A common airbag replacement cost is $3,000 to $6,000+ for a full system after a crash, and a single deployed airbag often runs about $1,500 once parts and labor are included. That's enough to change the entire direction of your insurance claim, because once airbags go off, you're usually no longer arguing about a simple repair. You're arguing about whether the car should be repaired at all.

That's the moment many drivers find themselves in. The crash is over. The cabin still smells burnt from the airbag propellant. There's dust on the dash, maybe a torn steering wheel cover, maybe a split dashboard on the passenger side. Then the adjuster starts talking about an estimate, and the number on paper doesn't match what a proper repair takes.

When airbags deploy, the primary concern usually isn't just “what does a new bag cost?” The fundamental problem is whether the insurer is understating the safety-system repair so they can keep the vehicle in the repairable category and control the payout. If you were not at fault, that matters even more. A borderline vehicle is often worth more to you as a fair total-loss settlement than as a repaired car with a crash history and lingering value loss.

The Shocking Price Tag Behind the Powder Cloud

The crash is over, the cabin is full of dust, and the steering wheel or dash is ripped open. At that point, the claim stops being a simple body-shop estimate. It becomes a fight over whether the insurer is pricing the safety repair correctly or keeping the numbers low enough to avoid a total-loss payout.

Drivers often focus on the visible bag that went off. The actual exposure is the bill that follows deployment. Once the supplemental restraint system is involved, a thin preliminary estimate can make a borderline vehicle look repairable on paper even when the full repair picture points somewhere else.

I see that gap all the time in claim files. The first estimate may include obvious damage and little else. A more careful review adds related safety items, diagnostic work, and manufacturer-required procedures, and the value of the claim changes fast. That does not mean the second estimate is padded. It usually means the first one was incomplete.

Practical rule: Treat airbag deployment as a safety-system claim with total-loss implications.

That point matters most on lower-value vehicles and older daily drivers. Airbag-related costs can consume a large share of the car's actual cash value before the shop even gets deep into body damage, calibration, or hidden impact repairs. If you want to challenge a weak insurer position, it helps to understand how CCC market valuations can shape a total-loss offer and why an understated repair estimate benefits the carrier.

Published consumer repair guidance has put post-crash airbag work in the several-thousand-dollar range for many vehicles, with much higher totals when multiple components are involved, as noted earlier from ConsumerAffairs. For an owner trying to decide whether to accept a repair path, that number is not just a repair expense. It is often the strongest fact in the file for arguing that the vehicle should be totaled and valued fairly.

That is the part many accident victims miss. A deployed airbag is expensive bad news, but it can also be the fact that forces an honest settlement discussion.

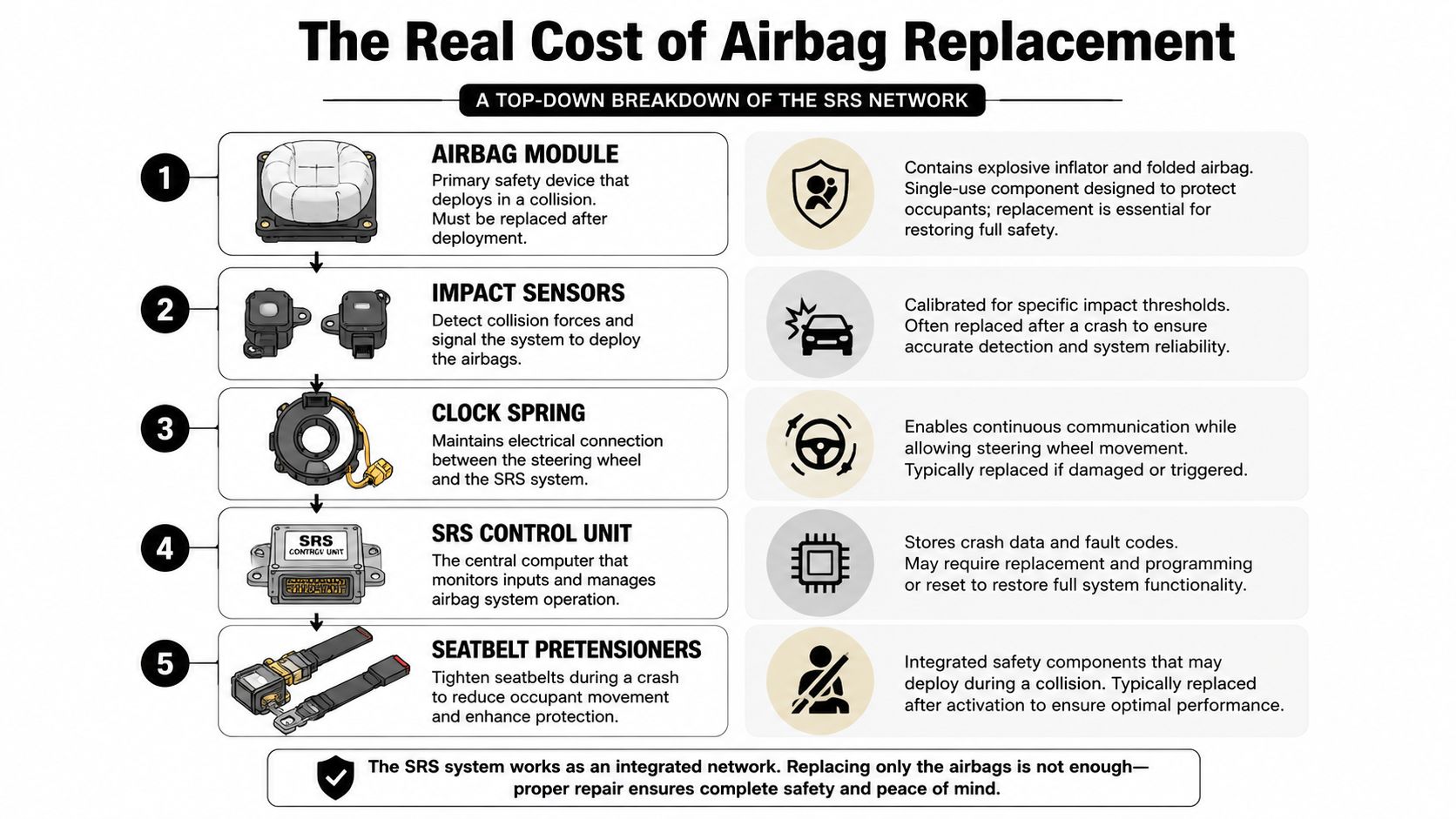

Breaking Down the Real Cost of Airbag Replacement

Airbag deployment changes the claim immediately. Once the bags fire, the repair bill stops being about one blown component and starts becoming a safety-system rebuild.

A modern SRS includes the airbags, the control module, crash sensors, steering wheel components, wiring connections, and the diagnostic steps needed to return the system to proper working order. As noted earlier, published consumer repair guidance puts a single airbag replacement around $1,500 in many cases, while a broader SRS repair can climb into the $3,000 to $6,000-plus range.

What usually appears on a proper estimate

A serious estimate usually includes more than the visible bag. Common line items include the airbag unit itself, the airbag control module, crash sensors, and the clock spring when the steering wheel bag deployed. Earlier published repair guidance also put typical totals around $773 for a control module, $399 for a crash sensor, and $439 for a clock spring.

That list matters for one reason. If those parts are absent, the estimate may be incomplete in a way that keeps the vehicle under the insurer's repair threshold.

Why early estimates often come in low

I see this pattern all the time in files that later turn into total-loss disputes. The first sheet may show the obvious deployed bag and visible body damage, but skip a module, leave out a sensor, or ignore the diagnostic and calibration work the shop will eventually have to perform. That lower number can make a borderline vehicle look repairable when it really is not.

Read the estimate like a negotiator, not just an owner. If the SRS section looks thin, ask what is missing and why.

If the estimate only prices the blown airbag, it is not pricing the full safety repair.

That gap can affect valuation too. An understated repair estimate can push the claim away from a total loss, especially when the carrier is also relying on software-driven values. If you want to see how those numbers get built and challenged, review these CCC auto valuation issues in total-loss claims.

A quick way to review the repair sheet

Use this checklist when the insurer or shop sends over an estimate:

| Item on estimate | Why it matters |

|---|---|

| Airbag listed | Confirms the deployed unit itself is included |

| Control module listed | Shows the crash-event memory and system reset were addressed |

| Crash sensors listed | Indicates the estimate covers impact-triggered hardware |

| Clock spring listed | Often required when the steering wheel airbag deployed |

| Diagnostics or calibration noted | Shows the repair plan treats the SRS as a working safety system |

Missing items do not automatically prove bad faith. They often do prove the first number is too low. For an owner fighting a weak offer, that difference is not academic. It can be the fact that turns a repairable-looking claim into a stronger total-loss argument.

Why Your Vehicle's Make and Model Drastically Changes the Price

Two vehicles can have airbags deploy in similar collisions and end up with very different repair bills. That isn't a mystery. It's how parts pricing and labor work in practice.

A basic commuter sedan and a high-end luxury car don't use the same parts network, don't require the same disassembly, and don't get billed at the same labor rate. That matters when an insurer hands you a generic estimate that feels suspiciously light.

The difference isn't small

Published repair guidance shows labor can vary by 400%, from $100-$150 at an independent shop to over $1,000 at a Porsche or Audi dealership for complex work. The same source notes a full-system replacement on a Mercedes S550 can cost $4,500-$6,500, while a comparable repair on a Toyota Corolla might cost $2,000-$3,000, according to CarParts on airbag replacement labor and model-specific cost differences.

That's the kind of spread insurers tend to blur when they write a broad estimate instead of a vehicle-specific one.

What drives the spread

Some of the reasons are obvious. Luxury brands charge more for parts. Dealer labor is often higher. But the hidden issue is system complexity.

A newer vehicle may have front airbags, side airbags, curtain airbags, and knee airbags integrated into a tighter interior package. Removing trim, steering components, seat assemblies, or headliner sections changes the labor picture fast. It also raises the chance that one missed component keeps the estimate artificially low.

Here's the practical comparison:

| Vehicle type | Likely repair reality |

|---|---|

| Older basic sedan | Fewer integrated safety components and simpler labor path |

| Mainstream late-model SUV | More interior disassembly and more possible deployment points |

| Luxury sedan or premium SUV | Higher parts prices, dealer-heavy repair path, more expensive labor |

| Performance or specialty model | Brand-specific parts and repair procedures can push the estimate up fast |

A generic repair estimate is a red flag when your vehicle is anything other than a basic model with a simple restraint system.

What to push back on

If you drive a premium brand, a truck with a more complex cabin layout, or a newer vehicle with layered safety systems, challenge any estimate that looks built from averages instead of your actual trim and equipment. Ask what parts category was used, what labor source was assumed, and whether the estimate reflects your exact make, model, and year.

That's where many owners lose their advantage. They accept an insurer's low repair number as if it were objective. Often it's just incomplete.

OEM vs Aftermarket Parts A Critical Strategic Choice

Part choice changes more than the invoice. It changes the claim.

Once an insurer decides the car might be repairable, the next pressure point is usually parts sourcing. You may see references to OEM, aftermarket, or recycled components. On paper, that can look like a simple cost-saving exercise. In a real claim, it's a fight over safety, restoration quality, and whether the repair estimate reflects the vehicle you owned before the crash.

Why OEM often matters more than the insurer wants to admit

Published consumer guidance shows a driver airbag replacement is often cited at $1,000-$2,470, and the use of OEM parts on luxury vehicles can push multi-airbag repair totals above $6,000, according to Sunbit's airbag replacement cost guide.

That matters most for:

- Newer vehicles: The owner bought a vehicle with a specific safety configuration and parts standard.

- High-value vehicles: Cheap parts can understate the true cost to restore the car to pre-loss condition.

- Collector or custom vehicles: A low-cost repair path may not reflect the market impact after a deployment event.

The strategic point most owners miss

If the insurer builds its repair estimate around the cheapest acceptable parts path, that can keep the car under the line where they'd rather total it. But if OEM-equivalent restoration is the proper standard for your vehicle, the estimate should reflect that.

That's not gamesmanship. That's an accurate claim.

When the repair estimate depends on bargain parts to stay viable, the repairability decision itself deserves scrutiny.

For a not-at-fault owner, this can be decisive. A repaired vehicle with crash history and airbag deployment on record can carry a market stigma even if the shop does clean work. If a proper OEM-based estimate pushes the vehicle into a total-loss outcome, that may be financially better than accepting a repaired car that no longer holds the same market position.

A practical decision table

| Parts choice | Claim impact |

|---|---|

| OEM | Better reflects restoration cost on many newer or premium vehicles |

| Aftermarket | May lower estimate, but can also lower the credibility of the repair path for some vehicles |

| Salvage or recycled | Can reduce cost sharply, but may create disputes over quality, compatibility, or market value impact |

If your vehicle sits near the edge between repair and total loss, this is not a small detail. It's one of the central questions in the file.

When Airbag Costs Trigger a Total Loss

A driver gets the first estimate after a crash and sees a few obvious line items. Driver airbag. Passenger airbag. Dash work. The file still looks repairable. Then the missing safety-system parts start getting added, and the claim shifts fast.

That shift is often where the financial decision gets made. Consumer guidance from SoFi's discussion of airbag costs and total-loss decisions notes that full airbag-system repairs can run **$3,000 to $6,000 **. On a modest-value vehicle, that is enough to change the claim from "repair it" to "pay it out."

What the insurer is actually measuring

The insurer is comparing two numbers. One is the vehicle's actual cash value. The other is the repair cost, sometimes with salvage value worked into the calculation depending on the state and carrier method.

If the estimate is thin, the car stays in the repair lane. If the estimate reflects the full SRS repair, recalibration, trim replacement, and related labor, the same vehicle can cross into total-loss territory. That is why owners should understand the total loss formula used in these claims. The formula explains why a safety-system line item can change the outcome before the body estimate is fully developed.

I see this in borderline files all the time. The first number is often just low enough to keep the carrier's options open.

Costs that get missed early

The expensive part is not limited to the bags you can see hanging out of the wheel or dash. A proper post-deployment estimate may include sensors, seat belt pretensioners, dash panels, module work, coding, calibration, and diagnostic time. Some shops also flag related warning-light work that cannot be ignored if the car is going back on the road.

One omitted item will not always total the vehicle. But on an older sedan, an economy crossover, or any car with only moderate pre-loss value, one missing SRS component can be the difference between a repair authorization and a total-loss settlement.

That is why I tell owners to read the estimate like a valuation document, not just a repair bill.

Why that can help you

A total loss is not automatically bad news. In many airbag claims, it is the cleaner result.

A repaired vehicle with deployment history usually carries market baggage after the work is done. Future buyers ask questions. Trade offers get tighter. If the insurer keeps the car repairable by trimming the estimate, you may end up with the long-term loss while they save money upfront.

For a not-at-fault owner, that is the wrong outcome. If the repair cost supports a total loss, pushing for a complete estimate can improve your position in the settlement discussion. It gives you a stronger basis to reject a low repair path and argue for a payout that reflects what the loss did to the vehicle.

If the file later turns into a dispute over module resets or warning-light issues, get that addressed by a qualified shop. For readers in Hawaii, Hawaii's choice for airbag light resetting is one example of the kind of specialized service these claims sometimes require.

Here's a short explainer that helps many owners understand why these decisions become contentious once the repair estimate climbs:

What strengthens your position

What works

- A line-item estimate that includes the full safety system: airbags, belts, modules, sensors, coding, and calibration

- A value discussion tied to the actual vehicle: trim, mileage, condition, options, and local market comps

- An independent review when the estimate looks artificially lean: especially on a borderline total-loss file

What hurts your position

- Treating the first insurer estimate as final

- Assuming visible damage tells the whole repair story

- Authorizing repairs before the full SRS scope is documented

Once repairs start, the argument usually gets harder. The stronger move is to get the actual numbers on paper first, then decide whether repair still makes financial sense.

Your Action Plan After an Airbag Deployment

You walk away from the crash, see powder in the cabin, and the insurer starts talking repair before anyone has shown you a full estimate. That is the point where owners lose ground. An airbag deployment changes the claim immediately, and you need the file documented before you agree to a repair path that may not make financial sense.

Treat the first 48 hours like evidence gathering. Your job is to pin the claim to written facts, a complete estimate, and the actual pre-loss value of the vehicle. If the numbers are close, airbag-related repairs can support a total loss position instead of a rushed repair decision.

Follow these steps in order

Photograph the cabin and the damage before teardown

Get clear photos of the steering wheel, dash, seats, seat belts, warning lights, windshield area if affected, and the exterior impact points. Take wide shots and close-ups. You want proof of deployment and collision severity before the car disappears into shop intake.Get the insurer's estimate in writing

A phone summary is not enough. Ask for the line-item estimate and read it. That document tells you whether the adjuster priced the full SRS repair or only the obvious parts.Check what is missing, not just what is listed

Airbag claims get underestimated when the paperwork is thin. Look for airbags, seat belt components, sensors, diagnostic work, coding, calibrations, and any scan or reset procedures tied to the safety system. If the estimate uses vague language or broad part allowances, ask for clarification in writing.Do not authorize repairs too early

Once teardown starts and parts get ordered, the claim tends to drift toward repair. That makes it harder to argue later that the vehicle should have been totaled. On a borderline file, waiting for a complete scope can protect thousands of dollars in settlement value.Be disciplined on the first recorded call

Stick to facts. State where the loss happened, what was hit, and that the airbags deployed. Do not guess about hidden damage, and do not say you are fine with repair before you have seen the full estimate.

Ask this early: “Are you evaluating this as a potential total loss, and will you send me the complete written estimate?”

If the estimate looks light

Start with a simple paper review.

- Missing safety items: If the estimate lists deployed airbags but skips related belt work, scans, or calibration steps, ask why.

- Unclear parts assumptions: Ask whether the estimate assumes OEM, aftermarket, or recycled parts.

- Compressed labor: If the labor time looks lean for your vehicle, ask which procedures were excluded.

- No value discussion: If the carrier is pushing repair without a solid pre-loss valuation, request the valuation report too.

If you need a broader checklist before you get into the numbers, these steps after a car accident give you a useful starting point.

Know when to bring in outside help

Some files need pressure from someone outside the claim loop. If the insurer's estimate feels incomplete, or the value they assigned to the vehicle seems low, an independent appraiser can review both sides of the equation. That matters because total loss decisions are not just about repair cost. They also depend on whether the carrier has understated what your vehicle was worth before the crash.

If your policy includes an appraisal clause, use it when the numbers justify it. Total Loss Northwest handles total-loss and diminished-value appraisals in Washington and Oregon, and that kind of review can help when an airbag deployment is being treated like an ordinary repair file.

If the dispute later shifts to post-repair warning lights or system follow-up on an island-based vehicle, Hawaii's choice for airbag light resetting is a specialized service example worth knowing about.

Timing matters here. Get the estimate, review the omissions, and challenge the value before the insurer's number hardens into the default outcome.