You open the claim letter, scan the settlement amount, and feel that drop in your chest. The car was clean, maintained, and worth far more than the number on the page. You already know what the adjuster is going to say. “That's what the system shows.”

That's where many individuals freeze. They assume the insurance company's number must be official, fixed, and somehow beyond challenge. It isn't.

An insurance value dispute is a disagreement over what your vehicle was worth or how much value it lost. It's not unusual. In a market this large, disputes happen constantly. In the U.S., the national average auto insurance expenditure rose 6.1% from $1,062 in 2021 to $1,127 in 2022, according to the Insurance Information Institute citing NAIC data, and in the UK the FCA reported insurers sold over 44 million policies in 2024 and collected more than £20 billion in premiums, which shows just how large and routine these claims systems are in major markets (Insurance Information Institute auto insurance facts).

That scale matters. When insurers process claims in volume, they standardize. Standardization saves them time, but it also creates sloppy matches, hidden deductions, and settlement offers that miss the actual market.

If you're in Oregon or Washington and you think the offer is low, trust that instinct. Then stop arguing emotionally and start building a valuation case. That's how these disputes get resolved.

The Lowball Offer That Sinks Your Stomach

You didn't expect to get rich from your claim. You expected to be made whole, or as close to whole as an insurance policy allows. Then the offer arrives, and it's nowhere near enough to replace the vehicle you owned.

I see this all the time with daily drivers in the Pacific Northwest. Someone has a Subaru, Toyota, Ford, or Honda with solid maintenance history, clean interior, decent tires, and useful trim options. The insurer treats it like an average used car with average wear, average equipment, and average demand. That's how a practical, well-kept vehicle gets valued like a forgettable one.

Why the first offer feels insulting

The first number often ignores the reality of your local market. In Oregon and Washington, buyers pay differently for all-wheel drive, documented maintenance, truck packages, utility setups, and clean-condition vehicles. If the report uses weak comparables or broad deductions, the offer can miss badly.

That doesn't mean the adjuster is personally targeting you. It means the process is built to move fast.

You are not stuck with the first valuation. You are looking at an opening position, not a verdict.

What this dispute is really about

A common belief is that they're arguing about fairness in the abstract. They're not. They're arguing about inputs. Which vehicles count as proper comparables. Whether mileage adjustments are sensible. Whether condition deductions are documented. Whether upgrades, trim, and pre-loss condition were recognized.

That's good news, because inputs can be challenged.

- If the car was totaled: the fight is over what the entire vehicle was worth before the crash.

- If the car was repaired: the fight may be over diminished value, meaning the vehicle is worth less in the market because of the accident history.

- If the vehicle is classic, modified, or rare: the usual insurance math often falls apart fast.

What works is evidence, not outrage. You need the insurer's valuation report, your own comparables, proof of condition, and a strategy. Once you have that, the tone of the conversation changes.

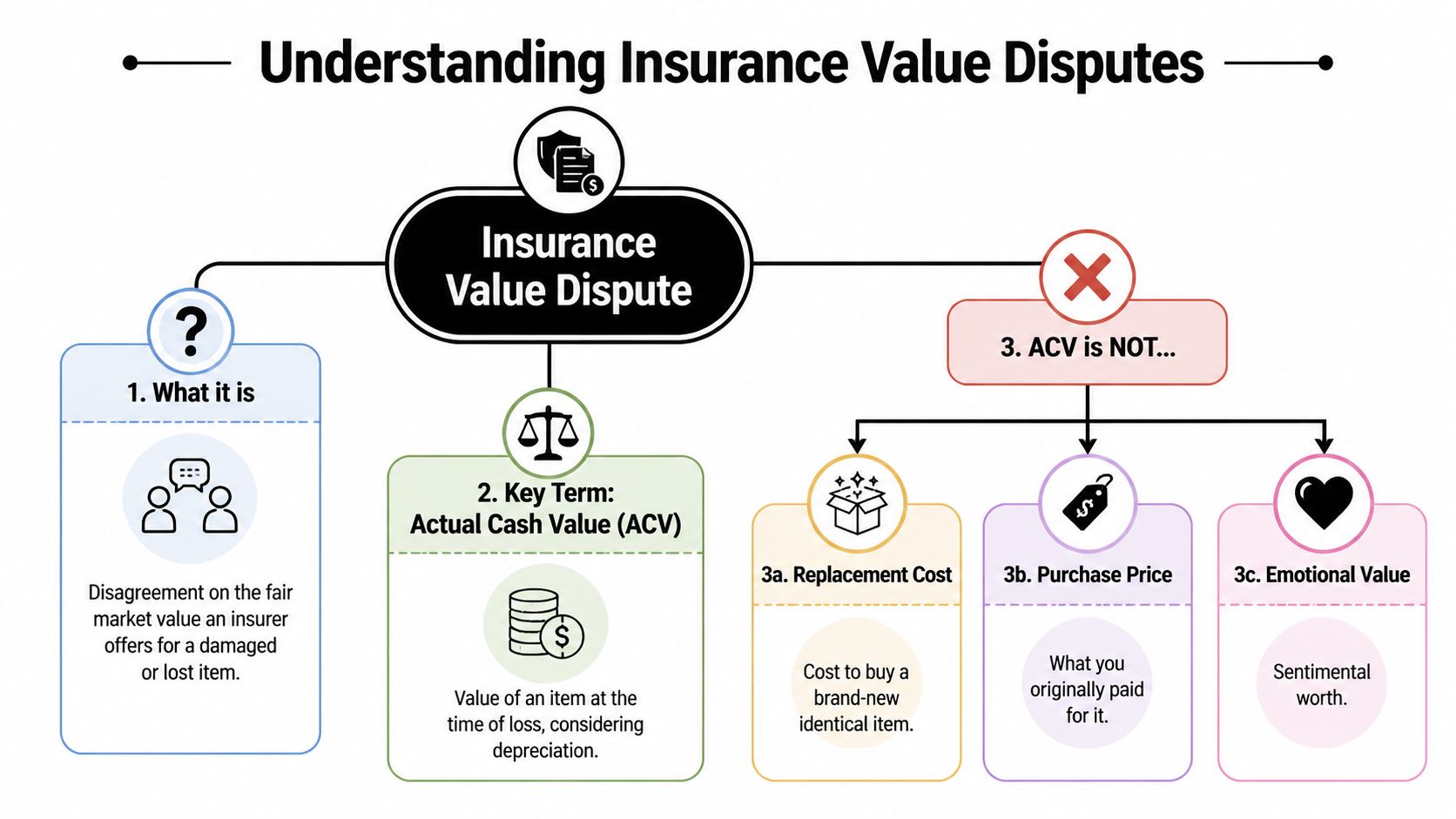

What an Insurance Value Dispute Really Means

At the center of most auto valuation fights is Actual Cash Value, usually shortened to ACV. That's the number insurers typically use for a total-loss payout. It is not what you paid for the car. It is not what you still owe on the loan. It is not what it costs to buy a nicer replacement this week.

It's what a similar vehicle would likely have sold for immediately before the crash, after adjusting for depreciation, mileage, and condition, as explained in Investopedia's overview of how car insurance companies value cars.

Think of ACV like a private sale

If you were selling your vehicle the day before the crash, a buyer wouldn't care what you originally paid. They'd care about year, make, model, trim, mileage, options, condition, title history, maintenance, and what similar vehicles were selling for nearby.

That's the logic behind ACV. The problem is not the concept itself. The problem is how insurers apply it.

They may use comparables that aren't close enough. They may under-credit options. They may grade condition in ways you never agreed to. They may rely heavily on software output even when local listings tell a different story.

Two disputes that people mix up

A lot of owners use the same language for two very different claims. That creates confusion and weakens the argument.

Total loss dispute

This happens when the insurer says the vehicle is a total loss and offers a settlement based on its pre-accident market value. The technical issue is the pre-loss valuation model. The insurer weighs make, model, age, mileage, and condition, then compares that value against repair costs to decide whether the car is economically repairable, as described in Activate Group's explanation of write-off calculations.

If the comparables are poor or the condition adjustments are flawed, the payout can shift materially.

Diminished value dispute

This happens when the car is repaired but has still lost market value because accident history now follows it. Buyers and dealers usually care about that, especially on newer, cleaner, or premium vehicles.

Practical rule: If your car was repaired, don't argue as if it was totaled. If it was totaled, don't waste time arguing repair stigma. Match your evidence to the exact type of loss.

What ACV is not

People get blindsided because they compare the settlement to the wrong benchmark.

- Not replacement cost: the next comparable vehicle for sale may cost more than your ACV payout.

- Not purchase price: what you paid years ago doesn't control today's market value.

- Not emotional value: insurers don't pay more because the car was special to you.

That gap between ACV and replacement reality is why insurance value disputes feel so personal. You're trying to replace a real-world vehicle. The insurer is calculating a market-adjusted number on paper.

Why Insurance Companies Offer So Little

Low offers usually come from process, not mystery. The insurer starts with a valuation system, plugs in vehicle details, pulls comparables, applies adjustments, and produces a report that looks more objective than it often is.

That report can still be wrong.

The big weakness is hidden inside the math

A major consumer problem is that insurers often use condition deductions that aren't transparent, while the industry still disagrees about how some valuation losses should even be defined. That leaves drivers dealing with a technical process without consistent standards, as discussed in the NAIC CIPR analysis on valuation loss issues.

That matters more than is often realized. A deduction for paint, interior wear, prior cosmetic damage, tires, or “overall condition” can push a payout down quickly, especially when the insurer doesn't clearly show how it arrived at the deduction.

Common ways the valuation gets distorted

Some offers come in low because the insurer used weak comparable vehicles. Others come in low because the software was fed bad assumptions. In both cases, the output looks polished enough that people accept it.

Here's what I tell clients to look for first:

- Wrong trim or equipment: A base model comp is not a fair comp for a better-equipped vehicle.

- Mismatch on mileage: A lower-value high-mileage comp can drag your number down.

- Condition downgrades: The report may assume wear or prior issues that weren't documented well.

- Poor local matching: Vehicles from a different market don't always reflect Pacific Northwest pricing.

- Missed maintenance or upgrades: New tires, service history, and options often get ignored.

If you want a deeper look at how valuation software can shape these outcomes, review this breakdown of CCC auto valuation issues.

Don't argue that the insurer is “being unfair” in general terms. Argue that the valuation uses bad matches, unsupported deductions, or omitted features.

Low valuation and claim resistance often travel together

A weak vehicle valuation isn't always an isolated problem. It can sit inside a broader claim strategy where the insurer narrows the loss, leans on technicalities, or pushes the burden back to you. If you want a plain-English look at related tactics, Martin Hernandez, P.A. has a useful overview of reasons for insurance claim denials.

That doesn't mean every low offer is bad faith. It means you should treat the valuation report like evidence to be audited, not a neutral truth.

Your Legal and Contractual Resolution Options

Once you've identified a bad valuation, you need to choose the right pressure point. Don't jump straight into threats. Start with the least expensive tool that can still move the file.

Start with a written demand

A solid demand letter does three things. It states the insurer's number, explains why it's flawed, and attaches evidence supporting your number. Keep it businesslike.

Include comparable listings, photos of pre-loss condition, maintenance records, trim and option details, and any independent valuation support. Ask for the full valuation report if you don't already have it.

The appraisal clause is often the strongest tool

For disputes over the amount of loss, the appraisal clause is often the cleanest contractual remedy. It is not a coverage tool. It does not decide whether the claim is covered. It resolves value.

That distinction matters a lot with unusual vehicles. The process can be effective, but each side pays its own appraiser and shares the umpire cost, which is exactly why owners of high-value, classic, and modified vehicles need to think carefully before invoking it, as explained by the General Insurance OmbudService of Canada on claim value disagreements.

Compare the options before you act

| Method | Typical Cost | Timeline | Best For |

|---|---|---|---|

| Demand letter | Low | Short to moderate | Clear documentation gaps, weak comparables, missed options |

| Appraisal clause | Moderate because each side pays its own appraiser and shares the umpire cost | Moderate | Strong disputes over amount of loss, especially where valuation evidence is solid |

| Mediation | Varies | Moderate | Cases where both sides still want a negotiated settlement |

| Small claims court | Filing and time costs | Moderate to longer | Smaller disputes where the amount justifies direct court action |

Mediation can work, but only if both sides are serious

Mediation is useful when the gap is real but the insurer is still engaging. It can save time and reduce posturing. It is less useful when the insurer keeps repeating the same unsupported report and won't revisit the inputs.

If you choose mediation, bring the same evidence you'd use in appraisal. Good faith discussion without evidence goes nowhere.

Know when the issue may be more than valuation

Sometimes the insurer isn't just undervaluing the car. It may be delaying, misrepresenting process, or refusing to evaluate evidence fairly. If you're seeing that pattern, it helps to understand the broader concept of how insurers act in bad faith.

That doesn't replace your valuation strategy. It sharpens it.

If the dispute is strictly about dollars attached to the vehicle, push valuation evidence hard. If the carrier is also mishandling the claim process, document every communication.

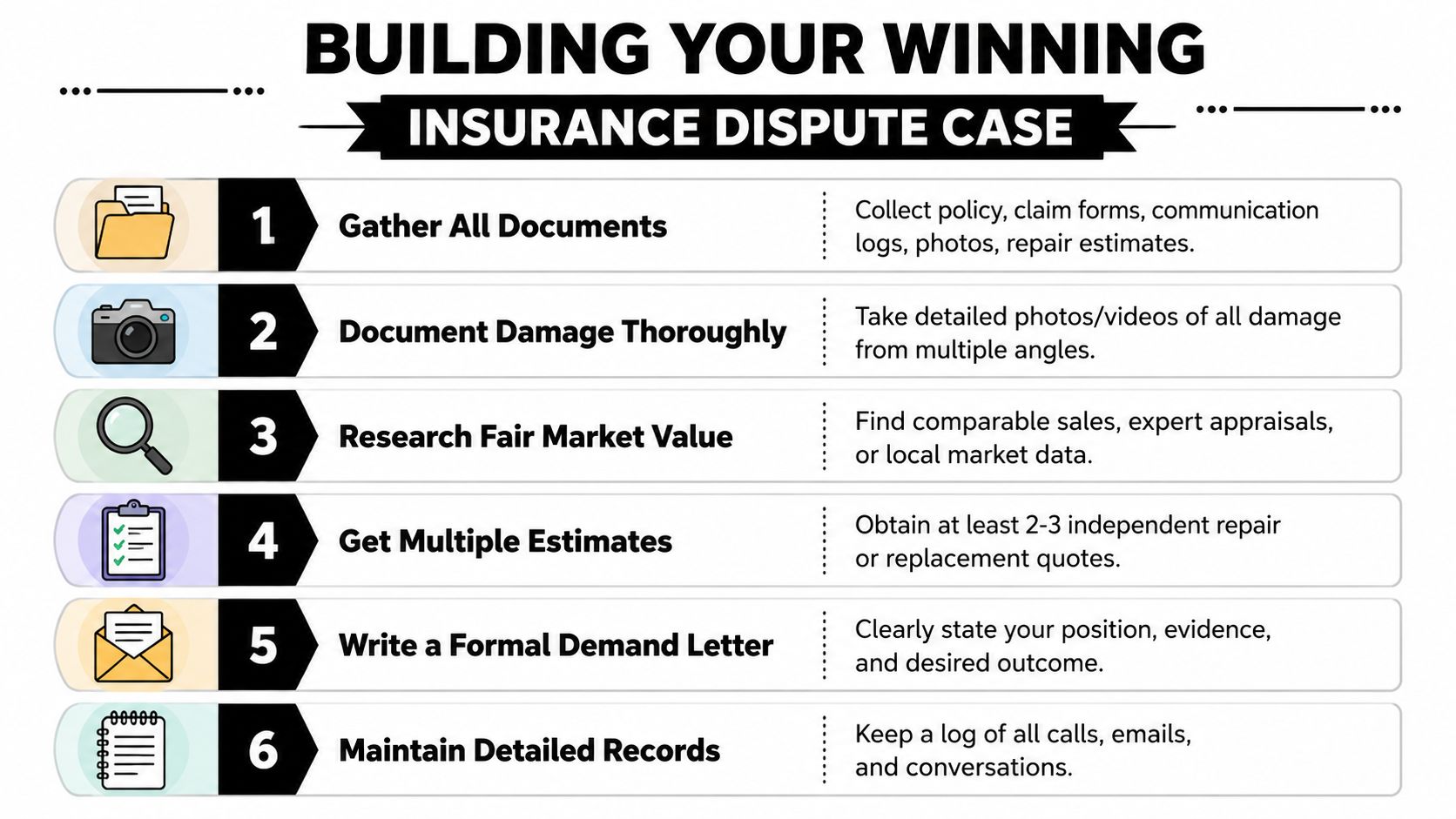

How to Build a Winning Dispute Case Step by Step

You win an insurance value dispute by making it easier for the insurer, appraiser, mediator, or judge to accept your number than to defend theirs. That means organized proof. Not a pile of screenshots and frustration.

Step one through three

Get the valuation report

Ask for the full report the insurer relied on, not just the settlement summary. You need to see the comparable vehicles, adjustments, mileage assumptions, condition grades, and any deductions.Audit every comparable

Look for trim mismatches, wrong drivetrain, missing features, title issues, different condition, and poor location matching. If a comp would never be accepted by a real buyer comparing vehicles side by side, challenge it.Build your own fair market value file

Use actual market listings and organize them cleanly. This guide to calculating fair market value is a practical place to start.

Regulators and ombudsmen test valuation fairness using market evidence. Maryland's consumer guidance tells claimants to prove diminished value with a dealership written offer differential or an independent appraisal, which is a strong reminder that a persuasive dispute combines comparable listings, condition evidence, and an expert report (Maryland auto insurance consumer guide).

Step four through six

Before you organize your file, this walkthrough is worth watching:

Document pre-loss condition like you're proving a sale

Gather photos, service records, receipts, tire information, upholstery condition, and any evidence that shows the car was above average for its age. If you had a recent detail, mechanical work, or dealer inspection, include it.Get an independent appraisal when the gap is meaningful

This is where many cases turn. A qualified independent appraiser can evaluate the vehicle, assess the insurer's report, and produce a valuation supported by actual market data. For injury-related claims that overlap with property issues, I also like practical resources such as Spivak & Sakellariou's injury claim advice because they reinforce the same principle: document everything and don't leave value on the table.Write a clean counter-offer package

Your letter should be calm and direct. State the insurer's figure, your figure, and the exact reasons for the difference. Attach your comp sheet, photos, records, and expert report if you have one.

What your package should include

- Core claim documents: policy pages, adjuster letters, valuation report, claim number, and loss date.

- Vehicle proof: VIN, trim, options, mileage, ownership documents, and title status.

- Condition evidence: interior photos, exterior photos, service records, receipts, and recent work.

- Market support: comparable listings with notes explaining why they match better than the insurer's.

- Expert support: independent appraisal or dealer opinion when available.

A strong dispute file reads like a professional valuation packet, not a complaint thread.

Navigating Disputes in Oregon and Washington

The Pacific Northwest has its own valuation rhythm. AWD vehicles, utility rigs, clean trucks, enthusiast cars, and well-maintained imports often carry stronger local demand than generic valuation models capture. That's why Oregon and Washington drivers should be especially skeptical when a report uses broad regional assumptions or thin comparable support.

What matters locally

The practical rule in both states is simple. Focus on evidence that reflects your real pre-loss market, not a generic national average. Local listings, trim accuracy, mileage consistency, and condition proof matter more here because the market often rewards specific configurations.

That's especially true for diminished value claims. If you're dealing with post-repair loss instead of a total loss, this overview of diminished value auto claims gives a useful local frame for how owners in Oregon and Washington should think about proof.

Daily driver versus specialty vehicle

A commuter SUV and a collector car do not belong in the same dispute strategy.

For a daily driver, your best argument is usually straightforward market support. Good comparables, corrected condition, and accurate options can often move the claim.

For a high-value, classic, or modified vehicle, the hard question is whether ordinary “market value” even reflects replacement reality. That's where appraisal may be worth the cost. If the insurer's report treats a specialty vehicle like a generic used car, you need someone who understands niche market behavior, not just a standard valuation template.

Timelines and expectations

Most owners expect this to be fixed in a few phone calls. Sometimes it is. Often it isn't.

A realistic approach looks like this:

- Initial review period: you request the report, inspect the comps, and gather your records.

- Counter-offer phase: you submit corrected comparables and condition evidence.

- Escalation phase: if the insurer won't move, you consider appraisal, mediation, or court.

- Resolution phase: the matter closes after negotiated revision or formal valuation process.

The best way to stay in control is to act early. Don't wait until frustration turns into a deadline problem.

When to Hire an Expert like Total Loss Northwest

Some disputes are simple enough to handle yourself. If the insurer missed a trim package, used a bad comp, or ignored obvious maintenance, a sharp written challenge may fix it.

Others are not simple. If the vehicle is high-value, classic, modified, rare, or unusually clean for its age, standard valuation systems often miss the market by a wide margin. That's when independent help stops being optional.

The situations where expert help makes sense

- Large valuation gap: the insurer's number and your evidence aren't even close.

- Specialty vehicle issues: classic, collector, performance, custom, or heavily optioned vehicles.

- Opaque condition deductions: the carrier reduced value without giving you a clear factual basis.

- Appraisal clause decisions: you need to know whether the likely upside justifies the cost.

The appraisal clause can be effective, but it isn't free. Each side pays its own appraiser and shares the umpire cost, which is exactly why owners of unusual vehicles need to weigh the economics carefully. That cost structure is spelled out in the earlier cited guidance on appraisal disputes.

If you need an Oregon or Washington appraiser who works specifically on total loss and diminished value matters, Total Loss Northwest is one factual option. The company handles independent auto appraisals and appraisal clause disputes for drivers dealing with low ACV offers and post-accident value loss.

The right time to hire help is before you've spent weeks making emotional arguments that don't change the file. Bring in an expert when the valuation is technical, the vehicle is unusual, or the insurer keeps hiding behind software output.

If you're staring at a low settlement and don't know whether to negotiate, invoke appraisal, or get an independent opinion, talk to Total Loss Northwest. A focused review of the valuation report, comparables, and condition deductions can tell you quickly whether the offer is defensible or worth challenging.