The tow truck is gone. Your car is at a shop, a yard, or sitting in an insurer's inspection queue. The crash itself took seconds. The transportation problem starts the next morning.

That's when people learn a hard lesson. Getting your vehicle repaired is only one part of the claim. Getting around while you wait is a separate fight, with separate rules, separate limits, and plenty of room for an insurer to leave you paying out of pocket.

Most drivers treat a rental like a side issue. It isn't. If you handle it poorly, you can burn cash, lose advantage in a total loss negotiation, and weaken the paper trail you need for a diminished value claim. If you handle it correctly, the rental file becomes part of your broader settlement strategy.

The Accident Is Over but Your Transportation Problem Just Began

You wake up sore, irritated, and already behind. The body shop hasn't started repairs. The adjuster hasn't called back. You still need to get to work, pick up kids, make appointments, and keep life moving.

That's why rental car coverage after an accident matters more than is commonly understood. The Insurance Information Institute says the average car is in the repair shop for two weeks after an accident, which can mean 14 days of transportation costs out of pocket if you don't have rental benefits in place (Insurance Information Institute on post-accident rental coverage).

For a household with one vehicle, that gap isn't a nuisance. It's a budget problem. It can also become a claim problem if you wait too long, rent the wrong vehicle, or fail to document why you needed transportation every day the car was unavailable.

What most drivers get wrong

A lot of people assume the other driver's insurer will “just take care of it.” Sometimes they do. Often they stall while they investigate fault, inspect damage, or argue over how long the rental should last.

Meanwhile, you still need transportation.

If the crash also left you dealing with lingering stress, sleep disruption, or post-collision anxiety, practical recovery matters too. For British Columbia readers dealing with the human side of a claim, Support for ICBC related injuries can be a useful resource while the insurance side gets sorted.

Practical rule: Treat the rental as part of the property claim from day one, not as an afterthought once the shop calls.

Regain control fast

Start with one simple move. Pull your declarations page and confirm whether you bought rental reimbursement. Then map out your immediate next steps, including claim reporting, documentation, and preserving evidence through this post-crash action checklist.

If you don't take control early, the insurer controls the pace. When that happens, you're the one paying for their delay.

Understanding Your Three Rental Coverage Options

Think of rental coverage as coming from three different wallets. Your job is to identify which wallet is available, how quickly it opens, and what strings are attached.

Option one is your own rental reimbursement coverage

This is the cleanest path when you need a car immediately. If you bought rental reimbursement before the crash, your insurer may help arrange a rental or reimburse you up to your policy limits.

Progressive explains that rental reimbursement is usually built around a daily limit of about $40 to $70 and a total duration of 30 or 45 days, depending on the state (Progressive's explanation of rental reimbursement limits). That sounds fine until you realize two things. First, your local rental rates may exceed the daily cap. Second, your repair or replacement timeline may outlast the day limit.

It also generally applies to a covered accident, not a mechanical breakdown.

Option two is the at-fault driver's liability coverage

If the other driver caused the crash, rental expense is usually claimed through their property damage liability coverage as part of your loss of use damages. This route can save you from using your own policy benefits, but it usually moves slower because their insurer won't pay before it decides liability and confirms the rental was necessary.

If fault is obvious and accepted quickly, this can work well. If fault is disputed, you may be stuck waiting while still needing transportation.

Option three is paying now and seeking reimbursement later

This is the fallback when neither insurer sets up direct billing fast enough. It's not ideal, but sometimes it's the only practical move.

If you go this route, assume nothing. Keep every receipt, preserve every email, and confirm in writing what rate and time period the insurer says is reasonable. Reimbursement fights usually start when the paper trail is sloppy.

Sources of Rental Car Coverage After an Accident

| Coverage Source | Who Pays | Typical Speed | Key Consideration |

|---|---|---|---|

| Your own rental reimbursement | Your insurer | Usually faster | Limited by your policy's daily and time caps |

| At-fault driver's liability coverage | Other driver's insurer | Often slower | Depends on liability acceptance and claim handling |

| Out of pocket with reimbursement request | You first, insurer later | Immediate access if you can afford it | Documentation must be airtight |

My recommendation

If you have your own rental reimbursement, use it when speed matters. Transportation is a today problem, not a theoretical reimbursement problem. Then let the insurers argue with each other.

If you don't have it, push the liability carrier hard, but don't rent blindly. Confirm what they'll authorize before you sign for a vehicle that exceeds what they consider reasonable.

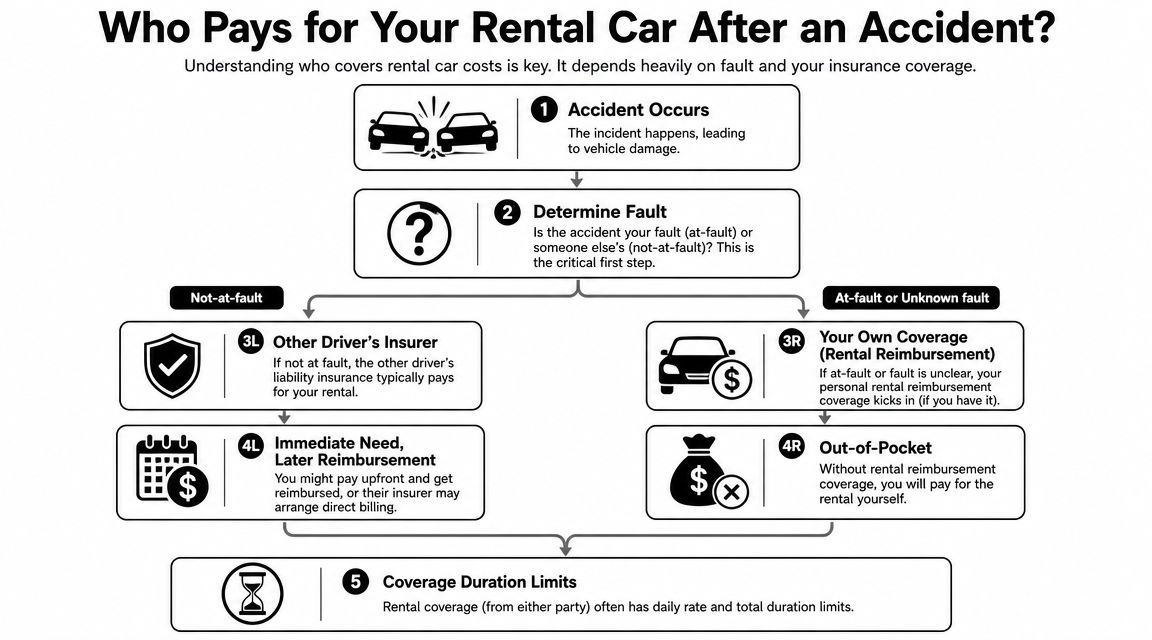

Who Actually Pays for the Rental Car and When

Drivers often lose time and money. They focus on who should pay, not on when payment starts.

If another driver is at fault, rental costs are usually pursued under that driver's liability coverage as loss of use damages. The strongest file includes receipts, the rental agreement, exact rental dates, and repair estimates or invoices showing the vehicle was unavailable (guidance on loss of use rental claims and documentation).

Not at fault doesn't mean immediate payment

A driver can be clearly not at fault in real life and still wait while the liability carrier “investigates.” That insurer works for the other side. Until they accept responsibility, they may refuse to authorize a rental, cap the rate, or tell you to pay first and submit later.

That's why I tell clients not to confuse legal responsibility with practical access to transportation. Those are different issues.

Why your own coverage often gives you more control

If your policy includes rental reimbursement, using it first often gives you the fastest path to a vehicle. Your insurer can then try to recover what it paid from the at-fault carrier through subrogation. You may still care about the final allocation, but you're no longer stranded while two companies debate fault.

That control matters. It also keeps you from making bad short-term decisions, like accepting a weak damage offer because you're desperate to stop paying for a rental.

For a plain-English overview of how fault-based coverage works, this guide on what liability insurance covers is worth reviewing.

The insurer with the least incentive to help you quickly is usually the one you're asking to pay when you file only against the other driver.

The timing problem in third-party claims

Third-party claims often move in stages:

- Claim intake: The carrier opens the file and gathers statements.

- Liability review: They decide whether their driver caused the crash.

- Damage review: They confirm the vehicle is not drivable or is reasonably in repair.

- Rental approval or reimbursement: They authorize direct billing or ask you to front the cost.

That timeline may be manageable if you can wait. For many, that isn't possible.

So the practical answer to “who pays?” is often this: your own insurer pays first if you planned ahead, the other insurer may reimburse later if liability is accepted, and you pay personally if neither moves fast enough.

A Step-by-Step Guide to Claiming Your Rental Costs

Action beats frustration. The drivers who get paid are usually the drivers who build a clean file early.

Start with the basics, then stay organized.

Step one through three

Report the claim immediately

Call your insurer and, if another driver caused the crash, open a third-party property damage claim with that carrier too. Ask one direct question: “Do I have rental reimbursement, and what are my limits?”Ask for direct billing if available

Don't assume reimbursement is the only route. Some insurers or rental agencies can arrange billing directly within approved limits. That helps you avoid fronting the full cost.Confirm the approved vehicle class in writing

You don't need a luxury upgrade unless there's a solid reason. But you also don't have to accept an impractical vehicle if your household needs something functionally comparable. Get the authorization by email if possible.

Build one claim file and keep it current

Your rental claim needs one organized folder, digital or paper. Put everything in it.

- Rental documents: Keep the agreement, pickup date, return date, and final bill.

- Repair records: Save estimates, supplements, shop updates, and final invoices.

- Communication log: Track calls, names, dates, and what each adjuster told you.

- Proof of unavailability: Keep anything showing the car wasn't drivable or was stuck waiting on inspection, teardown, or parts.

Claim file test: If an adjuster changed tomorrow, could a new person read your file and understand exactly why every rental day was necessary?

Stay ahead of the cutoff

Rental issues get messy when the body shop timeline changes. Call the adjuster before the current authorization expires, not after. If repairs are delayed, ask the shop for an updated projected completion date and send it over immediately.

Later in the process, review this walkthrough and compare it to your own file. Then watch this short video if you want a visual refresher on handling the claim process:

The documents that matter most

Some paperwork is merely helpful. Some is absolutely required.

- The rental agreement proves the terms and dates.

- Receipts prove what you paid.

- Repair estimates and invoices tie the rental period to the vehicle's loss of use.

- Written extensions protect you when an insurer later claims you kept the rental too long.

If you skip the documentation, you hand the insurer an opening to cut the claim down.

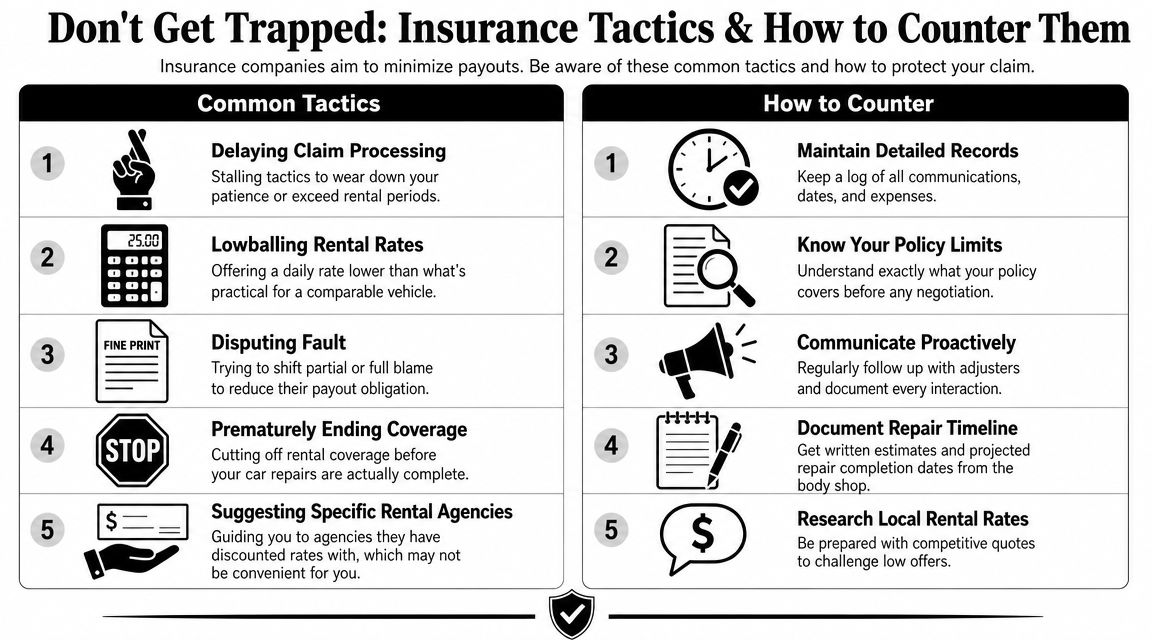

Common Pitfalls and Insurance Company Tactics to Avoid

Most rental disputes aren't about whether you needed transportation. They're about shrinking what the insurer has to pay.

Baldwin notes that rental reimbursement is typically an optional add-on, not automatic, and it usually must be purchased before the loss. It also highlights the practical mismatch when the repair timeline outlasts the policy's capped rental period, often leaving the insured paying the difference (Baldwin on optional rental coverage and time-limit mismatch).

Tactic one is delay

Delay works because rental costs create pressure. The longer the carrier drags its feet, the more likely you are to accept a bad repair decision, a weak total loss number, or a short rental period just to stop the bleeding.

Counter it with documentation and deadlines. Send updates by email. Ask for written responses. If the shop is waiting on approval, note the date that request went in.

Tactic two is pushing an unrealistic rate

Some adjusters quote a daily allowance that only works for a tiny vehicle or a heavily discounted corporate rate at one rental counter across town. That doesn't automatically make it reasonable for your situation.

Push back with local quotes and practical facts. If you need cargo space, child-seat capacity, or a vehicle that matches normal use in a basic way, explain that clearly and calmly.

Tactic three is ending coverage early

This often happens when the shop finds additional damage, a part gets delayed, or the insurer says the “reasonable repair period” has ended even though the car still isn't ready. The carrier may try to frame shop delays as your problem.

Sometimes that argument sticks. Sometimes it doesn't. What matters is whether you can show the rental period stayed tied to the collision claim and repair process.

Don't argue in generalities. Argue with dates, shop emails, estimates, supplements, and written authorization history.

Tactic four is making you think rental is separate from the main claim

It isn't separate. Rental pressure is an advantage. Insurers know some people will fold on value if transportation becomes too expensive or too inconvenient.

That's why you need to treat the rental file as part of the full settlement strategy from the start.

Rental Coverage for Total Loss and Diminished Value Claims

Many drivers find themselves blindsided. A rental car can support you during the claim, but it can also expose the insurer's strategy.

Total loss claims create a dangerous timing gap

When a vehicle is headed toward total loss, rental coverage often ends before your life is back to normal. In practice, the critical moment is usually when the insurer makes its settlement offer, not when you've deposited a check, paid off a loan, or found a replacement car.

That gap matters. If you're still disputing value, still waiting on lienholder paperwork, or still trying to locate a comparable vehicle, the rental clock may already be running out.

So don't wait until the total loss offer arrives to think about transportation. Ask early when rental coverage will stop if the vehicle is declared a total loss. Get that answer in writing.

Long repair history can support a diminished value argument

If the vehicle isn't totaled and goes through extensive repairs, the rental file becomes useful evidence. A long rental period, combined with repair estimates, supplements, and invoices, helps show the seriousness of the damage and the length of loss of use.

That doesn't automatically prove diminished value, but it strengthens the story. A vehicle that needed major structural or extensive repair work is harder to defend as “just as good as before” in the resale market.

If your claim has moved into value-loss territory, review how an automobile diminished value claim works and whether your repair documents support it.

Use the rental file as leverage, not just reimbursement support

Here's the smarter way to approach this topic:

- In a total loss case: the rental timeline pressures you to resolve value quickly, so be ready with comps, records, and a negotiation plan.

- In a repair case with serious damage: the rental period helps document severity and downtime, which can complement a diminished value claim.

- In either case: rental stress should not push you into accepting the insurer's first number.

This is one place where an independent appraiser can matter. Total Loss Northwest handles diminished value and total loss appraisals, including use of the appraisal clause where available. That's relevant when the insurer's valuation, not just the rental cutoff, is the actual problem.

Your Next Steps to Secure a Fair Rental Reimbursement

Don't leave this to chance. Pull your policy today and find out whether you have rental reimbursement. If you do, confirm the daily cap and the day limit. If you don't, stop assuming the other driver's insurer will move quickly enough to protect you.

Then build your file. Save the rental agreement, every receipt, every repair update, and every email with the adjuster. If a phone call matters, send a follow-up email confirming what was said. That one habit prevents a lot of nonsense later.

Use your own coverage first if speed and control matter more than waiting for the liability carrier to cooperate. If you're claiming through the at-fault insurer, keep the documentation tight and force them to deal with specifics, not vague objections. Don't let them cut off coverage casually. Make them explain it in writing.

Most important, don't let rental pressure force a bad settlement on the vehicle itself. That's the trap. People accept weak total loss numbers and drop diminished value claims because they're desperate to end the rental expense.

Stay organized. Stay firm. And if the claim has turned into a valuation fight, get independent help before you sign off on an unfair number.

If your rental problem is tied to a low total loss offer or a serious diminished value dispute, Total Loss Northwest is a practical next call. They work on auto appraisal disputes involving total loss and diminished value, which is often the underlying issue once the rental clock starts working against you.