The call usually goes the same way. Your Skyline GT-R has been hit, or the insurer has declared it a total loss, and the adjuster reads out a number that sounds like they priced a generic old Nissan instead of one of the most scrutinized Japanese performance cars in the collector market.

If you're in that spot right now, your frustration is justified. A Skyline owner can spend years preserving originality, documenting import history, collecting factory parts, and maintaining a car that trades in a specialist market. Then one low-ball valuation tries to flatten all of that into a database entry.

That disconnect is the whole fight. A fair settlement on a GT-R doesn't come from saying, “This car is special.” It comes from proving, with documents and market evidence, exactly why the insurer's number is wrong and exactly what your car is worth on the market.

The Nightmare Scenario for Every GT-R Owner

The worst part isn't always the crash. It's the first settlement offer.

An owner gets rear-ended in traffic. The body shop says the structure may be compromised, or the insurer leans toward total loss because repair costs are climbing. A few days later, the valuation report arrives. The comparable vehicles are wrong, the trim is vague, the import status is barely addressed, and the modifications are either ignored or treated as a liability without context.

That happens because the default insurance process is built for mainstream vehicles. It works tolerably well for common daily drivers with deep domestic transaction data. It breaks down fast when the car is a Skyline GT-R, especially an imported one with rare factory specification, documented provenance, or enthusiast-grade upgrades.

The owner usually sees three problems at once:

- The wrong vehicle baseline. The report treats the car like a broad Nissan coupe instead of a specific GT-R generation and trim.

- The wrong market. It leans on generic valuation channels instead of enthusiast and collector transactions.

- The wrong evidence standard. It expects the owner to accept a number without proving how that number was built.

A low offer isn't proof that your GT-R isn't worth more. It's often proof that no one has forced the insurer to value it correctly.

I've seen owners make the same mistake in this moment. They argue from emotion first. They talk about rarity, sentimental value, and how hard the car was to find. All of that may be true, but it won't move a claim unless it gets converted into evidence: import papers, trim verification, service history, photos, receipts, sale comparables, and a report from someone who knows what a Skyline is in the market that buys them.

You don't win this by being louder. You win it by making the insurer's number impossible to defend.

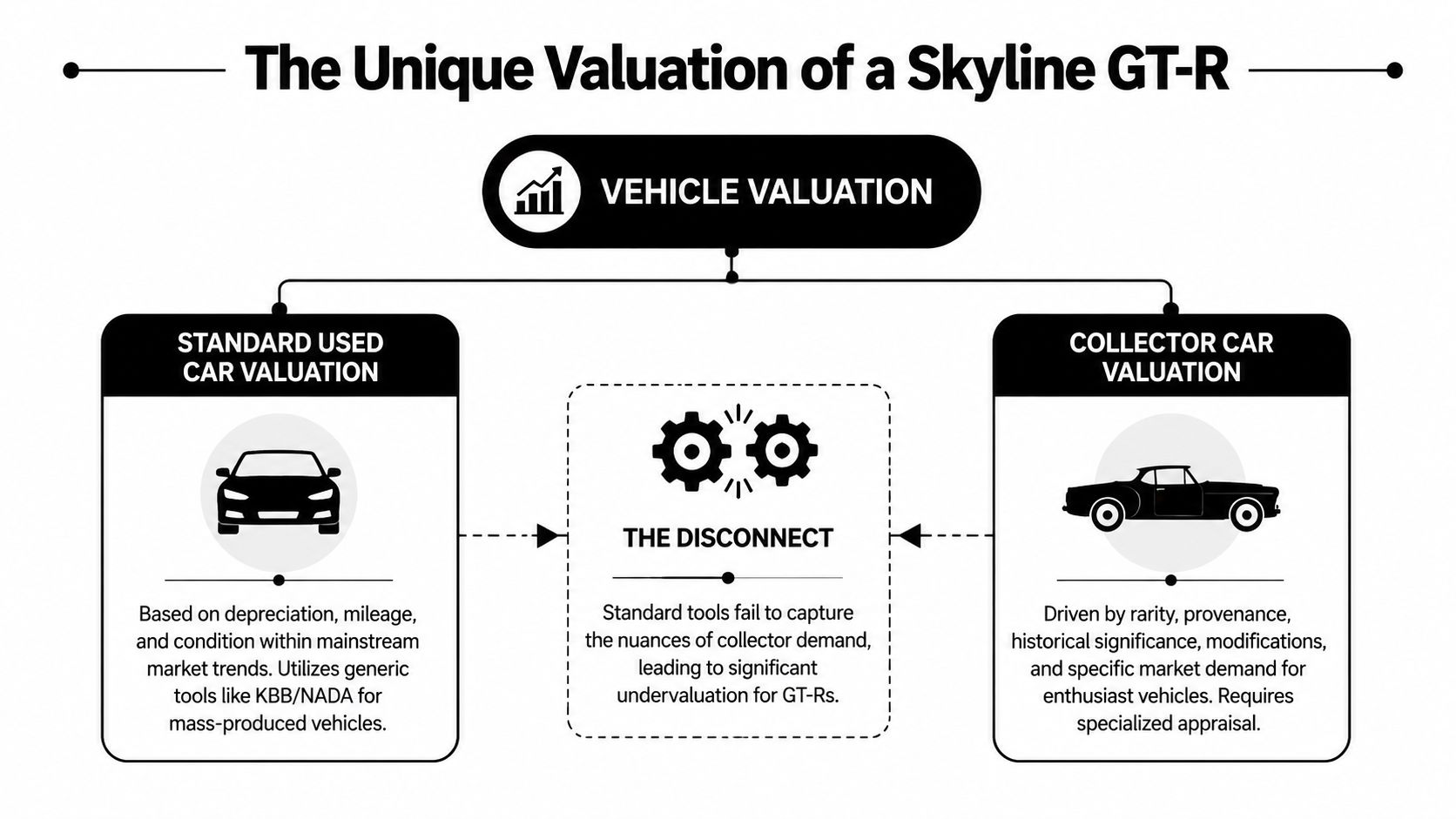

Why Your Skyline GT-R Is Not Just Another Used Car

A low-ball settlement usually starts with a bad category match. The insurer drops your Skyline GT-R into a standard used-car system, and the report starts pulling depreciation logic from ordinary Nissan sales instead of collector-grade GT-R transactions. Once that happens, the burden shifts to the owner to prove why the car belongs in a different market.

The market reality standard tools miss

A Skyline GT-R trades on factors that ordinary valuation systems either flatten or miss completely. Legal import eligibility matters. Verified trim matters. Factory-original components matter. A documented grade auction sheet, export certificate, service records, and clear pre-loss photos can shift value in a way a generic report will never capture.

The R34 proves the point. JDM Buy Sell's R34 market overview discusses how U.S. import eligibility changed buyer demand and also notes that just 11,578 R34 GT-Rs were built globally. That is not normal used-car supply. It is constrained collector supply, and buyers pay accordingly when the car is real, documented, and correctly represented.

That difference shows up fast in a claim file. If the insurer sees "1999 Nissan coupe," you lose ground. If your file shows GT-R chassis verification, subtype, import documents, condition photos, and market comparables for the same specification, the discussion changes.

Why insurer language can mislead owners

Terms like actual cash value sound precise, but the result depends on what inputs the insurer used and whether those inputs reflect the market for your car. For a Skyline GT-R, that means asking a hard question early: did the valuation use true GT-R comparables, or did it use broad substitutes that happen to share a badge or body style?

For a clear baseline, review how fair market value is defined in an auto claim. The practical takeaway is simple. Fair market value is tied to what a willing buyer would pay for that specific vehicle, in that specification, in its real buying market. If the valuation ignores provenance, trim, legality, or documented condition, it is incomplete.

Parts quality also matters more than many adjusters admit. If your car has been repaired, maintained, or restored with correct components, document it. The difference between OEM, period-correct parts, and generic replacements can affect both desirability and value, and the Carmedics Autowerks car parts guide is a useful reference when you need to explain that distinction in plain terms.

The claim turns on proof, not reputation. A Skyline's status helps only when you back it with records.

What this means for your claim

A proper Skyline GT-R appraisal is not just a number on letterhead. It is a documented argument.

The file should show exactly what the car is, why this example commands stronger money than a generic comp, and how that conclusion was reached. In practice, that means gathering the documents an insurer can verify and a buyer would care about:

- Identity records. VIN or chassis verification, trim confirmation, and market-of-origin paperwork.

- Ownership and import file. Export certificate, customs entry documents, auction sheet if available, and title history.

- Condition evidence. Pre-loss photos, underbody photos, paint meter readings if you have them, service history, and inspection notes.

- Parts and modification records. Receipts, installer invoices, dyno sheets, and evidence showing whether changes improve or hurt market appeal.

- Comparable sales. Same generation, same subtype, similar condition, similar originality, and ideally the same legal-market context.

Without that record, the insurer gets to define the car for you. With it, they have to answer your evidence.

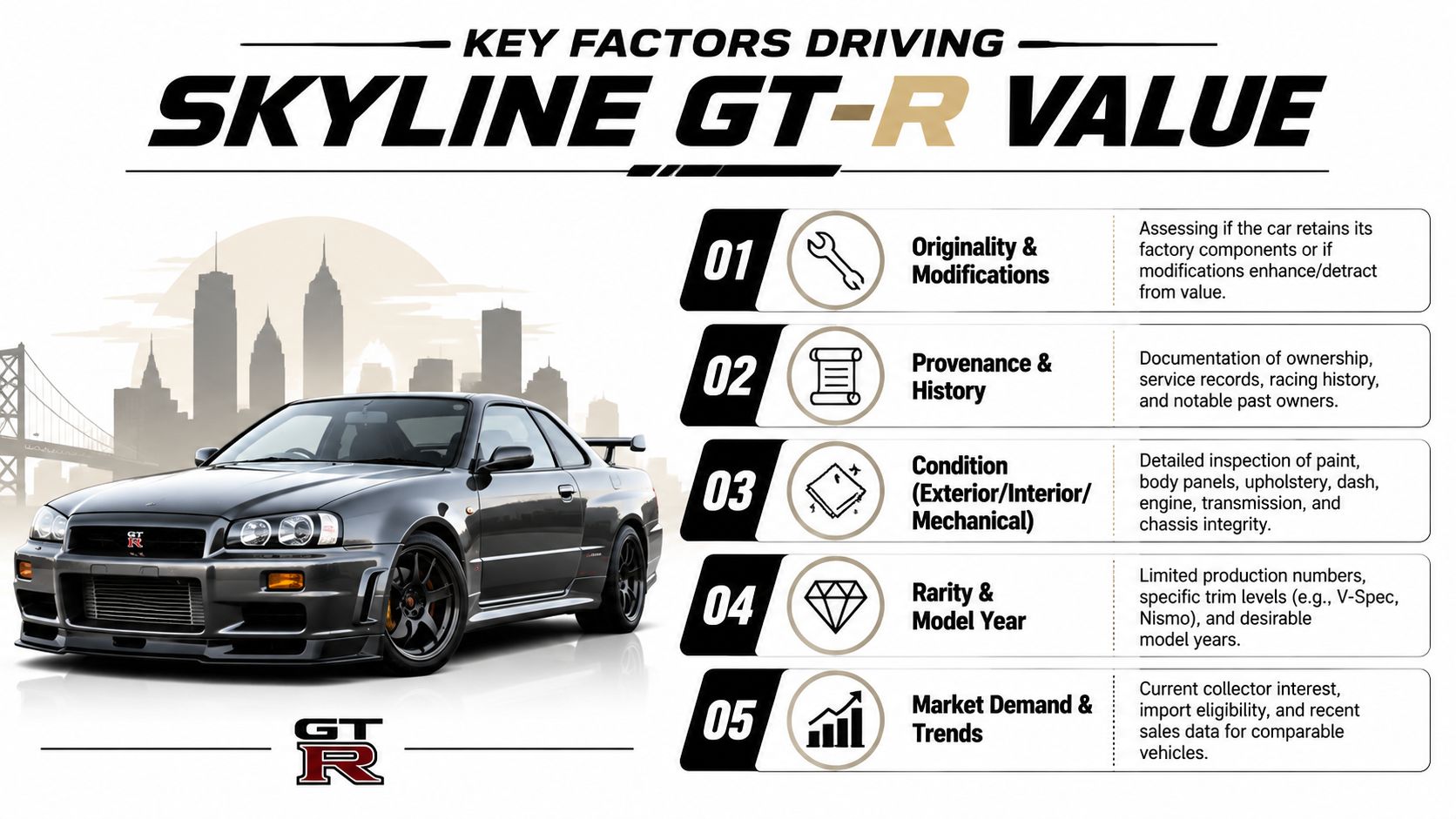

Decoding the Key Drivers of Your GT-Rs Value

A Skyline appraisal rises or falls on specificity. If the report cannot prove exactly which GT-R you owned, how it was equipped, and why buyers pay more for that configuration, the insurer has room to price it like a generic import.

Specification decides the market lane

Start with identity. I want the file to answer a simple question without hesitation. What is this car, down to the exact subtype?

For an R34 GT-R, that means confirming the chassis code and engine designation and tying both to the car in front of you. The RB26DETT 2.6L twin-turbo inline-six was officially rated at 280 PS under Japan's voluntary agreement, and period reporting and enthusiast market references have long noted that actual output was commonly understood to be higher, which is why brochure numbers alone are a poor valuation shortcut, as outlined in JDM Buy Sell's Skyline technical guide.

That detail affects comp selection immediately. A report that says "Skyline coupe" or even "GT-R" without sorting out V-Spec, M-Spec, Nür, Series changes, or market-specific equipment is leaving money on the table.

The evidence should include:

- VIN and chassis verification that confirms the exact GT-R subtype.

- Engine documentation showing whether the RB26DETT is original to the car.

- Factory equipment notes covering AWD hardware, trim-specific features, and option packages.

- Photos of identifying tags and stampings so the insurer cannot claim the appraiser relied on owner statements alone.

Originality versus modification quality

Modifications change value in different directions. The deciding factor is not whether the car was modified. It is whether the parts, workmanship, and documentation support the car's market position.

Poorly installed aftermarket parts, missing factory take-offs, unknown tunes, and vague seller descriptions usually hurt. Well-documented upgrades from respected brands can help, but only if you can prove what was installed, who installed it, when it was done, and how buyers in the GT-R market respond to those changes.

If you're sorting through receipts and trying to explain the difference between factory and replacement components, Carmedics Autowerks car parts guide is a useful plain-language reference. In a GT-R claim, that distinction matters because "modified" is too broad to mean anything by itself. The question is whether the parts strengthen the car's identity in the market or weaken it.

Practical rule: If a modification cannot be documented, photographed, and connected to recognized buyer demand, do not expect it to raise the settlement.

Condition has to be broken into parts

A Skyline does not get one blanket condition grade if you want a number you can defend. Paint, structure, interior, driveline, underside, and originality need separate treatment because each one affects market confidence differently.

Look for evidence in each category:

- Exterior condition. Paint quality, panel fit, corrosion, and signs of prior repair.

- Interior preservation. Seat wear, trim condition, dash integrity, switchgear, and factory pieces that disappear over time.

- Mechanical credibility. Compression or leakdown results if available, service history, drivetrain behavior, and known GT-R maintenance items.

- Underside and chassis. Rust, seam sealer disturbance, impact evidence, and condition of suspension and AWD components.

This is where photos matter. Underbody images, paint meter readings, shop inspection notes, and dated service invoices carry more weight than broad statements like "clean car" or "well maintained."

Provenance and sale context

Documentation changes an opinion into an argument. Service books, import papers, export certificates, deregistration records, auction sheets, receipts, ownership history, and period photos help prove that your car belongs in a narrower and stronger comp set.

That proof is what supports what fair market value means in a vehicle claim. For a GT-R, that means the price supported by the market for your exact specification, condition, history, and legal-market context. It does not mean an average pulled from older sports cars with similar age or body style.

The strongest appraisal files do one thing well. They make it hard for the insurer to substitute a weaker comparable without getting caught.

The Appraisal Process From Start to Finish

The claim usually turns on what you can prove in the first few days after the insurer sends a low number. A phone argument does not fix a weak file. Documents, photos, and a report that ties your exact car to the right market do.

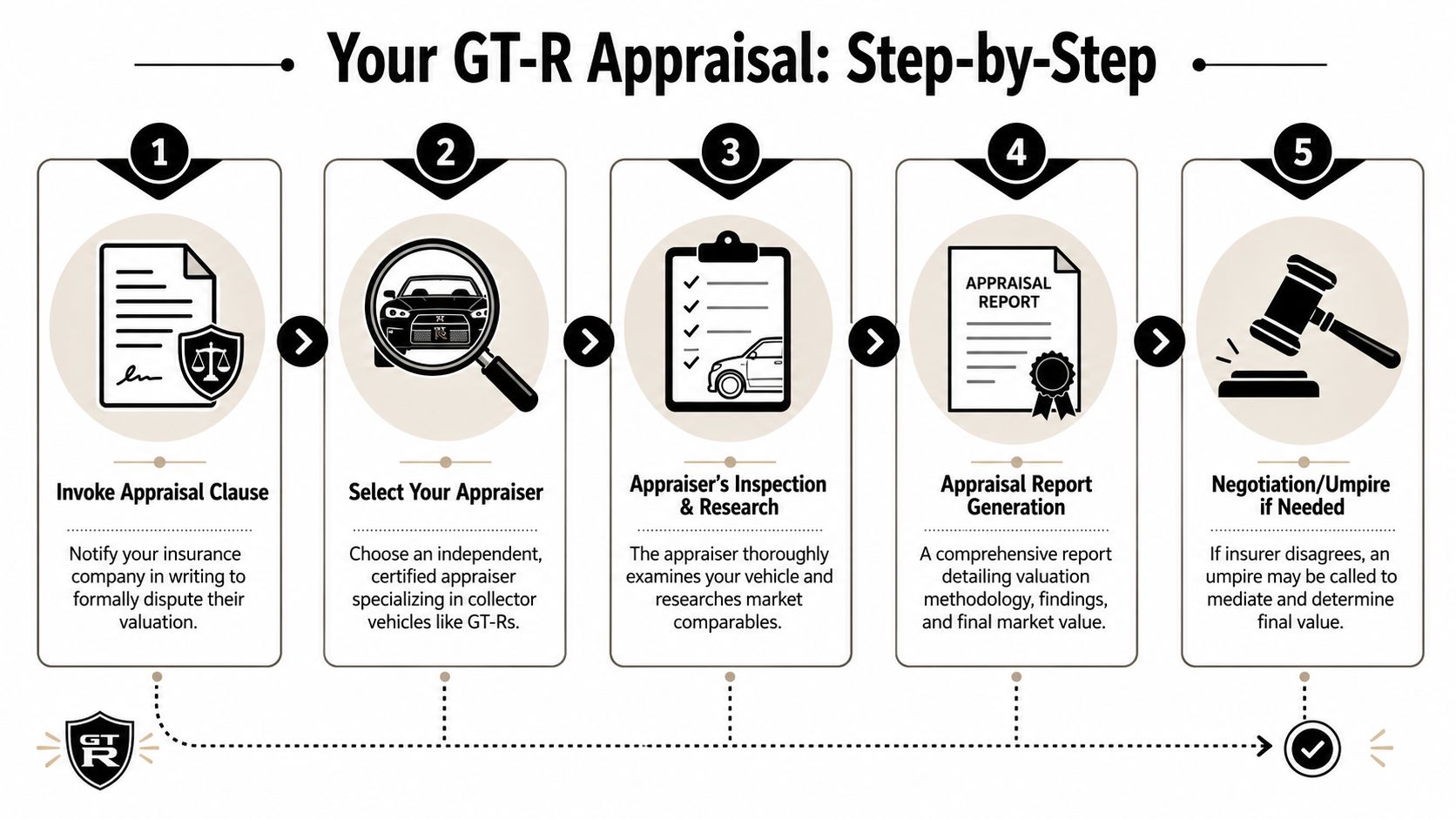

Start with a formal dispute, not a phone argument

Once the insurer's valuation misses the mark, move the dispute into the policy process in writing. Review the appraisal clause, follow the notice requirements, and keep a clean paper trail from day one.

Keep the letter short. State that you dispute the valuation and are invoking the applicable process under the policy. Do not argue the whole case in that first notice, and do not volunteer opinions you cannot support yet.

If you want a plain-language explanation of what a car appraisal does in an insurance claim, read that before you send anything.

Build the file before the inspection

A Skyline appraisal is only as strong as the evidence behind it. The appraiser's job is to verify and explain. Your job is to preserve the records that prove why your car belongs in a tighter, stronger set of comparables than the insurer wants to use.

Gather these items before the inspection is scheduled:

- Ownership and import records. Title, registration, customs entry paperwork, import approval documents, export certificates, auction sheets, and foreign registration records.

- Service history. Invoices, specialist inspection reports, timing belt or chain service where relevant, fluid services, drivetrain work, alignment sheets, and tuning or maintenance notes from known GT-R shops.

- Modification support. Receipts, part numbers, installer invoices, dyno sheets, emissions paperwork if applicable, and photos showing the parts on the car before the loss.

- Pre-loss photos. Exterior, interior, engine bay, trunk, VIN tags, glass markings, wheels, underside, and close-ups of areas that show preservation or originality.

- Loss-related records. Damage photos, tow receipts, storage invoices, body shop estimates, salvage bids if disclosed, and the insurer's valuation report.

Do not hand over a stack of unlabeled documents. Organize it. Date it. Match each record to a point you want the appraiser to make, such as import legitimacy, originality, recent mechanical work, or the presence of period-correct parts that affect buyer demand.

A public example of the problem with generic channels showed a Skyline GT-R being taken to CarMax, underscoring how mainstream appraisal systems miss collector nuance. The better path is to challenge low offers with market-specific comparables and import-specific documentation, not generic software, as discussed in this Skyline GT-R CarMax appraisal video.

What the appraiser actually does

The work has two parts. First, the appraiser verifies the car. Second, the appraiser builds a valuation argument that can survive scrutiny from an adjuster, a valuation vendor, or an umpire.

On inspection, the appraiser confirms chassis identity, trim level, market of origin, legal import status, condition, damage impact, and whether the claimed features are present. On research, the appraiser screens comparable sales for the factors that matter on a GT-R. Year, generation, trim, legality, mileage, modifications, provenance, and sale timing all affect whether a comp belongs in the report.

Method matters. If the report does not explain why a comparable was selected, how differences were adjusted, and why weaker sales were rejected, the insurer has room to attack the conclusion.

A firm such as Total Loss Northwest handles this kind of dispute work by preparing independent appraisal reports for total loss and diminished value claims. Whatever provider you use, pick someone who can document the reasoning line by line. For a Skyline, that is what turns "my car is worth more" into a settlement position that is hard to dismiss.

Independent Appraiser vs Insurance Company Valuation

The two sides are often using the word “value” to mean different things. That's why these disputes get stuck.

An insurance valuation vendor often starts with speed, scale, and consistency across thousands of claims. An independent appraiser starts with the individual vehicle and asks whether the chosen comparables, condition adjustments, and market assumptions fit.

The gap becomes obvious with performance heritage. An independent appraiser may consider facts that matter to collectors, such as the R34 GT-R's 4.4-second 0 to 62 mph time and the R33 era Nordschleife production-car record of 7:59, both of which contribute to the model's reputation and collector significance, as summarized in the Skyline GT-R historical overview. Insurance software usually doesn't care about those facts at all.

Valuation method comparison

| Aspect | Insurance Company Valuator | Independent Appraiser |

|---|---|---|

| Goal | Resolve the claim within the insurer's valuation system | Determine supportable fair market value for the specific vehicle |

| Vehicle identification | May rely on broad database categories | Verifies chassis, trim, engine, options, and import details |

| Comparable sales | Often filtered through mainstream valuation channels | Screens for collector-relevant and specification-relevant comparables |

| Modifications | Frequently minimized or ignored | Evaluates whether modifications harm, help, or simply change market position |

| Documentation | Uses what is readily available in the file | Builds the file with receipts, records, photos, and provenance evidence |

| Market view | Looks for standardization | Accounts for enthusiast demand and transaction quality |

| Settlement effect | Can support a lower starting offer | Creates a defensible counter supported by evidence |

Why the difference matters

This isn't just a second opinion. It's a different method.

An insurer's valuation might be neat, fast, and wrong. A specialized Skyline GT-R appraisal is slower because it has to be. It has to verify identity, inspect condition, test the insurer's comparables, and explain each adjustment in a way that can survive negotiation.

If you're weighing whether to bring in outside help, independent car appraisers for disputed valuations gives a useful overview of how that role differs from the insurer's process.

The strongest appraisal reports don't ask for trust. They show their work.

Common Pitfalls That Cost Owners Thousands

Owners lose ground in GT-R claims long before any final number is issued. The expensive mistakes are usually procedural.

Mistaking an initial offer for the final answer

Some owners verbally accept the framework of the insurer's valuation before they've reviewed the report carefully. They may not cash a check yet, but they start negotiating inside the insurer's low baseline.

That's dangerous, especially in a market that isn't moving in one clean direction. One high-profile Skyline GT-R auction group sale reportedly brought $1.537M combined, 44% below the low-end estimate, which is a reminder that headline pricing can mislead in both directions, according to this discussion of uneven Skyline GT-R auction results. You can't use one flashy result, or one disappointing one, as a shortcut for your car's value.

Hiring the wrong appraiser

A licensed or experienced appraiser is not automatically the right appraiser for a Skyline. Plenty of competent professionals know domestic total loss work but don't know imported Japanese collector cars well enough to defend trim-level differences, period-correct modifications, or weak comparables.

Screen them hard. Ask what they need from you. Ask how they handle imported-vehicle documentation. Ask how they separate a generic Skyline from a true GT-R market comp.

Poor documentation habits

Many owners have spent real money on preservation and upgrades but kept terrible records. Receipts are missing. Import paperwork is scattered. Photos are low quality or taken only after the crash.

Avoid that by treating your claim file like a presentation, not a junk drawer:

- Create a chronology. Purchase date, import milestones, major service, and recent improvements.

- Match receipts to photos. If you bought parts, show the parts installed on the vehicle.

- Label originality clearly. Note what remains factory, what has been changed, and whether factory take-off parts are included.

- Preserve pre-loss evidence. Cloud backups matter. Old listing photos, maintenance photos, and event photos can help prove condition.

A GT-R owner with ordinary records often loses to an insurer with ordinary software. Documentation is how you break that tie.

Assuming all modifications add money

They don't. Some make the car easier to sell. Some narrow the buyer pool. Some raise questions about tuning quality or driveline stress. If you can't prove parts quality, installation quality, and market acceptance, don't expect the insurer to give full credit.

The useful habit is to document modifications the way a skeptical buyer would want to see them. Brand, date, installer, supporting photos, and any removed OEM components.

Your Next Steps for a Fair Skyline GT-R Settlement

The call usually goes the same way. The insurer gives you a number that might fit an ordinary imported coupe, but not a real GT-R with documented history, proven condition, and a paper trail that supports its market position. At that point, arguing from memory is a losing move. Build the file that forces a better valuation.

Use this checklist and treat each item like evidence, not admin work:

- Reject the valuation in writing and state clearly that you dispute it.

- Ask for the insurer's full valuation report and review the actual comps, condition adjustments, and trim description they used.

- Assemble your proof file. Include title, registration, import paperwork, auction sheet if available, service records, parts receipts, dyno or tuning records where relevant, and clear pre-loss photos.

- Define the car precisely. Document the chassis code, generation, trim, drivetrain, mileage, factory options, color, ownership history, and pre-loss condition.

- Separate OEM, period-correct, and aftermarket changes. Show what was factory, what was upgraded, who installed it, and whether original take-off parts are included.

- Get an independent appraisal from someone who understands collector imports and can defend comp selection, rarity, and condition adjustments.

- Review legal options if needed. For a plain-language overview of how totaled car claims can intersect with legal remedies, Mattiacci Law on totaled car claims is a practical reference.

The owners who get paid fairly usually do one thing better than the insurer. They present a file that answers every predictable objection before it comes up. If the report says "Skyline," your evidence needs to prove "GT-R." If the carrier questions condition, your dated photos, service history, and import records need to close that gap.

That is how low-ball offers get challenged. Specific documents. Defensible comps. Clean chronology. A Skyline GT-R settlement turns on proof.

If you're dealing with a low total loss or diminished value offer, Total Loss Northwest provides independent auto appraisals for disputed vehicle claims. For Skyline GT-R owners, that means building a settlement case around market comps, import documentation, condition evidence, and the exact facts of the car, instead of relying on generic valuation software.