You just got the call or email. Your car is totaled. The adjuster sends a valuation report, and the number looks wrong the second you see it. You know what similar vehicles are selling for in your area. You know the tires were new, the maintenance was current, and the trim package matters. The insurer's number still comes in low.

That feeling is common, and in my opinion, your instinct is usually right.

If you're searching for total loss car appraisal near me, you probably don't need another vague article telling you that insurance is complicated. You need a practical way to push back, document your vehicle correctly, and use the tools already built into your policy. That starts with understanding one simple fact. A total loss value is not sacred just because an insurance company printed it.

Why Your Insurer's First Offer Is Just a Starting Point

Many assume the first settlement offer is based on hard market truth. It often isn't. It's usually a software-driven estimate built from the insurer's process, not from your financial interest.

Insurance carriers declare approximately 1.5 to 2 million vehicles as total losses annually, and insurer-generated valuations can undervalue vehicles by 20-40% compared to independent appraisals because they often rely on automated software, according to CCC Intelligent Solutions claims valuation data. If your number feels low, that doesn't make you difficult. It makes you part of a very common pattern.

What ACV means to you

The insurer will talk about Actual Cash Value, or ACV. You should think of ACV this way: what would it have cost to buy your vehicle, in its pre-loss condition, in your local market, right before the crash?

That's not the same as a generic database result. It's not the same as a stripped-down model with fewer options. It's not the same as a comp from far outside your area. And it definitely isn't accurate if the report ignores condition, service history, or upgrades.

If you want a more grounded sense of that number before you respond to the adjuster, review this guide on how fair market value is calculated after a total loss.

Practical rule: Never argue that the offer is “unfair” in general. Argue that the offer fails to reflect the vehicle's actual pre-loss market value.

Why the first number is rarely the last number

Adjusters work from reports. Reports can be challenged. That's the whole point.

A low first offer doesn't mean the claim is over. It means the valuation phase has started. The mistake I see most often is emotional acceptance. People are tired, they need a replacement car, and they assume delay will only make things worse. So they sign off on a bad number and move on.

Don't do that.

Use the first offer as a draft. Read every comparable vehicle. Check the mileage adjustments. Look for missing options. Ask whether the comps are local and recent. If the report doesn't hold up under basic scrutiny, treat it like any other weak valuation. Push back with evidence.

What to do before you say yes

Before you accept anything, do three things:

- Read the valuation report line by line. Check trim, mileage, condition, and options.

- Pull together your records. Maintenance, upgrades, photos, title history, and recent work matter.

- Decide whether you need an independent appraiser. If the report is built on weak comps or ignores value-adding details, you probably do.

You are not obligated to treat the insurer's first offer like a final judgment. It's an opening position. Act like it.

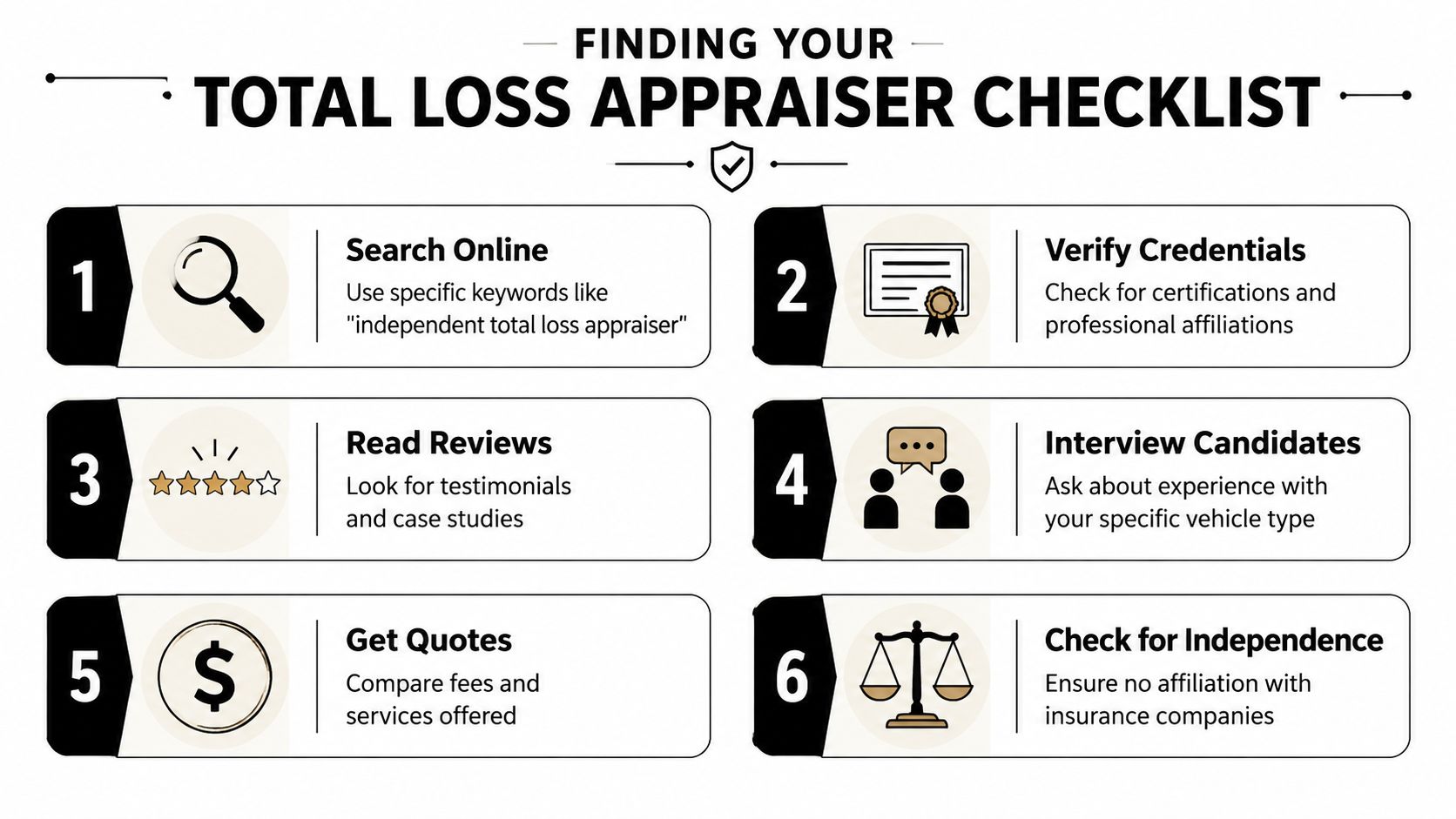

How to Find a Qualified Total Loss Appraiser

Typing total loss car appraisal near me into Google is easy. Picking the right appraiser isn't. You need someone who understands valuation, policy language, and your state's total loss rules. If they miss any one of those, your advantage diminishes.

A big reason this matters is state law. Thirty-seven U.S. states use a total loss ratio, typically 70-80% of ACV, and whether a vehicle is considered totaled can vary by state. The Zebra notes, for example, that a vehicle might be totaled in Washington but treated differently elsewhere, which changes how the claim proceeds and what the appraiser needs to address in the file, as outlined in this state-by-state total loss threshold guide.

What a good appraiser should know cold

A competent appraiser should be able to explain, in plain English, how they determine value. If they can't explain their process clearly, move on.

Look for someone who can speak specifically about:

- Local comparable vehicles. They should discuss recent sales or listings in your market, not broad national guesses.

- Vehicle-specific factors. Trim, condition, prior maintenance, packages, and upgrades should all come up quickly.

- Policy disputes. If they handle appraisal clause cases, they should know how to present a formal dispute file.

- State-specific total loss rules. This isn't optional. The threshold or formula in your state affects strategy.

If you want a starting point for vetting providers, review a directory-style resource focused on an independent auto appraiser near you.

Questions I'd ask before hiring anyone

Don't ask, “Can you help?” Ask sharper questions.

How do you source comparables for a total loss valuation?

You want a real answer about local market data, not a canned response about software.Have you handled my kind of vehicle before?

A daily driver, luxury SUV, modified truck, and collector car should not be appraised the same way.Do you work for insurance companies?

Independence matters. You want somebody representing the value issue, not somebody tied to carrier volume.What does your report include?

You want detail. Photos, options, condition analysis, comps, and a written valuation rationale should all be part of it.Will you help if the insurer pushes back?

A report without support can leave you doing the hard part alone.

A qualified appraiser should sound methodical, not salesy. If they promise a guaranteed payout increase before reviewing the file, that's a red flag.

Red flags people ignore

I've seen clients lose time with appraisers who looked polished online but did weak work. Watch for these problems:

- Opaque fees. If they can't explain exactly what you're paying for, stop there.

- No discussion of local comps. That usually means they're leaning too heavily on generic tools.

- No interest in your records. A serious appraiser wants documentation.

- Immediate promises. No honest appraiser can guarantee a result before reviewing the insurer's report and your vehicle details.

There's a simple parallel here. When people need a repair shop after a collision, they often use guides on how to find trustworthy Whitby mechanics because they want a vetting framework, not just a name. The same mindset helps when choosing an appraiser. Screen for independence, process, and credibility.

My recommendation

Hire the appraiser who asks the best questions, not the one who talks the fastest. In this kind of claim, discipline beats confidence every time.

Gathering the Right Documents for a Stronger Case

A strong appraisal doesn't start with an opinion. It starts with an evidence file.

When owners lose money on a total loss, it's often because key details never made it into the valuation record. If the insurer doesn't see the recent tires, the service history, the upgraded package, or the pre-loss condition, those things may never be reflected in the number. Your job is to make the missing value visible.

Build an evidence locker

Don't hand over random screenshots and hope for the best. Organize your records like you're proving the vehicle's real-world condition to somebody who knows nothing about it.

Here's the checklist I tell people to build first:

| Document | Why It's Critical |

|---|---|

| Pre-accident photos | Shows actual condition, cosmetic care, wheels, interior, and overall presentation before the loss |

| Maintenance records | Proves the vehicle was serviced and supports a stronger condition argument |

| Receipts for recent repairs | Documents money recently put into the car, such as brakes, tires, or mechanical work |

| Upgrade and accessory receipts | Helps support value for options, aftermarket parts, or added equipment |

| Original window sticker or build sheet | Confirms trim, packages, and factory options the insurer may have missed |

| Title and registration | Verifies ownership details and vehicle identity |

| Loan payoff information | Helps you understand the financial gap between value and payoff, if any |

| Carfax or vehicle history report | Supports ownership history and can help confirm pre-loss status |

| The insurer's valuation report | Gives your appraiser something specific to challenge line by line |

| Comparable listings you found locally | Useful when they closely match your vehicle and market |

Which documents matter most

Not every document carries the same weight.

Pre-accident photos are powerful because they cut through lazy condition assumptions. Maintenance records matter because they support your argument that this wasn't a neglected vehicle. Upgrade receipts help when the insurer ignores equipment that buyers in the market would notice and pay for.

Bring proof, not adjectives. “Well maintained” is a claim. Service invoices and clean photos are evidence.

Keep the file clean

A messy claim file slows everything down. Put your documents into clearly named folders or a single PDF if possible. Label photos by date. Highlight recent work. If you found local comparables, save the full listing pages, not just cropped price screenshots.

Also, don't alter or exaggerate. Credibility matters. A clean, honest file gives your appraiser something solid to work with and makes it easier to challenge a weak insurer report without drama.

Your Secret Weapon The Appraisal Clause

Most policyholders never use the strongest tool sitting in their own insurance contract. That tool is the Appraisal Clause.

The Appraisal Clause is standard in most U.S. auto policies, yet few people invoke it. According to Auto Appraisal Group's overview of total loss value disputes, independent appraisers win 85% of these disputes, and the process typically takes 30-45 days. That's why I consider it the most underused pressure point in a total loss claim.

What the clause actually does

The clause gives you a structured way to dispute value without immediately filing a lawsuit. In plain terms, you hire your appraiser, the insurer hires theirs, and if those two can't agree, an umpire gets involved. The fight is narrowed to value.

That matters because it shifts the conversation away from generic customer service scripts and into a formal dispute process. Once the clause is invoked, the insurer usually has to treat the disagreement more seriously.

If you want a plain-language breakdown of the process, this guide on the auto insurance appraisal clause is useful.

Sample language you can send today

You do not need to sound like a lawyer. You need to be clear.

Sample email or letter

Subject: Invocation of Appraisal Clause for Total Loss Valuation DisputeI am disputing the insurer's valuation of my vehicle in connection with my total loss claim. I do not agree that the current settlement offer reflects the vehicle's actual cash value in the local market prior to the loss.

Pursuant to the Appraisal Clause in my policy, I am formally demanding appraisal. Please confirm receipt of this demand and provide your position on the appraisal process, including selection of your appraiser, within a reasonable time.

I will designate my appraiser and provide contact information promptly.

Sincerely,

[Your full name]

[Claim number]

[Policy number]

[Vehicle year, make, model, VIN]

Short. Direct. No rambling.

What happens after you invoke it

Once you send the demand, the process usually becomes more structured:

- You appoint your appraiser. Choose someone experienced in total loss disputes, not just general vehicle pricing.

- The insurer appoints theirs. Their appraiser will defend the carrier's valuation position.

- Both sides exchange support, at which point report quality matters.

- If they disagree, an umpire may be selected. The umpire helps resolve the remaining gap.

- The value decision is issued. That figure then drives settlement.

A lot of claimants get intimidated here. Don't. The process is designed for disagreement. Disagreement is not a problem. It's the trigger.

Here's a video that gives additional context on how appraisal disputes work in practice:

Mistakes that weaken your leverage

I see the same errors over and over.

- Waiting too long. Once you accept the offer, your bargaining power can shrink fast.

- Arguing emotionally instead of factually. Anger won't move a valuation. Evidence might.

- Using a weak appraiser. The clause is only as strong as the report behind it.

- Sending a vague demand. Be specific that you dispute value and are invoking the Appraisal Clause.

If the insurer says, “That's our final number,” that often means it's time to move out of phone-call mode and into clause-invocation mode.

My advice on timing

If the insurer's report is clearly off and informal negotiation goes nowhere, invoke the clause. Don't spend weeks hoping the same flawed process will suddenly produce a fair result. It usually won't.

Appraising High-Value Custom and Classic Vehicles

If your totaled vehicle is a classic, collector, exotic, or custom build, standard valuation software is a poor fit. It tends to flatten important differences that drive price.

That's not a minor issue. Standard insurer valuations can undervalue unique features on custom or collector cars by 40-60%, and a proper appraisal uses real-time data from auction sources such as Mecum and Barrett-Jackson. Collector car sales have also risen 15% in the last year, according to this collector and custom appraisal discussion.

Why generic comps fail on special vehicles

A standard daily driver can often be valued from normal retail market activity. A restored muscle car, rare trim package, engine-swapped build, or high-end custom truck cannot.

Those vehicles need a different proof set:

- Build sheets and factory documentation for original equipment and rarity

- Restoration invoices to support work quality and investment

- Detailed pre-loss photos to show condition and finish quality

- Specialty market comps from auctions and enthusiast markets

- Modification records for parts, fabrication, and labor

A software report that lumps your vehicle into a generic trim line can miss the entire reason the vehicle was worth more.

What a proper specialty appraisal looks at

A real appraisal for a special vehicle should weigh market behavior, not just database defaults. That means looking at auction results, niche listings, provenance, quality of restoration, and whether modifications add value or narrow the buyer pool.

On a classic or custom vehicle, the question isn't just “What is this model worth?” It's “What would a real buyer have paid for this specific example right before the loss?”

That distinction is everything.

Don't let the insurer erase your documentation

Owners of collector and custom vehicles often have the best records and still get lowballed because they don't present those records in a way the claim process can use. Gather the build sheet, receipts, prior appraisals if you have them, and clear photos. Then make sure the appraiser knows how to position those materials against the insurer's generic valuation.

If you're in Oregon or Washington and need an appraiser for this kind of dispute, Total Loss Northwest handles independent total loss and diminished value appraisals, including appraisal clause disputes, using market-based valuation rather than insurer software.

From Appraisal to Settlement What Happens Next

Once the appraisal is underway, the claim stops being a guessing contest and starts becoming a documented valuation dispute. That's where many owners finally feel some relief. The process has a structure, and structure is what lowball offers hate.

A certified appraiser's methodology matters here. The process typically includes vehicle inspection, local market analysis of 10-20 comparable vehicles sold in the last 90 days, ACV computation, and a detailed 20-30 page report, and that approach secures an average of $2,000-$10,000 more than the insurer's initial offer, according to this overview of total loss appraisal methodology.

How the final stage usually unfolds

After your appraiser finishes the report, the insurer's side has to deal with the substance of it. They can't just keep repeating the same original number and expect that to carry the day.

The usual sequence looks like this:

Your report is submitted and supported.

The appraiser presents the comps, condition analysis, and valuation logic.The insurer reviews or counters it.

Sometimes their appraiser adjusts. Sometimes they resist.The appraisers negotiate value.

If the claim is in appraisal, this is the heart of the dispute.An umpire may decide the remaining gap.

If needed, the umpire resolves the disagreement on value.The settlement amount is updated.

Once the value is set, the carrier processes payment based on the policy and claim details.

What to expect from the payment

When the value issue is resolved, the insurer calculates the final settlement according to the policy. If there's a deductible involved, that may still be applied depending on the claim structure and fault position. If there's a lender, payoff handling becomes part of the final paperwork.

Don't confuse valuation victory with instant check-in-hand timing. There can still be title and payment steps. Stay organized and keep copies of everything.

When appraisal isn't the end of the story

Most value disputes should be handled through evidence and the policy process. But occasionally the conflict goes beyond valuation. Maybe liability is disputed, maybe there are bad-faith issues, or maybe the carrier's conduct creates a separate legal problem.

In those situations, it helps to understand your broader legal options after a totaled car accident so you know when the problem has moved beyond appraisal and into legal territory.

You don't need to know every insurance rule. You need a clear file, a sound valuation, and the willingness to dispute a bad number before it becomes permanent.

If you've made it this far, you already know more than most claimants do when they accept the first offer. That alone changes the outcome. The insurer has a process. Now you have one too.

If you're dealing with a low total loss offer and need an independent review, Total Loss Northwest provides total loss and diminished value appraisals for Oregon and Washington vehicle owners, with appraisal clause support for disputed valuations.