The adjuster calls. Your imported Nissan has been declared a total loss. Then comes the number.

It sounds like they priced an old commuter, not the right-hand-drive car you spent years sourcing, maintaining, and protecting. If your R32 GT-R, Silvia, Chaser, or RX-7 is being valued like a vaguely similar U.S. market car, you're not dealing with a small clerical issue. You're dealing with a valuation method that was never built for this kind of vehicle.

That matters most right after a loss, when owners are exhausted and tempted to argue from emotion. Emotion won't move the claim. Documentation will. A proper JDM vehicle appraisal gives you a disciplined way to prove identity, condition, rarity, and market position, then use that evidence to push back on a weak total loss offer.

The Insurance Lowball on Your Imported Treasure

The usual scenario is predictable. Your insurer runs the claim through a standard valuation system, searches for whatever its database recognizes, and produces a settlement that feels detached from reality. A U.S. market Nissan gets treated as a substitute for a Japanese-market Nissan. A specialty car gets treated as transportation. A documented enthusiast car gets reduced to age and mileage.

That gap exists because JDM imports sit outside the assumptions behind mass-market pricing tools. Kelley Blue Book notes that JDM vehicles can be imported to the United States only if they're at least 25 years old, and that these vehicles are typically right-hand drive and use a frame number rather than a VIN. Those details aren't trivia. They directly affect identity verification, import eligibility, and authenticity, which are core parts of any credible value opinion in a claim dispute. See KBB's overview of JDM vehicles and the 25-year import rule.

Why the first offer often misses the point

A total loss adjuster usually wants speed, consistency, and internal defensibility. That sounds reasonable until the vehicle falls outside their normal universe. Your car may have a chassis code the software doesn't recognize well, factory trim distinctions the adjuster doesn't understand, and an import history that never shows up in mainstream databases.

For an owner, the experience feels personal because it is personal. You know what the car was. The insurer only knows what the system can classify.

Practical rule: If the offer reads like the car was valued as a generic used vehicle, treat the first number as a position in a negotiation, not the final answer.

What changes the claim

An independent appraisal changes the conversation from opinion to evidence. Instead of saying, "This car is worth more because it's special," you're saying, "Here is the chassis identity, import history, condition record, modification file, and comparable market support."

That distinction matters in a dispute. Insurance companies don't pay more because an owner is passionate. They pay more when the low offer becomes hard to defend.

When the vehicle is a legitimate imported JDM car, the appraisal has to establish the basics first:

- Identity matters because frame number verification is part of proving what the car is.

- Import status matters because age and eligibility affect whether the vehicle belongs in a normal domestic pricing bucket at all.

- Condition matters because collector-oriented cars can swing substantially based on originality, upkeep, and modifications.

If your prized import was just totaled, don't waste your best advantage on a phone argument. Build a record the insurer has to answer.

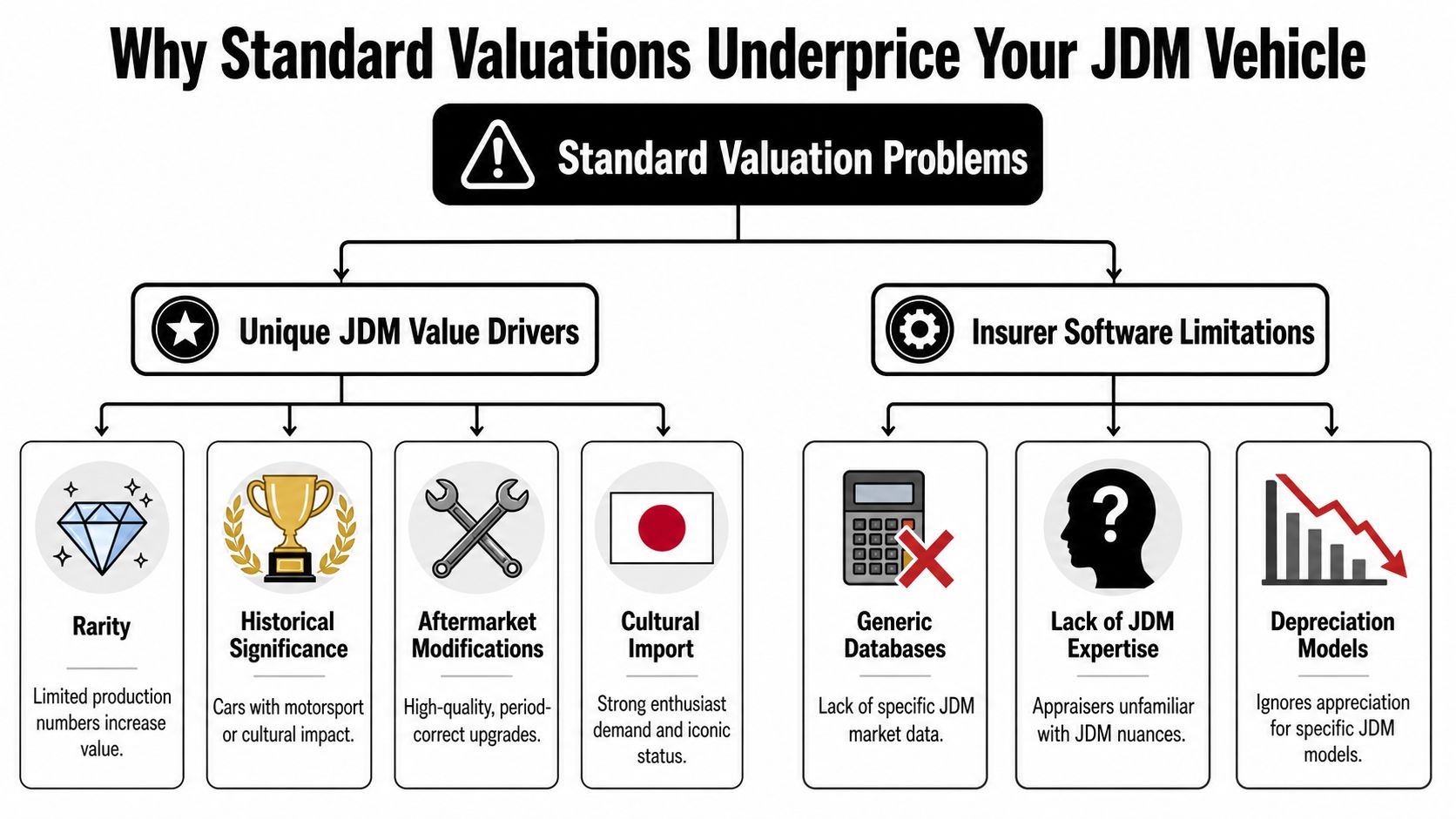

Why Standard Valuations Underprice Your JDM Vehicle

The core problem isn't that insurers are always acting in bad faith. The bigger problem is that their standard process is built for interchangeable vehicles with broad data coverage. JDM cars aren't interchangeable, and their values don't behave like ordinary used cars.

A good appraiser starts by deciding what kind of asset your car is. That's not semantics. Specialized valuation guidance notes that JDM cars often need insurance valuations because they sit between transportation and a collectible asset, and a real challenge is deciding when enthusiast demand spikes are no longer defensible without condition-based normalization. See this discussion of specialized insurance valuations for JDM cars.

Transportation value versus specialty asset value

If the insurer treats your car as transportation, the valuation leans toward age, mileage, and generic market averages. That method works reasonably well for common vehicles.

It breaks down on imported JDM metal because buyers don't shop these cars the same way. They care about chassis code, trim, originality, color, import paperwork, maintenance file, and whether the modifications improve desirability or narrow the buyer pool.

Here's how those two approaches differ:

| Valuation lens | What it emphasizes | What it tends to miss |

|---|---|---|

| Transportation | Generic age, mileage, condition bands, local used-car averages | Rare trims, enthusiast demand, right-hand-drive market, import identity |

| Collector or specialty asset | Authenticity, comparables, originality, provenance, market acceptance of modifications | It can still overstate value if hype isn't normalized |

That last point matters. Not every trend in enthusiast circles should flow straight into an insurance settlement. A serious appraisal has to sort durable market value from temporary excitement.

The details that software doesn't handle well

Standard systems often struggle with JDM cars for reasons that owners can identify immediately:

- Chassis-specific rarity matters more than model name alone.

- Import and compliance history affects buyer confidence.

- Originality versus modification quality changes desirability in different ways.

- Right-hand-drive status can either support collector value or narrow a general-buyer audience.

- Maintenance records often matter more on older imports than a generic book value suggests.

Modification analysis is where many claims go sideways. Some upgrades support value because they're period-correct, well-documented, and accepted by the market. Others don't. If you're preparing to explain that difference, a plain-language resource on aftermarket vs OEM parts explained can help owners frame why original-equipment parts and quality aftermarket parts aren't interchangeable in an appraisal dispute.

A weak total loss valuation usually isn't one big mistake. It's a stack of smaller mistakes that all lean downward.

Where owners get trapped

The insurer's number often looks official because it came from a report. That doesn't mean the report is persuasive. It may still rely on the wrong comparable pool, the wrong vehicle identity, or the wrong asset category.

If you want to understand how insurer-generated reports can fall short in a total loss dispute, review this breakdown of CCC auto valuation issues. The point isn't to reject every insurer report out of hand. The point is to test whether the method fits the vehicle.

For JDM claims, generic averages are often the enemy. They flatten meaningful distinctions. Once that happens, the insurer isn't valuing your car. It's valuing the nearest thing its software can digest.

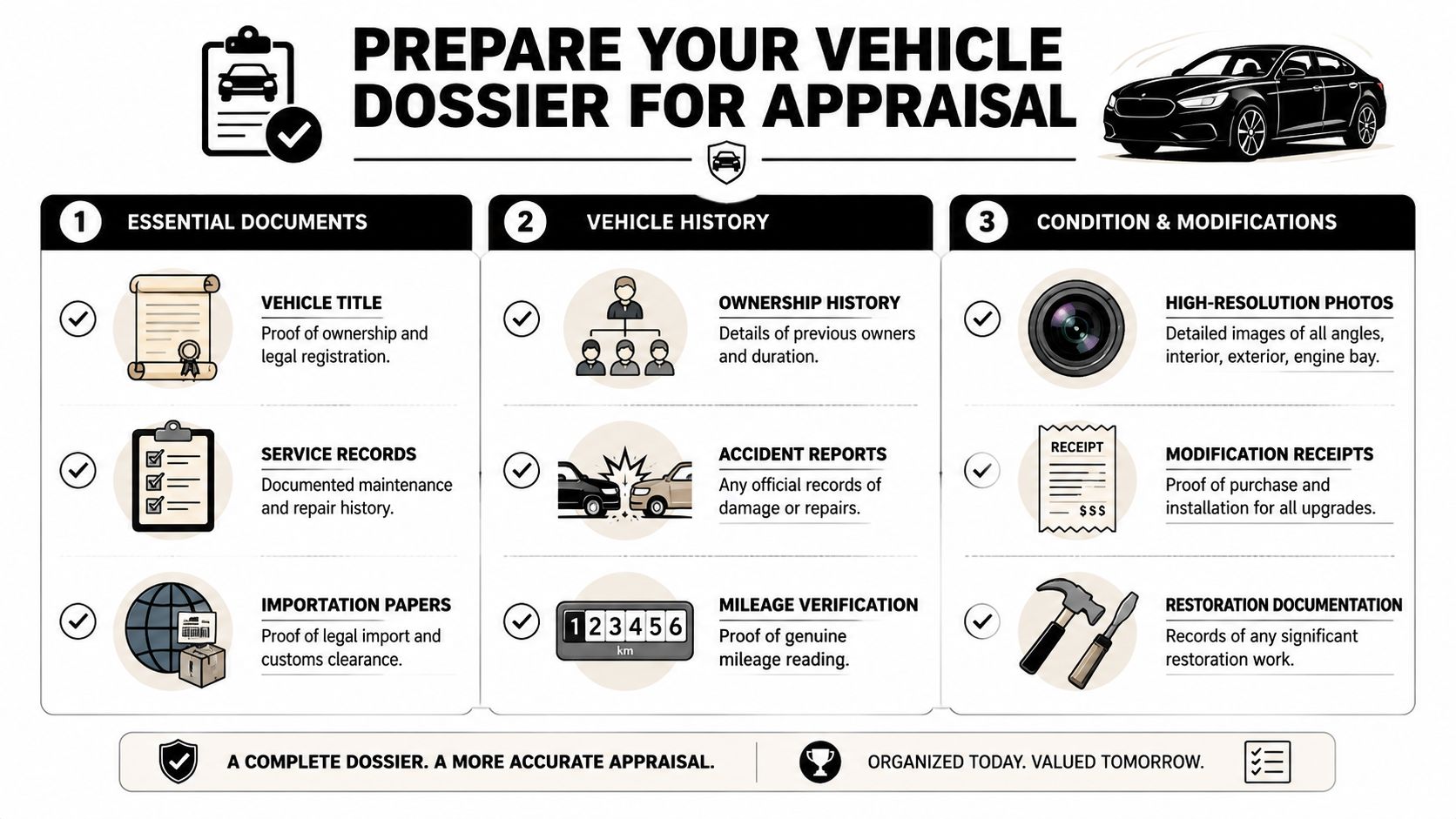

Prepare Your Vehicle Dossier for Appraisal

A strong appraisal starts before the appraiser sees the car. It starts with the file you hand over.

Owners who win these disputes usually do one thing well. They organize the vehicle's story so the appraiser doesn't have to guess. That means proving what the car is, how it got here, how it was maintained, and what was done to it.

Build the claim file before anyone asks for it

Don't wait for the adjuster to request documents one at a time. Assemble the dossier in a single folder, digital and physical if possible.

Include the basics first:

- Title and registration. These establish legal ownership and current registration status.

- Import paperwork. Customs entry forms, export documents, and any related import records help prove lawful importation and identity.

- Frame number documentation. If the car uses a frame number instead of a conventional VIN, keep photos and matching paperwork together.

- Service history. Maintenance invoices show care, consistency, and major mechanical work.

- Pre-loss photos. Good photos often become the clearest proof of condition.

- Modification receipts. Parts invoices and installation records help separate real value-added work from unsupported owner claims.

The records that carry the most weight

Not all paperwork does the same job. Some documents prove identity. Some prove condition. Some prove that money was spent intelligently, not just spent.

A simple way to think about it:

| Document type | Why it matters in a dispute |

|---|---|

| Import records | Shows the car's legal path into the U.S. and supports authenticity |

| Maintenance invoices | Supports condition, upkeep, and major service history |

| Parts receipts | Helps the appraiser evaluate modifications individually |

| Photographs | Locks in pre-loss condition and presentation |

| Ownership history | Gives context for continuity of care |

Bring documents that prove facts, not just passion. "I know what I have" isn't evidence. Receipts, photos, and records are.

Organize modifications with discipline

Many owners lose ground. They submit a pile of invoices and assume every part increased value. That's not how the market works.

Create a separate modification summary with part names, brands, install dates if known, and whether the original parts are still available. If you own a Japanese or Acura performance car and want a good example of how enthusiast owners document model-specific details and parts context, this essential guide for TL Type S owners shows the kind of component-level thinking that helps during valuation.

Your appraiser's job gets much easier when the file is clean. And when the file is clean, the insurer has fewer ways to dismiss the result as speculative.

How to Find a Qualified JDM Appraiser

A licensed appraiser isn't automatically a good JDM appraiser. Those are different things.

If your car is right-hand-drive, imported, modified, or collector-leaning, you need someone who knows how those factors affect marketability and price. A generalist may still produce a report, but a report isn't useful just because it exists. It has to survive scrutiny from an insurer that wants to minimize payout.

A neutral JDM appraisal benchmark is straightforward. The inspection should be in person, should last 30 to 60 minutes minimum, should capture 40 to 60+ photos, and the final product should be a multi-page signed report tying condition, rarity, and modifications to market value. One-page checkbox estimates are often too thin for insurance negotiations. See the full discussion of what a defensible JDM appraisal should include.

Questions that separate specialists from tourists

When you interview an appraiser, skip broad questions like "Do you do classics?" Ask questions that expose process.

Use prompts like these:

- How do you verify chassis identity on a JDM import?

- How do you select comparables for a right-hand-drive vehicle?

- How do you handle documented modifications that may help value in one market but hurt it in another?

- What does your final report include besides the number?

- Have you prepared reports used in total loss or insurance disputes?

The answers should sound methodical, not performative. If the appraiser can't explain their comparable selection process in plain English, that's a problem.

What the inspection should look like

A proper inspection is detailed and a bit tedious. That's a good sign.

The appraiser should examine exterior condition, interior wear, engine bay presentation, undercarriage condition, identity tags, and any non-OEM equipment that affects value. They should also ask for records and verify that the paperwork matches the vehicle.

A serious process usually includes:

- Identity review of chassis code, trim, and paperwork

- Condition documentation through a full photo set

- Modification analysis with attention to quality and reversibility

- Comparable research that goes beyond broad market averages

- Written reasoning that shows how the appraiser reached the conclusion

Red flags that should end the call

If you hear any of the following, keep looking:

| Red flag | Why it matters |

|---|---|

| "I can give you a number from photos alone." | Remote review may have limits, especially for undercarriage, prior repairs, and identity details |

| "All old imports are about the same." | That mindset destroys appraisal accuracy |

| "I use one standard classic-car form for everything." | JDM valuation often requires model- and market-specific analysis |

| "The insurer probably won't care about modifications." | The insurer may challenge them, which is exactly why they must be analyzed carefully |

If you're comparing options, this overview of an independent car appraiser is useful for understanding why independence matters when the insurance company already has a financial incentive to keep the number down.

Good appraisers don't promise a high value. They promise a defensible one. That's who you want in a disputed total loss.

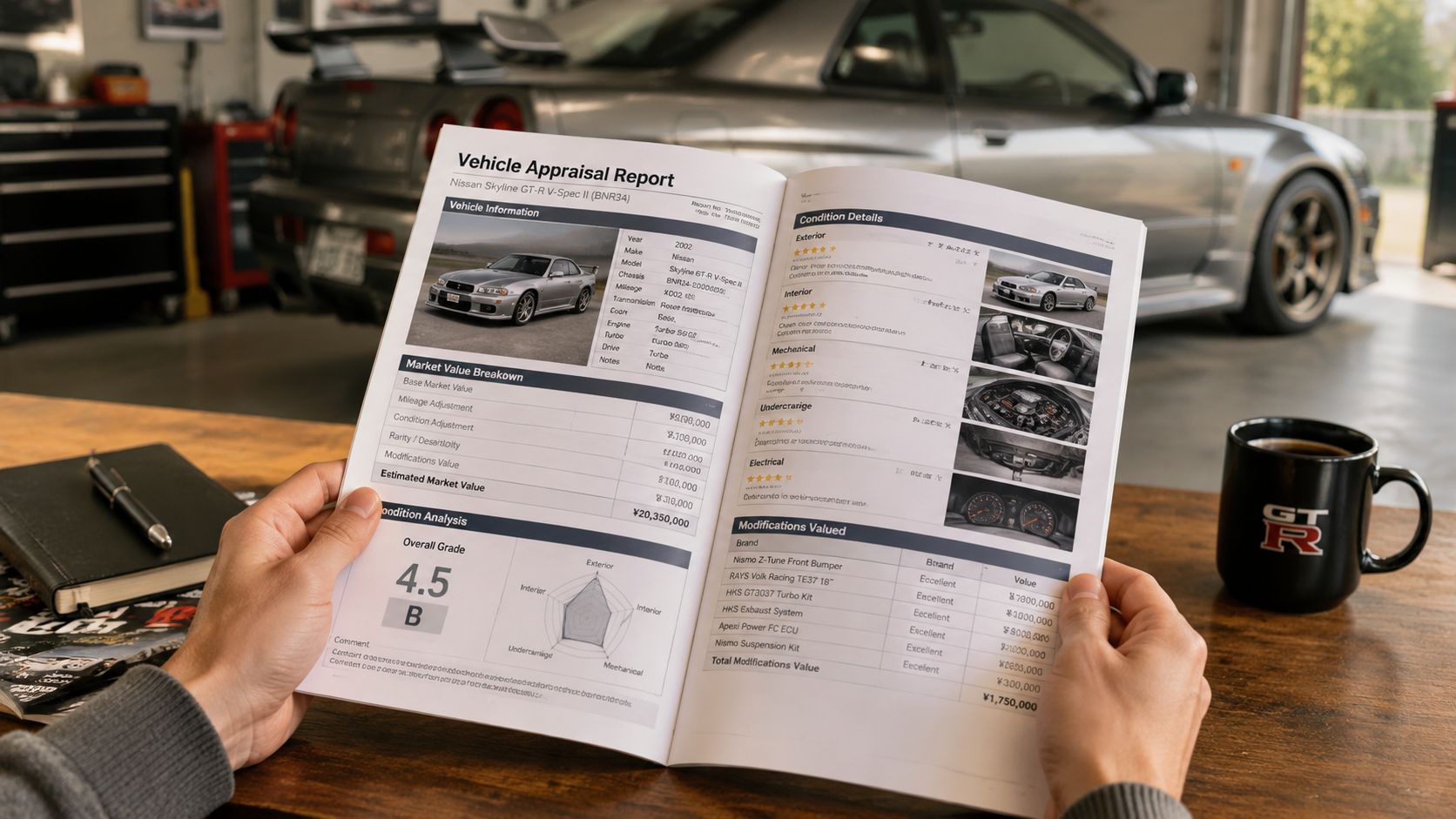

Decoding Your Professional JDM Appraisal Report

Once the report arrives, most owners flip to the final number first. That's understandable, but it's not the most important page.

The strength of a JDM vehicle appraisal is in the logic. If the insurer pushes back, the report needs to show how the appraiser identified the vehicle, built a base value, adjusted for meaningful differences, and landed on a conclusion that can be defended line by line.

A strong method separates base vehicle value from value-added modifiers such as originality, documented maintenance, and rare trim. That granular approach matters because broad market averages can understate uncommon cars and overstate heavily modified ones. See this discussion of consistent appraisal process and granular vehicle data.

What the appraiser is actually doing

Think of the report as an argument built from layers of evidence.

First comes identity. The report should specify the exact chassis and trim being appraised. Then comes condition, including both strengths and weaknesses. Then come comparables and adjustments. Finally, the appraiser explains why the final conclusion is more reliable than a generic pricing output.

Most strong reports contain these components:

- Vehicle identification with chassis-specific details

- Condition narrative covering exterior, interior, mechanical presentation, and any prior repair indicators

- Comparable market discussion with reasons the selected examples are relevant

- Adjustment analysis for mileage, originality, maintenance, rare trim, and modifications

- Signed reconciliation showing how the appraiser weighed all inputs

Base value versus modifiers

This is the part owners need to understand before challenging an adjuster.

The base value reflects the market position of the underlying vehicle before individual strengths and weaknesses are layered in. Modifiers come next. Some support value. Some reduce it. The appraiser's job is to explain each one rather than bury them in a single unexplained number.

A clean way to read that analysis looks like this:

| Report element | What it means |

|---|---|

| Base value | The starting point for the model, trim, and market position |

| Originality adjustment | Whether factory-correct features support desirability |

| Maintenance adjustment | Whether documented upkeep improves buyer confidence |

| Rare trim or option adjustment | Whether specific factory attributes strengthen the market position |

| Modification adjustment | Whether upgrades are market-accepted, neutral, or value-limiting |

If the report can't explain why a modification helped, hurt, or had no effect, the insurer will attack that gap.

What owners should check before submitting the report

Read the report like opposing counsel would. Look for missing facts, unclear assumptions, or unsupported conclusions.

Confirm these points:

- The identity details are correct. Chassis code, trim, transmission, and market specification should match the car.

- The condition narrative is balanced. Reports that sound like sales ads lose credibility.

- The modifications are analyzed individually. A lump-sum treatment is weaker than part-by-part reasoning.

- The final conclusion is reconciled. The report should explain why the appraiser favored certain evidence over other evidence.

A professional report isn't valuable because it says a big number. It's valuable because it gives you a number the insurer has to work to reject.

Leveraging Your Appraisal in Insurance Negotiations

Most owners make the same mistake after getting a good appraisal. They email it over and wait.

That rarely works. A strong report is an advantage, but only if you use it strategically. Insurance total loss disputes are adversarial. The carrier has its number, its process, and its preferred software. You need a process of your own.

Use the appraisal clause early, not as a last gasp

The most important strategic move in many policies is the appraisal clause. When available, it gives you a formal path to challenge a disputed value through an independent appraisal process instead of letting the insurer's internal method control the outcome.

Owners wait too long to invoke it because they think they need to "negotiate nicely" first. Usually, that only burns time while the insurer anchors the claim around its low number.

"If the dispute is about value, treat it like a valuation dispute immediately."

That doesn't mean you need to be hostile. It means you need to be precise. Put the insurer on notice that you dispute the amount of loss and that you are prepared to proceed under the appraisal provision in the policy if the matter isn't resolved.

How to present the dispute

Keep your communication short, factual, and organized. Don't write a manifesto.

A practical structure looks like this:

- State the disagreement clearly. Say you dispute the insurer's total loss valuation.

- Identify the basis. Note that the subject vehicle is an imported JDM vehicle whose market position isn't reflected by generic valuation tools.

- Attach the appraisal and supporting records. Include the report, key records, and any pre-loss photos.

- Request reconsideration within the claim. Give the adjuster a chance to review the evidence.

- Invoke the appraisal clause if needed. If the insurer stands by the low offer, escalate formally.

Sample language:

I dispute the insurer's valuation of my vehicle. The settlement does not reflect the vehicle's identity, condition, import status, and documented market position as established in the attached independent appraisal. Please review the enclosed report and advise whether the carrier will revise its valuation. If not, I request that we proceed under the policy's appraisal provision to resolve the dispute over the amount of loss.

What helps in negotiation and what doesn't

Owners often ask what moves the needle. In practice:

- Useful. A coherent appraisal, organized records, and a calm written position.

- Less useful. Screenshot compilations with no context, forum arguments, emotional comparisons, and undocumented claims about rarity.

- Very useful. A formal invocation of the policy process when the carrier won't move voluntarily.

If you need a practical overview of tactics that work in this stage, review these steps on how to negotiate with an insurance adjuster.

Stay firm on the right issue

The dispute isn't whether you loved the car. The dispute is whether the carrier can defend its number against better evidence.

That framing keeps you focused. It also keeps the adjuster from pulling the conversation into side issues. If your report is sound, your records are organized, and the carrier's number is still based on a weaker method, invoking the appraisal clause is often the cleanest way to force a serious review.

A fair payout on a JDM total loss usually doesn't happen because the insurer suddenly "gets it." It happens because the owner stops arguing from frustration and starts arguing from proof.

If you're fighting a low total loss offer on an imported, collector, or modified vehicle, Total Loss Northwest helps owners challenge weak insurance valuations with certified independent appraisals. They specialize in total loss and diminished value disputes, and they invoke the appraisal clause to take biased valuation software out of the driver's seat.