You open the total loss email, scan the number, and your stomach drops. The car was clean. The mileage was reasonable. You kept receipts. Yet the settlement offer looks like it belongs to a rougher, lower-trim version of your vehicle from a different market.

That reaction is common, and it's usually justified.

In an Actual Cash Value dispute, claimants often make the same mistake first. They argue from emotion, from what they paid, or from how much they still owe on the loan. None of that controls the claim. What controls the claim is the insurer's valuation method, the inputs fed into that method, and whether the policy gives you the right to force an independent appraisal process.

As a certified auto appraiser, this is the point where I tell clients to stop treating the insurance company's number like a verdict. It's a valuation position. That's different. And positions can be challenged.

Understanding the ACV Offer and Why It's Low

Actual cash value, or ACV, is not a single universal formula. In insurance law, it is commonly calculated by one of three methods: replacement cost minus depreciation, fair market value, or the broad evidence rule, and auto claims usually focus on the vehicle's pre-loss condition, mileage, age, and market trends rather than what you paid for it, as summarized in this ACV insurance law reference.

That last part matters. Your purchase price is almost never the controlling number in a total-loss car claim. The minute a vehicle leaves the lot, depreciation starts. That's why even a newer vehicle can be declared a total loss and still produce an offer that feels too low.

Where the offer usually goes wrong

The insurer's first valuation often comes from third-party software and a worksheet built around selected comparable vehicles. That process can miss the details that drive value in the prevailing market.

Common failures include:

- Wrong trim level. A base model gets compared to your better-equipped version.

- Mileage errors. Even a modest mistake can skew the valuation.

- Condition downgrades. The report may assume wear your vehicle didn't have.

- Missing options. Factory packages, premium audio, towing equipment, driver-assistance features, or wheel upgrades may not be coded correctly.

- Weak comparable vehicles. The report may pull vehicles that aren't comparable in region, equipment, or condition.

Practical rule: A low ACV offer is usually won or lost in the worksheet, not in the adjuster's email.

There's also a mindset issue. Policyholders often think the insurer is calculating one objective truth. In reality, an ACV dispute often turns on how depreciation is measured and what comparable market data are accepted under the governing method. That's why arguing “I paid more” rarely works, while proving “your inputs are wrong” often does.

What ACV is not

It is not replacement cost coverage. And it is not a promise to buy you a new version of your old car.

If you want a plain-language explanation of the valuation concept before you challenge the number, this breakdown of actual cash value in auto insurance claims is a useful starting point.

The claims process also follows incentives. If you want a broader consumer-side view of carrier behavior, this article on why insurance companies deny claims in Florida helps explain how insurers frame disputes, delay decisions, and narrow payouts. Different state, same lesson. Don't assume the first position is the fairest one.

Your First Moves After a Lowball Offer

The first 48 hours matter because this is when you either preserve your advantage or lose it.

When I get hired on an Actual Cash Value dispute, I don't start by debating the final number. I start by forcing disclosure. That's the most defensible approach. The insurer should identify the exact valuation path it used, and the practical workflow is to request the complete settlement worksheet, identify whether the carrier used comparable-market data or a cost-minus-depreciation model, and then test the inputs for errors in mileage, condition, options, and pre-loss wear, as explained in this insurance valuation methodology analysis.

What to request immediately

Send a short written request. Keep it calm and specific.

Ask for:

The full valuation report

Not the summary page. The entire worksheet.All comparable vehicles used

You want year, make, model, trim, VIN if available, dealer source, mileage, and location.Condition adjustments

Ask how they rated your vehicle and what standards they used.Option and package list

Confirm every factory and major installed option they credited.Any deductions

Especially pre-existing damage deductions and condition-related reductions.

How to read the report like an appraiser

Don't skim it. Audit it.

Use this quick review grid:

| Item | What to check | Why it matters |

|---|---|---|

| Vehicle identity | Year, trim, drivetrain, body style | Wrong model means wrong market |

| Mileage | Odometer reading used | Mileage errors distort value |

| Options | Packages, safety tech, premium features | Missing equipment lowers ACV |

| Condition | Interior, exterior, mechanical notes | Subjective downgrades reduce payout |

| Comparables | Region, trim, similarity | Bad comps anchor a bad offer |

The fastest way to weaken an insurer's report is to find a mismatch that should never have been there in the first place.

A short walkthrough helps if you want to see how claim disputes are often framed from the policyholder side:

What not to do

A lot of people sabotage a valid dispute by reacting too fast.

Avoid these moves:

- Don't argue your loan balance. The carrier doesn't owe the payoff unless the policy says so.

- Don't rely on a single listing. One overpriced ad won't carry the dispute.

- Don't send an angry email first. It feels good and usually helps nothing.

- Don't assume a denial ends the matter. If the claim position hardens, guidance on what if your insurance claim is denied can help you think through escalation paths.

The right first move is organized pressure. Once the worksheet is on the table, the negotiation gets clearer.

Building Your Case for a Higher Value

A strong counter doesn't start with “my car was worth more.” It starts with proof.

I'll give you a typical example. Say the vehicle is an older pickup in unusually clean condition. Not a collector truck. Just a well-kept, higher-demand regional vehicle with documented maintenance, decent tires, and the right trim. The insurer's report pulls a handful of comparables, but one is a lower trim, one has materially higher mileage, and another is from a market that doesn't reflect your local demand.

That's the opening.

How the evidence file comes together

The highest-value challenge in these disputes is building market value evidence strong enough to override a low offer. The practical method is to collect recent same-region sales of comparable vehicles, normalize for trim, mileage, and condition, and then compare those against the insurer's report for unsupported deductions or poorly matched vehicles. That same guidance also notes that ACV coverage is often described as roughly 20–25% cheaper than replacement-cost coverage because the insurer's indemnity obligation is lower, as discussed in this guide to negotiating total-loss claims.

What I look for in comps

I don't just search the same year and model. I narrow down to the actual market.

A useful comp file includes:

- Local dealer listings with screenshots showing date, mileage, trim, and asking price

- Private-party listings when they're well documented and close in spec

- Archived listings or sale evidence if current listings are thin

- Service records that support above-average condition

- Photos taken before the loss showing paint, interior, tires, accessories, and overall upkeep

The insurer's comp doesn't become credible just because it's printed in a report. It still has to match your vehicle.

What owners overlook most often

Recent repairs don't convert dollar-for-dollar into ACV, but they can support condition and marketability. Same with new tires, major scheduled maintenance, or hard-to-find factory options. If the valuation report treated your vehicle like an average example when it was clearly above average, that's where the correction happens.

Here's a working checklist I use with clients:

- Start with trim accuracy. If the trim is wrong, fix nothing else until that's corrected.

- Then confirm equipment. Technology, towing, off-road, luxury, and safety packages matter.

- Then attack condition. Photos and maintenance records are stronger than opinion.

- Finally, compare geography. A weak comp from the wrong market can drag everything down.

There's a related concept many drivers confuse with ACV: post-repair loss in resale value. If you're trying to separate those issues in your own mind, this piece on understanding diminished value in New York is a useful contrast. A total-loss ACV dispute is about pre-loss value. Diminished value is about residual loss after repair.

Build your file like you expect a neutral third party to read it. Because if you invoke appraisal, that's exactly what happens.

Invoking the Appraisal Clause in Your Policy

Many policyholders possess the most powerful advantage within their policy and never utilize it.

The Appraisal Clause is often the turning point in an Actual Cash Value dispute because it changes who decides the amount-of-loss issue. Instead of staying trapped inside the insurer's internal process, you move into a contractual procedure where each side names an appraiser and the valuation dispute gets examined outside the claims desk.

If you haven't read yours before, review a plain-language overview of the insurance appraisal clause process. Then pull your own policy and find the actual wording.

Why this changes the power dynamic

A lowball offer survives when the insurer controls the data, the framing, and the pace. Invocation of appraisal disrupts that.

It does three important things:

- Forces formality. The carrier can't hide behind vague conversation.

- Shifts the audience. Your evidence is prepared for appraisers, not just an adjuster.

- Raises the cost of weak positions. Unsupported comps and sloppy deductions are harder to defend.

This doesn't mean appraisal solves every dispute. Coverage issues can still sit outside appraisal depending on the policy wording and the issue in controversy. But when the fight is over amount of loss, appraisal is often the cleanest pressure point.

A simple invocation template

Keep the letter short. Don't over-argue it.

Use language like this:

I dispute the insurer's actual cash value determination and the amount of loss stated in the settlement valuation. Pursuant to the appraisal provision in the policy, I hereby demand appraisal. Please confirm the insurer's appraiser in writing and provide any additional procedural requirements you contend apply.

That's enough to trigger the issue without turning the letter into a rant.

What works and what doesn't

What works:

- A written demand tied to the policy language

- A clean evidence packet already in progress

- A named independent appraiser ready to proceed

What doesn't work:

- Threatening appraisal but never invoking it

- Sending a long emotional letter with no policy citation

- Waiting until after you've accepted the valuation

Working rule: The appraisal clause has value because it is contractual leverage, not because it sounds forceful in an email.

When I see a carrier stall for too long on obvious report errors, I stop asking for courtesy corrections and start preparing for appraisal. That's usually when the negotiation becomes real.

Choosing and Working with an Independent Appraiser

A low ACV offer gets harder to challenge once the insurer names its appraiser and starts the clock. Choose your appraiser before that happens.

The right person does more than argue that your car was worth more. They build a valuation that can hold up inside the appraisal process. In Oregon and Washington, that means knowing local markets, understanding how carriers in the Pacific Northwest build total-loss reports, and being able to explain why a comp should be thrown out, adjusted, or kept.

What the appraiser should actually know

Vehicle ACV disputes turn on method. Legal analysis of ACV ambiguity and depreciation issues shows why technical valuation work matters when policy language is unclear, as discussed in this legal analysis of ACV ambiguity and depreciation issues.

For an auto total loss, I want an appraiser who can do five things well:

- inspect the insurer's comps for trim, drivetrain, mileage, options, prior damage, and title issues

- make condition adjustments that can be defended, not guessed

- separate dealer asking prices from actual market indicators

- write a report an opposing appraiser or umpire can follow line by line

- stay inside the actual dispute, which is amount of loss, instead of drifting into coverage arguments

If you're comparing options, a specialist in independent car appraisal for total-loss disputes is usually a better fit than a general valuation service.

Questions I'd ask before hiring anyone

Ask short questions. Good appraisers answer them without fluff.

| Question | Good sign | Red flag |

|---|---|---|

| Have you handled appraisal-clause vehicle disputes before? | Describes the process, documents needed, and timing | Talks broadly about “vehicle values” |

| How do you choose comps in Oregon or Washington? | Explains region, trim, mileage, options, and condition filters | Relies on national averages or book figures alone |

| Will you audit the insurer's valuation report line by line? | Yes, and explains how unsupported adjustments are handled | Gives a vague “we review everything” answer |

| What does your final report look like? | Can describe the report structure and support for each conclusion | Says a short letter should be enough |

| Will you serve as the named appraiser if appraisal is invoked? | Gives a clear yes or no and explains the role | Avoids the question |

A good appraiser sells process, not outrage.

What working with one should look like

The first step is document control. I ask for the carrier valuation report, CCC or Mitchell output if available, photos of the vehicle before the loss, VIN details, option packages, service records, receipts for major work, and any facts that affect condition or market appeal. If the vehicle is modified, rare, or unusually clean for its age, that gets documented early because those points are easy for insurers to flatten into generic assumptions.

Next comes market testing. The appraiser should verify whether the insurer's comps are real substitutes for your vehicle in your region. In the Pacific Northwest, I often see comps pulled from outside the immediate market or from vehicles that look similar at a glance but differ in trim, cab configuration, AWD versus FWD, branded title history, or equipment packages that materially affect value.

Then comes the report. A usable report does not just announce a higher number. It shows the comp set, explains each adjustment, identifies bad deductions, and states a supportable ACV opinion that can be defended during appraisal.

Total Loss Northwest is one firm that handles certified independent appraisals and appraisal-clause disputes for vehicle owners in Oregon and Washington. Whether you hire that firm or another specialist, use the same standard. Pick someone who knows how to pressure-test an insurer's valuation inside the appraisal process, not someone who merely promises a bigger number.

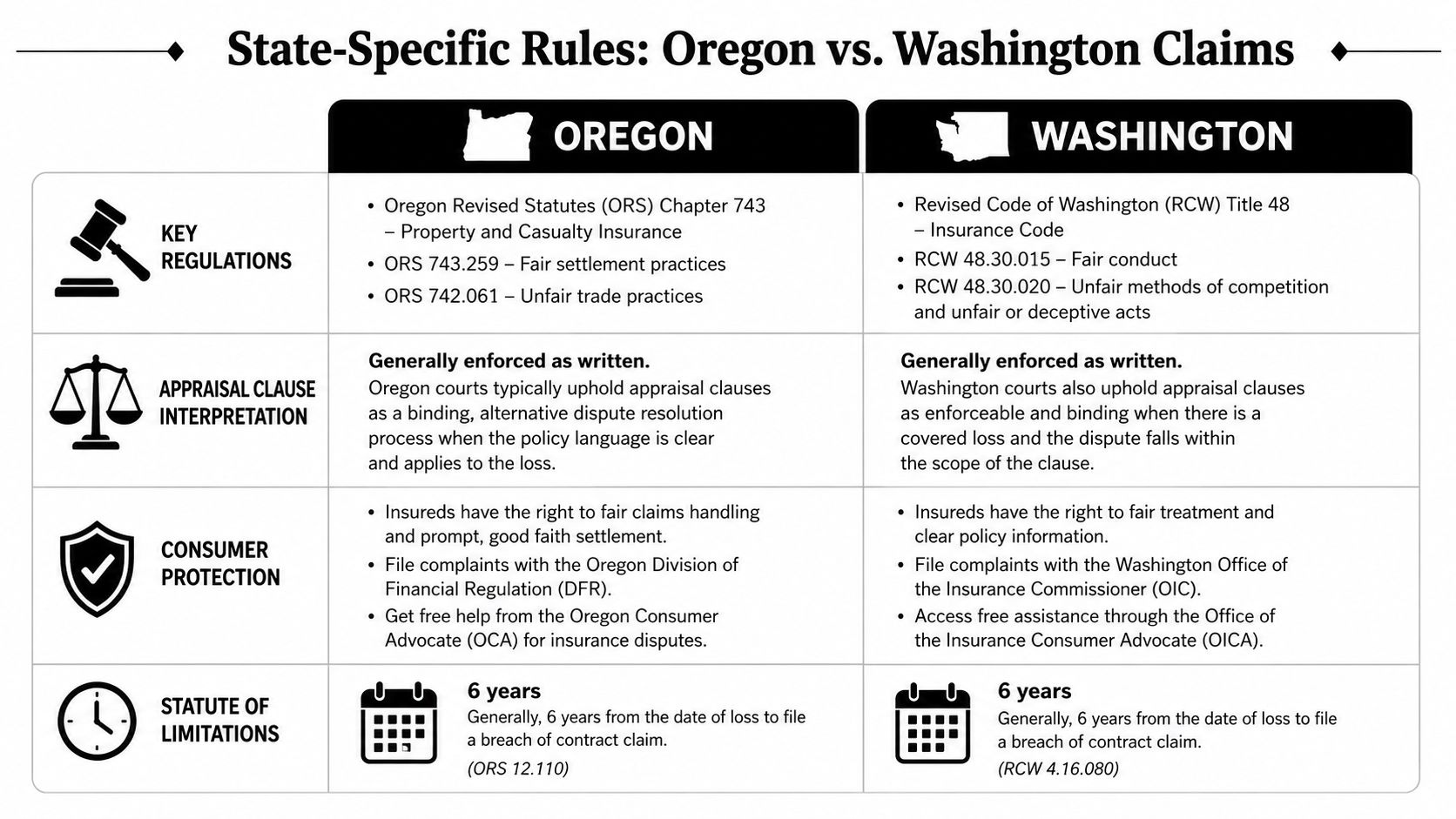

Oregon and Washington Rules and Final Negotiations

In the Pacific Northwest, the biggest mistake I see is assuming there's one mandatory valuation method for every total-loss dispute. That assumption can sink a good claim.

ACV disputes are not just fights about formulas. They are fights about proof and methodology. Legal reporting on a Texas federal court decision noted that insurers were not required by Texas law or policy language to use a specific approach such as comparable-sales, which shows how much these disputes can turn on policy wording and the evidence local law allows, especially for high-value, classic, or custom vehicles, as summarized in this report on ACV methodology disputes.

That case isn't Oregon or Washington law, but the lesson applies directly here. Don't walk into a dispute assuming “fair market value” wins by itself. Build the case around your policy and your evidence.

Oregon and Washington side by side

Here's the practical comparison I give clients.

| Issue | Oregon | Washington |

|---|---|---|

| First priority | Get the valuation report and policy language | Get the valuation report and policy language |

| Best leverage | Appraisal clause if amount of loss is the dispute | Appraisal clause if amount of loss is the dispute |

| Common risk | Accepting software-based comps too quickly | Letting condition and option errors go unchallenged |

| Strong cases | Clean documentation, local comps, formal demand | Clean documentation, local comps, formal demand |

I'm keeping that comparison practical on purpose. The exact rule set can shift with policy wording, claim posture, and the facts of the vehicle itself.

What tends to work in the Northwest

In Oregon and Washington, I've found these strategies consistently stronger than generic advice like “get more quotes”:

- Use regional comps, not random internet listings. A Seattle-area or Portland-area vehicle market can differ sharply from outlying markets.

- Document trim and option scarcity. This matters on trucks, hybrids, performance models, luxury trims, and niche vehicles.

- Move to appraisal when the report is structurally flawed. If the worksheet is built on bad inputs, endless back-and-forth rarely fixes it.

- Treat custom and collector vehicles as special cases. Standard valuation software often misses rarity, documented upgrades, or local demand.

If your vehicle is high-value, classic, or heavily optioned, you should assume the default software report may miss something important until proven otherwise.

Final negotiation posture

Once your evidence file is ready, your final negotiation shouldn't sound like a plea. It should sound like a record.

A strong closing response usually does three things:

- identifies the insurer's valuation errors

- attaches corrected market evidence

- states a deadline for revised review or confirms appraisal demand

That's the point where you stop trying to persuade casually and start documenting professionally.

If you're in Oregon or Washington and the insurer is holding to a weak ACV number, Total Loss Northwest provides certified independent total-loss appraisals and appraisal-clause support built around actual vehicle market evidence, not carrier software shortcuts. If you want to know whether your dispute is strong enough to push, get the report reviewed before you sign, cash, or concede anything.