Don't accept that lowball offer. The first settlement number on an auto claim is often a starting position, not a finished valuation. If your vehicle was declared a total loss, or the repair path leaves you arguing over value, you're not stuck with whatever the adjuster says the car is worth.

A lot of drivers enter an insuance car dispute at the worst possible moment. You're dealing with a wrecked vehicle, missed work, rental problems, and an insurer that talks like the file is already decided. Meanwhile, the valuation may be built on weak comparable vehicles, missing options, wrong condition assumptions, or a market search that doesn't reflect your area.

That matters because auto claims are big business and heavily contested. Private auto insurers in the U.S. lost nearly $170 billion in 2021, with 57% tied to liability claims and 43% tied to physical damage claims, according to auto insurance loss and claims data. When that much money is moving through the system, you should expect the carrier to protect its position.

The good news is that policy language, independent appraisals, and regulator complaint channels give you an advantage if you know how to use them. Below are seven practical ways to force a fairer number and stop letting the claim happen to you.

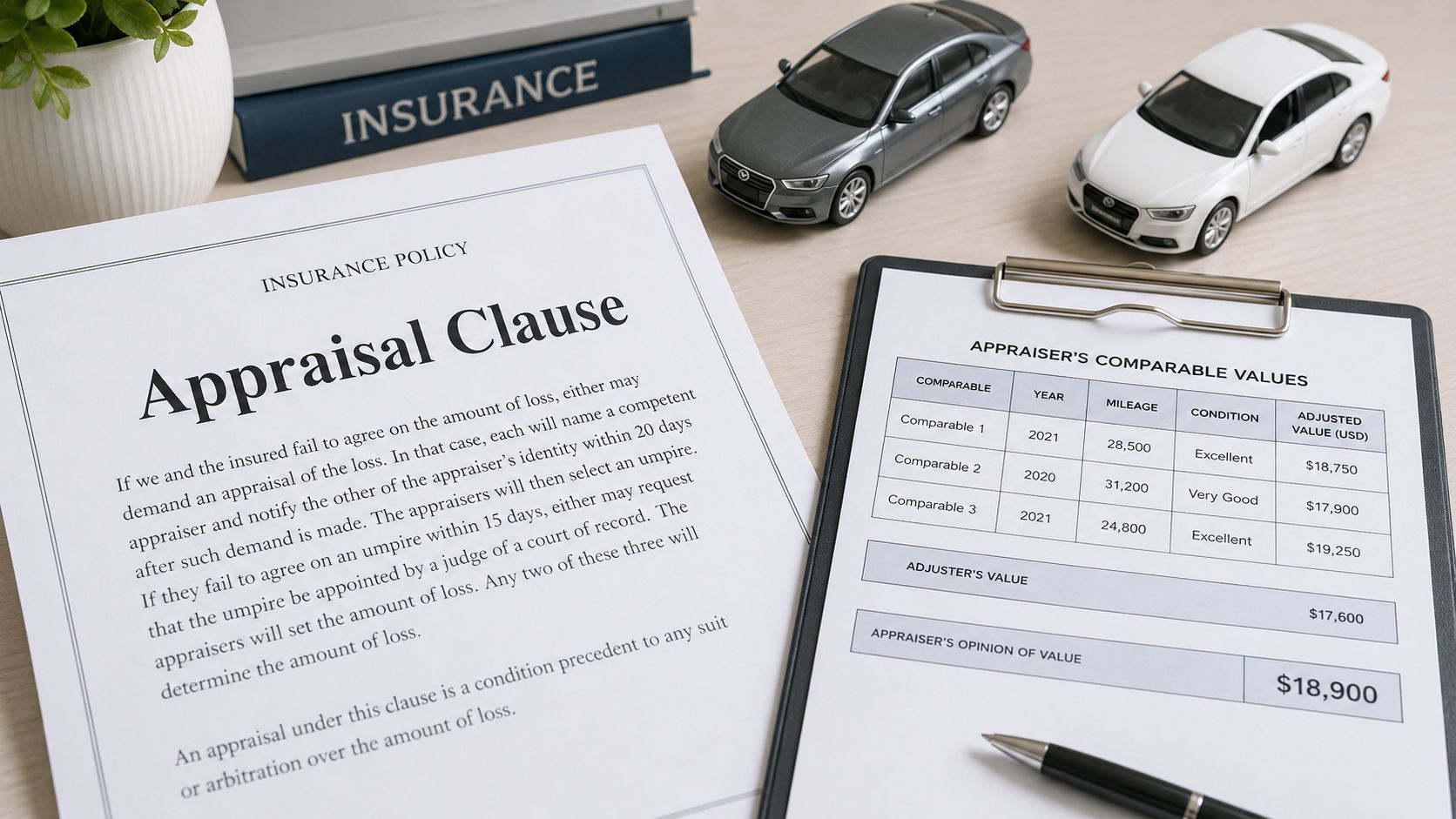

1. Invoke the Appraisal Clause to Challenge Insurer Valuations

The most useful part of the policy is often overlooked. That's the appraisal clause.

If your fight is over value, not coverage, this clause can move the dispute out of the insurer's normal valuation loop. Instead of arguing forever with an adjuster who keeps repeating the same number, you trigger a formal process that puts independent appraisers in play.

Texas specifically notes that appraisal applies to amount-of-damage disputes, not coverage disputes, in its auto insurance complaint guidance. That's a critical distinction. If the carrier says the policy doesn't cover the loss at all, appraisal usually won't fix that. If the carrier agrees the claim is covered but undervalues the vehicle, appraisal can be the right pressure point.

What this changes in practice

An appraisal clause is most effective when the insurer has valued your vehicle like a generic example of its model. That's where owners of rare trims, luxury packages, collector vehicles, and modified trucks get hurt. The software may grab "similar" vehicles that aren't similar.

I've seen disputes turn on basic misses like these:

- Wrong trim level: The report treats a higher trim as a base model.

- Missing options: Factory packages, tow equipment, upgraded audio, or driver-assist features aren't reflected.

- Bad comparables: The insurer uses vehicles from weaker markets or with materially different mileage and condition.

- Condition flattening: A very clean, documented vehicle gets treated like an average used car.

Practical rule: If the fight is about "what it's worth," read the appraisal clause before you argue with the adjuster for another week.

A focused total loss appraisal service can help you decide whether the policy language and facts support that move. The key is speed. Invoke the clause in writing, ask for the insurer's full valuation report, and make them show the comparable set and adjustments they relied on.

2. Obtain an Independent Professional Appraisal Before Accepting Settlement

Never negotiate blind. If you don't have your own value opinion, you're just reacting to theirs.

An independent professional appraisal gives you a documented counter-position. That's different from telling the adjuster you found a few listings online. A proper appraisal addresses the vehicle itself, the local market, the condition, the equipment, and the flaws in the insurer's report.

Why this matters before you sign anything

In major U.S. auto-insurance markets, the average 2024 property damage liability claim was $6,770, while the average bodily injury liability claim was $28,278, and claim frequency was 2.50% for property damage liability versus 0.80% for bodily injury liability, according to Insurance Information Institute auto insurance facts. That gap helps explain why carriers are often conservative on vehicle valuation. Property damage claims are common, and insurers don't want to overpay across a large volume of files.

That doesn't mean your number is fair. It means you should expect resistance.

What a usable appraisal should include

A good appraiser doesn't just state a value. The report should show how they got there and why the insurer's number doesn't hold up.

- Vehicle-specific inspection: VIN, trim, options, mileage, pre-loss condition, prior damage, and maintenance history.

- Comparable market analysis: Similar vehicles from the right region, not random listings from a different market.

- Adjustment logic: Clear reasoning for mileage, equipment, package, and condition differences.

- Rebuttal points: Direct response to errors in the carrier's valuation report.

If your car is unusual, the appraiser's background matters. A daily driver, a modified diesel truck, and a collector Mercedes don't belong in the same valuation bucket.

Use an independent car appraiser before you accept the settlement, not after. Once you sign a release and cash out the claim, your bargaining power usually weakens considerably. At that point, you may still have options, but you've made the fight tougher than it needed to be.

3. Document and Compile Comprehensive Evidence Before Negotiations

The strongest disputes are built before the first demand letter goes out. Documentation wins because it forces the insurer to answer facts instead of brushing off opinions.

Start with the paper trail and the photo trail. Then organize it so someone outside the claim, including an appraiser, supervisor, mediator, or regulator, can understand the file in minutes.

What to gather before you push back

You don't need fancy software. A clean folder structure and a dated timeline are enough.

- Pre-loss photos: Exterior, interior, odometer, wheels, seats, dash, bed, cargo area, engine bay.

- Service history: Dealer records, independent shop invoices, recent maintenance, major replacements.

- Upgrade proof: Receipts and installation records for wheels, tires, suspension, audio, lighting, towing gear, or factory add-ons.

- Valuation package: The insurer's report, comparable listings, and notes showing why a comp is not comparable.

- Communication log: Dates, names, phone calls, emails, text messages, and each settlement number discussed.

A lot of claims stall because the owner has the right facts but no presentation. Build a simple timeline. Accident date. Inspection date. First offer. Your objection. Documents sent. Follow-up requests. Silence from the carrier. That timeline becomes a key advantage if the claim drags.

Keep every version of the insurer's valuation report. Small changes between drafts can tell you exactly where the dispute is.

One more point. Don't mix repair disputes and valuation disputes unless you have to. If your argument is total loss value, stay on value. If your argument is poor repair handling, separate those documents so your file stays clean.

If part of your claim involves glass or related repair issues, this windshield claim process explained guide can help you keep that piece organized without muddying the valuation fight.

A quick visual overview can also help if you're trying to explain the claim to a family member or advisor before you respond to the adjuster:

4. Understand Total Loss Thresholds and State-Specific Regulations

State rules determine influence. A lot of drivers miss that and argue fairness in general terms when they should be pressing on rule compliance.

If your vehicle is labeled a total loss, your next move depends partly on your state's framework. Some states are more explicit about valuation practices, disclosures, complaints, and what counts as an amount-of-loss dispute. Others leave more room for insurer process.

Why state law changes the pressure

Most motor vehicle lawsuits are filed in state courts, and the combined excess value of motor vehicle tort filings in federal and state courts from 2014 to 2023 reached about $42.8 billion, according to an Insurance Research Council litigation brief. That tells you two things. First, claim disputes are not rare. Second, state-level rules and practices matter because that's where most of the legal friction lives.

For a total loss owner, that means you need to stop speaking in broad complaints and start asking targeted questions:

- Was the valuation method allowed in my state?

- Did the insurer disclose the comparable vehicles and adjustments?

- Does my state offer mediation, complaint review, or another neutral process?

- Is my dispute about coverage, amount of loss, repairability, or claim handling delay?

Use your state as a negotiation tool

A weak insurer valuation often collapses when you ask for the right records in writing. If the report doesn't reflect your trim, region, mileage normalization, or equipment, make the carrier explain each one.

For drivers in the Pacific Northwest or anywhere else trying to understand salvage and total-loss rules, a state-by-state total loss threshold guide is a useful starting point. Then verify the details with your own state's insurance department, because the exact rules and terminology can differ.

The fastest way to strengthen a dispute is to quote the policy and the state rule in the same email.

That's what changes the conversation from "I don't like your number" to "Explain why your process complies with the policy and the rules that apply to this claim."

5. Engage Professional Claim Consultants or Insurance Attorneys

Some disputes are too small for formal help. Others are expensive enough that handling them alone stops making sense.

The trick is knowing the difference. If the disagreement is minor, a strong appraisal package may do the job. If the carrier is denying obvious evidence, hiding the file behind supervisors, or turning a simple valuation issue into a long paper chase, outside help can change the pace fast.

When professional help is worth it

A consultant or attorney is most useful when the dispute has one of these features:

- Policy language fight: The insurer is leaning on technical wording you don't fully understand.

- Bad process: Repeated delays, inconsistent explanations, or missing written responses.

- High-value vehicle: Luxury, collector, specialty, or heavily modified units need specialized valuation support.

- Liability overlap: The file includes both vehicle value and injury exposure, which changes settlement posture.

J.D. Power's 2025 U.S. Auto Insurance Study reported that 38% of customers were in a marketplace where they had to work harder to get the service they wanted, and LexisNexis described increased shopping activity and growing vehicle-mix complexity in its 2026 trends report, as noted in this auto insurance trends report summary. In plain English, claims and service are not getting simpler for drivers. More complexity means more room for poor communication and weak valuations.

Choose the right kind of professional

Not every lawyer understands vehicle valuation, and not every appraiser handles policy disputes well. Match the professional to the problem.

- Independent appraiser: Best when value is the main issue.

- Claim consultant: Useful when the file is disorganized and you need strategy and presentation.

- Insurance attorney: Best when the carrier may be breaching the policy, mishandling the claim, or exposing itself to extra-contractual risk.

If you hire help, ask one direct question first. "What exactly are you going to do that I can't do myself?" A good professional will answer clearly. They won't hide behind jargon.

6. File Formal Complaints with State Insurance Commissioner

A complaint is not magic. It is pressure.

Used correctly, it forces the insurer to answer in writing through a channel it can't ignore as easily as a policyholder email. That's especially useful when your claim isn't flatly denied but keeps getting dragged through delay, partial responses, and repeated document requests.

When a complaint makes sense

File after you've already tried to resolve the dispute directly and have the record to prove it. That means you should have the valuation report, your objections, your supporting documents, and a communication timeline.

California's consumer guidance highlights auto mediation as a neutral resolution path, and Texas also points consumers to complaint processes and escalation routes in claim disputes. Those channels matter because many claim problems today look like friction, not formal denials, and California's auto mediation guidance shows that neutral options are available when communication breaks down.

What to put in the complaint

Don't rant. Regulators respond better to organized facts than emotional summaries.

- Claim identifier: Policy number, claim number, date of loss, carrier name.

- Dispute summary: One paragraph stating whether this is a value dispute, delay issue, or communication failure.

- Specific conduct: Missing comparables, unexplained adjustments, unanswered emails, repeated requests for the same records.

- Supporting records: Valuation report, your independent evidence, timeline, and key correspondence.

- Requested action: Ask for a written explanation, disclosure of valuation support, or review of handling conduct.

A complaint is strongest when you can show the insurer had the information, had time to respond, and still didn't address the actual issue.

Don't use the complaint as your first move. Use it when the insurer has shown you that normal requests won't get the file moving. Then keep negotiating while the complaint is pending. A regulator file and a clean appraisal package work well together.

7. Request Insurer Appraisal Under Policy's Appraisal Clause With Certified Appraiser Partnership

The insurer names its appraiser. You name yours. That choice can swing thousands of dollars.

A lot of policyholders invoke the appraisal clause and then treat the rest of the process like a formality. That is a mistake. Appraisal is a structured value fight governed by the policy, and the stronger appraiser usually wins because the stronger appraiser brings better support, cleaner comparables, and a report that can hold up if the matter goes to an umpire.

Choose the appraiser before deadlines start closing in. If the vehicle is a basic daily driver, a competent total loss appraiser may be enough. If it is a performance trim, collector car, restored classic, diesel truck, modified off-road build, or a luxury SUV with expensive factory packages, hire someone who works in that segment and knows how those vehicles trade in your market.

That specialization matters because insurers often use broad valuation systems that flatten the details. A base model and a high-option example can get treated as near twins. They are not near twins in the actual market.

What your appraiser needs to prove

A certified appraiser working with you should be ready to challenge the insurer's file point by point, not just announce a higher number.

- Bad comparables: Wrong trim, wrong drivetrain, missing packages, salvage history, poor condition, or listings from the wrong market area.

- Weak adjustments: Mileage or condition adjustments that are arbitrary, inconsistent, or unsupported by local market reality.

- Missed equipment: Factory options, recent tire sets, upgraded towing packages, premium audio, ADAS packages, or specialty accessories omitted from the valuation.

- Condition evidence: Photos, maintenance history, detailing records, and repair invoices that support above-average condition before the loss.

- Category-specific value: Collector interest, limited-production status, documented restoration work, or modifications that add market value rather than personal sentimental value.

In appraisal, opinions do not carry much weight by themselves. Support does.

Stay involved with the report. Read it before it is submitted. Check the VIN details, trim level, mileage, options, title history, and every comparable unit. I have seen cases weakened by simple errors such as the wrong drivetrain, missing package codes, or a comparable from a market two states away. Those mistakes are fixable early and expensive later.

If the two appraisers cannot agree, the dispute usually goes to an umpire under the policy terms. At that point, the file in front of the umpire matters more than how strongly anyone complains. A certified appraiser partnership gives you a real seat at the table and turns the appraisal clause from a line in the policy into a tool you can use.

7-Point Car Insurance Dispute Comparison

| Strategy | Complexity 🔄 | Resources & Effort ⚡ | Expected Outcome ⭐📊 | Ideal Use Cases / Tips 💡 |

|---|---|---|---|---|

| Invoke the Appraisal Clause to Challenge Insurer Valuations | 🔄 Moderate, formal written invocation and coordination with appraisers | ⚡ Moderate, appraisal costs (often split) and additional time | ⭐📊 High, binding neutral valuation; often yields substantially higher settlements for total loss/diminished value | 💡 Best for total loss, diminished value, high‑value/collector/modified vehicles; read policy clause and document vehicle |

| Obtain an Independent Professional Appraisal Before Accepting Settlement | 🔄 Low–Moderate, hire certified appraiser and supply documentation | ⚡ Moderate, appraisal fee and scheduling time (often recouped) | ⭐📊 High, credible third‑party valuation; commonly increases settlement 15–40% | 💡 Use when insurer offer seems low; choose ASA/AAA appraiser and provide full records |

| Document and Compile Comprehensive Evidence Before Negotiations | 🔄 Moderate, time‑intensive organization but straightforward process | ⚡ Low–Moderate, mainly time and digital tools to gather photos, receipts, comparables | ⭐📊 Moderate–High, strengthens negotiations and improves appraisal accuracy | 💡 Essential for all disputes; maintain pre‑accident photos, maintenance records, receipts and 3–5 comparable listings |

| Understand Total Loss Thresholds and State‑Specific Regulations | 🔄 Moderate, requires research into state laws and insurer obligations | ⚡ Low–Moderate, research time or contact insurance commissioner | ⭐📊 Moderate, reveals insurer compliance obligations and potential legal leverage | 💡 Critical when state rules affect valuation/diminished value; check state commissioner and NAIC resources |

| Engage Professional Claim Consultants or Insurance Attorneys | 🔄 High, legal strategy, negotiation, possible litigation | ⚡ High, contingency fees or retainers, plus time; access to experts and databases | ⭐📊 Very High, can substantially increase recovery and pursue bad‑faith damages | 💡 Use for large or complex disputes; confirm contingency rates and attorney experience in total‑loss claims |

| File Formal Complaints with State Insurance Commissioner | 🔄 Low–Moderate, formal complaint process and follow‑up | ⚡ Low, free to file but requires thorough documentation and time | ⭐📊 Moderate, regulatory pressure often prompts insurer action but won't guarantee a specific settlement amount | 💡 File after documenting dispute in writing; include valuation differences, timelines and policy citations |

| Request Insurer Appraisal Under Policy's Appraisal Clause With Certified Appraiser Partnership | 🔄 Moderate–High, formal clause invocation plus coordinated certified appraiser and possible umpire | ⚡ Moderate, appraisal fees, coordination and scheduling time | ⭐📊 Very High, binding, expert‑backed valuation; particularly effective for specialty vehicles | 💡 Invoke in writing immediately; select certified specialist, provide full documentation, participate in umpire selection |

Take Control of Your Settlement

An insuance car dispute feels personal because it is personal. The insurer sees a claim file. You see a vehicle you maintained, paid for, relied on, and now have to replace. If the valuation is wrong, the financial hit lands on you, not on the software that produced the number.

The fix is method, not outrage. Start with the policy. Find the appraisal clause. Get the insurer's full valuation report. Then compare every line of that report against your vehicle's actual trim, options, mileage, condition, and local market. Most weak offers start falling apart at that stage.

Next, build evidence that another person can verify. Service records. Photos. upgrade receipts. Comparable listings. A claim timeline. Written objections that point to specific errors. That's what turns a frustrated owner into a credible claimant. It also gives an independent appraiser, consultant, attorney, mediator, or regulator something useful to work with.

If the carrier still won't move, escalate in the right order. Independent appraisal first when the issue is value. Appraisal clause invocation when the policy supports it. State complaint when the claim handling breaks down. Legal help when the dispute grows beyond a straightforward amount-of-loss fight.

The larger claim environment explains why this matters. Auto insurance isn't a low-friction system, and disputes over valuation, liability, and process are part of a much bigger claims machine. But none of that means you have to accept a bad number. It means you need a structured response that uses the same language the insurer uses. Policy terms, written evidence, market support, and procedural strength.

If you need outside help, Total Loss Northwest is one relevant option for drivers dealing with low total-loss or diminished-value offers, particularly in Oregon and Washington. The key is to act before you sign away your bargaining power. Review the policy, gather your records, and challenge the number while the file is still open. That's when you have the best chance to force fair value.

If you're dealing with a low total-loss offer or a disputed vehicle valuation, Total Loss Northwest can review the claim and help you understand whether an independent appraisal or appraisal clause strategy fits your situation.