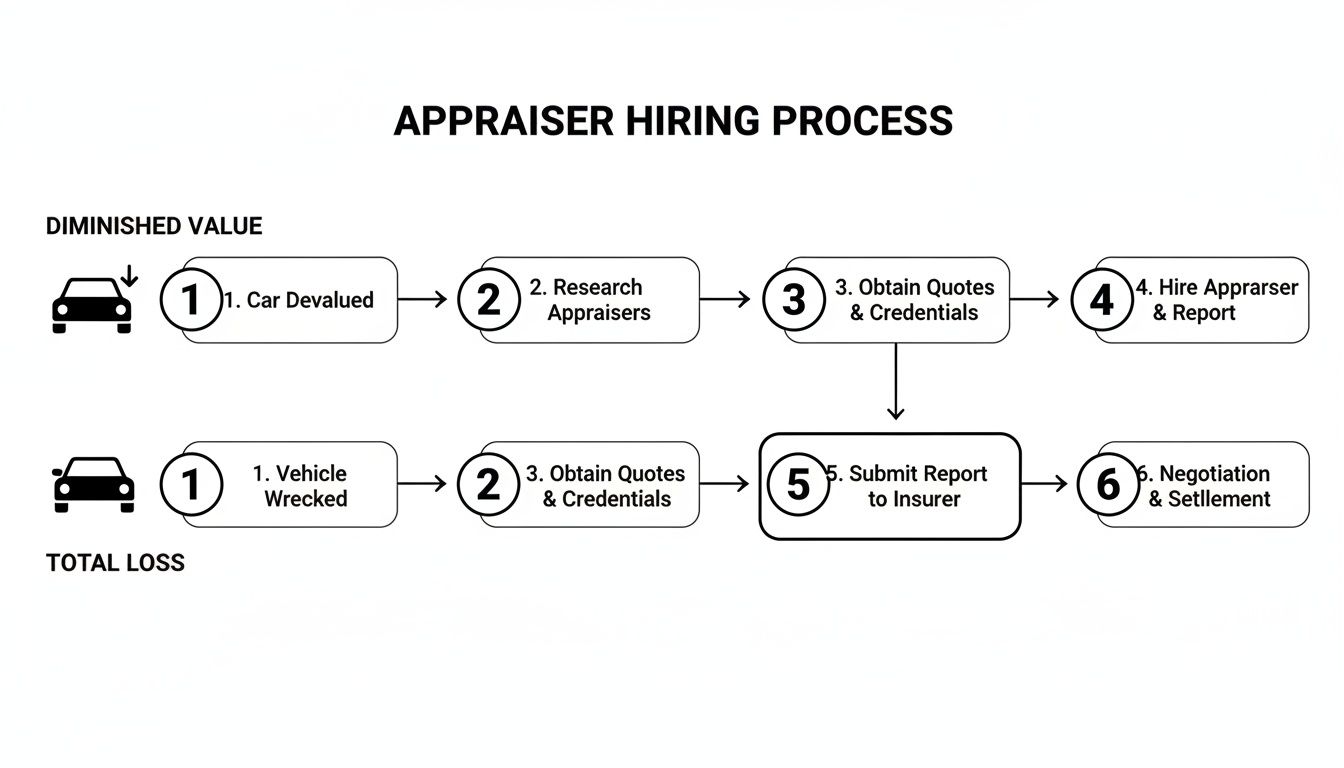

How the Independent Appraisal Process Works, Step by Step

Hiring an independent car appraiser might feel like a big move, but the process itself is surprisingly straightforward. Think of it less as a mystery and more as a methodical investigation into your vehicle's true worth. Let's walk through each stage so you can see exactly how an expert builds an undeniable case for your claim.

It all starts with a simple conversation about your accident and the insurance company’s offer. From there, we move into a clear, step-by-step process of gathering documents, conducting a physical inspection, and digging into deep market research. Everything culminates in one powerful, fact-based report.

This flowchart maps out the typical journey for both diminished value and total loss claims when you work with a professional appraiser.

As you can see, whether your car was repaired or totaled, the core process is the same: gather the evidence, establish a true value, and negotiate from a position of strength.

The Initial Steps: Documentation and Consultation

First things first, we need to gather the right paperwork. Think of yourself as building the initial case file—collecting the evidence your appraiser needs to lay a strong foundation. This isn't just busywork; every single document helps paint a detailed picture of your vehicle's condition and value right before the accident.

Your appraiser will typically ask for a few key items:

- The insurance company's valuation report (if you have it)

- The official police or collision report

- The body shop’s final repair estimate or invoice

- Any photos you have of the vehicle (before and after the accident)

- Recent maintenance records or receipts for any upgrades

With the documents in hand, the consultation solidifies our game plan. We’ll review the details together, and the appraiser will explain exactly how they'll approach the valuation. You'll understand the path forward before any work even begins. This groundwork is what separates a professional appraisal from a quick guess.

The Core of the Appraisal: Vehicle Inspection and Market Research

Once the paperwork is sorted, the real investigation begins. The appraiser will conduct a thorough, hands-on inspection of your vehicle. This is far from a quick walk-around; it’s a detailed examination to document the car's pre-accident condition, looking for everything the insurer’s software ignores.

This includes the quality of the interior, the condition of the paint, tire wear, and any special features or aftermarket parts that add real value. For a diminished value claim, this is also when we meticulously inspect the quality of the repairs, noting any imperfections that will absolutely impact its future resale value.

Next up is the most crucial part of the entire process: market research. An independent appraiser doesn't just pull numbers from a generic, nationwide database. They become a detective in your local market, hunting down truly comparable vehicles, or "comps."

A "comparable vehicle" isn't just the same make and model. A true comp must match your car's year, trim, mileage, options, and overall condition. Crucially, it must also be for sale in your immediate geographic area.

This local focus is non-negotiable. A car’s value in Portland, Oregon, can be thousands of dollars different from its value in Seattle, Washington. Your appraiser will find and document multiple real-world examples of what cars just like yours were selling for right before the accident, creating a rock-solid baseline for your vehicle's actual cash value. It's this localized, evidence-based approach that makes the final report so difficult for an insurance company to argue with.

Finalizing the Report and Negotiation

The last step is to bring all this research together into a comprehensive, professional report. This document is much more than just a number—it’s a detailed narrative that tells the complete story of your vehicle’s value. It will include photos, the appraiser’s inspection notes, links to all the comparable vehicles found during the market research, and a clear, logical explanation of how the final value was calculated.

This report is your ultimate negotiation tool. Suddenly, it’s no longer your opinion against the insurer’s. It's an expert’s factual conclusion against a computer algorithm. Armed with this evidence, you can reject their lowball offer with confidence and demand the fair settlement that your car's true, documented worth commands.

How to Invoke the Appraisal Clause in Oregon and Washington

Buried deep within your auto insurance policy is a powerful tool you probably don’t know exists: the Appraisal Clause. This isn't just a bit of fine print; it's a contractual right that gives you the power to challenge a lowball settlement offer from your insurer.

When you and your insurance company are at a complete standstill over the value of your vehicle, invoking this clause forces the issue. It triggers a structured, fair, and legally binding process that takes the final decision out of the insurance company’s hands and places it with unbiased experts.

For drivers here in Oregon and Washington, knowing how to use this provision is one of the most effective ways to secure the fair settlement you’re owed.

What Is the Appraisal Clause?

Think of the Appraisal Clause as a dispute-resolution mechanism built right into your policy. When you invoke it, you're formally demanding to move the valuation process to neutral ground.

The process is designed to find a fair, evidence-based value. Here’s how it works:

- You hire your own appraiser. This is a certified, independent professional you choose to represent your financial interests.

- The insurer hires their appraiser. They will also select an expert to argue for their valuation.

- The two appraisers negotiate. The experts present their data, evidence, and reports to try and agree on your vehicle’s true pre-accident value.

But what if they can't agree? That's where the next step comes in.

Your insurance policy is a contract, and the Appraisal Clause is a key provision that protects you. Invoking it is not an act of aggression; it's you exercising your contractual right to an unbiased and evidence-based valuation.

This entire mechanism ensures the final settlement isn't just a number spit out by the insurance company's software. Instead, it's determined by real professionals looking at actual, real-world market data.

The Umpire: A Neutral Tie-Breaker

So, what happens if the two appraisers are still miles apart on the value? The Appraisal Clause has a built-in solution for this exact scenario. The two appraisers agree on a neutral third-party expert, known as an umpire.

This umpire acts as the tie-breaker. They review the evidence, reports, and valuations from both sides and can even conduct their own research before making a final determination. A binding settlement is reached as soon as any two of the three parties (your appraiser, the insurer's appraiser, or the umpire) agree on a final value.

This three-person panel is what makes the process so fair. It's almost impossible for one side’s biased valuation to dominate the outcome. Once an agreement is reached, that number is binding on both you and the insurance company, bringing the dispute to a close. We cover this in much greater detail in our complete guide to the insurance appraisal clause.

How to Formally Invoke the Clause

To kick things off, you must formally notify your insurance carrier in writing that you intend to invoke the Appraisal Clause. This can't be a casual phone call—it needs to be a clear, documented request that creates a paper trail.

Your letter should state plainly that you are disputing their valuation and exercising your right to an appraisal as outlined in your policy. You should also name the independent car appraiser you’ve hired to represent you. This official notice legally compels them to participate, finally leveling the playing field and forcing them to defend their numbers against a true expert.

How to Choose the Right Certified Appraiser

Knowing you need an independent appraiser is the first step. Actually choosing the right one? That’s what makes the difference between getting a fair settlement and leaving money on the table.

Not all appraisers are built the same, and your choice has a direct impact on the outcome of your claim. You have to look past a basic business listing and dig into their credentials, their real-world experience, and their knowledge of our local market here in the Pacific Northwest.

Think of it this way: you wouldn't hire a general handyman to rewire your entire house. You’d call a licensed electrician. It’s the same idea here. You need a specialist with a proven track record in the very specific world of insurance claim disputes.

Vetting Your Appraiser Checklist

To protect your claim, you absolutely have to vet any professional you're considering. A truly credible appraiser will be transparent and have no problem showing you proof of their qualifications. A great place to start is by asking about their industry certifications.

Look for credentials from respected organizations like:

- I-CAR (Inter-Industry Conference on Auto Collision Repair): This certification signals a deep understanding of modern vehicle construction and repair standards—absolutely critical when assessing damage.

- ASE (Automotive Service Excellence): This is the gold standard for mechanic competence, proving they have a rock-solid technical foundation.

These aren't just fancy acronyms. They prove an appraiser has the foundational knowledge to accurately assess vehicle damage and repair quality, which is the bedrock of both diminished value and total loss claims.

Next, you need to confirm their direct experience. Ask them straight up how many diminished value and total loss cases they handle specifically in Oregon and Washington. An appraiser who mainly works on classic car valuations for collectors probably isn't the right person to go to bat against a major insurance company.

The single most important question you can ask an appraiser is: "Can I see a sample report?" A detailed, well-researched report is their primary tool. If the sample they show you looks thin, generic, or unprofessional, it’s not going to hold up under the insurance adjuster's scrutiny.

The Importance of Local Expertise

Hiring an appraiser with deep, firsthand knowledge of the Pacific Northwest market isn't just a "nice to have"—it's a must. The value of a used car can swing pretty wildly between Portland and Seattle, and a generic appraiser from out of state just won't get those critical nuances.

Local experts live and breathe regional market trends. They know the dealership practices and, most importantly, they know what genuinely comparable vehicles are selling for right here in your area. A good starting point is to specifically look for an independent auto appraiser near you to guarantee they have this vital local insight.

This local focus is more critical than ever. The global used car market is massive, valued at USD 1.7 trillion and on track to hit an incredible USD 3.1 trillion by 2033. In this fast-moving environment, independent appraisers who truly understand their local market are indispensable for ensuring fair valuations. You can learn more about the trends shaping the used car market and see why expert, localized valuations are so essential.

Finally, think of the appraiser's fee as an investment. A quality, thorough appraisal isn't going to be cheap, but it's a small price to pay when the result is a settlement that's thousands of dollars higher. The work of a skilled appraiser almost always pays for itself by delivering the hard evidence needed to get you the full and fair value you're legally owed.

Still Have Questions? Here Are Some Common Ones

It’s completely normal to have a few questions swirling around before you decide to hire an independent appraiser. Making a smart choice is what matters most, so let's clear up some of the most common things people ask.

Think of this as a quick-reference guide to help you move forward with total confidence. Knowing what to expect makes the whole process smoother and shows why having a real expert in your corner is so valuable.

Is Hiring an Appraiser Really Worth the Money?

Absolutely. The best way to look at the appraisal fee isn’t as a cost, but as an investment in getting a much, much better settlement. In most cases, the extra money we get you far outweighs the fee—often by thousands of dollars.

Let's be blunt: insurance companies’ first offers are designed to be low. An appraiser gives you the hard evidence needed to push back and get them to pay what your claim is actually worth.

What if the Insurance Company Just Says "No" to the Appraisal?

This is exactly why the Appraisal Clause in your insurance policy is such a powerful tool. In states like Oregon and Washington, this clause is a contractual right. It means your insurer can't just toss a legitimate expert valuation in the trash. It gives you real leverage.

If they try to ignore our report or refuse to negotiate, we help you formally invoke that right. This step legally forces them into the appraisal process, often involving a neutral third-party "umpire." It’s your ultimate safeguard against being steamrolled.

An independent appraisal isn't just a second opinion; it's a documented valuation built on hard facts. When you back it up with the Appraisal Clause, it becomes a legal tool that forces a fair outcome, taking the final decision out of the insurance adjuster's hands.

How Long Does This Whole Thing Take?

Every situation is a little different, but the appraisal itself—from inspecting your vehicle to delivering the final, detailed report—usually takes about 5 to 10 business days. We need that time to do a thorough inspection, dig into local market data, and assemble all the evidence properly.

Once we send the report to the insurance company, the negotiation timeline can vary. That said, handing them a professional, fact-based report almost always gets things moving faster. It’s hard to argue with clear, well-documented proof.

Can You Help Me with a Classic Car or a Modified Truck?

Yes, and frankly, these are the situations where our expertise shines brightest. The standard software insurers use—think Kelley Blue Book or NADAguides—is terrible at valuing classic, custom, or rare vehicles. These automated systems have no way of understanding things like restoration quality, unique modifications, or what a passionate buyer would actually pay.

Our independent car appraisers specialize in digging up the real-world value of these one-of-a-kind vehicles. We make sure your settlement reflects what your car is truly worth on the open market, not some generic number spit out by a computer.

Don't let an insurance adjuster tell you what your car is worth. If you're navigating a diminished value or total loss claim in Oregon or Washington, the team at Total Loss Northwest is here to make sure you get the fair settlement you’re entitled to.

Get your free consultation today and put a certified professional on your side of the table.