You did everything right after the crash. The other driver was cited, their insurer accepted liability, and then the offer arrived. It doesn't cover the full loss. If your car is a total loss, the valuation feels thin. If it was repaired, the diminished value number may feel pulled from nowhere. And if your damages exceed the other driver's limits, you're suddenly dealing with your own insurer too.

That's where an underinsured motorist claim is often confusing. The basic idea sounds simple. The at-fault driver didn't have enough coverage, so your policy should make up the difference. In practice, the fight often turns on proof. Not just proof of fault, but proof of value.

As an appraiser, I see the same mistake over and over. People focus on whether they have UIM coverage, but not on how the loss amount is being measured. That's the part that changes the outcome. A weak valuation keeps the claim small. A documented, supportable valuation strengthens your position.

What Is an Underinsured Motorist Claim

An underinsured motorist claim comes into play when the driver who caused the crash has insurance, but not enough insurance to pay for the damage they caused. That shortage can affect injury claims, property damage claims, or both, depending on your policy language and your state's rules.

A simple way to think about it is this. The other driver's policy pays first. Your UIM coverage is the backup layer that can fill part of the remaining gap.

How UIM differs from UM and collision

People often mix up three separate coverages:

| Coverage | What triggers it | What it generally does |

|---|---|---|

| Uninsured motorist | The at-fault driver has no applicable insurance | Helps cover losses that would have been paid by the other driver's liability policy |

| Underinsured motorist | The at-fault driver has insurance, but not enough | Helps cover the shortfall, subject to your policy terms |

| Collision coverage | Your vehicle is damaged in a crash, regardless of fault in many cases | Pays for your vehicle damage under your own policy, usually subject to your deductible |

That distinction matters because the claims process, valuation method, and available rights can be different under each path. If you want a plain-language comparison of UM coverage basics, this overview of uninsured motorist coverage is a useful starting point.

Why this coverage matters in the real world

A lot of drivers carry too little insurance for a serious crash. The national uninsured motorist rate rose to 15.4% in 2023, which means more than one in seven drivers may not have adequate coverage to pay for the damage they cause, according to the Insurance Research Council data cited by the Insurance Information Institute.

That statistic is about uninsured drivers, but it points to the same claims environment that makes UIM so important. Low liability limits don't go very far when a newer vehicle is totaled, when repairs are extensive, or when a crash involves both bodily injury and property damage.

Practical rule: Don't treat UIM as an obscure add-on. It exists because the at-fault driver's policy often isn't enough.

The two forms people usually care about

Most policyholders run into one or both of these:

- Bodily injury UIM covers injury-related losses such as medical bills, lost wages, and pain and suffering if your policy and state law allow it.

- Property damage UIM may apply to vehicle damage, but only if your policy includes that protection and your state recognizes it in that form.

Many claimants get blindsided. They assume “underinsured motorist” automatically means every unpaid loss gets covered. It doesn't. Coverage depends on the wording in your policy, the kind of damage involved, and whether the other driver's limits are first used up.

When You Can Use Your UIM Coverage

You can usually use UIM coverage only after a specific trigger is met. The at-fault driver's liability coverage must be fully paid out first. That's why adjusters keep using words like exhaustion and offset.

Here's the core rule in plain English. Your insurer doesn't step in just because the other driver's limits look low. It steps in after those limits are paid and after you can show that your damages exceed that amount.

The exhaustion and offset rule

A UIM claim is typically built as an exhaustion/offset mechanism. The at-fault driver's liability limits must be fully paid before UIM coverage applies, and your insurer covers only the uncompensated portion of your proven damages, up to your own UIM policy limit, as explained in this guide on how UIM coverage works.

That's why the first settlement matters so much. If the liability claim isn't documented properly, your own carrier may argue that UIM was never triggered, or that the numbers don't support the amount you're asking for.

A simple example of the gap

Use this framework when you're trying to understand whether a UIM claim is worth pursuing:

- Add up the proven damages. For a property damage claim, that may include total loss value or diminished value, depending on the facts and coverage.

- Subtract the at-fault driver's payment. That's the amount already available from the liability claim.

- Check your own UIM limit. Your policy may cap what you can recover even if your loss is higher.

If the other driver's insurer pays its full limit and your actual loss is still higher, that remaining gap is where a UIM claim may operate.

Why policy language matters more than people expect

Two policies can both say “underinsured motorist coverage” and still operate differently. One may reduce your available recovery by the amount already paid by the other insurer. Another may contain language about setoff, consent to settle, notice, or appraisal rights that changes strategy.

A few items deserve close review before you sign anything:

- Settlement consent requirements so you don't accidentally affect your UIM rights.

- Definition of covered damages because some policies are narrower on property damage than people expect.

- Proof requirements such as confirmation of the at-fault driver's limits and payment.

- Dispute resolution language including appraisal or arbitration provisions.

In Oregon and Washington, the exact wording in the policy drives the next move. People lose advantage when they treat UIM as automatic. It's contractual. The contract controls.

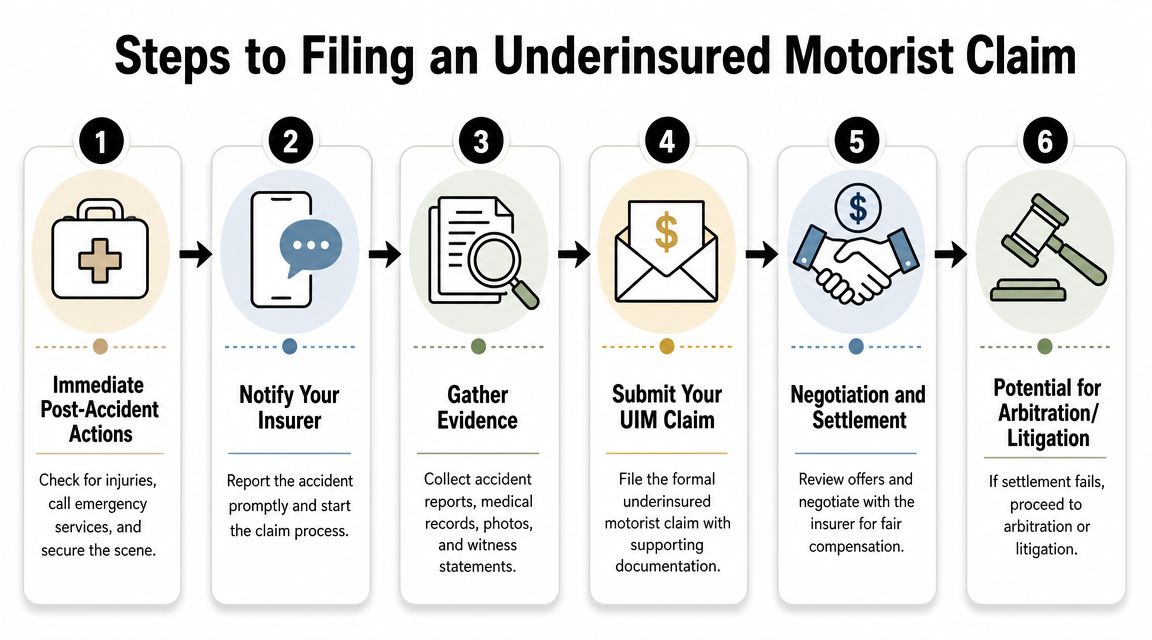

How to File an Underinsured Motorist Claim

The process is often made harder than necessary by delaying file organization. A good UIM claim starts with clean documentation. Your insurer is looking for a chain of proof. Fault, damages, limits, exhaustion, and notice all need to line up.

Start with the basics immediately after the crash, even if you think the other driver's carrier will handle everything.

What to gather first

In many states, UM/UIM bodily injury coverage often has minimum limits around $15,000/$30,000 or $25,000/$50,000, and serious losses can exceed those amounts. That's one reason documentation becomes critical. This overview of UM and UIM claim documentation notes the practical need for police reports, medical records, and proof that the other party's limits were exhausted.

For a property damage focused file, gather these early:

- Police report if one was made, because fault disputes often spill into coverage disputes.

- Photos of the damage before teardown, salvage transfer, or repairs.

- Repair estimate or total loss valuation from the insurer.

- The at-fault carrier's declarations or limits information if available.

- Written proof of settlement or tender from the at-fault insurer.

- Receipts and ownership records for options, upgrades, recent work, or custom equipment.

- Comparable vehicle listings if the insurer's valuation appears weak.

A short explainer may also help if you want to hear the process discussed visually:

Notify your own insurer early

Don't wait until the liability settlement is done to alert your carrier. Give notice as soon as it appears the other driver's policy may be inadequate.

A simple notice can look like this:

Subject: Notice of Potential Underinsured Motorist Claim

Claim Number: [insert if known]

Date of Loss: [insert date]

Insured: [your name]

Vehicle: [year, make, model, VIN]Please accept this letter as notice of a potential underinsured motorist claim arising from the above loss. The at-fault driver's liability coverage may be insufficient to fully compensate my damages. Please confirm receipt of this notice, provide any policy provisions that apply to UIM claims, and advise of any consent, documentation, or preservation requirements.

Sincerely,

[Your name]

That kind of letter doesn't argue the whole claim. It preserves your position and forces the carrier to identify its process.

Filing workflow that keeps the claim clean

Follow this sequence:

- Open the liability claim first. Get the other carrier's position on fault and limits.

- Notify your own carrier of a potential UIM claim. Do it in writing.

- Build the damages file. For a vehicle, that means valuation evidence, not just the insurer's report.

- Get written proof of exhaustion or tender. Oral summaries aren't enough.

- Submit the UIM package. Include the loss documents in a logical order.

- Read the policy before accepting the final amount. Notice, consent, appraisal, and arbitration language matter.

Keep one master file with every email, letter, photo, and valuation document. Messy files create slow claims.

Deadlines matter, but they vary. The safest move is to review the policy and local law early, not after negotiations stall.

Proving Your Vehicle's True Value

Many underinsured motorist claims go sideways when the insurer agrees there's coverage and the other driver's policy was insufficient, yet keeps the payout low by disputing the vehicle's value.

That happens most often in total loss and diminished value claims. The argument isn't really about whether you suffered a loss. It's about how the carrier measures that loss.

Why valuation becomes the real fight

A major gap in typical UIM advice is the failure to address vehicle valuation disputes. UIM is supposed to cover the gap between the other driver's limits and your damages, but the fight is often over the true Actual Cash Value of the vehicle, especially for newer, custom, or high-value cars where standard valuation tools may miss the market, as noted in this article on uninsured and underinsured motorist coverage.

That's not a technical side issue. It's the number that often controls the claim.

Common ways insurers undervalue a vehicle

Insurers often rely on valuation systems such as CCC or Mitchell, then apply condition adjustments, mileage adjustments, and comparable-vehicle selections that can pull the number down. Those tools aren't automatically wrong, but they are not automatically right either.

Watch for these problems:

- Weak comparable vehicles that don't match trim, drivetrain, package content, or market desirability.

- Condition downgrades that don't reflect the vehicle's actual pre-loss state.

- Missing options and packages such as technology, towing, performance, or premium interior equipment.

- Geographic mismatch where the valuation pulls from a market that doesn't reflect your local replacement cost.

- Unsupported adjustments that appear in the report without meaningful explanation.

If you manage commercial units, the same issue shows up in business claims. Shops that work around vehicle downtime, equipment specifications, and commercial repair realities often understand how much value can be lost when a carrier oversimplifies the vehicle. A practical example is the operational perspective discussed in fleet collision repair, where repairability, use case, and equipment details affect real-world value.

The insurer's number is an opening position

Many owners make the same assumption. If the insurer sent a total loss report, that must be the number. It isn't. It's the insurer's position based on the inputs it chose.

That's why I tell clients to review the report like an evidence packet, not like a verdict.

Ask these questions:

| Question | Why it matters |

|---|---|

| Does the report list the correct trim and drivetrain? | A wrong trim can distort the base market value |

| Are the comparables actually comparable? | Small spec differences can move price materially |

| Were options omitted? | Missing equipment lowers the valuation |

| Are condition adjustments supported by photos or inspection notes? | Unsupported deductions deserve challenge |

| Does the market area make sense? | Replacement cost depends on the actual market |

If you need a clearer grounding in how value should be measured, this explanation of fair market value is useful. It helps separate a genuine market-based number from a software-generated figure that hasn't been tested.

A low valuation doesn't become fair just because it was printed in a formal report.

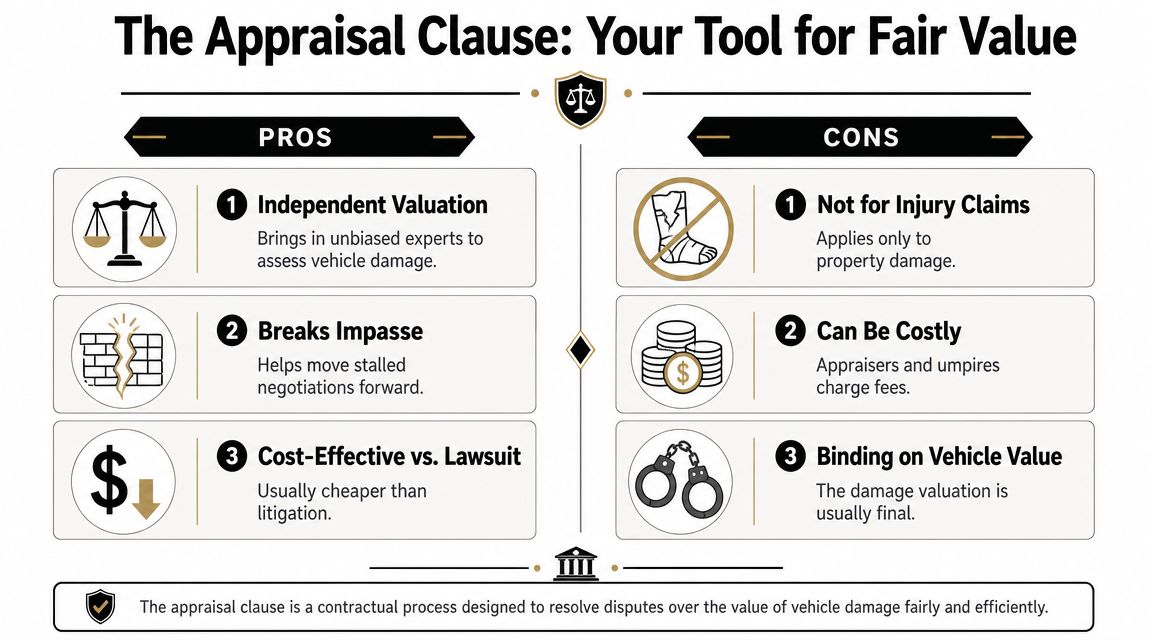

Using the Appraisal Clause to Get Paid Fairly

Once the dispute is about value, argument alone usually won't fix it. You can send emails, highlight errors, and point out missing options. Sometimes that works. Often it doesn't. The adjuster reiterates the original report.

That's when the appraisal clause becomes important.

What the appraisal clause actually does

The appraisal clause is a policy mechanism for resolving disputes over the amount of loss. It doesn't decide liability for the crash. It doesn't resolve bodily injury disagreements. It addresses the value question.

That matters in UIM property damage claims because the claim rises or falls on provable loss amount. State rules can affect value in major ways. Maryland's consumer guidance, for example, notes that uninsured coverage may require the other driver to be 100% at fault and that property damage claims can involve a $250 deductible by law. The broader point carries into UIM practice as well. Liability and damages both have to be proven, and an independent appraisal report can provide strong evidence of the financial loss. See the Maryland guidance on uninsured motorist claims.

Why this process works better than informal back-and-forth

An appraisal clause changes the conversation in three ways:

- It forces evidence into the record. The insurer has to defend a valuation, not just repeat it.

- It narrows the issue. Instead of arguing about everything, the process centers on the amount of loss.

- It puts independent experts in the room. That's usually better than letting software assumptions control the file.

In Oregon and Washington property damage disputes, this can be far more effective than trying to negotiate from the owner's opinion alone. Market support matters. Documentation matters. A structured process matters.

How to invoke appraisal without making avoidable mistakes

The right way to invoke appraisal depends on your policy wording, but the practical sequence usually looks like this:

- Read the policy first. Confirm that appraisal applies to the dispute you have.

- Identify the valuation disagreement clearly. Total loss value, diminished value, or another property amount.

- Give written notice. Keep it direct and tied to the policy language.

- Choose an independent appraiser who understands market valuation. This is not the place for guesswork.

- Submit supporting documents. Listings, build data, service history, photos, pre-loss condition evidence, and option verification all matter.

- Stay disciplined. Appraisal is strongest when the issue stays focused on value.

A detailed overview of the insurance appraisal clause can help you understand how the process is usually framed and what documents tend to matter most.

“If the insurer's valuation is weak, don't just object. Replace it with a better one.”

That's the practical difference between frustration and advantage.

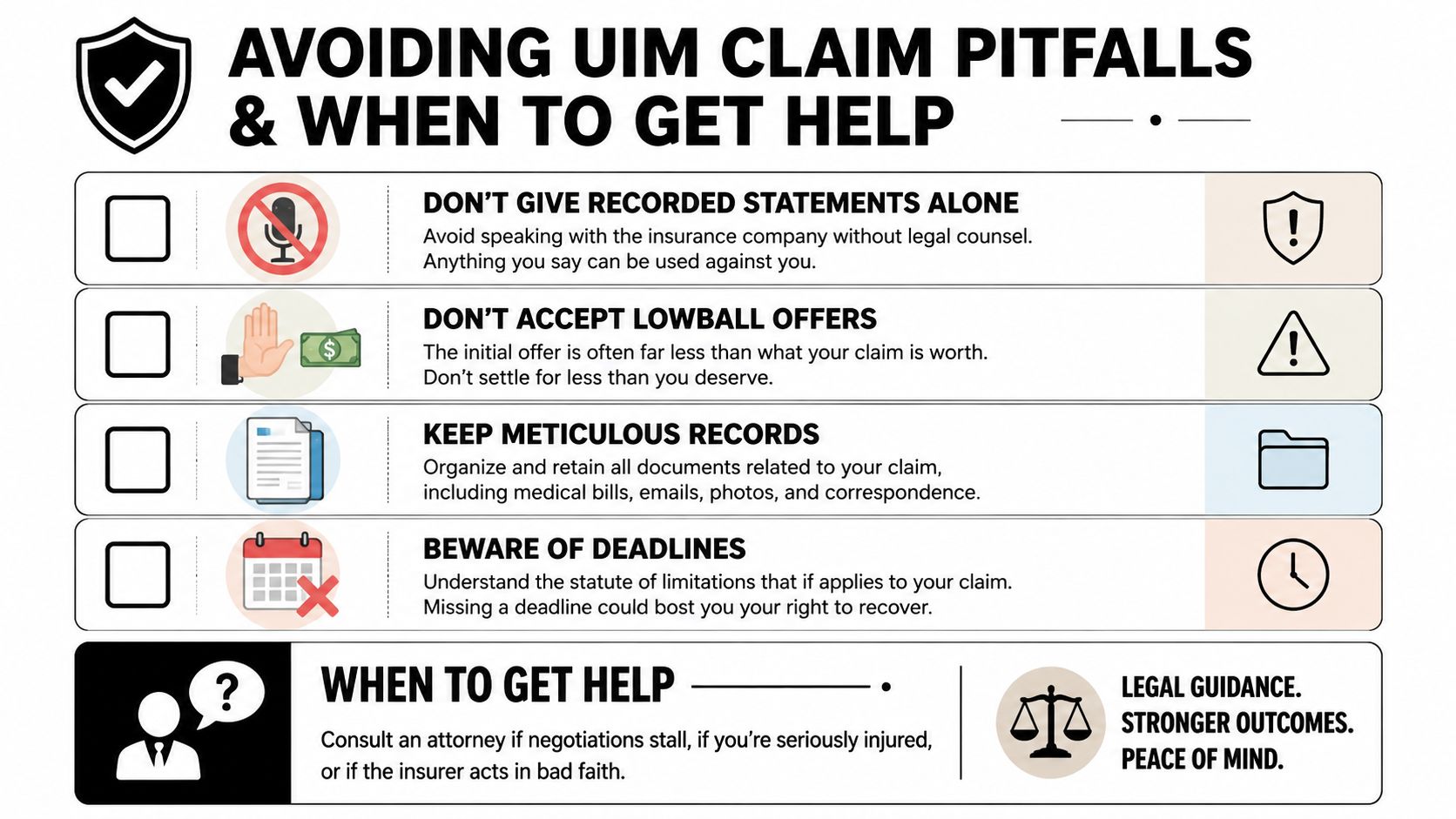

Common UIM Pitfalls and When to Get Help

Most bad outcomes in an underinsured motorist claim don't come from one dramatic mistake. They come from a series of small decisions that weaken the file. A rushed statement. An unreviewed release. An unsupported acceptance of the insurer's value.

The hard part is knowing which problem needs an appraiser and which problem needs an attorney.

Mistakes that cost people money

These are the issues I see most often in vehicle-loss cases:

- Accepting the first valuation because the report looks official. Many reports contain fixable errors.

- Failing to preserve evidence such as photos, receipts, listings, and service records that support pre-loss condition.

- Settling the liability claim without reviewing UIM conditions in your own policy.

- Treating property damage as secondary when the vehicle itself represents a major part of the total loss.

- Assuming the insurer will correct obvious mistakes on its own. Usually, it won't unless you document them clearly.

When an appraiser is the right professional

Bring in an independent appraiser when the core dispute is the amount of vehicle loss.

That usually means:

| Situation | Best fit |

|---|---|

| Total loss valuation seems low | Appraiser |

| Diminished value offer seems unsupported | Appraiser |

| Options, condition, or comparables are wrong | Appraiser |

| You need to invoke appraisal on property value | Appraiser |

An appraiser's job is to measure the loss, support it with market evidence, and challenge weak valuation methods.

When an attorney is the right professional

An attorney is usually the better fit when the dispute goes beyond valuation:

- Fault is contested and the carrier is denying legal responsibility.

- The insurer alleges policy breaches involving notice, consent, or coverage exclusions.

- You suffered serious bodily injury and the main dispute concerns medical causation or non-economic damages.

- Bad faith concerns appear because the insurer is stonewalling, misrepresenting coverage, or refusing to follow policy procedures.

Use the right expert for the right problem. A valuation dispute needs valuation evidence. A legal dispute needs legal strategy.

Some claims need both. That's common in larger losses. But people waste time and money when they hire only for one side of the problem and ignore the other.

Oregon and Washington UIM Claim FAQs

Drivers usually have the same practical questions once they realize the at-fault driver's insurance won't fully cover the loss. Here are the answers that matter most in Oregon and Washington.

Can I make an underinsured motorist claim if the other driver had insurance

Yes, if the other driver's policy was insufficient and your policy provides applicable UIM coverage. The key issue isn't whether the other driver had a policy. It's whether that policy fully covered the proven loss.

Do I have to settle with the at-fault insurer first

In many cases, yes. UIM commonly works only after the liability limits are paid and documented. Before you finalize that settlement, review your own policy for notice and consent requirements so you don't create a second problem while solving the first one.

What if my vehicle is a total loss and the insurer's value is too low

Challenge the valuation directly. Review the comparable vehicles, trim level, options, market area, and condition adjustments. If the policy includes appraisal and the dispute is about property value, appraisal may be the strongest route.

Can I bring a UIM claim for diminished value

It depends on your policy language and the way the claim is framed. The important point is that diminished value is a valuation question. If the carrier minimizes the loss by using weak market support, the file needs evidence, not just objections.

What if the at-fault insurer is delaying and won't confirm limits

Keep pressure on documentation. Ask for written confirmation of policy limits, liability position, and any tender decision. At the same time, notify your own insurer of a potential UIM claim so you're not accused of waiting too long.

Will a UIM claim raise my insurance rates

That depends on the policy, carrier, and claim history. People often assume any claim will automatically raise rates, but that's not always how it plays out, especially in a not-at-fault situation. The better move is to focus first on protecting the claim and getting the valuation right.

What if my UIM limits still aren't enough

Then the policy may not make you whole. UIM is a gap-filling tool, not an unlimited recovery source. When limits are tight, accurate valuation becomes even more important because every disputed dollar matters more.

Should I hire a lawyer for every UIM claim

No. If the dispute is mainly about what the vehicle was worth, an appraiser may be the more efficient first move. If the dispute involves fault, injury, coverage denial, or insurer misconduct, legal help makes more sense.

If you're in Oregon or Washington and your total loss or diminished value number doesn't match the actual market, Total Loss Northwest can help you challenge it with an independent appraisal. Their work focuses on the aspect of the underinsured motorist claim that is often overlooked, yet insurers seldom ignore: the actual value of the vehicle.