A few hours after a crash, many find themselves doing the same thing. They're staring at a claim number, a repair estimate, a pile of discharge papers, and a browser tab that says injury settlement calculator.

That search makes sense. You want one answer to one urgent question: What is my case worth?

The problem is that online calculators feel more certain than they are. They can help you get your bearings on the injury side of a claim, especially when you're trying to understand medical bills, lost wages, and pain and suffering. But they also leave out some of the most expensive parts of a real-world accident claim, especially when your vehicle was totaled or lost market value after repairs.

I'm going to walk through this the same way I would explain it to a vehicle owner or injured driver after an accident. Plain language. No legal theater. No mystery math. Just what these calculators do, where they help, and where they subtly fail.

Demystifying the Injury Settlement Calculator

When you use an injury settlement calculator, you're usually being asked to enter a few basic facts. Medical bills. Time missed from work. Sometimes property damage. Then the tool gives you a rough estimate.

That estimate can be useful. It gives you a starting point when everything still feels scattered. If you're trying to make sense of the claim process in a no-fault state or compare how different expenses fit into a bodily injury claim, a state-specific resource like this Oregon auto injury compensation guide can help you understand the terms before you start plugging in numbers.

What the calculator is really doing

Most calculators are not predicting your settlement. They're modeling it.

They take the costs that are easiest to document, then apply a general formula to estimate the less visible parts of harm, such as pain, interruption to daily life, and emotional strain. That's why two different calculators can produce two very different outputs from the same accident.

Why people get confused so quickly

The confusion usually comes from three assumptions:

- A calculator result feels official: It isn't. It's a rough estimate based on limited inputs.

- A bigger medical bill always means a bigger payout: Sometimes it does, but only if the treatment, diagnosis, fault picture, and insurance coverage all support it.

- The injury claim and the vehicle claim are one thing: They're related, but they're often valued through different processes.

Online calculators are best used as a sketch, not a verdict.

The hidden risk

If you only use a standard injury settlement calculator, you may end up evaluating only half your loss. That matters if your car was declared a total loss, if repairs affected resale value, or if the insurer's valuation software came in low.

That's the part many people don't find out until after they've already started negotiating.

The Core Components of Your Settlement Value

After a crash, people often ask one question: “What is my case worth?” A better starting question is, “What losses am I trying to measure?”

Your settlement value usually has two parts. One covers losses you can document with records and invoices. The other covers the human impact that does not show up neatly on a bill.

That split is easy to miss when you are sore, busy, and dealing with calls from insurers.

The first pile is economic damages

Economic damages are the measurable costs of the accident. These are the numbers an adjuster can point to in a file, such as treatment charges, wage records, and vehicle-related expenses. They form the starting point for many settlement estimates, even though they are only part of the picture.

Economic damages often include:

- Medical expenses: Ambulance charges, emergency care, follow-up visits, physical therapy, medication, imaging, and projected future treatment tied to the injury.

- Lost income: Missed paychecks, reduced hours, used sick leave, and loss of earning ability if your injuries affect the type of work you can do.

- Property-related losses: Vehicle repair bills, rental car costs, towing, storage fees, and other out-of-pocket costs caused by the crash.

Insurance coverage can affect how these costs get paid in the short term. If you are trying to sort out first-party benefits while building your claim, Professional Insurance Advisors PIP gives a useful explanation of how Personal Injury Protection can fit into the process.

Good records help here. A practical guide on steps after a car accident can help you keep bills, photos, repair documents, and claim communications organized from the start.

One point many online calculators blur: vehicle losses are not just a footnote to the injury claim. If your car is a total loss, or if it was repaired but worth less afterward, that can change the size of your overall recovery in a way a basic injury-only calculator often misses.

The second pile is non-economic damages

Non-economic damages cover the part of the loss that people live with, not the part they can easily total on a spreadsheet.

Pain is part of it. So are sleep problems, anxiety, loss of normal movement, missed family routines, embarrassment from visible injuries, and the strain of trying to work or drive while your body is still healing.

These losses are real, but they are harder to prove. That is why details matter. A medical record that notes ongoing pain, activity limits, or disrupted sleep often carries more weight than a vague statement that you were “still hurting.”

Simple way to view it: Economic damages measure what the accident cost you in money. Non-economic damages measure what it cost you in day-to-day life.

How This Distinction Affects Your Claim

Insurance companies usually examine the documented expenses first because those numbers are easier to limit, question, or discount. If you focus only on bills, you may end up valuing only the visible half of your case.

A sound estimate looks at both piles together. It also keeps a separate eye on the vehicle side of the claim, because car damage, total loss disputes, and diminished value are often handled through a different valuation process than bodily injury. That gap is one of the biggest reasons online settlement calculators can give people a false sense of precision.

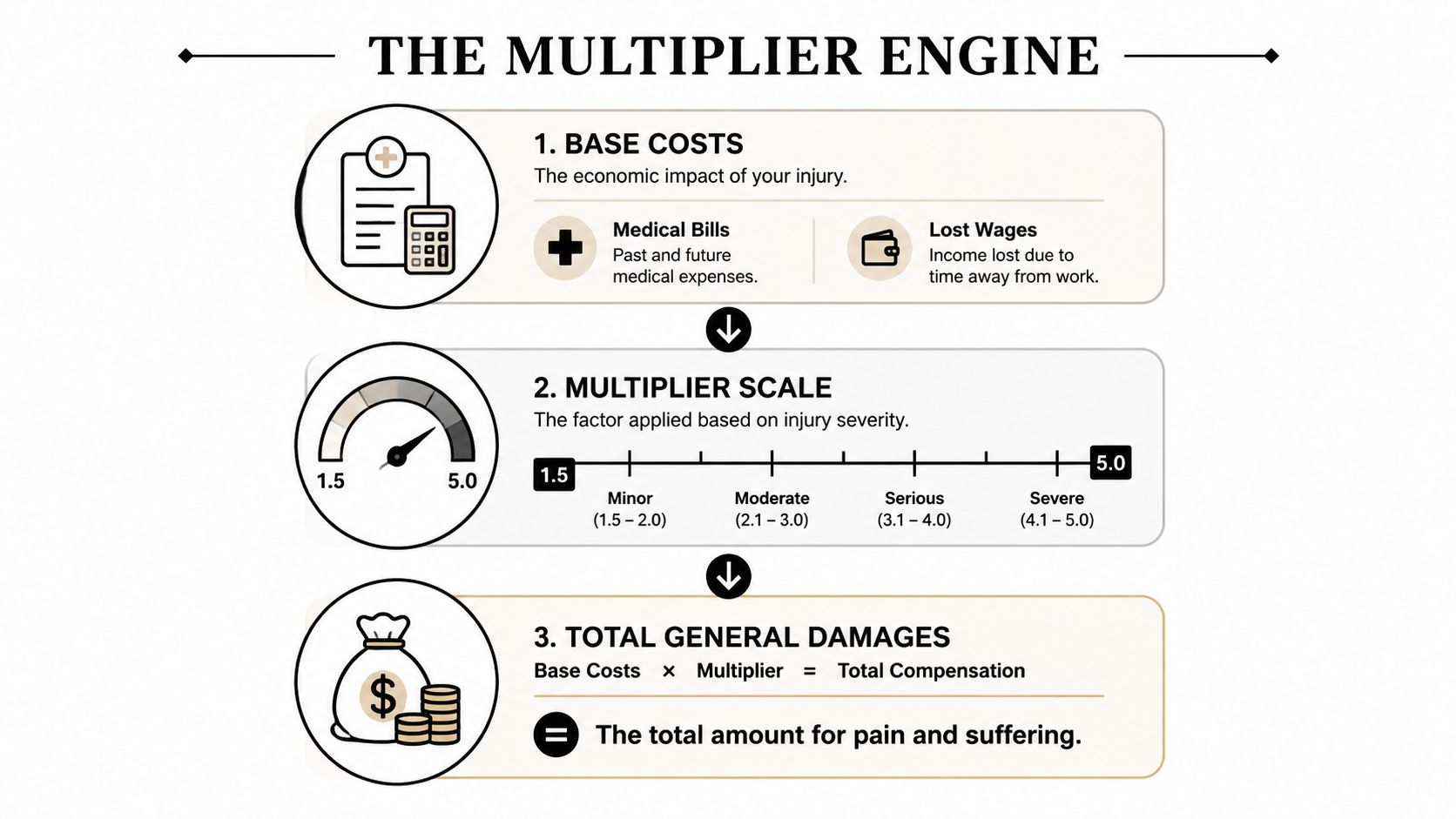

Understanding the Pain and Suffering Multiplier

The multiplier is the engine inside most injury settlement calculator tools. Once the calculator totals your economic losses, it applies a number to estimate pain and suffering.

That number is usually tied to severity. The common range is 1.5 to 5, and some severe cases may go higher. One example from the Gage Mathers settlement calculator explanation shows $85,000 in economic damages with a 3x multiplier, producing $255,000 in non-economic damages and a total claim value of about $340,000.

What pushes the multiplier up

A higher multiplier usually reflects a harder recovery and a deeper life impact.

Some of the facts that tend to support a higher number include:

- More serious injuries: A fracture, spinal injury, burn, or brain injury usually carries more weight than a strain that resolves quickly.

- Longer treatment: Ongoing physical therapy, specialist visits, injections, or surgery show a more intrusive recovery.

- Permanent change: Lasting symptoms, visible scarring, reduced mobility, or work limitations affect value more than a full and fast recovery.

- Daily disruption: If the injury changed sleep, parenting, driving, work, or basic movement, that often matters.

What keeps it lower

Not every injury justifies an aggressive multiplier. A claim tends to stay lower when the person recovers quickly, treatment is limited, records are thin, or the symptoms don't seem to affect day-to-day functioning in a documented way.

Many self-calculated claims often go wrong. People either choose a number based on emotion alone or choose one so conservatively that they undersell the claim before the negotiation starts.

Practical rule: Don't pick a multiplier first. Build the story of the injury first, then ask what number that story reasonably supports.

Why software often misses the human side

This part gets more technical, but it matters. The same Gage Mathers source notes that software such as Colossus uses 600 injury codes to assign values, and those systems can undervalue claims by 20 to 40 percent when they ignore many specific medical codes and details that don't fit neatly into the coding structure.

That means the number on the insurer's screen may not reflect the actual burden of your recovery. The computer can count treatment dates. It can't fully grasp what six months of disrupted sleep, missed work, and chronic pain does to a person's life unless someone documents it well and argues it clearly.

Major Factors That Can Reduce Your Settlement

A calculator can tell you what a claim might be worth in theory. Real claims get reduced in practice.

Two forces usually do the cutting. One is fault allocation. The other is the ceiling created by insurance coverage and claims software.

Comparative fault changes the math

Think of liability like a pie. If the insurer says you were responsible for a slice of the accident, they'll try to reduce your payout by that same slice.

A common example from the verified data is a $50,000 economic loss with a 3x multiplier, producing a $200,000 total claim. If the injured person is found 20 percent at fault, the claim is reduced by $40,000.

State rules matter here. Some states let you recover even if you share fault, while others cut off recovery after a certain point. That's one reason a generic calculator can mislead you if it doesn't account for the law where the crash happened.

Software can reduce value before a person ever reviews it

Insurers don't always start with a blank page. Many use structured claims software. According to Miller & Zois on Colossus, over 50 percent of U.S. insurers use Colossus, which relies on about 600 injury codes and is known to reduce payouts by 25 to 50 percent when important factors such as PTSD are not coded precisely. The same source says it can also bias vehicle valuation by favoring its own Actual Cash Value data over real market comparisons.

The number you see may not be the number they use

Here are the common places claims lose value:

- Missing records: Gaps in treatment make symptoms easier to dismiss.

- Coding problems: If the diagnosis or long-term impact isn't captured cleanly, software may assign a lower value.

- Disputed fault: Even a modest fault allegation can materially shrink the payout.

- Property valuation shortcuts: Vehicle losses often get processed through a separate valuation track that may not reflect actual market conditions.

A settlement estimate is never just math. It's math filtered through documentation, software, fault arguments, and coverage limits.

Two Worked Examples From Start to Finish

A calculator feels reassuring until you try to match it to a real claim.

You enter a few numbers, get a settlement estimate, and for a moment it seems concrete. Then questions start piling up. Why did one injury get a modest figure while another jumps much higher? Why does fault change the result so sharply? And why is the car missing from the math when the crash damaged far more than your body?

These two examples walk through the process the way an appraiser would. The goal is not to promise an outcome. It is to show how the common formula works, where it helps, and where it leaves out losses that can matter a great deal.

Injury Settlement Calculation Examples

| Calculation Step | Case A: Simple Whiplash | Case B: Complex Fracture |

|---|---|---|

| Medical bills | $3,000 | $25,000 |

| Lost wages | $0 | $25,000 |

| Property damage included in economic losses | $0 | $0 |

| Total economic damages | $3,000 | $50,000 |

| Multiplier selected | 1.5x | 3x |

| Non-economic damages | $4,500 | $150,000 |

| Preliminary total | $7,500 | $200,000 |

| Comparative fault adjustment | None | 20% reduction |

| Final estimated value | $7,500 | $160,000 |

How to read the table

Case A is the kind of claim many online calculators are built around. The injuries are limited, treatment is short, and there are no wage losses. Using the standard formula, $3,000 in medical bills multiplied by 1.5 produces $4,500 in pain and suffering, which brings the total estimate to $7,500.

Case B shows why larger claims can rise fast. Medical bills and lost wages create a much bigger base. Once that $50,000 in economic loss is paired with a 3x multiplier, the estimate reaches $200,000 before fault is applied. A 20 percent fault reduction then cuts the result to $160,000.

That reduction is not a technical footnote. It is money out of the claim.

A helpful way to read these examples is to picture the calculator as a measuring tape. It can give you a rough length, but it does not tell you whether the wall is straight, whether part of the room is missing, or whether someone else is disputing where the measurement starts. The output is only as good as the facts fed into it.

What these examples actually teach

First, the multiplier gets attention because it is easy to see, but the documented losses underneath it do just as much work. A small claim with clean records can still produce a relatively small number. A larger claim grows because every medical bill, work loss record, and treatment note adds support.

Second, fault can change the outcome more than injured people expect. The injury in Case B did not get smaller. The payment estimate did.

Third, both examples reveal the biggest weakness in many online tools. They treat the injury claim as if it were the whole file. It rarely is. If your vehicle was totaled or repaired poorly, the missing piece may be thousands of dollars. Before you accept any broad settlement estimate, it helps to understand how to calculate fair market value after a total loss and to gather supporting records such as VekTracer VIN history reports, which can help document accident history and condition issues that affect a vehicle claim.

A calculator can estimate the injury portion. It cannot fully price a claim file that includes fault disputes, missing records, and vehicle losses.

The Calculator's Biggest Blind Spot Your Vehicle

Most online tools generally break down.

They treat the vehicle as a side note, if they include it at all. But for many drivers, especially after a serious crash, the vehicle side of the claim isn't minor. It can be a major part of the financial loss.

Bodily injury calculators often ignore the most expensive property issues

The verified data is blunt on this point. Ajlouny Injury Law's settlement calculator discussion notes that existing calculators overwhelmingly focus on bodily injury and neglect vehicle-related claims such as diminished value and total loss settlements, even though vehicle damage can represent 40 to 60 percent of total payouts.

That's a serious blind spot.

If your car was repaired, you may still have a market-value problem. A damaged-and-repaired vehicle can be worth less than it was before the wreck, even if it looks fine and drives fine. If your car was totaled, the issue shifts to whether the insurer's Actual Cash Value figure reflects the local market's value.

Why this matters in the real world

Insurers often rely on valuation systems that prioritize internal data sets and standardized comparisons. That can work reasonably well for some everyday vehicles. It can miss badly on:

- High-value vehicles: Trim, package, condition, and regional demand can change the actual figure.

- Collector or custom vehicles: Standard software often struggles with rare comps.

- Repaired vehicles with stigma: A crash history can lower resale value even after proper repairs.

- Regional markets: Local pricing can differ sharply from national averages.

If you're trying to document the accident history that buyers, dealers, and appraisers will eventually see, VekTracer VIN history reports can help you understand how recorded damage affects resale conversations later.

For drivers trying to sanity-check the insurer's total loss number, a guide on how to calculate fair market value can help separate a broad software estimate from an evidence-based vehicle value.

The detail most calculators never mention

The same Ajlouny source notes that, in Washington and Oregon, invoking the Appraisal Clause with an independent appraiser can increase vehicle settlements by 20 to 50 percent by bypassing insurer software that undervalues cars.

That doesn't mean every vehicle claim should go into appraisal. It does mean that an injury settlement calculator is often incomplete by design. It may estimate your body claim and leave your vehicle claim underdeveloped, underdocumented, and undervalued.

A bodily injury estimate can be reasonable and still leave thousands of dollars of vehicle loss unresolved.

When to Stop Calculating and Start Consulting

An injury settlement calculator has one good job. It helps you form a rough starting point.

It stops being enough when the claim becomes layered. Serious treatment. unclear fault. low offers. total loss disputes. diminished value. that's where rough math starts giving false confidence.

Red flags that mean the calculator is no longer enough

You should stop relying on a calculator alone when any of these show up:

- The injury may be permanent: Long-term pain, surgery, disability, or work restrictions usually need a more careful valuation.

- Fault is being disputed: Comparative negligence rules can change the number dramatically depending on the state.

- The insurer made a quick offer: Early offers are often designed to close the file before the full picture is clear.

- Your vehicle was totaled or lost resale value: Standard bodily injury tools usually don't evaluate these losses well.

- You're using an AI calculator for a complex claim: The verified data from Mighty's AI settlement calculator discussion says AI-driven calculators emerging since mid-2025 often overestimate soft-tissue injuries but underestimate total loss vehicle claims by 25 percent. The same source notes they can miss Diminished Value add-ons averaging $5,000 to $15,000 and may ignore state-specific rules such as Washington's pure comparative negligence.

What good professional help actually does

A lawyer and a vehicle appraiser solve different problems.

An attorney can assess liability, injury documentation, treatment impact, and negotiation strategy. A certified appraiser can challenge a low vehicle valuation, support diminished value, or force a closer review through the appraisal process where that option exists.

If the adjuster's number feels low and you need a practical framework before responding, this guide on how to negotiate with an insurance adjuster is a solid next read.

This short video gives a useful overview before you make that call.

The calm rule to follow

Use the calculator to get oriented. Don't use it to make final decisions about settlement.

The right moment to consult someone is usually earlier than people think. Not because every claim turns into a fight, but because early mistakes are hard to undo. Once a statement is recorded, a release is signed, or a vehicle valuation is accepted, your bargaining power often shrinks.

The calculator gives you a ballpark. A professional tells you whether the ballpark is even the right field.

If your accident claim involves a total loss, diminished value, or a vehicle that insurer software may be undervaluing, Total Loss Northwest helps Oregon and Washington drivers get an evidence-based valuation rooted in real market data. They specialize in independent auto appraisals and Appraisal Clause disputes, which is often the missing piece when an injury settlement calculator leaves the vehicle side of the claim unfinished.