You open the claim expecting a rational number. Instead, the insurer sends a total loss offer that looks like it was built for a used luxury sedan with the same badge, not for your actual car. The mileage is wrong, the options are thinly described, the condition notes are generic, and nobody seems to care that your car had the right spec, the right service file, and the kind of market appeal that serious buyers notice immediately.

That frustration is justified. A high-end Porsche, Ferrari, McLaren, Aston Martin, or rare Alfa Romeo doesn't trade like a commuter car. When an adjuster leans on generic valuation software, the result is often a figure that misses how these cars are bought and sold in the market.

If you're in an insurance dispute, especially after a total loss or a repair that leaves a stigma on the vehicle history, the issue usually isn't just damage. It's valuation method. And when the method is wrong, the settlement follows it downhill. The most useful tool many owners overlook is the appraisal clause in their own policy. That clause can force the dispute into an independent valuation process instead of leaving your number trapped inside the carrier's system.

Your Exotic Car Is Not Just Another Used Car

A common pattern goes like this. The owner keeps the car meticulously. Records are organized. Paint is clean. The spec is desirable. Then an accident happens, or the vehicle is declared a total loss, and the settlement offer arrives as if none of that matters.

That disconnect is where most exotic car appraisal disputes begin.

I've seen owners focus first on the wrong question: "Why is the insurer being difficult?" The more useful question is, "What evidence did they use, and was it capable of valuing this kind of car at all?" If the answer is a generic market report built from broad category data, the offer may be low before anyone even starts negotiating.

The emotional part is real, but the fix is technical

To you, the car may represent years of maintenance, selective upgrades, and careful ownership. To the carrier, it may still be sitting in a pricing bucket with loosely similar vehicles. That's why a strong response needs more than indignation. It needs a defensible appraisal built around the actual VIN, actual condition, and actual market behavior.

A weak valuation argument says, "My car is special."

A strong valuation argument says, "These are the comparable sales, these are the condition adjustments, and this is why your report missed the mark."

This often comes up after transport too. If you're moving a collector or exotic vehicle for purchase, sale, or inspection, understanding how to ship an exotic car helps preserve the documentation trail and condition evidence that can matter later in a claim.

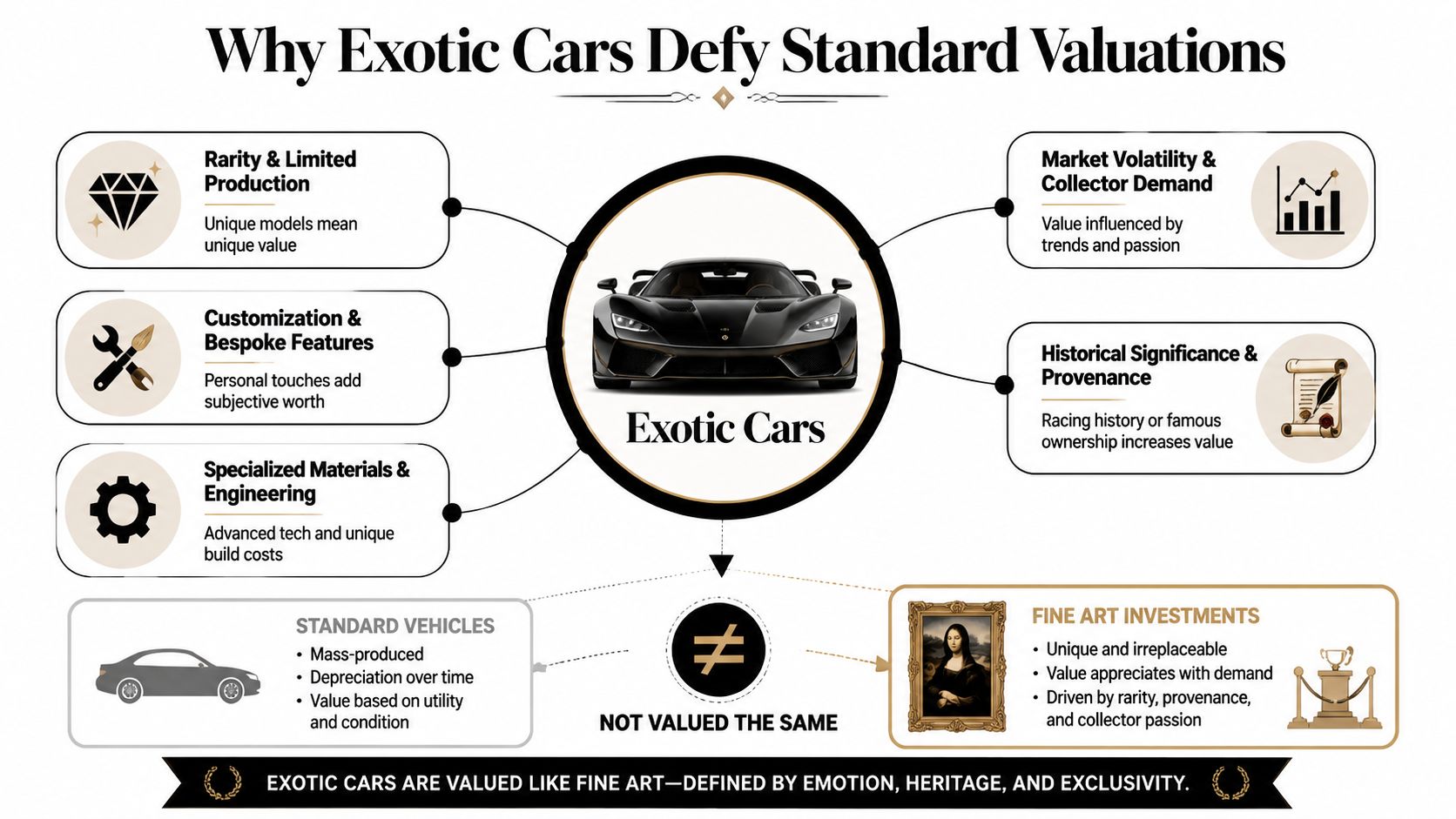

Why Exotic Cars Defy Standard Valuations

Standard valuation tools work best when the market is deep, the vehicles are common, and buyers treat one example much like another. Exotic cars fail all three tests.

A better analogy is real estate. A generic pricing model might estimate a two-bedroom house in a ZIP code fairly well if there are many nearly identical sales. It does poorly when the property is architect-designed, sits on a premium lot, and has features that only a narrow set of buyers understand. Exotic vehicles behave the same way. The badge alone doesn't tell you the value.

What the generic tools miss

For collector vehicles, professional appraisers weigh rarity, condition, history, and modifications, and when only a few thousand, or even just hundreds, of examples exist, small differences in provenance or production numbers can move value substantially. Good appraisal practice also requires documented comparisons with similar vehicles sold in the current market, typically within the last year, as noted in collector-market valuation guidance.

That is far removed from a broad pricing algorithm.

Here are the usual failure points:

- Production rarity: A low-volume trim or special series doesn't behave like the standard model line.

- Option sensitivity: Seats, brakes, carbon packages, factory paint, and trim combinations can change buyer demand sharply.

- History and provenance: Complete service records, prior ownership story, and originality matter more in a thin market.

- Market depth: There may be very few legitimate comparables, so one poor comparable can distort the whole conclusion.

Why this matters in a claim

An insurer may still present a polished-looking report. The format can appear objective. That doesn't mean the input data was adequate.

Practical rule: If the report would value your car the same way regardless of color, provenance, factory options, repair history, or collector demand, it is not built for an exotic car.

The hardest part for owners is that the low number often arrives with institutional confidence. It can feel final. It isn't. If the valuation method is flawed, the dispute is still open, and the right response is a specialized exotic car appraisal, not a louder argument.

The Art and Science of Exotic Valuation

A defensible appraisal isn't guesswork. It's an investigation.

The work starts with the VIN, because exotic values often turn on exact specification. Expert practice for these vehicles is built from VIN-specific, condition-adjusted market evidence, combining exact identification, mileage, documented condition, service history, options, and comparable-market sales to isolate how rarity, color, and trim affect price in a thin market where standard depreciation curves don't apply, as described in this valuation practice overview.

What a serious appraiser actually examines

A proper assignment usually includes several layers of review:

- Identity and configuration: The VIN, factory build information, trim, drivetrain, wheels, brakes, interior, and original equipment all need verification.

- Condition evidence: Paint consistency, panel fit, interior wear, glass, wheels, tires, underbody condition, and signs of prior repair all matter.

- History file: Service invoices, marque-specialist maintenance, ownership chain, and any disclosed damage history can move the number.

- Market comparables: Auction results, dealer offerings, and private-market evidence are filtered for similarity, timing, and credibility.

Not all comparables deserve equal weight. An asking price is not the same as a completed transaction. A base car is not a comp for a heavily optioned example. A repaired car is not a clean-history comp.

What works and what doesn't

What works is a narrow, disciplined set of comparisons. What doesn't is stuffing a report with loosely related listings to create the illusion of market support.

If you're trying to understand how condition ties into fair market value, this guide on calculating fair market value is useful because it shows why the valuation question is broader than a single retail estimate.

Owners can strengthen the file before the inspection too. Presentation doesn't replace market evidence, but it does affect how condition is documented. If the vehicle is still in your possession and you're preparing it for appraisal or sale, practical detailing steps can increase vehicle resale value by making condition easier to verify and photograph accurately.

The strongest appraisal reports read like evidence files, not opinion letters.

What should appear in the report

A quality exotic car appraisal should leave little room for ambiguity. Look for:

| Report element | Why it matters |

|---|---|

| VIN-specific identification | Prevents valuation drift toward a generic trim level |

| Condition analysis | Supports adjustments with observable facts |

| Comparable selection notes | Shows why each comp belongs in the report |

| History and service discussion | Explains market confidence or hesitation |

| Value conclusion with reasoning | Makes the final number defensible in negotiation |

When the report is thin, the insurer has room to dismiss it. When the report is documented carefully, it becomes much harder to ignore.

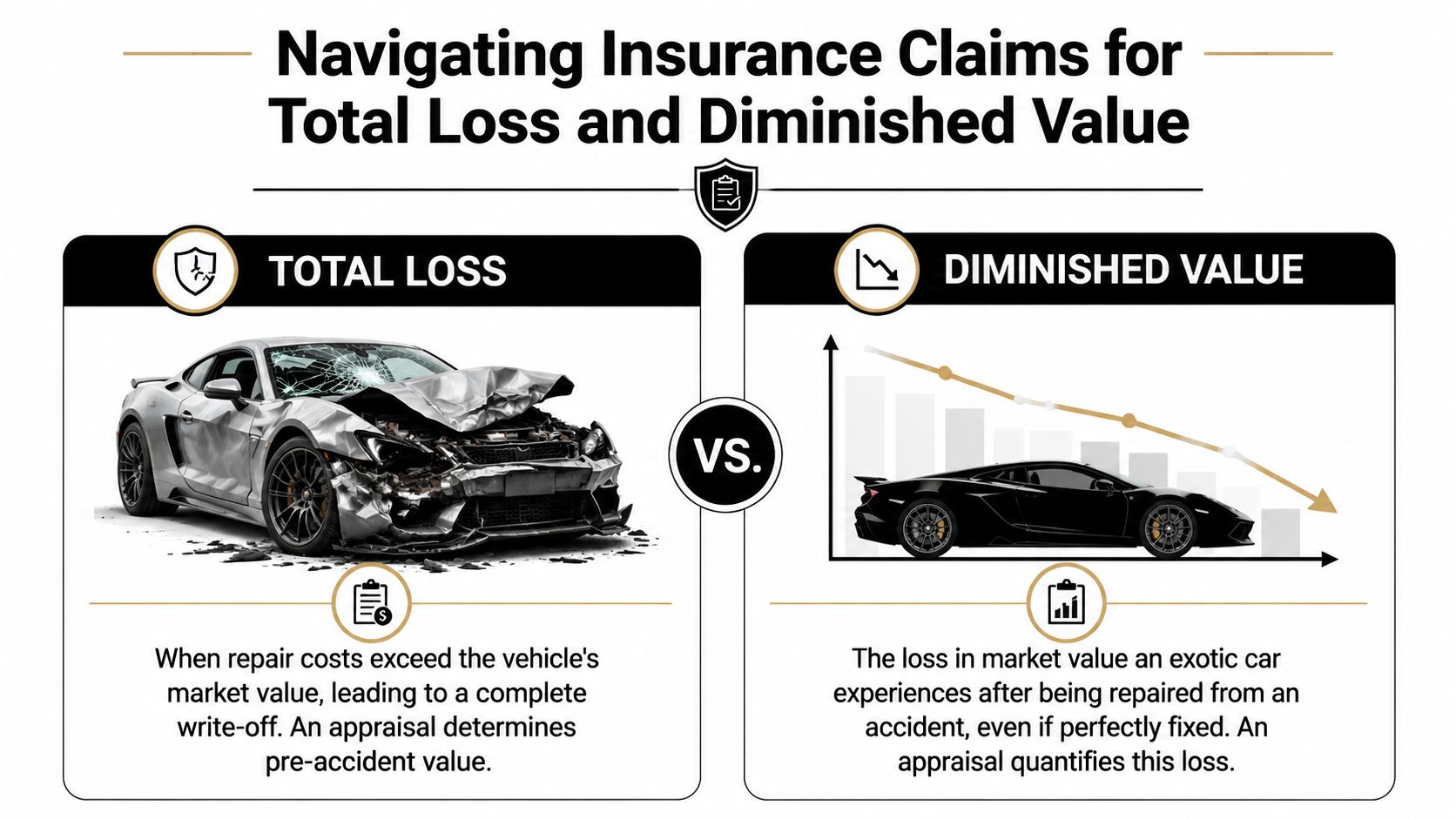

Navigating Insurance Claims for Total Loss and Diminished Value

Two claim types trigger most valuation fights. One is a total loss claim, where the dispute centers on what the car was worth immediately before the accident. The other is a diminished value claim, where the car is repaired but the market still treats it as less desirable because the accident is now part of its history.

The distinction matters because the evidence differs. A total loss appraisal aims at pre-loss fair market value. A diminished value appraisal measures the gap between a comparable clean-history vehicle and your repaired vehicle in the current market.

Why repaired exotics lose value differently

For high-end and exotic vehicles, even small defects can create outsized losses because buyers inspect closely for paint inconsistency and repair evidence. Proper appraisal work compares the repaired vehicle against similar accident-free sales rather than applying a flat percentage reduction, as explained in this discussion of diminished value in the exotic market.

That point is critical. Flat formulas are attractive to insurers because they're simple. The market is not.

A Ferrari with prior paintwork, a McLaren with repair history, or a Porsche GT product with disclosed damage may still be excellent mechanically. Buyers can still discount it because clean-history alternatives exist, and those buyers are often exacting. The loss is not theoretical. It's rooted in how the next buyer shops.

The appraisal clause is your pressure valve

When the insurer won't move off a weak number, the appraisal clause can change the entire posture of the claim. Most auto policies contain some version of this provision. If you and the insurer disagree on value, each side selects an appraiser. Those appraisers try to resolve the amount. If they can't, an umpire may decide the remaining dispute according to the policy process.

Taking valuation out of the normal adjuster loop means you are no longer asking the carrier to please reconsider. You are invoking a contractual mechanism that requires an independent valuation process.

If your policy has an appraisal clause, use it strategically. Don't threaten it casually. Invoke it when you have a real valuation dispute and a qualified appraiser ready to support the number.

When to invoke it

The clause is often most effective when these facts are present:

- The insurer used generic software: The report doesn't capture spec, rarity, or condition correctly.

- Comparable vehicles are weak: The insurer's comps are older, dissimilar, poorly equipped, or from the wrong segment.

- Repair history changed marketability: The carrier treats the repaired car like a clean example.

- Negotiation has stalled: You have supplied records and corrections, and the offer still doesn't reflect the evidence.

Oregon drivers dealing with post-repair stigma can also review legal context around diminished value claims for Oregon drivers to understand how these claims are framed outside the insurer's internal language.

What owners usually get wrong

Many people wait too long. They argue by phone, send screenshots, and assume the adjuster will eventually see reason. Sometimes that happens. Often it doesn't.

The more effective approach is disciplined:

- Gather your service history, build details, photos, and prior condition records.

- Get the insurer's valuation report in full.

- Identify the errors and weak comparables.

- Hire an independent appraiser who understands exotic cars.

- Invoke the appraisal clause if the value dispute remains unresolved.

That step can be the difference between debating a number and forcing a process.

How to Hire a Certified Independent Appraiser

The appraiser you choose can strengthen your claim or weaken it. In an exotic dispute, credentials matter, but relevance matters just as much. A person can have appraisal experience and still be the wrong fit for a low-volume, option-sensitive, collector-adjacent vehicle.

The market context is one reason. A late-2025 industry forecast estimated the U.S. luxury and exotic car market at about $110 billion today and projected it to reach over $180 billion by 2035, with used luxury and exotic sales expected to grow 1.5 times faster than new and the $100,000 to $170,000 band identified as the strongest growth segment. The same forecast said about 80% of buyers browse online weekly or even daily, which is why recent transaction activity matters so much in appraisal work, according to this BCG market forecast.

What to ask before you hire

Don't start with price. Start with fit.

- Ask about vehicle-specific experience: Have they handled your make, model, and market segment before?

- Ask how they source comparables: You want a clear answer about auctions, private sales, dealer data, and adjustment logic.

- Ask whether they work in appraisal-clause disputes: Insurance negotiation requires a report built to withstand pushback.

- Ask what the final report includes: You should expect written reasoning, not a one-line number.

If you're comparing providers in this category, independent car appraiser services can give you a baseline for what a dispute-focused appraisal engagement looks like. In the Pacific Northwest, Total Loss Northwest is one example of a firm that handles diminished value and total loss appraisals and invokes the appraisal clause in valuation disputes.

Documents that help your appraiser

A good appraiser can work around missing pieces, but a complete file provides a stronger basis for their assessment.

Bring or send:

- Service records: Especially marque-specialist work and major maintenance.

- Purchase documents: Window sticker, build sheet, sales invoice, and option list if available.

- Photos from before the loss: These can support pre-accident condition.

- Repair paperwork: If the car was repaired, the estimate, supplement, and final invoice are essential.

- Ownership history and modifications: Factory options and quality modifications need documentation.

This video gives a useful visual overview of what to look for in the appraisal process:

Red flags that should make you walk away

Some warning signs are obvious. Others are subtle.

| Red flag | Why it's a problem |

|---|---|

| They rely on book values alone | Exotic claims need market-specific evidence |

| They can't explain comparable adjustments | Weak methodology won't survive insurer scrutiny |

| They promise a result before reviewing records | That's advocacy theater, not appraisal work |

| They avoid issuing a detailed written report | You need documentation, not just a verbal opinion |

Choose the appraiser who can explain the process calmly and precisely. In insurance disputes, clarity beats bravado.

Special Considerations for Oregon and Washington Owners

Owners in Oregon and Washington face the same core problem as everyone else: insurers often begin with valuation systems that flatten the unique features of a high-value vehicle. But the local claim environment adds a practical layer. Regional buying patterns, transport costs, specialty dealer presence, and the availability of comparable inventory can all affect how replacement-market evidence is assembled.

Why local knowledge matters here

In the Pacific Northwest, appraisers often need to look beyond the nearest mainstream dealer network and into specialty channels. The issue isn't distance alone. It's whether the comparable reflects the kind of car your market recognizes as a substitute.

That becomes even more important after a repair. The local claim strategy should account for how diminished value is documented and negotiated in the region. If your vehicle was repaired and now carries a market stigma, this overview of diminished value auto claims is a useful starting point for understanding the claim path.

The appraisal clause is especially useful when local inventory is thin

Oregon and Washington owners often run into insurer reports built from questionable substitutes pulled from wider databases. When the local market for your exact vehicle is thin, a disciplined independent appraisal matters more, not less. The appraiser has to justify why a given comp belongs, why another should be rejected, and how condition and history affect the number in a market where every example isn't interchangeable.

If you're in either state, don't let the carrier frame the dispute as a simple pricing disagreement. For an exotic, it's usually a data-quality problem first.

Exotic Car Appraisal FAQs

How long does an exotic car appraisal take

It depends on the vehicle, the records available, and whether the case involves total loss, diminished value, or an appraisal-clause dispute. A straightforward file moves faster than a claim with disputed repair quality, sparse comparables, or missing option documentation. The key variable isn't speed. It's whether the appraiser has enough evidence to support the conclusion.

Do I need an appraisal if the insurer already sent a valuation report

Usually yes, if the report is generic or the comps don't resemble your car closely. An insurer's report may be useful as a starting point because it shows what they relied on. It is not the final word if the methodology is weak.

What if my repaired exotic looks perfect

That doesn't end the valuation issue. A major challenge in this space is that repaired exotics sit in a thin market where conventional valuation tools are weakest. Generic software often can't determine how much value is lost when rarity, provenance, and prior damage interact, especially when transaction data comes from volatile online auctions and specialty marketplaces, as noted in this discussion of the appraisal gap for repaired specialty vehicles.

What happens if my appraiser and the insurance company's appraiser disagree

That is exactly why the appraisal clause exists. In many policies, if the two appraisers can't agree, they select an umpire to resolve the remaining dispute. The process varies by policy language, but the basic point is the same: value doesn't stay stuck in a circular argument between you and the adjuster.

Can I use dealer listings as proof of value

Dealer listings can help, but they are not enough by themselves. Asking prices aren't completed sales, and the listing may omit condition details or hidden history. Strong appraisals use listings carefully and test them against more reliable market evidence.

Is a diminished value claim worth pursuing on an exotic

Often yes, because exotic buyers inspect history and finish quality much more critically than mainstream used-car buyers. Even after proper repairs, the accident disclosure can change who is willing to buy the car and what they are willing to pay.

If you're dealing with a low total loss offer or a repaired exotic that no longer commands clean-market money, Total Loss Northwest handles independent appraisals for Oregon and Washington owners and uses the appraisal clause process to challenge insurer valuations with documented market evidence.