You get rear-ended. The other driver admits fault. Their insurance is active, so at first it sounds manageable.

Then the numbers start moving the wrong way. Your medical treatment keeps going. Your vehicle may be a total loss. If it's repaired, the resale value may still drop. The other driver's policy doesn't come close to covering all of it. That's the moment many people learn the hard way that “insured” doesn't mean “adequately insured.”

That's where underinsured motorist protection matters. If you're searching what is underinsured motorist protection, you're probably not looking for textbook language. You want to know whether your own policy can protect you when the at-fault driver's coverage runs out, and whether that protection helps with the car itself, not just injuries.

The Hidden Risk on the Road You Need to Know

Many drivers assume the primary danger is getting hit by someone with no insurance at all. That's only half the problem.

The more frustrating claim often involves a driver who did carry insurance, but only enough to satisfy a minimum requirement, not enough to cover a serious injury claim or a badly damaged vehicle. You can do everything right, get hit by someone else's mistake, and still end up fighting over unpaid losses.

A common post-accident problem

Here's the pattern I see most often. The liability insurer for the at-fault driver opens a claim, accepts responsibility, and starts talking settlement. Then the scope of damage becomes clear.

Your car might need major structural repair, or the carrier may declare it a total loss. At the same time, medical bills, missed work, and pain-related damages push past the other driver's limits. The claim doesn't collapse because the driver was uninsured. It collapses because their insurance was too small for the harm they caused.

Practical rule: The dangerous driver isn't always the one with no policy. It's often the one with a policy that runs out early.

That isn't a rare edge case. The Insurance Research Council reported that in 2023, 18.0% of drivers nationwide were underinsured, meaning more than one in six drivers could not fully cover injury costs after a crash. The same data showed 15.4% of drivers were uninsured, so about one out of every three drivers was either uninsured or underinsured in 2023, according to the Insurance Research Council's 2023 auto insurance findings.

Why this hits harder than people expect

The problem isn't just bodily injury. A severe crash creates multiple buckets of loss at once:

- Medical exposure that keeps growing while treatment continues

- Income disruption if you miss work or can't return right away

- Vehicle value disputes when the car is totaled or loses value after repair

- Use-related costs like transportation and rental issues, depending on coverage

When purchasing auto insurance, the focus isn't always on claim structure. The common expectation is, “If I get hit, insurance handles it.” Sometimes it doesn't. Sometimes it handles part of it, then stops.

That gap is exactly why underinsured motorist protection exists.

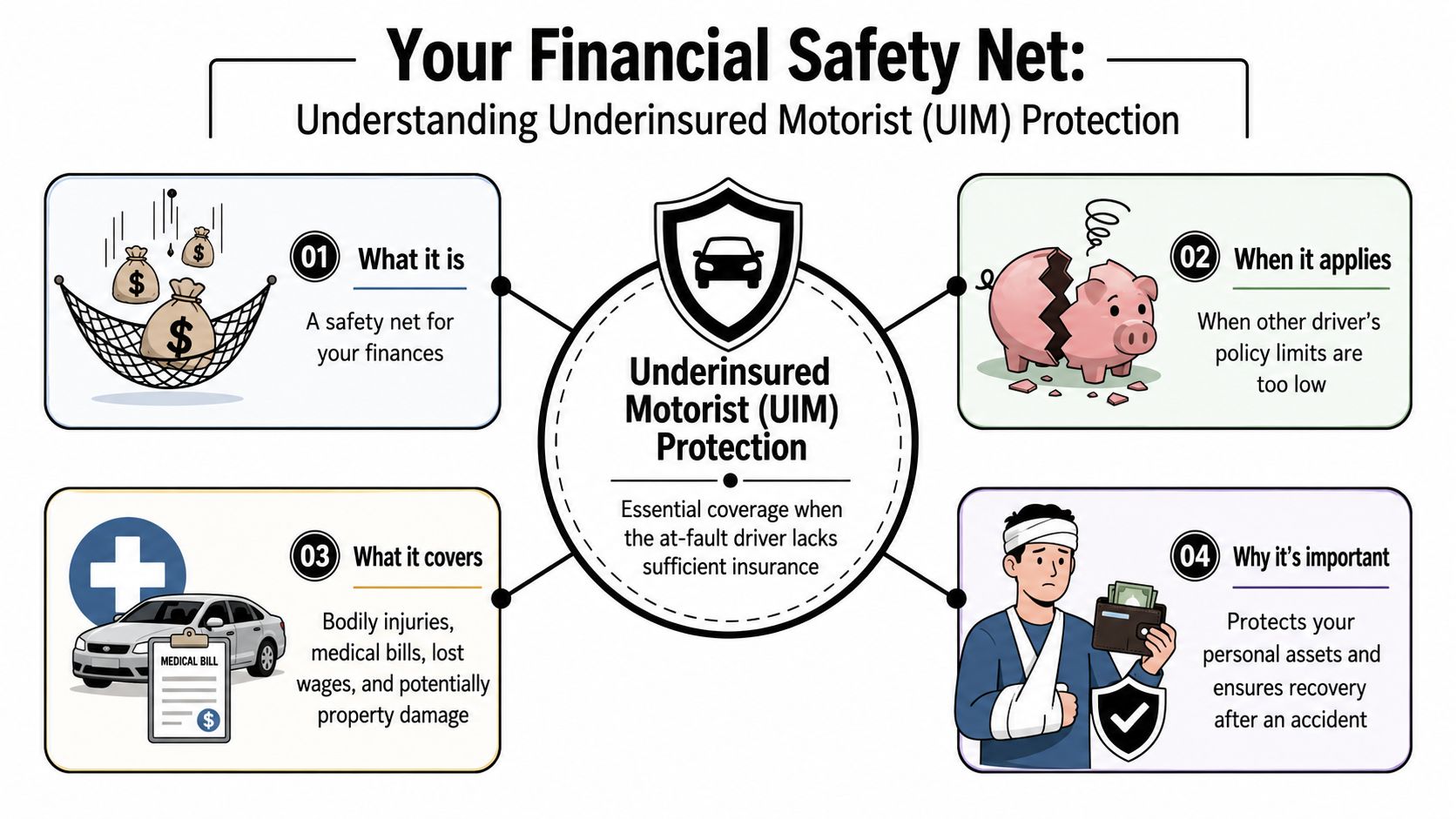

Understanding Underinsured Motorist Protection at Its Core

Underinsured motorist protection is your backup layer when the at-fault driver has insurance, but not enough of it.

The cleanest way to think about it is this. The other driver's liability coverage pays first. If that policy tops out before your damages are fully covered, your own underinsured motorist protection, often shortened to UIM, may step in to cover part of the remaining loss.

What UIM actually does

Illinois describes the core mechanics clearly. UIM is a secondary coverage layer triggered when the at-fault driver's liability limits are insufficient. It fills the gap between the other driver's available coverage and your total damages, including medical bills, lost wages, and pain and suffering, but only up to the UIM limit you selected. You must exhaust the at-fault driver's policy first, as explained by the Illinois Department of Insurance auto definitions page.

That last part matters. UIM doesn't replace the other driver's insurance. It doesn't skip ahead in line. It comes into play after the liability layer is used up.

Why people misunderstand it

Many policyholders think UIM means, “My insurer pays whatever the other insurer didn't.” That's too broad.

UIM is still limited by contract language, claim proof, and the limit you purchased. You still have to document your losses. You still have to prove the amount that remains unpaid. And your insurer is still going to evaluate the claim the same way an insurer evaluates any money-out file, carefully and often conservatively.

Your UIM claim is a first-party claim, but it still needs hard proof. Your insurer won't simply accept the shortfall because the other carrier exhausted its policy.

The practical version

When clients ask me what is underinsured motorist protection in plain English, I put it like this:

- The other driver pays first

- Your damages have to exceed that amount

- Your own policy may cover part of the unpaid remainder

- Your recovery stops at your policy limits and policy terms

If you understand those four points, you understand the foundation of UIM better than most policy summaries explain it.

UIM vs Uninsured Motorist Coverage A Critical Distinction

These coverages get lumped together all the time, and that causes real confusion in claims.

They are related, but they are not the same trigger. Uninsured motorist coverage applies when the at-fault driver has no insurance. Underinsured motorist coverage applies when the at-fault driver does have insurance, but not enough to fully cover the loss.

The side-by-side difference

Liberty Mutual explains the distinction this way: UM protects against drivers with no insurance, while UIM protects against those with insufficient insurance. Depending on the policy, this coverage can also respond in hit-and-run situations and may cover car repairs, rental costs, and even diminished value, though property damage coverage often has specific rules and may require the at-fault driver to be identified, as outlined in Liberty Mutual's guide to understanding uninsured and underinsured coverage.

Here's the quick comparison.

| Coverage Aspect | Uninsured Motorist (UM) | Underinsured Motorist (UIM) |

|---|---|---|

| Basic trigger | At-fault driver has no insurance | At-fault driver has insurance, but limits are too low |

| Typical claim setup | You turn to your own policy because there is no liability policy to collect from | You collect from the at-fault policy first, then pursue your own policy for the shortfall |

| Hit-and-run potential | May apply, depending on policy terms and claim facts | Sometimes connected to the same UM/UIM package, but the trigger is still inadequate insurance |

| Property damage issues | May include property damage coverage, often with extra rules | May include property-related protection, but it can be limited and state-specific |

| Main confusion point | People assume “uninsured” only means no card at the scene | People assume “insured” means there will be enough money available |

Where drivers get tripped up

The trouble starts when someone says, “I have full coverage,” but they don't know whether that includes UM, UIM, property damage features, or the conditions attached to them.

If you want a more focused explanation of the no-insurance side of the issue, this guide on what uninsured motorist coverage is helps separate the two.

For vehicle owners, the property damage piece deserves special attention. A policy may treat bodily injury and vehicle damage very differently. That's one reason a car owner can have a valid injury claim path and still face a fight over total loss value or diminished value.

How UIM Claims Actually Work Limits Stacking and Setoffs

Most policy language makes UIM sound simple. Real claims are not simple.

The headline problem is this. Having UIM does not automatically mean your insurer writes a check for the entire unpaid balance after the at-fault driver's insurer tenders limits. The actual payout depends on policy wording and state law.

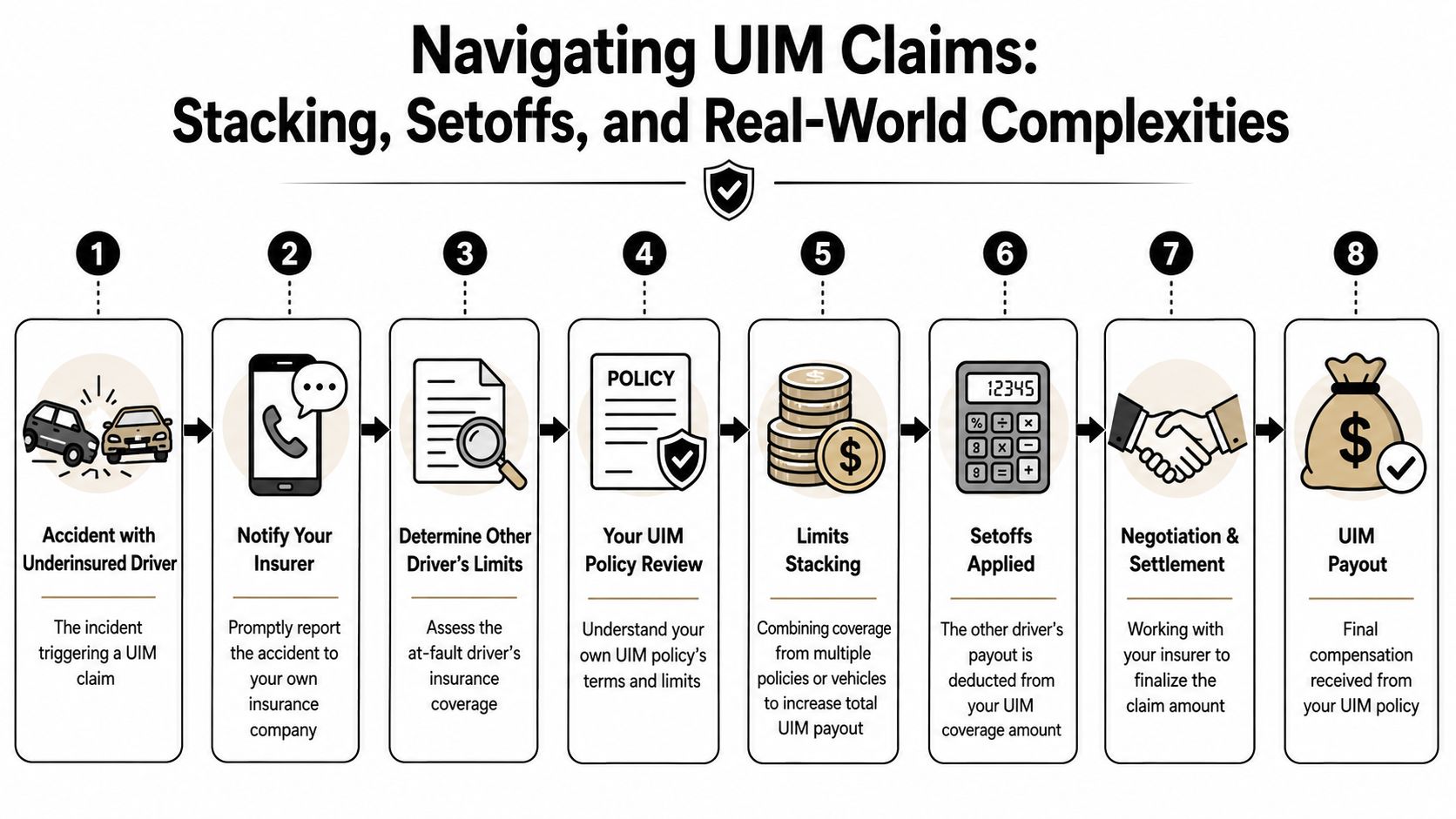

Here's a visual breakdown of how the process usually unfolds.

The two words that change payouts

State Farm notes a common misconception directly. UIM doesn't automatically fill the entire gap between your damages and the at-fault driver's limit. The actual payout depends on state laws regarding offsets and whether your policy allows stacking of multiple UIM coverages, as discussed in State Farm's overview of uninsured and underinsured coverage options.

Those two terms matter:

- Setoffs or offsets mean the at-fault driver's payment may reduce what's available under your UIM claim, depending on how the law and policy apply the credit.

- Stacking refers to combining available UIM coverages from more than one vehicle or policy when the law and policy permit it.

A lot of disappointment in UIM claims comes from not understanding those rules upfront.

What the process looks like in practice

A UIM claim usually moves through these stages:

Liability claim first

The at-fault driver's insurer investigates and eventually tenders its available policy limits if the damages justify it.Notice to your own carrier

Your insurer should be notified early that a UIM claim may be coming. Waiting too long can create avoidable disputes.Proof of exhaustion

Your insurer typically wants confirmation that the at-fault policy has been fully used.Damage proof

You still have to document medical losses, wage losses, pain-related damages, and any vehicle-related loss that fits the policy.

A short explainer can help if you want a visual walk-through of that claim sequence.

What works and what doesn't

What works:

- Early policy review so you know the UIM limits, endorsements, and restrictions

- Written documentation from the liability carrier showing its limits were tendered

- Organized proof of damages instead of rough estimates or verbal summaries

- Careful release handling so you don't accidentally impair your own claim rights

What doesn't work:

- Assuming your insurer will calculate the claim for you

- Treating bodily injury and vehicle damage as one blended loss without support

- Accepting vague statements about offsets without reading the policy and applicable law

- Thinking the first UIM offer reflects the full contractual value

The biggest mistake in a UIM claim is assuming the hard part ended when the at-fault carrier paid its limits. Often that's when the technical fight begins.

Your Step-by-Step Guide to Filing a UIM Claim

Once it's clear the at-fault driver's insurance won't cover the full loss, you need to build your UIM claim deliberately. Sloppy files get delayed. Thin files get discounted.

The claim file you want to build

Start with notice. Tell your own insurer that the crash may involve an underinsured motorist claim. Don't wait until the liability carrier is done if you already see that the losses are outpacing the available coverage.

Then collect the proof that matters most.

Liability limits evidence

Get written confirmation of the at-fault driver's coverage and, when the time comes, proof that the limits were tendered or exhausted.Medical documentation

Keep records of treatment, bills, diagnosis notes, and any care recommendations that show the scope and duration of injury.Wage loss support

If you missed work, gather payroll records, employer verification, and any documentation that ties the time away from work to the crash.Vehicle loss documentation

Save repair estimates, photos, valuation reports, total loss paperwork, and comparable market data if value becomes disputed.

The order matters

A strong UIM claim usually follows a clear sequence.

First, preserve all evidence from the crash itself. That includes scene photos, vehicle photos, police report information, witness details, and every communication from either insurer.

Second, track losses as they develop. Injury claims change over time, and vehicle valuation disputes often get more technical after the first estimate or total loss offer.

Third, review your own policy before signing anything. Some people settle the liability claim without understanding how that release, notice requirement, or consent issue can affect their UIM rights.

If a document affects your ability to recover under your own policy, don't sign it just because the other carrier says it's routine.

A practical checklist

Use this as your baseline checklist:

- Open the UIM claim early with your own carrier

- Request the full policy language for your UM/UIM coverage, not just the declarations page

- Document every category of loss separately, especially injury and vehicle value

- Keep all insurer communications in writing whenever possible

- Verify deadlines and consent requirements before resolving the third-party claim

- Push for complete valuation support if your car is a total loss or has post-repair value loss

The better your documentation, the less room the insurer has to treat your claim like a guess.

Key UIM Rules for Drivers in Oregon and Washington

Oregon and Washington drivers need to pay attention to local claim mechanics, especially where injury coverage and vehicle valuation start interacting.

I'm not going to oversell state-specific magic here. UIM claims are still contract-driven. But the practical handling environment can feel different depending on where the claim lands and what the policy says.

Oregon drivers need to watch how coverages interact

In Oregon, drivers often have multiple moving pieces in the same file. Injury-related benefits may flow through one part of the policy while UIM issues develop through another. That means timing and documentation matter more than people expect.

The practical problem is overlap. If you don't understand how your medical payments, injury proof, and final uncompensated damages line up, your UIM claim can get reduced or delayed while the carrier sorts out credits, offsets, and what it believes has already been paid elsewhere.

For vehicle owners, Oregon claims can also turn into valuation disputes quickly when the car is near total loss territory. Once that happens, you need to stop looking only at repair cost and start looking at market value evidence.

Washington drivers should read the policy language carefully

Washington drivers often hear that stacking can be more favorable there. Sometimes that's true. Sometimes the policy language still controls the fight. What matters is whether the available coverages can be combined under the policy and governing law.

That's why broad assumptions are dangerous. A driver may think multiple insured vehicles automatically mean more UIM money is available. Sometimes yes. Sometimes no. The answer sits in the contract and the claim facts, not in a casual summary from an adjuster.

Where state rules meet vehicle value fights

This is the part many articles skip. Even when the injury side gets most of the attention, your vehicle may represent a major unresolved loss. If your car is pushed into functional or market-value total loss territory, you need to understand that valuation process on its own terms.

For a closer look at when a damaged vehicle may qualify as a loss worth challenging, this explanation of constructive total loss is useful.

The key takeaway for Oregon and Washington drivers is simple:

- Read the policy, not the marketing summary

- Separate injury proof from vehicle valuation proof

- Don't assume a local rule helps you unless it clearly applies to your policy

- Treat total loss and diminished value disputes as their own battleground

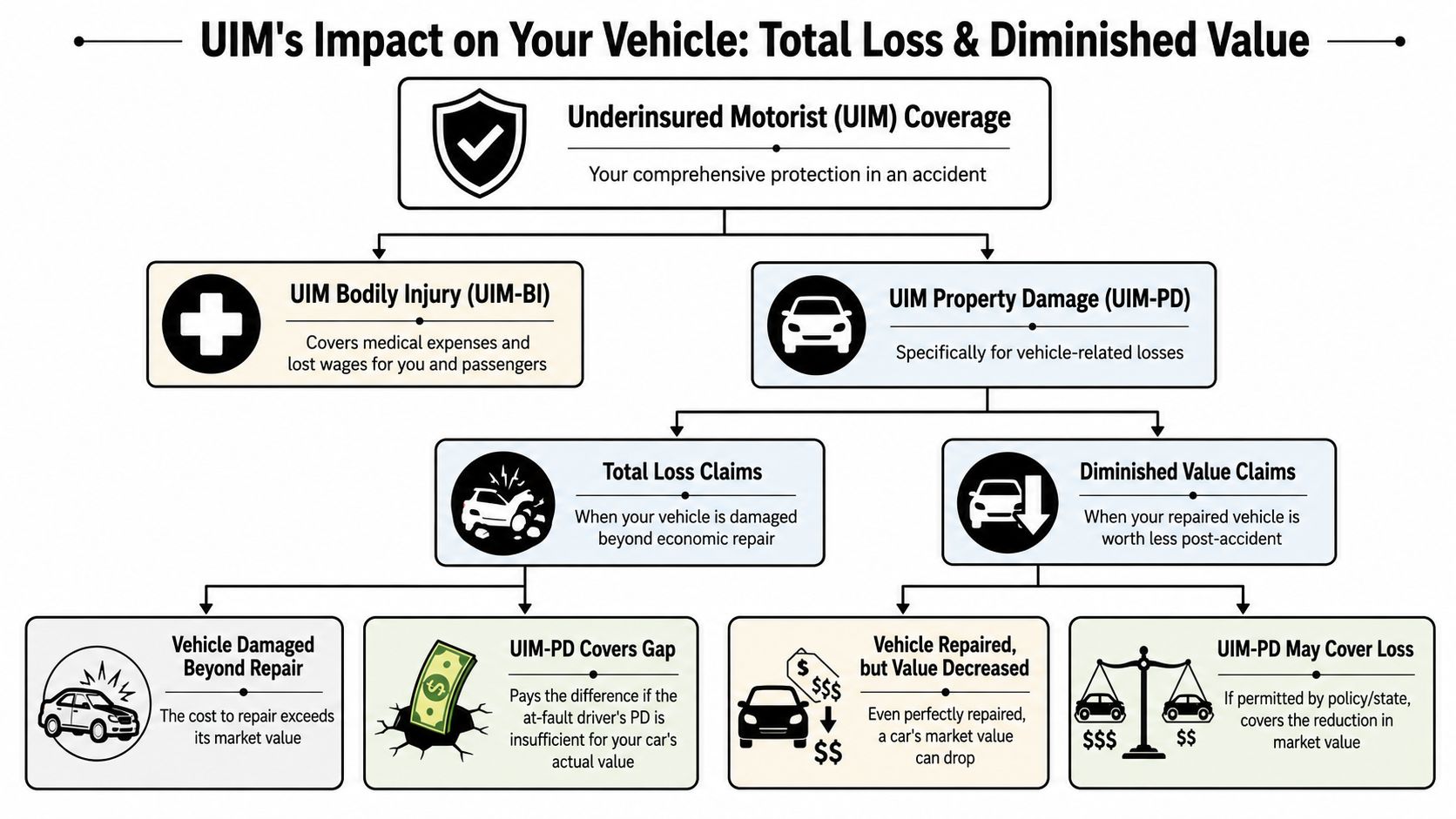

UIM's Role in Total Loss and Diminished Value Claims

The conversation now gets real for vehicle owners.

Most explanations of what is underinsured motorist protection focus on injuries. That matters, but it leaves out the part many drivers care about just as much. What happens if your car is totaled, or repaired badly enough from a market standpoint that it's worth less afterward?

UIM and vehicle value are not the same thing as a repair bill

Texas consumer guidance points to a gap many owners discover late. Some UM/UIM property damage coverage exists, but it is often limited and may not adequately address disputes over total loss valuations or diminished value, especially for newer, high-value, or classic cars. In those situations, an independent appraisal becomes critical because it provides a defensible, market-based valuation to counter a low initial offer, as noted by the Texas Department of Insurance on uninsured motorist coverage.

That matches what happens in real files. An insurer may acknowledge coverage, then undervalue the car.

Those are separate issues:

- one is whether coverage exists

- the other is how much the vehicle loss is worth

Carriers often handle the second issue with valuation systems, condition adjustments, and comparable selections that deserve close review. If the vehicle is uncommon, highly optioned, especially clean, modified, collectible, or hard to match in the local market, the first offer may not reflect actual market value.

Total loss and diminished value are different fights

A total loss dispute asks whether the settlement reflects the vehicle's real pre-loss market value.

A diminished value dispute asks how much resale value the vehicle lost after proper repair because the accident history now follows it.

Those aren't fringe issues. They can be the main financial dispute in the claim, especially when the bodily injury side is modest but the vehicle is valuable. If your car has lingering market stigma after repair, or if the total loss valuation is built on weak comparables, you need evidence that goes beyond the insurer's worksheet.

If you're dealing specifically with post-repair market stigma, this guide to automobile diminished value gives useful background on the issue.

Why independent appraisal changes the leverage

An independent appraisal does something the average owner can't do alone. It turns “I think your offer is low” into a documented market position.

That matters because valuation disputes are won with support, not frustration. A serious appraisal can analyze vehicle condition, trim, options, market comps, pre-loss status, and the actual resale impact of damage history. It gives you something concrete to put against the carrier's number.

When the dispute is about vehicle value, the strongest move is usually not arguing harder. It's bringing better valuation evidence.

If your UIM-related vehicle claim involves a total loss offer, a diminished value loss, or a weak market valuation, independent appraisal is often the most effective tool on the table.

If you're in Oregon or Washington and you're being lowballed on a total loss or diminished value claim after a crash, Total Loss Northwest focuses on the part of the insurance fight most drivers aren't equipped to handle alone. They provide certified independent appraisals, invoke the Appraisal Clause, and build market-based valuation reports that can stand up in negotiation when the insurer's number doesn't match your vehicle's real value.