You walk away from the crash thinking, “At least everyone's okay.” Then the paperwork starts. The adjuster sounds polite. The estimate arrives fast. And the number on that first offer doesn't come close to what you've lost.

That's where most drivers get trapped. They assume the insurer's number is the number. It isn't. It's an opening position based on the insurer's process, the insurer's software, and the insurer's version of your facts.

I'm going to be blunt. If you've been offered a low total loss payment, a weak repair valuation, or a settlement that ignores how much your car dropped in resale value, you need to stop reacting and start building your case. The same goes for injury claims. Car accident settlement value isn't a magic number. It's a range shaped by evidence, documentation, and how hard you push back.

For property damage disputes, that means learning how to challenge valuation reports, how to document local market value, and when to force the issue through an independent appraisal. If you need a practical primer on how to negotiate your property damage claim, that resource is worth reviewing before you answer the adjuster again.

The First Offer Is Just the Beginning

A lot of people open the adjuster's email and feel two things at once. Relief that the claim is moving, and anger that the number is low.

That reaction is usually justified. The first offer often reflects what the insurer can defend with its internal tools, not what your claim is worth in the marketplace. If your car was exceptionally clean, had recent work, rare trim, upgrades, or unusually strong local demand, canned valuation software can miss that. If your injuries are real but your records are incomplete, the offer can miss that too.

You are not obligated to accept a weak valuation just because it arrived on official letterhead.

The right mindset is simple. A settlement offer is a proposal, not a verdict. Your job is to test it, challenge it, and replace bad assumptions with better evidence.

That matters even more in Oregon and Washington, where drivers often have options they never use. One of the biggest is the Appraisal Clause in the policy. It is often not invoked because no one explains it early enough. But if you're fighting over total loss value or diminished value, it can shift the dispute away from the insurer's software and toward actual appraisals.

What most people get wrong

Drivers usually make one of these mistakes:

- Accepting speed over accuracy: They want the claim finished and sign off before reviewing the valuation report.

- Arguing feelings instead of evidence: “My car was worth more” won't move the file. Comparable sales, condition evidence, and corrected options data will.

- Ignoring the property side while focusing on the injury side: If both are in play, each part needs its own documentation.

- Letting the insurer define the playing field: Once you do that, you're negotiating inside their system instead of forcing a better one.

If the offer feels low, treat that feeling as a signal. Then go get proof.

What Does Settlement Value Really Mean

Think of a car accident claim like a two-part build. One part is the car. The other part is the person. Add them together, and you get the full car accident settlement value.

Property damage

This side covers the physical loss tied to the vehicle and anything else damaged in the crash.

The main pieces are:

- Repair cost: What it takes to restore the vehicle to pre-loss condition.

- Total loss value: What the vehicle was worth immediately before the crash if repairs don't make economic sense.

- Diminished value: The loss in market value after a repaired vehicle now carries an accident history.

- Related personal property: Items damaged in the vehicle, if covered and properly documented.

A lot of drivers focus only on repair cost or total loss value. That's too narrow. If your vehicle was repaired but now carries a permanent stigma in the market, diminished value may matter just as much as the body shop invoice.

Personal injury

This side is built from economic damages and non-economic damages.

Economic damages are the direct financial losses. Medical bills, future treatment, lost wages, and reduced earning capacity fit here. Non-economic damages cover the human side, such as pain and suffering.

The broad national anchor is lower than many people expect. The Bureau of Justice Statistics found that motor vehicle crash cases had a median award of about $16,000, which makes median a better reality check than flashy averages because it's less distorted by a few massive verdicts, as summarized in this discussion of personal injury settlement medians.

Practical rule: Don't ask, “What's the average settlement?” Ask, “What are the components of my claim, and what evidence supports each one?”

Why this matters in the real world

If you only think about “my settlement,” you'll miss where the money is won or lost. A weak total loss valuation can short you on the vehicle. Thin medical records can shrink the injury side. A missed diminished value claim can leave money on the table even after the repair check clears.

Here's a clean way to look at it:

| Claim component | What drives value |

|---|---|

| Property damage | Vehicle condition, trim, options, mileage, local comparables, repair quality, accident history |

| Economic injury damages | Bills, wage proof, treatment records, future care evidence |

| Non-economic injury damages | Severity, recovery length, permanence, daily impact, documentation quality |

If you want to compare how another state-specific legal guide frames the broader claim process, this overview of the auto accident settlement process in Florida gives a useful contrast on how claims are assembled and negotiated.

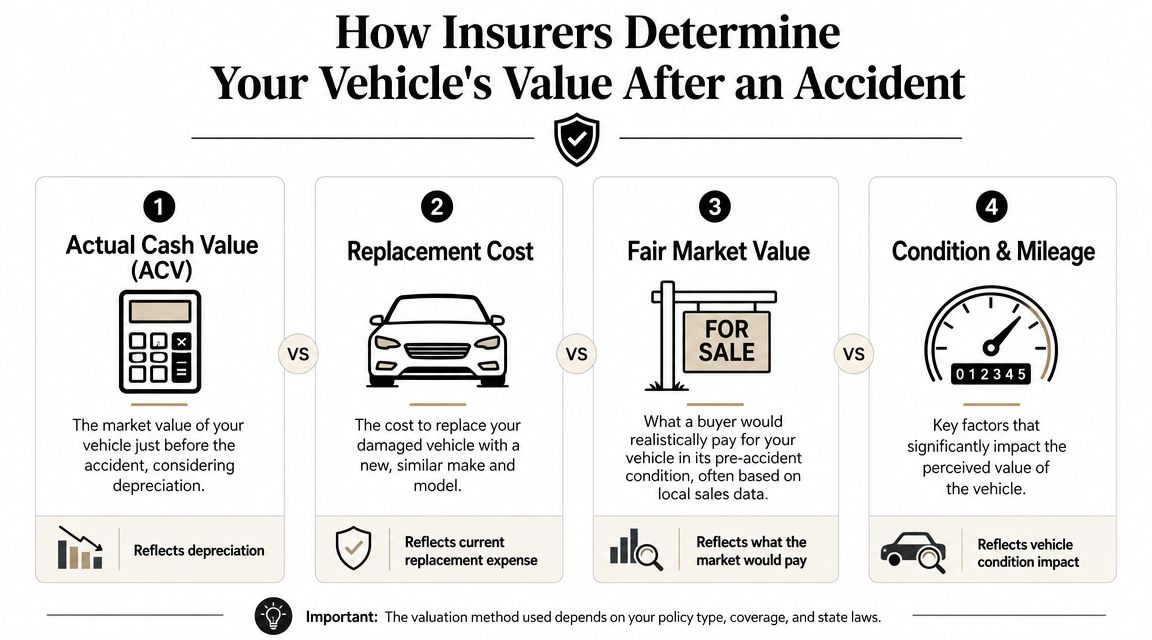

How Insurers Calculate Your Vehicle's Value

When an insurer declares your vehicle a total loss, the number usually doesn't come from a person studying your local market by hand. It usually comes from valuation software, a database, and a report that looks objective because it's formatted to look objective.

That's the first problem.

What the report is trying to do

Insurers generally build an Actual Cash Value opinion from comparable vehicles, mileage adjustments, condition scoring, and option lists. On paper, that sounds reasonable. In practice, small errors stack up fast.

A missed package. Wrong trim. Generic condition adjustments. Comps pulled from outside your real buying area. Listings that don't reflect what buyers would pay for a similar vehicle in your market. Any one of those can drag the number down.

If you want to understand the software side more clearly, this breakdown of CCC auto valuation is worth reading before you argue over the report line by line.

Where lowballing usually happens

Most low valuations don't come from one giant mistake. They come from several smaller ones.

- Condition gets flattened: Your well-kept vehicle gets treated like an average one.

- Local demand gets ignored: A strong Oregon or Washington market for your model may not show up correctly in broad database pulls.

- Comparable vehicles aren't comparable: Similar year and make isn't enough if trim, drivetrain, mileage, or equipment are off.

- Dealer asking prices and actual market realities get blended poorly: The result can look polished and still miss your car's real pre-loss value.

That's why I tell clients to stop arguing with the final number first. Start with the inputs. If the inputs are wrong, the result will be wrong every time.

The insurer's report is only as good as the data inside it. Review every line like you're auditing a tax return.

Diminished value gets overlooked far too often

Drivers also lose money after repairs because they never assert a diminished value claim. Buyers pay less for a vehicle with an accident history. That's normal market behavior.

There are two broad ways this shows up:

| Type of diminished value | What it means |

|---|---|

| Inherent diminished value | The automatic loss in resale value because the vehicle now has an accident record |

| Repair-related diminished value | Extra loss caused by poor repairs, visible defects, mismatched finishes, or unresolved issues |

Insurers don't volunteer this. You usually have to raise it yourself, then support it with an appraisal that reflects market reaction, not internal assumptions.

Why an independent market-based appraisal matters

A proper independent appraisal shifts the dispute from software output to market evidence. That's a major difference. Instead of debating the insurer's black box, you're presenting a documented valuation based on comparable sales, vehicle specifics, and pre-loss condition.

For clean daily drivers, the gap can matter. For specialty, collector, custom, and high-end vehicles, it can be decisive.

Key Factors That Affect Your Payout Amount

Some claims settle cleanly. Others get squeezed from every angle. The difference usually comes down to a handful of variables that move the payout up or down.

Injury severity and vehicle damage

The bigger the injury and the longer the recovery, the wider the settlement range becomes. Publicly reported ranges show that minor to moderate injury cases often settle between $10,000 and $60,000, while catastrophic injuries such as traumatic brain or spinal cord damage can move above $100,000, with paralysis cases often estimated at $750,000 to $5 million or more, based on this reported settlement range overview.

That doesn't mean your claim fits neatly into a chart. It means severity changes scale.

On the property side, a heavily damaged newer vehicle, a rare trim, or a car with unusually strong resale demand will create a bigger valuation fight than a basic commuter with abundant comps.

Documentation quality

At this stage, many valid claims get cut down.

If your file has clear photos, repair records, maintenance history, window sticker data, receipts for upgrades, medical records, wage loss proof, and a clean timeline, you're harder to lowball. If your file is thin, the insurer has room to narrow everything.

Here's the truth:

- Photos matter: Pre-loss and post-loss condition photos help establish value and damage scope.

- Medical continuity matters: Gaps in treatment can weaken the injury side.

- Receipts matter: Tires, recent service, parts, and upgrades can support pre-loss condition and vehicle value.

- Paper trails matter: If it isn't documented, the adjuster may treat it as if it didn't exist.

Fault and policy limits

Some levers are in your control. These are not.

If liability is disputed, the argument over fault can shrink your recovery. If the at-fault driver has limited coverage, that can cap what's available through that policy, even when your damages are stronger than the policy.

That doesn't mean you stop pushing. It means you evaluate the whole recovery path, including your own coverages where applicable.

State law and claim type

The rules vary by state. Oregon and Washington drivers need to pay attention to local claim handling, comparative fault issues, available coverages, and whether the fight is about injury, total loss, or diminished value.

A strong claim is part facts, part paperwork, and part timing. Miss one of those, and the number drops.

A quick self-audit

Before you respond to the insurer, ask yourself:

- Do I have proof of the vehicle's pre-loss condition?

- Can I show true local market value, not just generic comps?

- Have I documented every injury-related expense and work loss?

- Is fault clear, or do I need to address blame arguments?

- Am I dealing with a repair claim, a total loss claim, a diminished value claim, or all three?

Most low settlements aren't mysterious. They trace back to one of those pressure points.

Sample Calculations and Settlement Ranges

Let's strip the theory out of this and look at the math the way a claim professional would.

Example one: Total loss valuation dispute

Your insurer says your vehicle is a total loss and sends a valuation report. You review it and find weak comps, missing options, and condition adjustments that don't match the car you owned.

The insurer offers $12,000. You commission an independent appraisal based on real comparables and your vehicle's documented condition. That analysis supports $15,500 as fair market value.

That gap matters because total loss disputes are often won by replacing a weak report with a better one, not by arguing harder. If you want to understand the framework behind market-based valuation, this guide on how to calculate fair market value lays out the logic.

Example two: Personal injury using the multiplier method

Now take an injury claim. Start with documented economic damages such as medical bills and lost wages.

A common benchmark is the multiplier method, where non-economic damages are estimated at 1.5x to 2x economic losses for minor injuries, and can rise to 4x to 5x or more for severe or permanent injuries, as explained in this overview of car accident settlement values in California.

Use the moderate-injury example from your prompt notes:

| Item | Amount |

|---|---|

| Medical bills and lost wages | $10,000 |

| Applied multiplier for a moderate injury | 3x |

| Estimated non-economic damages | $30,000 |

| Target total settlement | $40,000 |

That's not a promise. It's a framework.

Why examples matter

Settlement value gets clearer when you separate the parts:

- Vehicle claim: What was the car worth right before impact?

- Diminished value claim: What did the accident history do to resale value after repair?

- Injury claim: What are the hard costs, and what multiplier is supported by the records?

The same source above also notes that $50,000 in economic damages could imply a case value of about $250,000 or more when severe-injury multipliers apply. That shows how sharply claims can separate once surgery, long recovery, permanent impairment, or future care enters the record.

If you don't break the claim into pieces, you can't test whether the insurer's number makes sense.

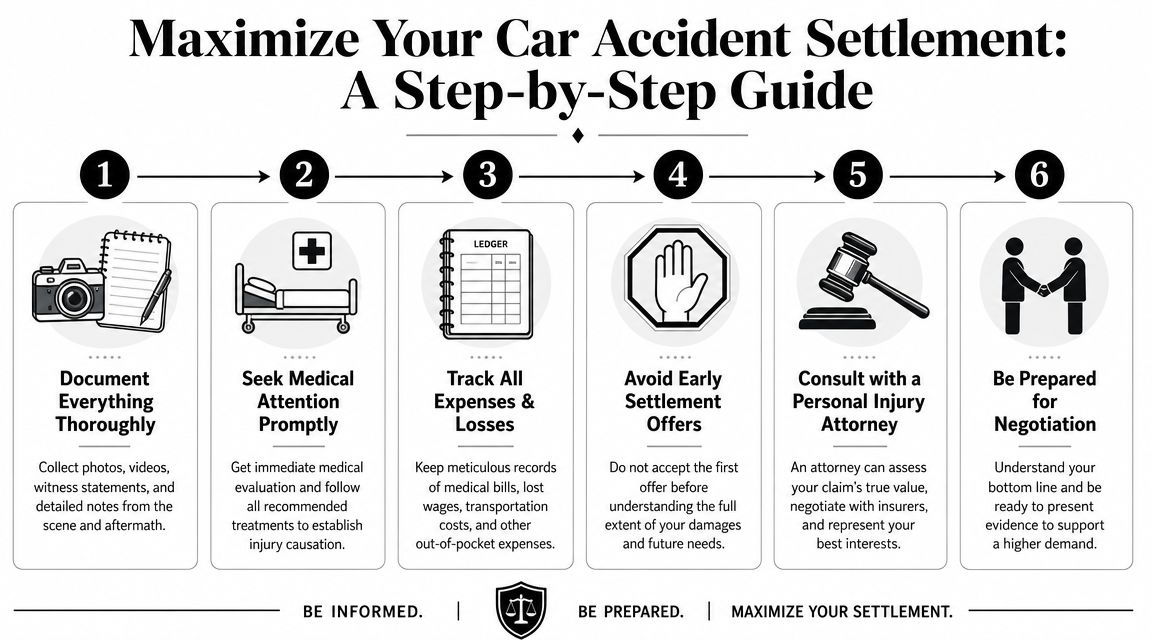

A Step-by-Step Guide to Maximize Your Settlement

You get the insurer's valuation, scan the number, and feel your stomach drop. The car was clean, well-maintained, and worth more than the offer suggests. That moment matters. If you accept the carrier's report at face value, you hand over control of the claim.

Use a process instead. Oregon and Washington drivers get lowballed for one reason more than any other. They argue with the number before they inspect how the number was built.

Step one: build your evidence file first

Start with documents, photos, and records. Get the insurer's valuation report, the repair estimate, vehicle photos, crash photos, maintenance receipts, title records, option packages, recent upgrades, and every email or letter from the adjuster.

For injury-related damages, keep medical records, bills, treatment notes, and proof of lost income in one folder. Insurers often rely on software and coded inputs to value injury claims, which is one reason supported records matter so much, as explained in this analysis of how insurers value injuries.

Weak paperwork gets weak offers.

Step two: challenge the offer in writing

Reply fast, but stay controlled. Tell the adjuster you dispute the valuation and want the full basis for the offer, including comparable vehicles, condition adjustments, trim level, mileage, options, prior condition, and any deductions.

Keep it short. Keep it factual. Ask for the valuation report if they have not sent it.

Bottom line: Written, specific objections carry more weight than angry phone calls.

Step three: audit the insurer's report line by line

Owners often miss out on money. Be sure to check for the wrong trim, missing packages, bad mileage adjustments, poor condition grades, unrelated prior damage, weak comparable sales, or comps pulled from the wrong market area.

If the car is repairable but the estimate is close to the tipping point, learn how a constructive total loss claim is determined. That issue comes up often in Oregon and Washington, and the carrier's math is not always as solid as it looks.

Do not argue in general terms. Mark each error and attach proof.

Step four: get an independent appraisal

For a total loss or diminished value dispute, this is usually the turning point. An independent appraiser can inspect the vehicle history, review the insurer's valuation, verify options and condition, and pull better market comparables.

That gives you something the adjuster has to answer. Total Loss Northwest provides independent total loss and diminished value appraisals for Oregon and Washington vehicle owners and can assist with the appraisal process under the policy.

Step five: invoke the Appraisal Clause when the carrier stalls

If your policy includes an Appraisal Clause and the fight is about the amount of loss, use it. Stop waiting for the adjuster to suddenly become generous.

The Appraisal Clause shifts the dispute into a formal valuation process. That matters because insurers are comfortable repeating the same internal number for weeks. They are less comfortable defending a weak report against an independent appraiser in a structured process.

| Approach | What usually happens |

|---|---|

| Back-and-forth with the adjuster alone | The same report gets repeated with small or no movement |

| Independent appraisal plus Appraisal Clause | The value dispute gets tested through a formal process with competing appraisals |

A short explainer may help if you want a visual overview of the process:

Step six: make a targeted demand

Once you have support, ask for a specific correction. Identify the exact errors, attach the independent appraisal, include your photos and receipts, and state the dollar amount you want paid.

Do not send a vague complaint. Send a clean package with:

- The valuation errors: wrong trim, omitted options, bad condition score, bad comps, unsupported deductions

- Your supporting proof: photos, maintenance history, receipts, title documents, local comparable vehicles

- The corrected number: revised total loss value, diminished value amount, or both

- Your deadline for response: a reasonable date for the carrier to confirm its position

Specific demands get better results than open-ended arguments.

Step seven: bring in a lawyer only when the dispute calls for one

For straight property damage valuation fights, an appraiser often solves the core problem faster than an attorney. For severe injuries, disputed fault, policy limit issues, or permanent impairment, get legal counsel involved early.

Use the right specialist for the right dispute. That is how you protect the claim and avoid a cheap settlement.

Special Rules for Drivers in Oregon and Washington

If you drive in Oregon or Washington, generic national advice won't cut it. The claim strategy has to fit the local rules.

Oregon drivers

Oregon policies commonly involve Personal Injury Protection, which means medical bills can start flowing through your own coverage early in the claim. That helps with immediate treatment issues, but it doesn't erase the need to document the injury side carefully if a liability claim follows.

For property damage, Oregon drivers should watch total loss and diminished value valuations closely. If the insurer's math feels off, don't treat that as normal. Audit the report and compare it to the local market.

Washington drivers

Washington follows a pure comparative fault approach. The practical takeaway is that being partly at fault doesn't automatically wipe out recovery. It can still reduce what you recover, so liability facts matter from day one.

That makes documentation especially important. Statements, photos, point of impact, scene layout, and repair evidence all become more valuable when fault is contested.

Why the Appraisal Clause matters here

In both states, drivers can run into the same problem. The insurer relies on its valuation system and expects the owner to give up after a few calls.

That's where appraisal becomes useful. A structured appraisal dispute is often more effective than endless informal negotiation, especially for total loss and diminished value cases. It also matters in borderline situations, including claims where the vehicle may be close to a constructive total loss even if the insurer hasn't framed it that way yet.

In Oregon and Washington, the fastest way to lose money is to assume the insurer's valuation process is neutral. It isn't.

If you own a high-value, collector, or unusually clean vehicle, this point gets even sharper. Automated systems tend to flatten nuance. Appraisals restore it.

Frequently Asked Questions About Settlement Value

A few questions come up in almost every claim, especially once you realize the insurer's first number isn't the final word.

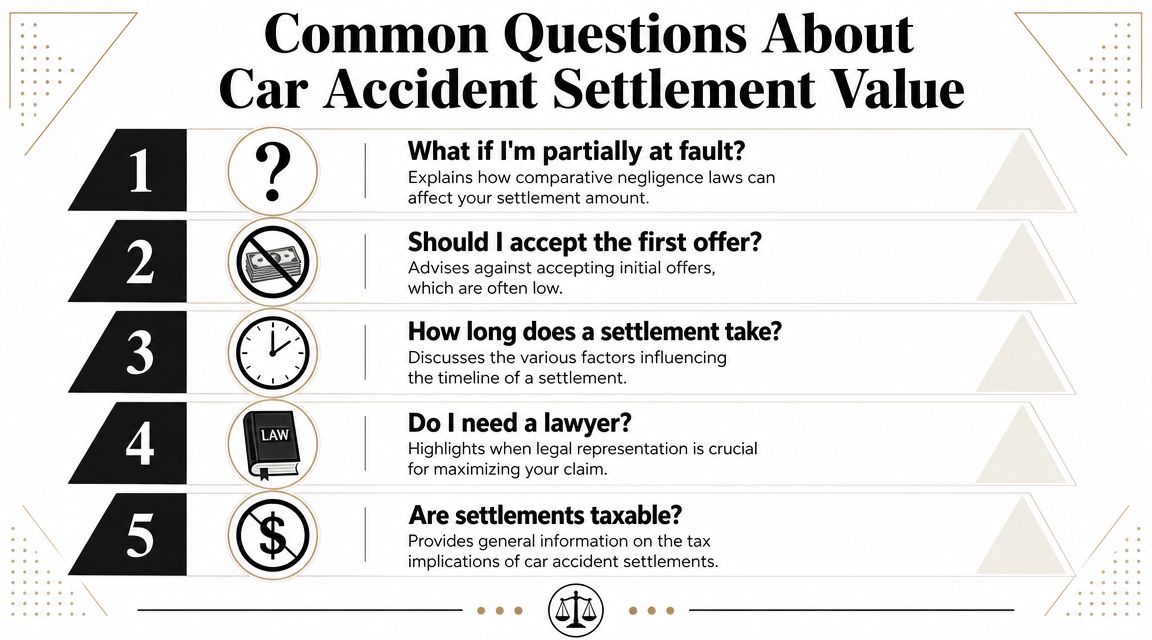

Do I need a lawyer to get a fair settlement?

Not always.

If the fight is mainly about property damage, total loss value, or diminished value, an independent appraiser is often the critical professional. If the claim involves severe injury, disputed fault, major wage loss, permanent impairment, or policy-limit issues, a lawyer becomes much more important.

Use the right tool for the right dispute.

Should I accept the first offer?

Usually, no. Not before you understand how the insurer reached it.

Ask for the valuation report, review the comparables, confirm the trim and options, check the condition adjustments, and compare the number to real local market evidence. On injury claims, review whether the offer reflects only bills already incurred or the broader impact supported by your records.

How long does a settlement take?

There's no honest one-size-fits-all answer.

Property damage claims can move quickly if value is clear. They can also drag if the insurer won't budge and appraisal becomes necessary. Injury claims often take longer because treatment has to stabilize before the claim can be valued intelligently.

Fast isn't always good. Fast often means discounted.

What if the at-fault driver is uninsured?

Then you look at your own policy. Uninsured or underinsured motorist coverage may become central, depending on the claim type and policy language.

Review the policy early. Don't wait until the liability carrier says there isn't enough coverage.

Are settlements taxable?

That's a tax question, not an appraisal question. Ask a qualified tax professional before you assume anything.

A lot of drivers also want a plain-language insurance FAQ from outside their own state to help decode common terms. This auto insurance guide for New York drivers is useful for that broader insurance vocabulary, even if your claim is in the Northwest.

What's the smartest next move if I think I'm being lowballed?

Do these three things first:

- Get the full valuation report or written basis for the offer.

- Organize your evidence before arguing.

- Decide whether the dispute is best handled by an appraiser, a lawyer, or both.

Most lowball offers survive because the driver never changes the process. Change the process, and you change the negotiating position.

If your insurer's number doesn't reflect your vehicle's real market value, don't guess and don't accept it out of frustration. Total Loss Northwest handles independent total loss and diminished value appraisals for Oregon and Washington drivers, and can invoke the Appraisal Clause when the insurer's valuation process needs to be challenged.