The call usually comes when you're already overloaded. The car's at a body shop or tow yard. You're trying to line up rides, deal with work, and figure out whether the other driver's insurer is going to do the right thing. Then the adjuster says your vehicle is a total loss and starts talking about ACV, owner retention, payoff amounts, and settlement paperwork.

A common assumption is that the number is fixed. It isn't.

A total loss claim is a valuation problem first, and a negotiation problem second. If the valuation file is clean, the offer may be reasonable. If the data is wrong, the offer can come in low for reasons that have nothing to do with the actual condition or market value of your car. That's where people get hurt. They focus on the damage, while the insurer is valuing the pre-loss vehicle.

Your Car Is Totaled Now What

The first few days after a total loss decision feel messy because the insurer moves fast and the owner usually doesn't. That's normal. The adjuster has a script. You don't. They do this every day, and you probably don't.

What usually happens is simple. The insurer declares the vehicle a total loss, tells you they're preparing a valuation, and then presents a settlement number as if it's the obvious answer. If you still owe money on the car, the conversation gets even more stressful because you're suddenly thinking about the lender, not just the vehicle.

The first offer is often the beginning of the conversation, not the end of it.

You don't need to argue on day one. You need to slow the process down just enough to get documents, verify facts, and keep from weakening your position too early. That means asking for the full valuation report, confirming whether the claim is going through your policy or the at-fault driver's policy, and making sure you remove personal property from the vehicle before it disappears into salvage handling.

A lot of drivers also need practical claims guidance before they need a valuation fight. If you want a plain-language overview of the insurance side, TCDS Insurance total loss support is a useful reference because it lays out the basic claim steps in consumer terms.

If you want a focused explanation of the process right after the insurer totals the vehicle, what happens when your vehicle is totaled is worth reviewing before you respond to the settlement. That's the point where small mistakes start costing real money.

What to do before you discuss numbers

- Ask for the valuation file: Don't rely on a phone summary. You need the written report.

- Confirm the vehicle details: Year, make, model, trim, mileage, options, and prior condition all need to be accurate.

- Hold your paperwork: Don't sign title or power-of-attorney documents until you understand the offer and whether you're disputing it.

- Collect your records: Maintenance receipts, photos, window sticker, purchase paperwork, and upgrade documentation matter more than people think.

What a Total Loss Valuation Really Means

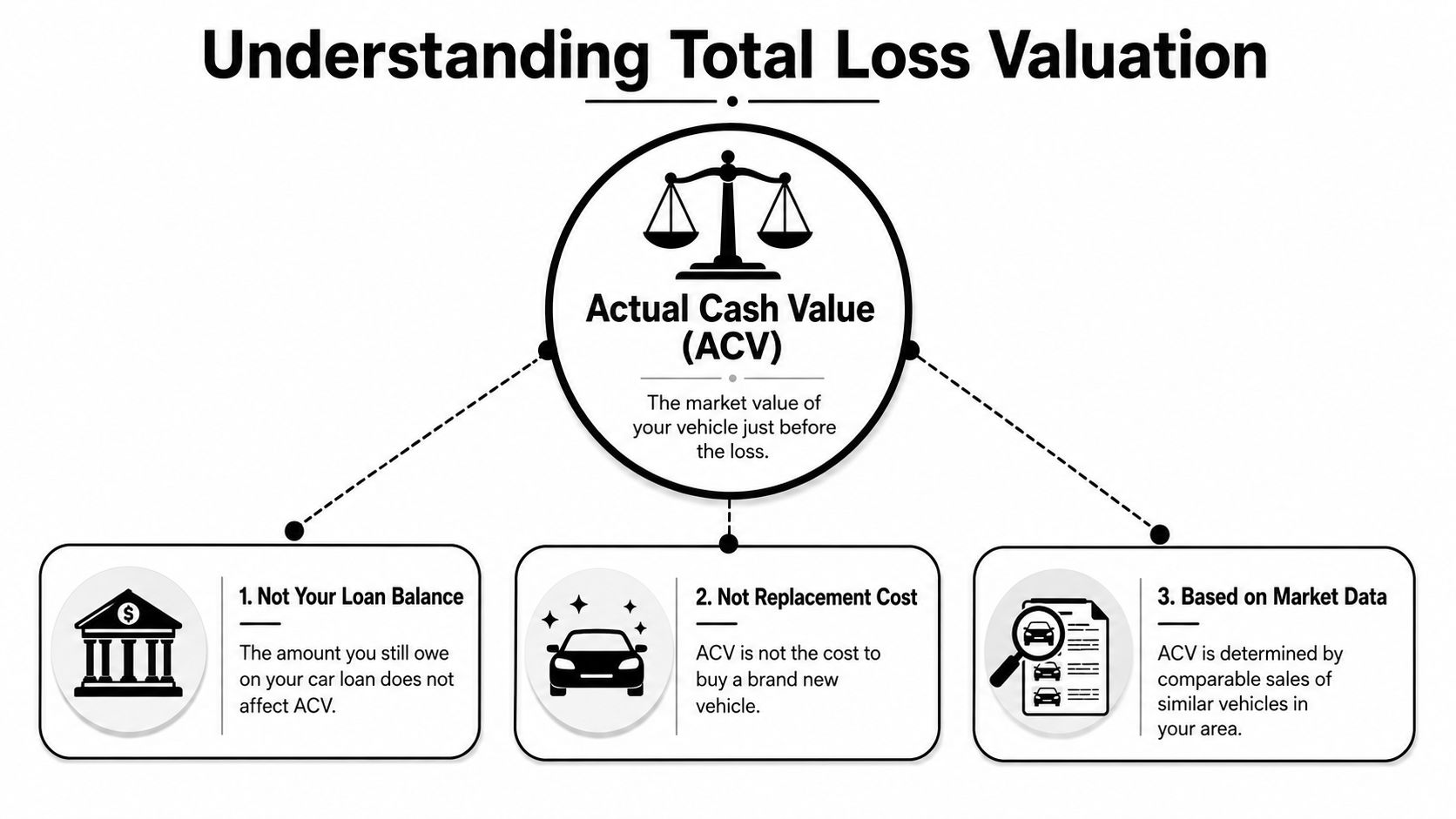

The term that matters most is actual cash value, or ACV. That is not your loan payoff. It is not the price you paid. It is not the cost of replacing your car with a brand-new one.

Think of ACV as the market price for your exact vehicle the moment before the crash. Same year, same model, same trim, similar mileage, similar equipment, similar condition, in your market. That's the target number the insurer is trying to reach, at least on paper.

What ACV is not

Many owners get tripped up because they compare the offer to the wrong benchmark.

| Comparison point | Why it doesn't control |

|---|---|

| Loan balance | Your lender's payoff reflects financing, not market value |

| Original purchase price | That number may be years old and no longer matches the current market |

| Cost of a new replacement | Insurance usually values the pre-loss used vehicle, not a new one |

If you want a simple outside explanation of the market concept behind ACV, understanding fair market value helps. It's the right lens for a total loss valuation because the claim turns on what a willing buyer would pay for a comparable vehicle, not on what the owner hoped the car was worth.

Why the vehicle gets totaled

Insurers don't total cars just because repairs are expensive. They compare repair economics to ACV. A widely cited industry explanation is that many markets use a threshold in the 70% to 80% range to decide whether a vehicle is totaled, and if a vehicle has an ACV of $25,000, a repair estimate around $17,500 to $20,000 can put it near a typical total-loss decision point, though state rules and formulas can differ (industry explanation on total-loss thresholds).

That doesn't mean every state uses the same formula. Some rules compare repair cost alone to value. Others compare repair cost plus salvage value to ACV. The important point for you is this: the total loss decision is one calculation, and the settlement amount is another. People often mix those together.

Practical rule: A car can be correctly declared a total loss and still be incorrectly valued.

What works when you're reviewing the offer

The strongest response is factual, not emotional.

- Use the insurer's own framework: If they're valuing a specific trim in a specific market, make them do that accurately.

- Separate the issues: First ask whether the vehicle should be totaled. Then ask whether the amount offered reflects the right ACV.

- Look at pre-loss condition objectively: A clean, well-kept vehicle deserves proper credit. A rough vehicle won't support the same argument.

How Insurers Calculate Your Car's Value

Most adjusters aren't making up a number from memory. They're using a report generated through a valuation system that pulls market data and applies adjustments. That's why these claims can look objective even when the result is off.

Historically, total loss valuation moved from simple book-value estimates to data-driven market comparisons using third-party systems that analyze comparable sales, regional market data, vehicle options, and mileage instead of relying on a single guide (how insurance companies determine total loss value). That shift made the process more standardized, but it also made it more dependent on the quality of the inputs.

What usually goes into the report

A typical valuation file pulls together several moving parts:

- Comparable vehicles: Listings or sales data for similar vehicles in the relevant market area.

- Mileage adjustments: The report usually tries to account for whether your vehicle had higher or lower mileage than the comps.

- Option credits: Factory equipment can affect value if the report correctly identifies it.

- Condition adjustments: Subjectivity often becomes a factor in the file.

- Regional pricing: A vehicle in one local market may not trade the same as the same vehicle elsewhere.

The insurer's valuation software can process all of that quickly. Quick does not always mean right.

Why owners need to open the black box

A valuation report often looks polished. It may include charts, condition grids, and adjustment lines that give the impression of precision. But a polished report can still rest on bad assumptions.

One common mistake is treating the report like a final answer instead of a draft built from data. If the base vehicle is identified incorrectly, every later adjustment sits on the wrong foundation. If the comparable pool is weak, the output will still be weak, just in a nicer format.

For a closer look at how insurers define and apply ACV in practice, auto insurance actual cash value is a useful companion to the valuation review process.

What works and what doesn't

Here's the trade-off I see most often in real disputes:

| Approach | Result |

|---|---|

| Arguing that the offer feels unfair | Usually goes nowhere |

| Pointing out incorrect vehicle data | Often gets the report revised |

| Sending random listings with no explanation | Easy for the adjuster to ignore |

| Matching listings to trim, equipment, and market area | Much harder to dismiss |

The insurer's playbook is process-driven. Yours should be too.

Common Valuation Pitfalls to Watch For

A lot of owners assume a low offer means the insurer is trying to squeeze them. Sometimes the issue is more specific than that. The file is wrong.

That's the overlooked part of total loss valuation. Consumer advice often says to “check the comps,” but that's too broad to be useful. A pertinent question is which errors affect value. The answer often comes down to trim, options, condition, and outlier comparables, especially on higher-value, collector, or modified vehicles. Kelley Blue Book's consumer guidance highlights this gap and notes that disputes are often a data-quality problem in the valuation file, not just a generic lowballing issue (Kelley Blue Book guidance on totaled cars).

The mistakes that matter most

Start with the vehicle identity itself.

- Wrong trim level: An LX isn't the same as an EX. A base truck isn't the same as one with a premium package. If the trim is wrong, the whole report can skew low.

- Missing factory options: Navigation, advanced driver-assist packages, upgraded wheels, towing packages, and premium audio don't always populate correctly.

- Mismatched comparables: If the insurer pulls weaker comps from a different market area or with materially different equipment, the report loses credibility.

- Condition deductions with thin support: Some reports apply downward condition adjustments that don't line up with the car's actual pre-loss state.

If you can show that the report describes a different vehicle than the one you owned, the dispute changes immediately.

Condition is where many fights go sideways

Owners often overstate condition. Insurers sometimes understate it. Neither helps.

The strongest position is documented condition. Before-loss photos, service records, recent detailing invoices, tire receipts, and body shop records can help show the car was well-maintained. If the report labels the interior or paint as below market and you have clean photos that show otherwise, that's useful. If the car had prior damage, be realistic about it. Overreaching weakens the rest of your file.

A short audit checklist

Use this before you respond to the offer:

- Verify the VIN-based vehicle description

- Confirm the exact trim and drivetrain

- Check mileage

- Review every listed option

- Read the condition lines carefully

- Map each comparable to your local market

- Reject outliers that don't match equipment or class

This is why two owners with the same model year can receive very different results. The report only works if the data is clean.

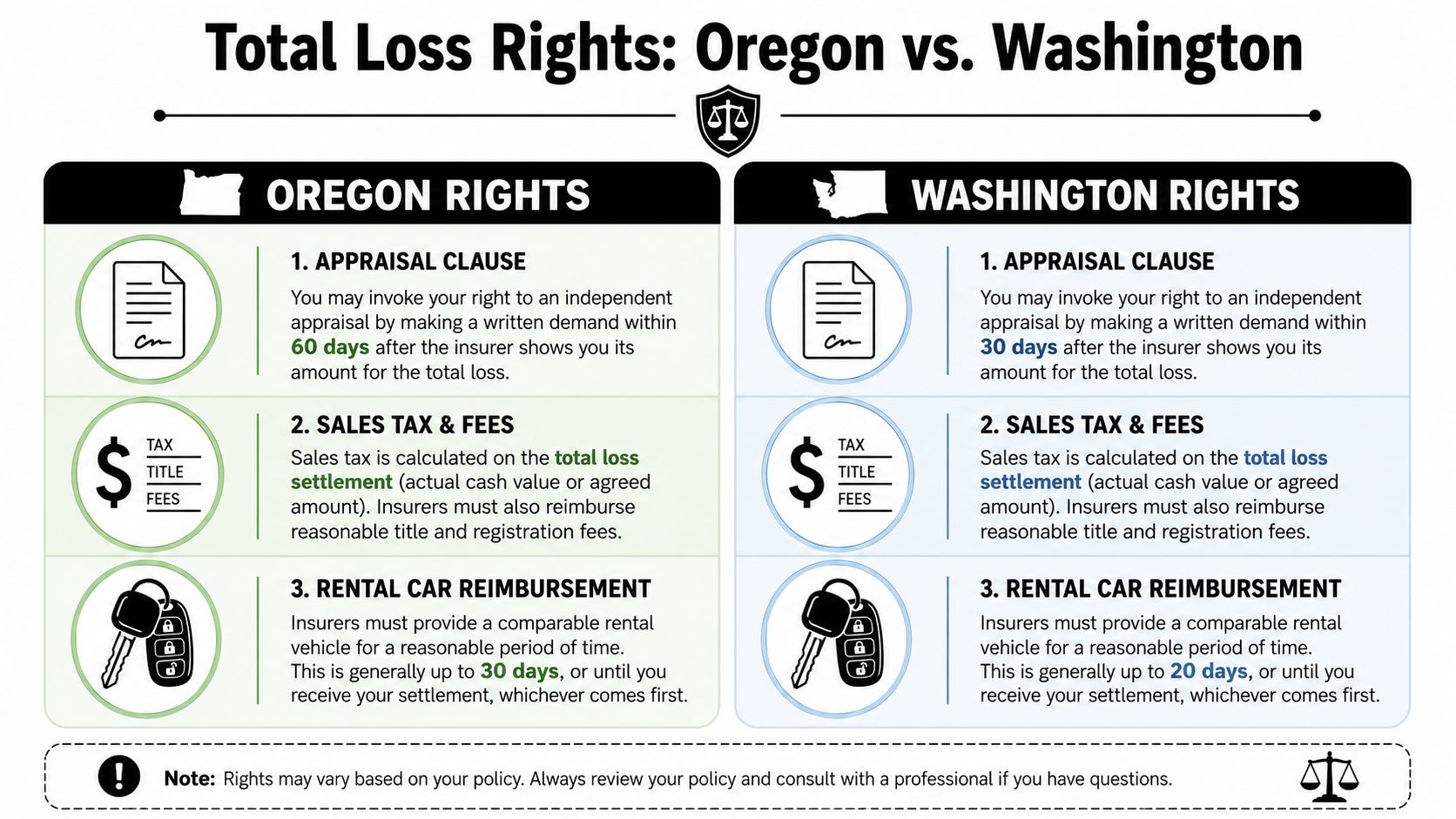

Your Rights in Oregon and Washington

State rules matter because they shape how the insurer handles the claim, what documents you can demand, and how disputes get resolved. Oregon and Washington drivers should not rely on generic national advice. Those articles usually flatten real differences that matter once the settlement number lands.

What matters most in practice

The first thing to understand is that state law and policy language work together. State rules set the frame. Your insurance policy often supplies the tool that breaks a deadlock.

That tool is usually the appraisal clause. In plain terms, it allows a valuation dispute to move out of the normal adjuster back-and-forth and into a structured appraisal process. Each side selects an appraiser, and the process follows the policy language. For many owners, that is the first real strategic advantage in a stalled total loss valuation dispute.

A valuation disagreement is not the same as bad faith. Often it's a contract dispute over value, and the appraisal clause is built for that.

Oregon and Washington issues drivers should check

Because claim handling can vary, owners in both states should focus on the parts of the file that affect what gets paid and when.

- Taxes and transfer costs: Ask how the insurer is handling applicable taxes, title, and registration-related items in the settlement structure.

- Rental cutoff timing: Clarify when rental coverage ends after the total loss decision so you're not surprised.

- Owner-retained salvage: If you're thinking about keeping the vehicle, ask how that changes the payment and title handling.

- Written explanation of value: Don't settle from a phone summary. Ask for the valuation report and the basis for any deductions.

The practical right most people underuse

The appraisal clause is often more useful than a complaint letter because it forces the dispute back to vehicle value. That is where a good total loss case is won. Not with broad accusations, but with a documented market-based valuation.

If your vehicle is repaired instead of totaled, a separate issue may exist after the body work is done. That's diminished value, not total loss valuation, and it should be evaluated on its own facts. Don't let the insurer blur those two claims together.

Step-by-Step Guide to Disputing a Low Offer

Start with the documents. Not the argument.

Step one gets everything else moving

Request the complete valuation report in writing. Ask for all comparable vehicles, all adjustments, and the condition breakdown used in the report. You can't dispute what you can't see.

Once you have it, read the first page slowly. I mean the basics. Year, make, model, trim, mileage, drivetrain, engine, cab style, packages. Many disputes are sitting right there before you ever get to the comp listings.

Audit the report line by line

Treat this like a file review, not a complaint.

- Vehicle identity first: Confirm trim, drivetrain, body style, and factory packages.

- Then mileage: If the mileage is off, note the source that proves the correct figure.

- Then equipment: Compare the report to your window sticker, build sheet, purchase documents, or photos.

- Then comparables: Are they comparable, or just loosely similar cars the software found?

- Then condition: Read every deduction and ask whether the file supports it.

If you need a reference point on when a dispute moves beyond a normal adjustment review and into a formal process, total loss appraisal explains how that path works.

Build your counter with evidence, not volume

A strong counteroffer is concise. It doesn't need ten pages of frustration. It needs a short list of factual corrections with attachments.

Here's a simple structure that works:

- State that you dispute the valuation

- List each factual error

- Attach proof for each correction

- Provide better comparable vehicles

- Request a revised report and updated offer

A weak counter says, “This is way too low.” A strong counter says, “The report identifies the wrong trim, omits the premium package, applies a condition deduction not supported by photos, and relies on comps with materially different equipment.”

Here's a useful explainer on the dispute process:

Sample counter language

You don't need to sound like a lawyer. You need to sound organized.

I dispute the current total loss valuation because the report does not accurately reflect my vehicle's trim, factory equipment, and pre-loss condition. The comparable vehicles also appear mismatched in market area and equipment level. I'm requesting a revised valuation based on the attached documentation.

That's enough to start.

When negotiation stops working

At some point, you'll know whether the adjuster is correcting errors or just repeating the original result. If they revise obvious mistakes and the number still looks arguable, keep working the file. If they won't correct basic data problems, the claim may need independent appraisal.

One option in Oregon and Washington is a certified independent appraiser such as Total Loss Northwest, which handles total loss and appraisal-clause disputes using a separate market-based valuation process rather than the insurer's software-driven result. That is not the only path, but it is a practical one when the paper review has stalled.

Common mistakes that hurt your leverage

| Mistake | Better move |

|---|---|

| Accepting the phone number without the report | Ask for the full written valuation |

| Sending emotional emails | Send a numbered factual rebuttal |

| Using unrelated listings | Use matching local comparables |

| Arguing from loan payoff | Argue from vehicle-specific market data |

| Waiting too long to object | Raise errors promptly and in writing |

Conclusion Putting It All Together for a Fair Payout

A total loss claim feels personal because it is personal. Your transportation is gone, your schedule is wrecked, and the insurer is talking about your vehicle like it's a spreadsheet line item. But the way to win this kind of dispute is not to out-argue the adjuster. It's to out-document the file.

That's the core lesson in total loss valuation. The settlement should reflect the market value of the actual vehicle you owned before the crash. When the report gets the trim wrong, misses key options, uses poor comparables, or applies unsupported condition deductions, the offer drifts away from that target. That's when you push back.

Keep the dispute narrow and factual. Ask for the report. Audit the data. Correct what's wrong. Support every correction with records, photos, and better comparables. If the insurer still won't move off a flawed file, use the appraisal rights built into the policy.

A fair payout usually comes from process, not pressure. The owners who do best in these claims are the ones who stop treating the valuation as a mystery and start treating it like evidence.

If you need help challenging a low total loss offer in Oregon or Washington, Total Loss Northwest provides independent auto appraisals for total loss and appraisal-clause disputes so the settlement can be tested against real market data instead of a flawed valuation file.