You're dealing with one of the most frustrating parts of an accident claim. The crash wasn't your fault, the bills or vehicle loss are real, and then the adjuster says the words that change the whole conversation: policy limits.

That usually happens when your damages are larger than the coverage available under the at-fault driver's policy. Maybe your injuries are serious. Maybe your newer SUV or custom truck is a total loss. Maybe both. Either way, the insurer is telling you there's a ceiling, and that ceiling may have very little to do with what you lost.

A lot of guides stop there. They define the term and move on. That doesn't help much when you still need to pay medical bills, replace a vehicle, cover sales tax and fees, or deal with a lowball total-loss valuation. What matters isn't just what a policy limits settlement is. What matters is what it leaves unpaid, what rights you may be giving up, and what recovery options still exist after that check is offered.

Your Accident Damages Are More Than Their Insurance Covers

A common call goes like this. You finally get through the first round of paperwork, you've sent photos, estimates, medical records, maybe the police report, and the insurer says they may be willing to tender the other driver's limits. That can sound like good news until you realize they're not saying your claim is fully paid. They're saying they may pay all that their insured purchased.

For injury claims, that can leave a large gap. For vehicle owners, it can create a different kind of trap. If your truck, classic car, or late-model daily driver is totaled, the at-fault driver's coverage may not be enough to match what the vehicle was worth in the market. That's one reason people carry extra protection themselves, including umbrella coverage. If you're trying to understand how extra layers work on the front end, this breakdown of umbrella insurance pricing in Kansas is useful because it shows how people buy protection above standard auto limits.

The first thing to understand is simple: liability insurance pays according to policy language and limits, not according to your stress level or the seriousness of the crash. If you're unclear on the basics of fault-based coverage, this guide on what liability insurance covers is a good grounding point.

Most people don't get taken advantage of because they're careless. They get taken advantage of because they assume “full limits” means “full compensation.”

That assumption is where expensive mistakes start. A policy limits settlement can be a smart move. It can also close one door while leaving major money unresolved. You need to know which situation you're in before you sign anything.

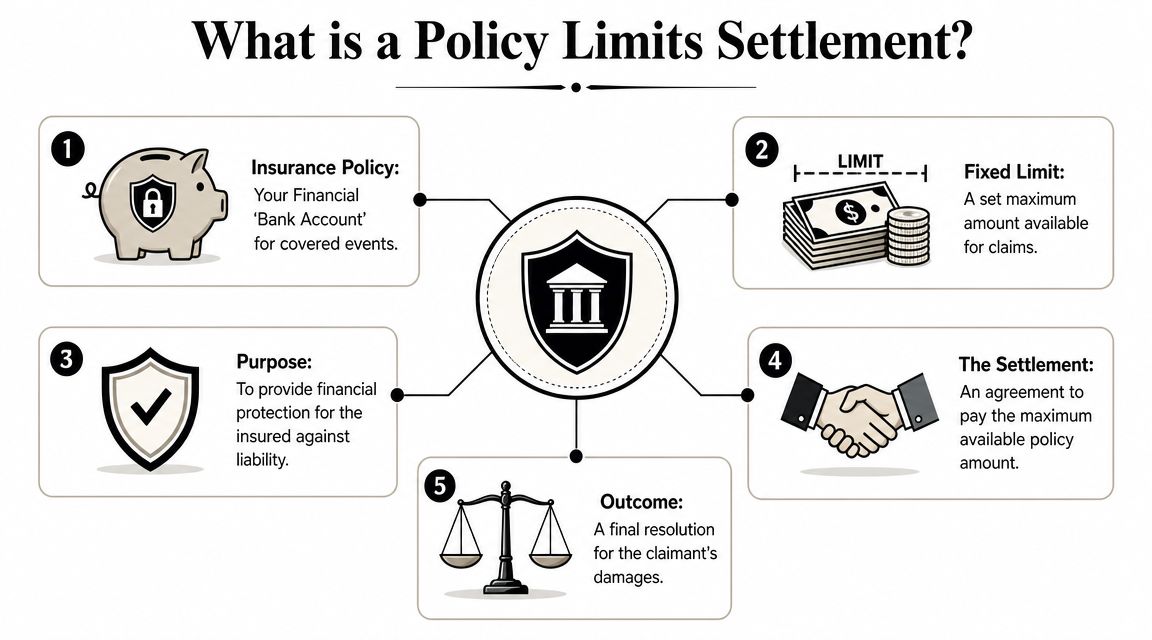

What a Policy Limits Settlement Actually Means

A carrier can tender policy limits and still leave you badly undercompensated.

That is the part many claimants miss. A policy limits settlement means the insurer is offering the most it says it owes under that specific policy. It does not mean your injuries were fully valued, your wage loss was fully covered, or your vehicle damage was resolved correctly.

What the limit applies to

Auto liability coverage is capped by the policy language. For bodily injury, those limits are often split by person and by accident. Property damage is usually capped separately. Once the available limit is exhausted, the insurer's payment obligation under that policy usually ends, even if your losses continue far past that number.

That distinction matters because financial recovery rarely fits neatly inside one insurance bucket. A bodily injury limits payment does not automatically solve a total loss dispute. A property damage limits payment does not address medical bills. If the at-fault driver's coverage runs out, the remaining question is where the unpaid balance can be pursued next.

Claim value and available insurance are different numbers

I tell clients to separate these issues early.

| Issue | What it means |

|---|---|

| Claim value | The full amount your injuries, income loss, vehicle loss, and out-of-pocket damages may support |

| Policy limit | The maximum payable from that one insurer under that one coverage part |

| Your remaining shortfall | What is still unpaid after the policy limit check is issued |

Expensive mistakes frequently occur. An insurer may be perfectly willing to pay limits because the exposure is obvious and the cap protects the company. That can be a fair tender under the policy and still be far short of what you need to recover overall.

What this means for your total recovery

The core question is not whether limits were offered. The core question is what remains open after that offer.

For injury claims, the shortfall may need to be pursued through other coverage, including your own underinsured motorist coverage, or in some cases directly against the at-fault party if collectible assets exist. For vehicle owners, the unresolved issue is often property damage. I see this in total loss files all the time. The carrier may say, "we paid the limit" or "we paid actual cash value," while the owner is still fighting over comparable vehicles, condition adjustments, aftermarket equipment, tax, title, fees, or the simple fact that the valuation came in low.

A policy limits settlement closes the insurer's ceiling. It does not automatically close every dollar you lost.

Why coverage documents matter before you sign

Before accepting any limits payment, get clear on which coverage part is being paid, whether other coverage may apply, and whether the release language wipes out claims you have not fully measured yet. The declarations page, tender letter, and release form matter as much as the check amount.

That is the practical meaning of a policy limits settlement. It sets the ceiling for one source of insurance. Your job is to make sure you do not mistake that ceiling for the full value of your case.

Common Scenarios for Policy Limits Demands

Some claims practically announce themselves as policy-limits cases from day one. Others don't look that way until records, estimates, and valuations come in.

Serious injury with low liability coverage

A rear-end collision can become a policy-limits case if the injuries are severe enough. Surgery, extended treatment, time off work, and permanent limitations can push losses far beyond the at-fault driver's available bodily injury coverage. When that happens, asking for the full available liability limit is often the right move because it forces the insurer to deal with the obvious mismatch between the damage and the policy.

That still may not make the injured person whole. When the at-fault driver is underinsured, your own coverage can matter a lot. If you haven't reviewed that yet, this explanation of uninsured and underinsured motorist coverage helps clarify where additional recovery may come from.

Total loss of a higher-value vehicle

At this point, many drivers get blindsided.

The other driver may have enough insurance to handle an average repair bill, but not enough to pay for a totaled newer pickup, a restored classic, or a customized vehicle with real market value. The insurer may acknowledge that the vehicle is a total loss and still tell you that property damage coverage is limited. At that point, the available liability insurance becomes a ceiling, not a valuation answer.

That leaves two separate questions on the table:

- Coverage question. Is there enough property damage liability coverage available?

- Valuation question. Did the insurer even value the vehicle correctly?

Those are not the same dispute. A carrier can say, “We'll pay the limits,” while still undervaluing the vehicle or omitting related property-damage items in the process.

Multi-layer claims

Sometimes the visible policy isn't the whole picture. A crash may involve a driver using a company vehicle, someone acting within employment, multiple potentially responsible parties, or additional coverage above the primary policy. Those cases need a wider lens.

A policy limits demand makes sense when one layer is clearly exhausted by the loss. It does not mean the file is necessarily over. It means one source of money may be maxed out, and the next recovery source needs to be identified quickly.

If your damages are larger than one policy, your real job is stacking recovery, not celebrating the first tender.

How Policy Limits Are Demanded and Paid

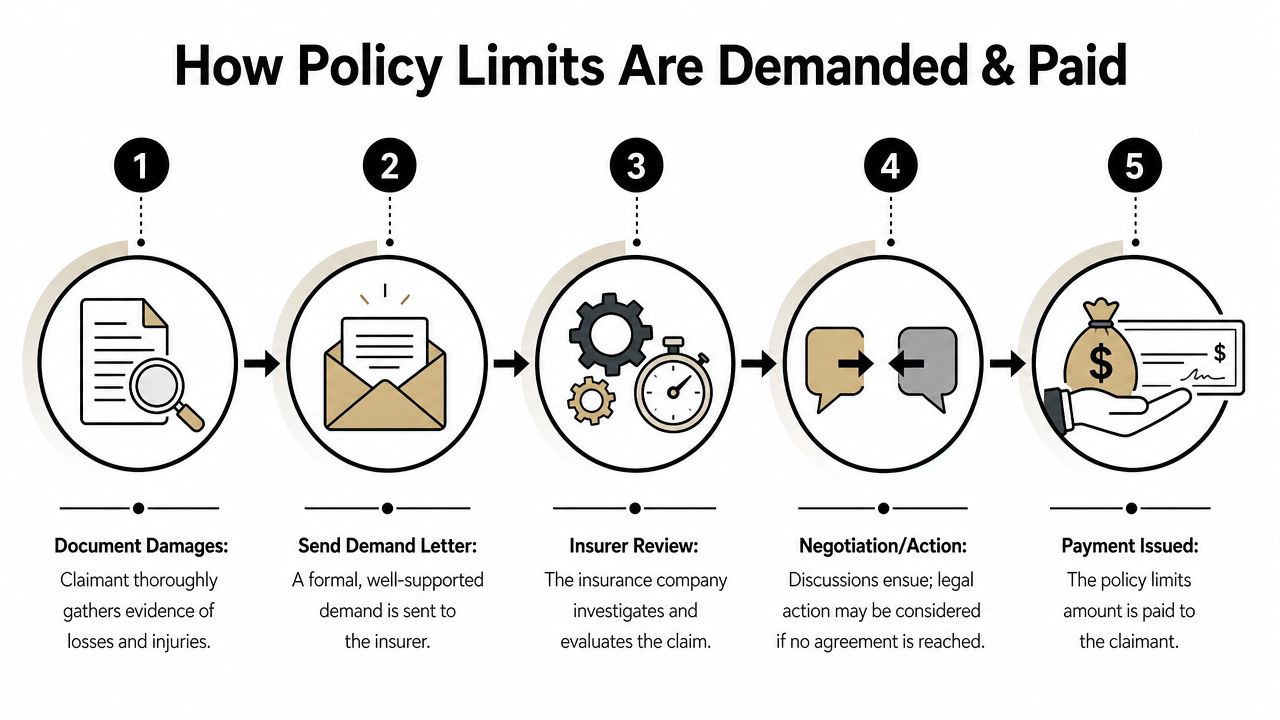

Insurers don't usually volunteer the cleanest path to paying limits. The process is driven by documentation, procedure, and pressure. If you want a policy limits settlement, you need to show why the claim clearly exceeds available coverage and make it easy for the insurer to justify paying every dollar of that layer.

Step one is proving the file, not arguing the file

The strongest policy-limits demands aren't emotional. They're organized. The package should show liability, document your damages, and remove doubt about the size of the loss.

That usually means assembling:

- Liability proof such as the police report, witness statements, scene photos, and any admission against interest

- Damage proof including medical records, repair estimates, total-loss documents, wage loss support, towing bills, and receipts

- Timeline proof that shows treatment, interruptions to work, and how the claim developed

The demand letter matters

Once the evidence is together, the claimant or attorney sends a formal policy limits demand letter. The letter typically states the facts, explains why damages exceed coverage, demands the full available limits, and gives the carrier a deadline to respond.

In Texas, policy-limits disclosure often happens through formal discovery after a lawsuit is filed, and when a proper Request for Disclosure is served, the responding party generally has 30 days to provide the requested insurance information, according to this explanation of Texas insurance policy limits disclosure. That timing matters because claimants often can't make a smart limits demand until they know what coverage exists.

What insurers do next

After receiving a demand, the insurer reviews the file and evaluates exposure. If the damages clearly exceed the policy and the demand is properly supported, the carrier may decide to pay limits to protect its insured and close that coverage layer.

A typical sequence looks like this:

- You document the full loss

- You send a supported demand

- The insurer investigates

- The carrier accepts, rejects, or seeks more information

- Payment is issued if the demand is accepted

The demand has to do more than ask for money. It has to show the insurer why refusing the demand creates risk.

What slows payment down

Several things drag out policy-limits cases:

- Incomplete records that leave the carrier room to say the claim isn't fully evaluated

- Unclear liability where the insurer argues fault isn't settled

- Missing policy information that prevents realistic demand strategy

- Property damage disputes where valuation itself is still being fought

The cleaner your file, the harder it is for the insurer to stall without exposing itself to trouble later.

Understanding the Legal Stakes and Release Forms

A policy limits settlement can protect you or hurt you. The difference usually comes down to paperwork. The money itself is only one part of the transaction. The release is the other part, and that's where people give away rights they didn't mean to surrender.

The settlement only resolves a policy layer

A policy limits settlement is the insurer's ceiling exposure under a liability policy, not a measure of your total damages. In practice, a carrier may pay the full per-occurrence limit even when the loss is much larger. For example, a $100,000 liability limit can resolve only $100,000 of a $200,000 injury claim, leaving the rest potentially collectible from other sources, as described in this overview of what a policy limits settlement means.

That is why claim strategy should begin by identifying every possible policy layer before negotiating final paperwork. Underinsured motorist coverage, excess policies, umbrella coverage, or defendant assets may still matter even after one insurer tenders limits.

Why bad-faith setup matters

When damages clearly exceed available coverage, a properly framed limits demand can do more than request payment. It can create a record. If the insurer refuses an objectively reasonable opportunity to settle within limits and exposes its own insured to a larger judgment, that refusal may become legally important later.

Few pursue litigation for a bad-faith issue themselves, but they should understand the pressure point. A well-supported demand with a clear deadline tells the insurer this isn't a vague complaint. It's a documented chance to do the sensible thing.

The release is where the danger lives

Once the carrier agrees to pay, it will usually require a release. Read that document slowly. A release can extinguish claims against the insurer, the at-fault driver, or both. It can also use broad language that reaches farther than commonly understood.

Watch for language tied to:

- All bodily injury claims

- All property damage claims

- Unknown future claims

- Any person or entity related to the accident

If you're signing electronically, make sure you understand the document workflow before clicking through. A practical primer like SignWith's guide on e-signatures helps people understand how electronic contract signing works, but the larger issue here is not the tech. It's the content of the release.

Before reviewing a release, it helps to hear how lawyers frame the risk in plain language.

Don't treat the release like a receipt. Treat it like the final map of what you can never claim again.

Writing an Effective Policy Limits Demand Letter

A good demand letter doesn't need dramatic language. It needs a clean file, a credible story, and enough support that the carrier can't pretend the exposure is unclear.

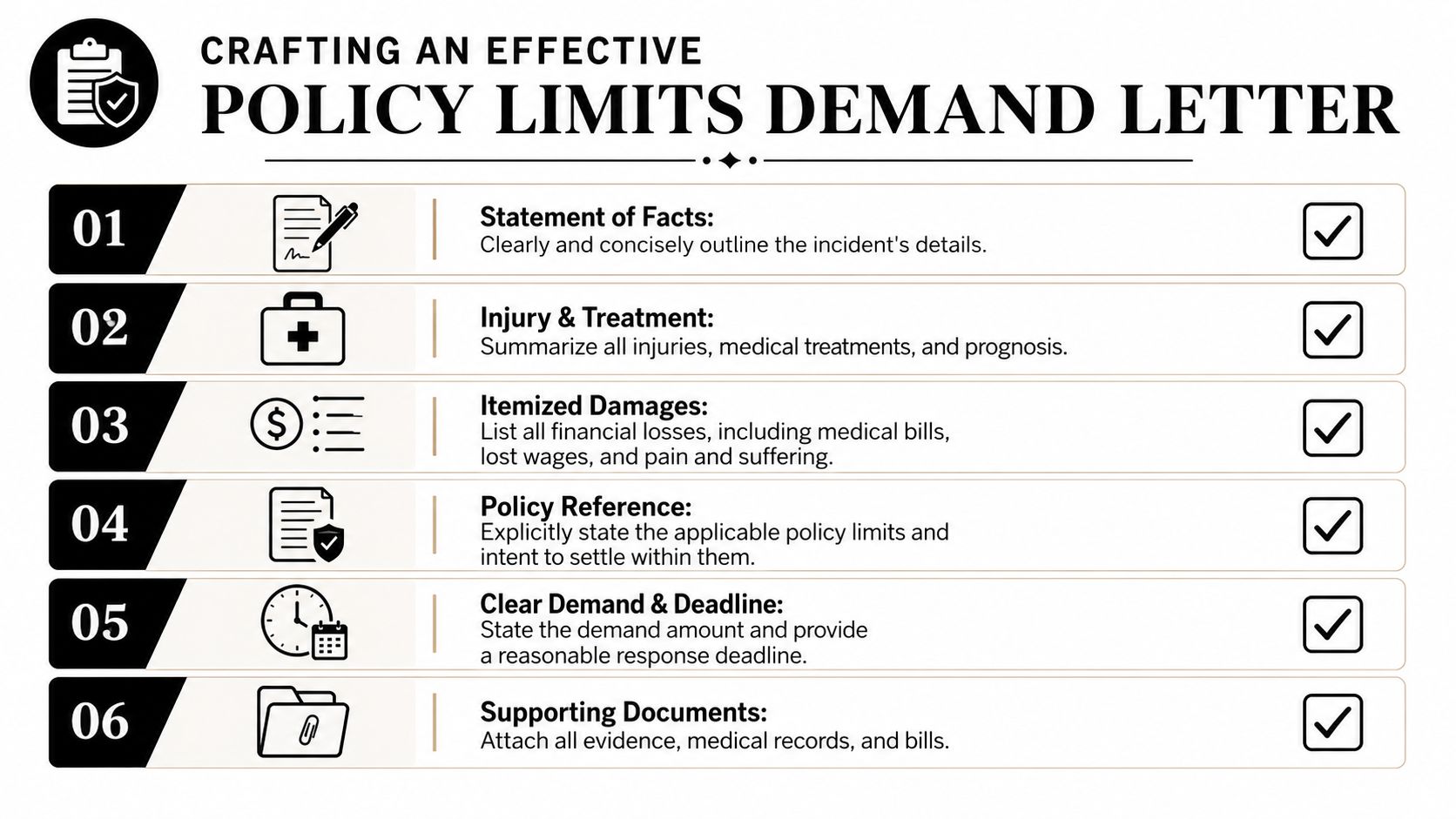

What to include

Build the letter like a claim package, not like a complaint.

- Start with fault. Identify the crash date, location, parties, and why the other driver is responsible.

- Summarize the harm. Describe injuries, treatment, vehicle damage, loss of use, or total-loss consequences in plain terms.

- Attach the paper. Include records, bills, photos, reports, estimates, receipts, wage support, and valuation material.

- State the demand clearly. Ask for the full available policy limits, not “fair compensation” in the abstract.

- Set a response deadline. Give the insurer a reasonable time to evaluate and respond.

- Preserve accuracy. Make sure the facts, names, policy references, and attachments line up.

A practical structure that works

Use this order because adjusters and defense counsel read for clarity first:

| Part | What it should do |

|---|---|

| Opening paragraph | Identify the claim and state that you are making a policy limits demand |

| Liability section | Show why the insured is at fault |

| Damages section | Explain the scope of injury or property loss |

| Attachments list | Prove what you are saying |

| Demand paragraph | Request full limits and set a deadline |

Please accept this correspondence as a formal demand for tender of all applicable liability policy limits arising from the collision. The evidence establishes your insured's responsibility, and the documented damages exceed the available coverage. If the carrier needs any additional records to evaluate this demand, that request should be made immediately and in writing.

What weakens a demand

A surprising number of demands fail because the claimant leaves gaps the insurer can exploit.

Common mistakes include:

- Asking without documenting. A demand is only as strong as what's attached.

- Bundling unresolved issues. If liability, injury, total-loss value, and rental charges are all mixed together unclearly, the insurer gains room to delay.

- Using inflated language. Overstated claims make under-supported files look weaker, not stronger.

- Ignoring property valuation evidence. For total-loss disputes, market comps, condition details, options, upgrades, and comparable vehicle support matter.

If you need a working example before drafting your own package, this guide to an insurance demand letter gives you a practical starting point.

For total-loss claims, separate limit issues from value issues

If the carrier says it is tendering available property damage limits, that does not automatically prove its valuation was correct. In Washington and Oregon, some owners also use the appraisal process to challenge the insurer's valuation methodology. Total Loss Northwest is one option for that kind of dispute. It works in the appraisal lane, where the fight is over market value rather than generic negotiation.

FAQs About Policy Limits and Your Total Recovery

Can I recover more after accepting a policy limits settlement

Yes, sometimes. It depends on the release you signed, the claim that was paid, and whether other coverage or other defendants are still in play.

A policy limits payment usually closes one lane of recovery, not every lane. You may still have a claim under your own uninsured or underinsured motorist coverage, medical payments coverage, an umbrella policy, or against another party who shares fault. The expensive mistake is treating the first limits check like a full accounting of your loss.

That matters most when your damages are larger than the at-fault driver's coverage. Medical bills, wage loss, rental charges, and vehicle-related losses can keep running long after one insurer tenders its limits.

If I accept a limits check for my totaled car, can I still dispute the value

Possibly, and in such cases, people give up money without realizing it.

A property damage limits payment does not automatically answer a separate valuation dispute. If your car was totaled, the key question may be whether the insurer paid fair market value, not whether it offered the most available under one coverage bucket. Those are different issues.

Depending on state law and the release language, you may still have unresolved property damage items such as sales tax, title and registration fees, loss of use, rental reimbursement gaps, or diminished value. The release controls a lot here. So does the wording on the check, the settlement letter, and any statement that says the payment resolves all property damage claims. For a closer look at how those issues can overlap, see this analysis of policy limits settlements and total-loss disputes.

In Washington and Oregon, I often see carriers frame a claim as a limits problem when the owner is still fighting over vehicle value. Those are not the same dispute.

How do I find out the at-fault driver's policy limits

It depends on the state, the insurer, and how far the claim has progressed.

Some carriers disclose limits early. Others disclose little until a lawyer presses the issue or formal discovery begins. If the insurer stays vague, do not assume that means the available coverage is low. It may mean the carrier is buying time, waiting to see how much support you have for the claim, or trying to settle before the full picture is clear.

Keep your strategy flexible until limits are confirmed in writing. If the carrier says it is paying limits on the property damage side, review whether the unresolved issue is coverage, valuation, or both. Total Loss Northwest handles appraisal-based disputes for vehicle owners in Washington and Oregon and can help sort out that difference.

If the insurer says it is offering policy limits, slow down before signing anything. A release can shut down claims you did not mean to waive, and a limits tender does not prove the valuation was fair. A careful review of the release, the payment language, and any remaining recovery path can protect money that is still on the table.