Out-of-warranty EV battery replacement costs now average between $5,000 and $20,000, and understanding that range is the first step to a fair insurance settlement. If you're dealing with an accident claim right now, the battery often isn't just a repair item. It's the number that can decide whether your EV gets fixed, totaled, or undervalued.

That catches many drivers off guard. They expect the insurer to focus on body damage, airbags, or frame issues. In EV claims, the battery can dominate the economics of the entire file.

As an appraiser, I see the same mistake repeatedly. People treat ev battery replacement cost as a future ownership concern, when in an accident claim it's often an immediate valuation issue. If the insurer prices the battery wrong, they can undervalue the car, push it into total loss status, or underpay diminished value.

The Real Cost of EV Battery Replacement in 2026

Your EV comes back from a collision with moderate body damage, a drivable chassis, and one line on the estimate that changes the whole claim: battery replacement. That single item can swing the file from repairable to total loss, or cut into diminished value even if the vehicle is repaired.

Out-of-warranty battery replacement still spans a wide range in 2026. In claim work, the practical takeaway is not the exact national average. It is that battery pricing varies enough by pack size, brand, sourcing method, and repairability that insurers regularly miss the financial impact on the vehicle's value.

What pushes the cost up or down

Three variables usually drive the number:

- Battery size. Larger packs usually cost more to replace because there is more material, more weight, and often more complexity in cooling and packaging.

- Manufacturer parts pricing. Two EVs with similar range can produce very different estimates because OEM pricing policies are not uniform.

- Replacement path. A new OEM pack, a remanufactured pack, or a used assembly can produce very different claim outcomes, both on repair cost and on post-repair market perception.

That last point matters more than many owners realize. In an insurance claim, the insurer may favor the cheapest viable battery path. That can reduce the repair estimate, but it can also raise fair questions about future resale value, remaining battery life, and whether a buyer will discount the car later because the pack is not new or not original.

I look at battery cost as a valuation issue first and a repair issue second.

Why this number matters in a claim

A high battery estimate does not automatically mean the insurer is overpaying. It also does not mean replacement is the right answer. The financial question is whether the full repair plan makes sense against the vehicle's pre-loss market value, expected salvage value, and the stigma that can follow a battery-related accident repair.

That is why owners should verify value early. A weak valuation gives the carrier too much room to argue that the vehicle was worth less before the crash, which makes a battery-heavy repair estimate look less reasonable. If you need a benchmark, review how to calculate fair market value after a total loss.

Battery economics also affect diminished value. Even when the car is repaired correctly, buyers and dealers often react differently to an EV with a documented battery event, pack replacement, or unresolved questions about battery health after impact. That reaction can cost you money later, and it should be part of how the claim is evaluated now.

For smaller electric vehicles, the same pricing logic shows up in a simpler form. Punk Ride's guide for urban commuters is a useful comparison for how battery size and replacement path change ownership cost, even outside the passenger car market.

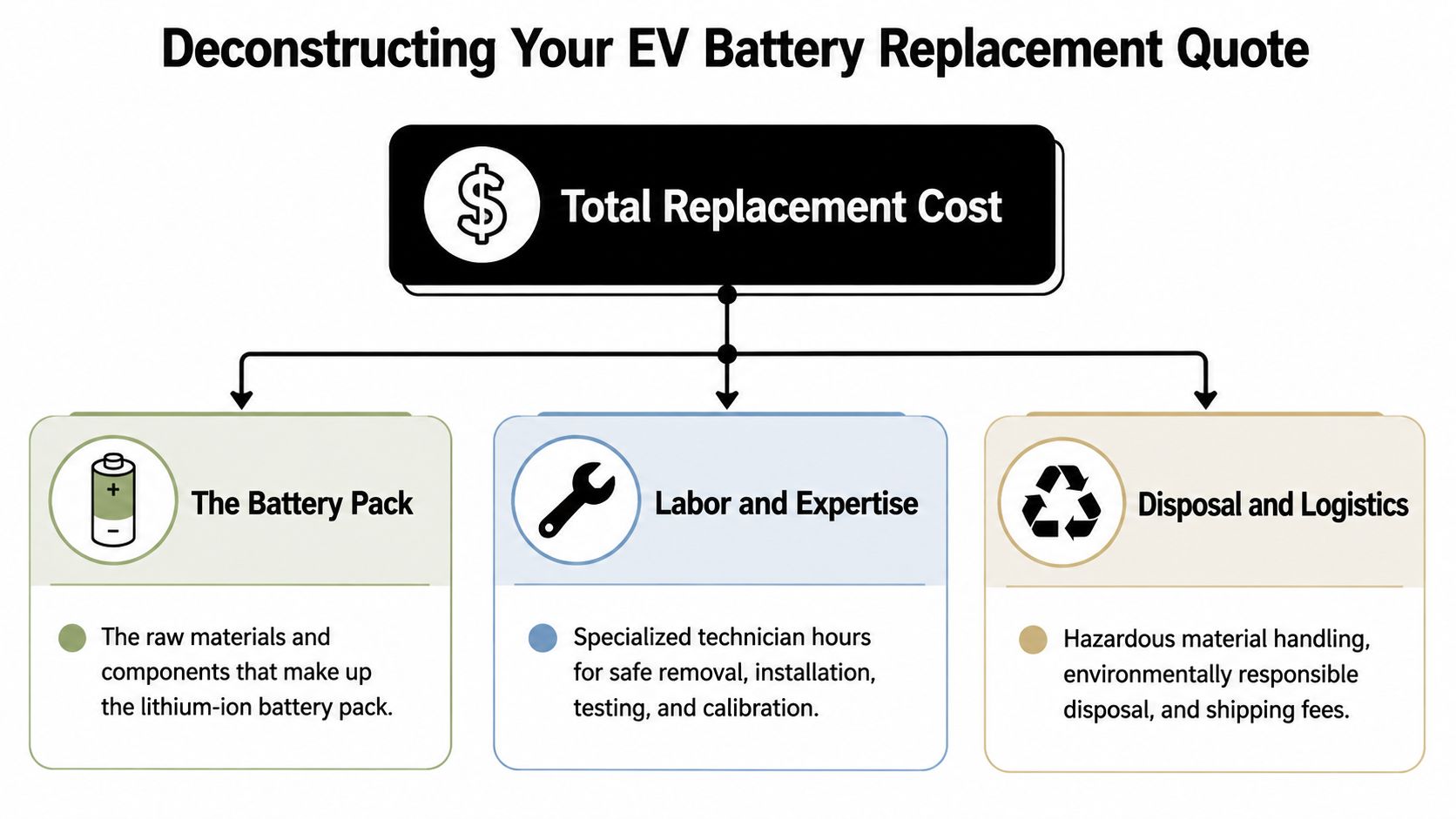

Deconstructing Your EV Battery Replacement Quote

A battery quote often decides the claim before anyone says it out loud. If the estimate is written as a full pack replacement with high labor, transport, programming, and disposal charges, the insurer may start treating the vehicle as a total loss candidate. If the estimate is vague, you lose ground on repair options, settlement value, and any later diminished value argument.

The quote should show more than a battery price

A usable EV battery estimate breaks the job into separate charges so you can see what is being replaced and why. If the shop or carrier gives you one large number, ask for the line-item version before you discuss settlement.

A proper quote may include:

- Battery assembly. This may be a new, remanufactured, or used pack, and the difference matters to both cost and future resale.

- Labor. High-voltage battery work usually carries a premium because it requires trained technicians, specialized equipment, and safety procedures that do not apply to a routine mechanical repair.

- Diagnostics and confirmation testing. The shop should show how it identified the battery issue and how it plans to verify the repair after installation.

- Software programming or coding. Many EVs need battery management system setup, vehicle integration, or manufacturer-specific initialization after battery work.

- Shipping, hazardous material handling, and disposal. These charges can be legitimate, but they should be stated clearly and not buried in labor or parts markup.

That breakdown matters in a claim because each line item can be challenged separately.

Read the estimate like a valuation document

Owners often focus on whether the total looks high. In a claim, the better question is whether the quote supports the repair path the insurer is using to value the case.

For example, a full pack replacement estimate carries very different claim consequences than a quote built around module repair, cell balancing, or post-impact testing. A full replacement number can push repair costs close to the vehicle's actual cash value. It can also create a stronger argument that the vehicle will carry stigma in the market even after proper repairs.

This is why vague language causes problems. Terms like "battery service," "pack issue," or "replace HV battery as needed" are not specific enough for a serious claim review.

What deserves pushback

Some battery-related charges are justified. Some are placeholders. The job is to separate the two before the insurer uses the quote to limit your options.

Ask direct questions:

- Is this quote based on confirmed battery damage, or is it a precautionary replacement recommendation after impact?

- Is the repair plan a full pack replacement, a module-level repair, or additional diagnostic teardown?

- What condition is the replacement unit in: new, remanufactured, or recycled?

- Are programming, shipping, and disposal listed separately, or folded into broader charges that are hard to verify?

- Did the insurer approve the most expensive battery path first, without documenting why a narrower repair was rejected?

If the answer to any of those questions is unclear, the estimate is not ready to drive a settlement decision.

A weak battery quote gives the insurer room to control the story of the claim. A detailed quote gives you room to challenge repair scope, total loss logic, and loss in market value after the repair.

EV Battery Replacement Costs by Make and Model

Model-specific examples help because "EV battery replacement" is too broad to be useful in a live claim. A compact hatchback and a larger crossover don't belong in the same mental bucket.

The data below reflects examples and ranges cited in the verified material. These aren't universal quotes for every market. They're a reality check for what parts and labor can look like on common vehicles.

Estimated EV battery replacement costs by model

| Vehicle Model | Battery Size (kWh) | Estimated Replacement Cost (Parts & Labor) |

|---|---|---|

| BMW i3 | 22 | $5,000 to $16,000 |

| Chevy Bolt | 60 | about $9,000 |

| Nissan Leaf | 40 | up to $12,500 |

| Hyundai Kona Electric | not specified in verified data | about $10,500 |

| Tesla Model 3 | 75 | $15,799 |

| Chevy Volt | 18.4 | $3,000 for a used pack example |

Those examples show the central pricing pattern. Smaller and older packs can land lower. Larger packs, newer architectures, and brand-specific sourcing can move the number quickly.

Full pack versus module repair

This is one of the most important distinctions in any EV estimate. A vehicle doesn't always need a complete battery assembly.

Edmunds, as summarized in the verified data, notes that module swaps can cost $1,000 to $3,000, while full integrated pack replacements cost much more. In practical terms, that means a battery-related estimate should always be read with one question in mind: is the quote solving the actual failure, or is it defaulting to the most expensive path?

A good repairer can identify when a modular approach is realistic. A weak estimate skips that step and jumps straight to replacement.

What works and what doesn't

Here's the trade-off I tell clients to focus on:

- What works. A line-by-line estimate tied to the actual battery architecture in your model.

- What doesn't. A generic insurer adjustment that treats all EV battery events like total pack failures.

- What works. Confirming whether the damage is electrical, physical, thermal, or software-related before accepting a total replacement figure.

- What doesn't. Assuming a scary number must be correct because the vehicle is electric.

If the estimate doesn't tell you whether the shop is replacing a module or the entire pack, you don't have enough information yet.

Understanding Your Warranty and Battery Health

After a crash, I often see owners get the same answer from the dealer. The battery is not covered under warranty. That may be true, but it does not settle the insurance claim, and it does not tell you what the vehicle was worth one minute before the impact.

What the warranty does and doesn't do

Battery warranties usually address capacity loss, defects in materials, and manufacturer-related failures. Collision damage falls into a different file. If the pack, enclosure, cooling lines, or high-voltage components were affected by the accident, the insurer has to evaluate repair cost, pre-loss condition, and market value. The warranty decision only answers whether the manufacturer will pay.

That distinction matters because insurers sometimes blur the issue. They may point to a denied warranty claim as if that proves the battery was already a problem. It does not. A warranty exclusion for accident damage is routine. The pertinent question is whether the battery was healthy before the loss and whether the current estimate matches the actual damage.

Why pre-accident battery health matters

Battery health affects value, total loss pressure, and diminished value after repair.

A well-documented pack gives you a stronger position on all three. If the battery showed normal operation before the crash, the insurer has less room to argue that poor range, hidden degradation, or prior faults were already dragging down the vehicle's value. That record also matters if the vehicle is repaired and later sold. Buyers and appraisers will ask whether the battery had pre-existing issues or whether the accident created the stigma.

Useful records include:

- State of health or range screenshots from the vehicle app or owner portal

- Service invoices showing no prior battery warnings or fault codes

- Charging records that reflect normal use

- Diagnostic reports pulled before teardown, if available

- Any pre-loss inspection or appraisal records that mention battery condition

Protect the paper trail

Handle battery documentation like evidence. Save the estimate, scan reports, photos of underbody damage, warning messages, towing invoices, and every supplement. If the vehicle changes shops or goes to a salvage yard, records often get harder to obtain and easier for the insurer to minimize.

If the insurer declares the EV a total loss, title branding becomes the next money issue. Before agreeing to owner retention or a settlement structure you do not fully understand, review what a salvage title means after a total loss.

Good records do more than support repair payment. They protect your valuation position, help challenge a weak total loss number, and preserve your argument for diminished value if the vehicle returns to the road with a documented battery event in its history.

How Battery Costs Can Trigger a Total Loss Declaration

The call usually comes after teardown. Your EV still powers on, the exterior damage does not look catastrophic, and then the shop adds a battery-related supplement. The insurer shifts from repair discussions to total loss handling because the battery estimate changed the economics of the claim.

Why battery estimates change the claim fast

Battery cost has outsized influence in EV claims because it is often the single largest repair line item. Once the estimate includes pack replacement, high-voltage diagnostics, cooling-system parts, hazardous material handling, calibration, and brand-specific labor procedures, the file can cross from repairable to uneconomical in one supplement.

That shift matters even when the pack is not obviously destroyed.

I see this in appraisal disputes regularly. The fight is often not whether the vehicle can be repaired in a technical sense. Instead, the dispute concerns whether the insurer wants to pay that repair bill once they compare it to the vehicle's Actual Cash Value.

The total loss decision is a formula issue

Insurers do not need a fire, a flooded pack, or a vehicle that will not charge to total an EV. They need repair costs that are high enough relative to the vehicle's value. If you want to see the framework adjusters use, review how insurers apply the total loss formula.

For EV owners, that creates a financial pressure point. A battery-related estimate can push the claim over the threshold before the average driver would expect it, especially on older EVs where market value has softened faster than battery-related repair pricing.

A common accident pattern

A side impact or underbody hit starts as a body claim. Then the shop documents possible intrusion near the pack, damage to shielding, disturbed cooling lines, fault codes, or isolation concerns. At that stage, the carrier may approve more diagnosis, or they may look at the growing estimate and move straight toward a total loss review.

The vehicle may still drive. It may still charge. Neither fact settles the claim.

That is the part many owner-focused battery cost guides miss. In an insurance file, the question is not only "What would I pay out of pocket to replace a pack?" The bigger question is whether battery-related repair cost changes the settlement path, the title outcome, and the value argument.

Why this matters to your settlement

A high battery estimate can hurt you two ways at once. It gives the insurer support for totaling the vehicle, and it can distract from the fact that the vehicle may have had a healthy battery before the loss. If the carrier uses a high repair figure to justify a total loss but assigns a weak Actual Cash Value, the owner absorbs the gap.

That is where documentation pays off. Strong proof of pre-loss battery health supports the valuation side of the claim, even if the insurer is no longer considering repair. A well-documented battery can affect the settlement number, and if the vehicle is repaired instead of totaled, it can also affect diminished value because a documented battery event changes how the market views the car.

A short explainer can help if you're sorting through these mechanics while the claim is active:

What owners should watch closely

Do not assume a total loss decision means the battery was certainly beyond repair. Sometimes that is true. Sometimes the carrier made an economic decision based on projected cost, parts availability, labor time, and risk.

Those are different conclusions, and the difference matters. One affects whether the vehicle was economically repairable. The other affects what your vehicle was worth before the accident and whether the insurer's payout is fair.

Strategies to Reduce Costs and Maximize Your Claim

When the battery estimate comes in high, most owners assume they only have two options. Accept the insurer's number or walk away from the car. That's rarely the full picture.

Look beyond a new OEM pack

Used and refurbished battery packs can slash replacement costs by 40% to 60%, with popular compact EVs landing around $3,000 to $8,000 for a refurbished pack versus $5,000 to $18,000 for a new one, according to Torque News coverage cited in the verified data.

That matters in two ways.

First, it can create a viable repair path when a new pack makes the claim look uneconomical. Second, it can expose a weak insurer position if their estimate assumes the most expensive possible parts route while ignoring legitimate alternatives.

Practical moves that help

Not every tactic fits every claim, but these are the moves worth considering:

- Ask for the battery sourcing basis. If the estimate assumes only a new OEM assembly, ask whether remanufactured or refurbished options were evaluated.

- Request the diagnostic basis for replacement. A battery quote should connect to a documented fault, contamination issue, impact concern, or safety finding.

- Preserve pre-loss battery evidence. App screenshots, charging history, service invoices, and BMS-related records can support market value.

- Compare the settlement to real vehicle value, not just the insurer's software output. If the ACV looks low, challenge the valuation before you sign.

Use the Appraisal Clause when valuation is wrong

This is the step many drivers miss. If the insurer undervalues the vehicle, you don't have to argue forever inside their internal process.

The Appraisal Clause can force the value dispute into a more defensible framework. Instead of letting the carrier's software dictate market value, the claim gets evaluated through independent appraisers using actual market data and condition analysis. In a battery-heavy EV claim, that matters because the battery's condition and contribution to value can materially affect the settlement outcome.

Claim advice: Don't argue only about repair cost. Challenge the vehicle value if the insurer's ACV doesn't reflect the battery's real contribution.

Decide whether repair, total loss, or salvage retention makes sense

This isn't just a technical decision. It's a financial one.

Sometimes the best move is to push back on a premature total loss and support a more realistic repair path. In other files, the better move is to accept total loss status but dispute the payout amount. In some situations, retaining the salvage can make sense if the battery, parts, or project value justify it.

What doesn't work is making that decision with incomplete numbers. You need to know whether the battery estimate is inflated, whether the ACV is suppressed, and whether the claim file reflects the vehicle's real pre-loss condition.

Your EV Battery Questions Answered

Does car insurance cover battery failure that wasn't caused by an accident

Usually, no. Standard accident claims focus on collision-related damage. If the battery failed from age, defect, or degradation, that usually points back to warranty or owner expense, not a crash claim.

Can I replace the battery with a larger one during a claim

Sometimes owners ask about upgrades during replacement. In practice, insurance typically owes for like-kind repair or value, not elective upgrading. If you want a larger-capacity pack, expect that to become a separate cost discussion.

Are battery prices still falling

Yes, based on projections. Goldman Sachs Research forecasts average EV battery prices dropping from $149/kWh in 2023 to approximately $80/kWh by 2026, a nearly 50% decline, driven by falling lithium prices and manufacturing efficiencies, according to Goldman Sachs Research on battery price trends.

That doesn't guarantee every repair bill drops immediately, because labor, manufacturer pricing, and parts availability still matter. But the long-term direction is favorable.

What else should I budget for as an EV owner

Charging setup often matters just as much as repair planning. If you're comparing ownership costs more broadly, it helps to compare home EV charger installation estimates so you're not looking at the battery in isolation.

If you're dealing with a disputed EV total loss or diminished value claim, Total Loss Northwest helps drivers challenge low valuations with certified independent appraisals. If the insurer is leaning on software instead of real market evidence, especially in a battery-driven claim, getting a defensible valuation can change the settlement outcome.