You open the claim email expecting a number that will let you replace your car. Instead, you get a settlement figure that doesn't come close to what similar vehicles are selling for in your area. That's the moment most drivers realize something important. The insurer's number isn't the same thing as your vehicle's real market value.

I've seen this pattern over and over in total loss claims. The report looks official. The valuation vendor has charts, adjustments, and comparable vehicles. But once you read it closely, the weak points usually show up fast. Wrong trim. Bad mileage match. Distant listings. Generic condition deductions. Local market changes that never made it into the software.

If you're dealing with a low total loss offer, the key issue isn't whether the insurer used a process. They did. The key issue is whether that process measured what it should have measured: what it would cost to buy a comparable replacement vehicle in your real local market now.

What Is Vehicle Market Valuation

A total loss usually starts with a simple sentence from the carrier: your vehicle is not repairable economically, so they're offering Actual Cash Value, often shortened to ACV. Most drivers hear that and assume it means some fixed, objective number. It doesn't.

In practice, vehicle market valuation is the process of estimating what your vehicle would have sold for immediately before the loss, based on the actual market for a similar replacement. That's close to what many people mean by fair market value. If you want a plain-English breakdown of that concept, this fair market value explanation is a useful starting point.

What the number is supposed to represent

Your car's value is not:

- What you paid for it last year

- What you still owe on the loan

- What a guidebook says in the abstract

It's the amount required to obtain a comparable vehicle in your market, with comparable age, mileage, trim, equipment, and condition.

That distinction matters because the broader auto market is enormous. The global car and automobile sales market is projected to reach US$4.3 trillion in 2026, which shows how much money turns on accurate valuation for insurers, lenders, dealers, and consumers handling total loss claims, according to this automotive market projection.

Why your first offer often isn't the last word

The insurer's initial offer is usually framed as if it's the answer. It's not. It's a position in a negotiation.

Practical rule: If the number wouldn't let you buy a comparable replacement vehicle locally, the valuation deserves scrutiny.

That's the mindset shift you need. You're not asking for a favor. You're challenging whether the insurer measured the right market and the right vehicle.

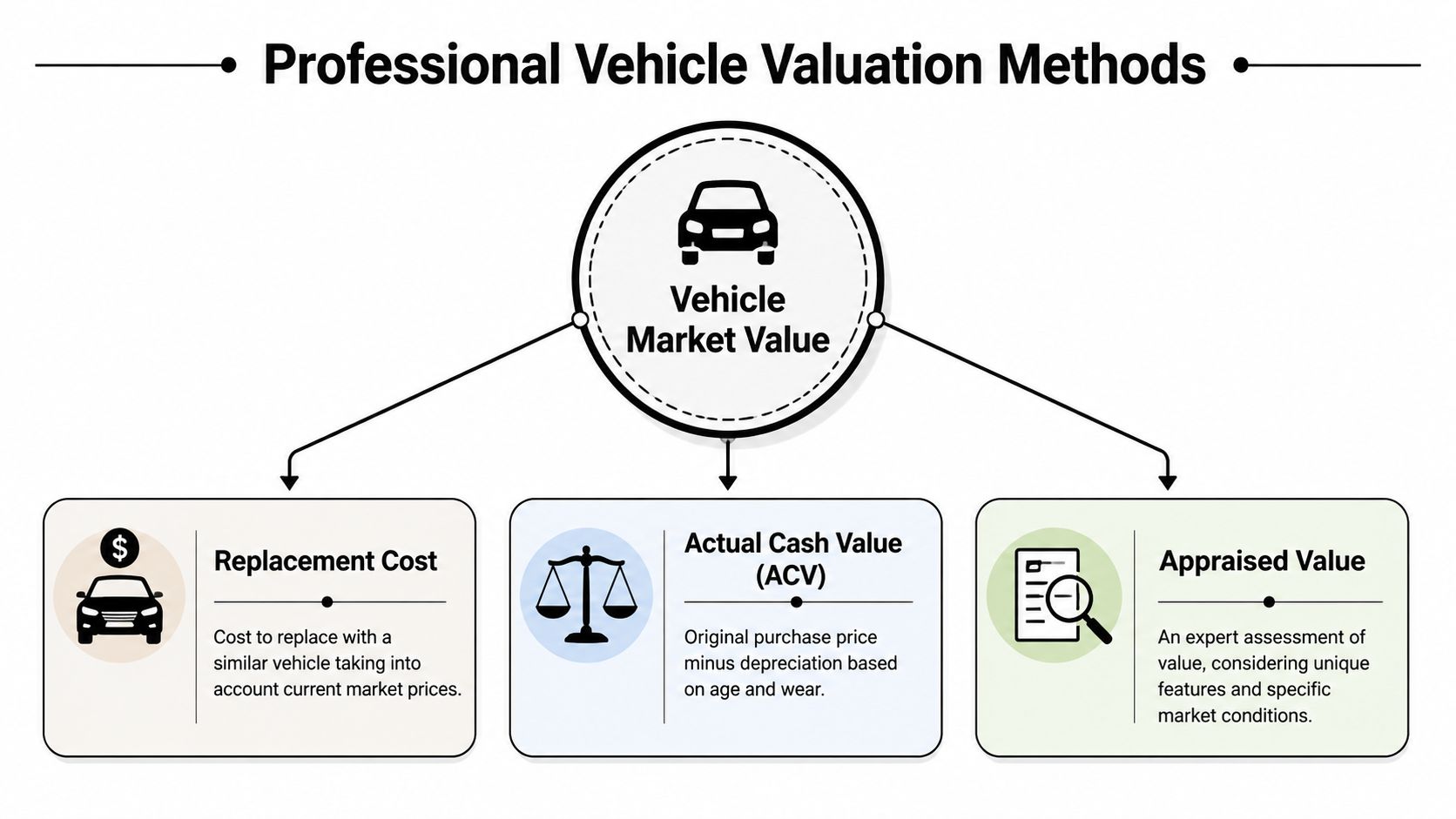

How Vehicle Value Is Professionally Determined

Professional vehicle market valuation isn't one tool or one number. It's a mix of methods. Good appraisers compare those methods against each other instead of treating any single output as final.

Comparable sales are the strongest foundation

The closest analogy is real estate appraisal. A house isn't valued by guessing what homes should cost. It's valued by looking at what similar homes have recently sold for nearby. Cars work the same way.

If I'm valuing a vehicle properly, I want comparables that match the make, model, year, trim, drivetrain, major packages, mileage range, and local market area as closely as possible. Comparable vehicles show what buyers are willing to pay, not what a formula predicts in the abstract.

Guides are useful, but they are not the market

Kelley Blue Book, NADA-style references, and consumer-facing calculators can help establish a rough range. They are useful as orientation tools. They are weak as final proof in a dispute because they flatten important differences between vehicles.

A guide value is similar to a home estimate online. It can be directionally helpful. It can also miss the exact options, regional demand, or real-time pricing pressure that separates one vehicle from another. That's why a deeper guide on calculating fair market value matters more than any single book figure.

The hybrid method professionals trust

A robust valuation combines market comparables with an automated valuation model, or AVM. That hybrid approach is more accurate than relying on one method alone because comparables reflect real buyer behavior while AVMs can process broad datasets such as listings, historical sales, trim details, and depreciation patterns, as described in this overview of hybrid car valuation methods.

Here's what each method does well:

| Method | What it does well | Where it falls short |

|---|---|---|

| Comparable listings and sales | Shows current asking or transaction behavior in the local market | Requires careful matching and judgment |

| Valuation guides | Gives a quick reference range | Often too generalized |

| AVM software | Processes large datasets quickly | Can miss unusual local shifts or unique vehicle features |

The best valuation work doesn't ask, “What does the software say?” It asks, “Does the software output match the real replacement market?”

Retail value and wholesale value are not the same

Many claimants get blindsided by the distinction between dealer retail pricing and auction-style wholesale pricing. These two valuation methods answer different questions. If you need to replace your vehicle from the consumer market, retail comparables often matter more than lower wholesale-oriented figures.

Insurers know that distinction. You should too.

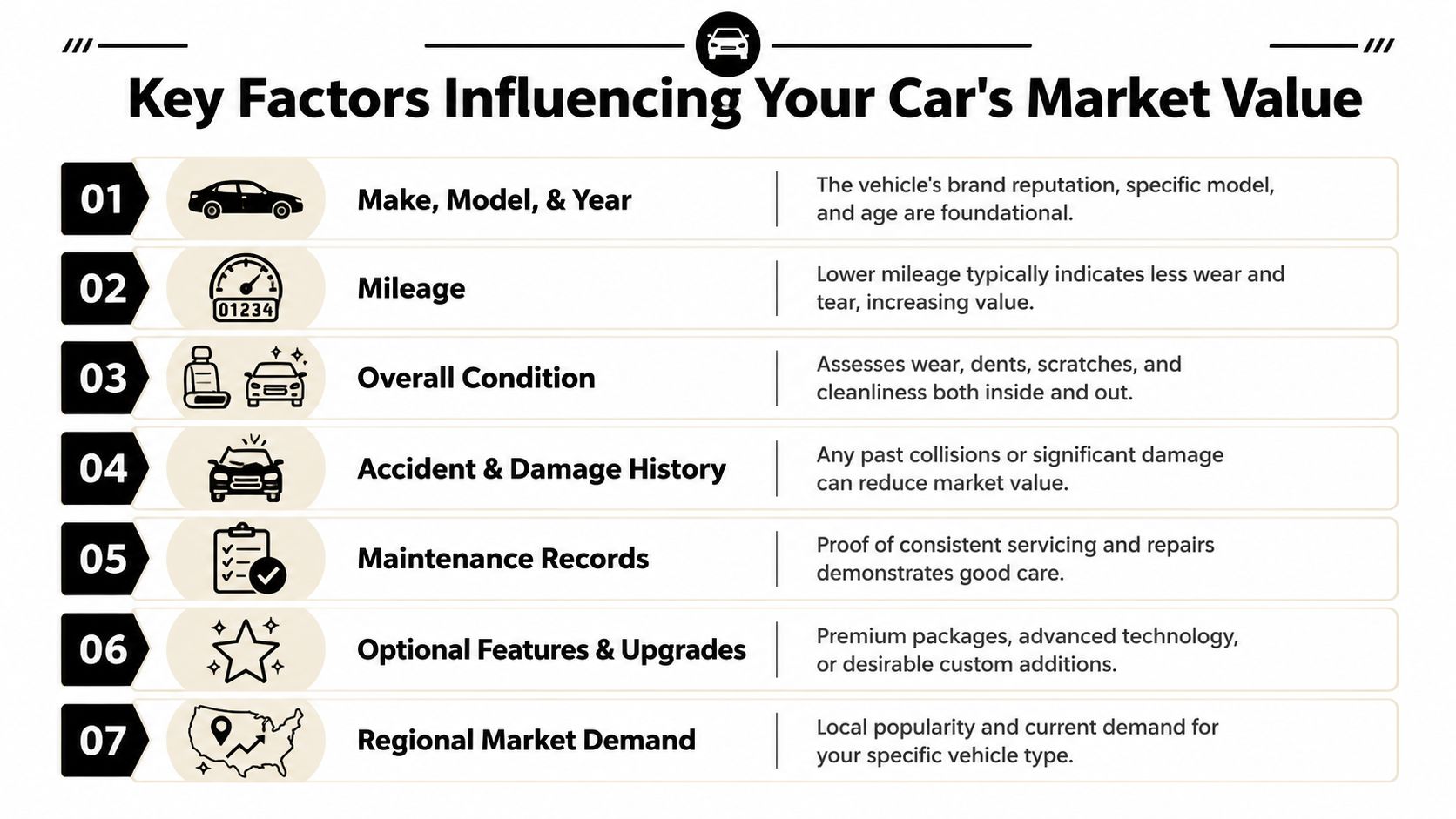

The Key Factors That Determine Market Value

Two vehicles can look almost identical at a glance and still have meaningfully different values. That gap usually comes from details that broad software models compress or miss.

The obvious factors still matter

Start with the basics. They drive the first layer of value.

- Year, make, and model: A common model with stable demand behaves differently from a niche model with fewer local comps.

- Mileage: Mileage affects wear, buyer perception, and the expected remaining life of major components.

- Trim level: A base trim and a loaded trim are not interchangeable. Leather, driver-assist packages, premium audio, towing equipment, and factory technology packages all affect replacement cost.

Condition also matters, but condition has to be handled carefully. Normal wear for age is not the same thing as prior body damage, torn upholstery, poor paint, or neglected maintenance. Yet many insurer reports apply broad condition adjustments as if they were proven facts.

The details that often swing a dispute

The strongest valuation challenges usually come from factors the insurer didn't document well:

- Service history: Recent brakes, tires, transmission work, suspension work, or major engine service can influence what a buyer would pay.

- Factory options: Original equipment matters because many listings don't fully disclose package differences.

- Title and history condition: A clean history doesn't automatically make a car exceptional, but prior damage or title issues can pull value down.

- Regional demand: A truck, AWD crossover, or specialty performance car can trade differently depending on where you live.

A bad comp doesn't become a good comp just because it's in the same model family.

Volatile markets expose weak valuation habits

The post-2020 market showed exactly how fast used vehicle values can move. Some used car segments saw values increase by over 40%, which is why stale guide values or lagging systems can miss the market badly, as shown in this Philadelphia Fed conference presentation on used vehicle price swings.

When values move that fast, a report built from delayed inputs can understate replacement cost even if it looks polished.

Standard methods break down with unusual vehicles

Collector vehicles, highly optioned trucks, modified cars, and special-use vehicles often don't fit standard templates. The more unique the configuration, the less reliable a generic model becomes.

In those cases, the central question isn't just market value in the broadest sense. It's whether the claimed benchmark reflects what it would require to replace that specific vehicle configuration in the current market.

How Insurers Calculate Value and Common Pitfalls

Most insurers don't sit down and manually appraise your car from scratch. They usually order a third-party valuation report through software platforms and vendor systems that standardize the process. That makes claims handling faster. It doesn't make every report accurate.

The common problem is that people treat the report as objective truth because it's formatted like a technical document. In reality, it's an output built from assumptions, data selection choices, and adjustment rules. If those inputs are weak, the final number is weak too.

Where the report often goes wrong

The first issue is market lag. Insurer valuation systems often rely on datasets that don't fully keep pace with a fast local market. When local asking prices or transaction behavior change quickly, the report can understate actual replacement cost.

The second issue is generic condition adjustments. Many reports deduct value for prior wear, paint condition, interior condition, or tires without any credible proof that the deduction matches your vehicle's true pre-loss condition.

A third issue is poor comparable selection. I routinely see reports built on vehicles that are technically similar but not meaningfully comparable.

Common examples include:

- Wrong trim: The report values your premium trim against a lower trim with fewer factory features.

- Bad geography: The listed comparable is far enough away that it doesn't reflect your buying market.

- Mileage mismatch: The comp has materially different mileage and the adjustment doesn't bridge the gap well.

- Inferior equipment: The comp lacks a towing package, upgraded safety suite, premium wheels, or other options your vehicle had.

- Condition mismatch: The comp is rougher than your car was, but the report still treats it as an equal.

According to this analysis of insurance valuation undervaluation issues, insurer valuation systems often suffer from market lag and use generic condition adjustments, which can systematically understate value when local sale prices move faster than software updates.

Why the software favors lower numbers

Insurance valuation systems are designed for consistency and speed. Those goals matter to carriers. They do not always align with the policyholder's need for a market-accurate replacement figure.

That's why wholesale-leaning data, broad condition deductions, and thin option matching can push the number downward without looking obviously unfair on page one. You have to audit the report line by line.

Don't argue with the report at a high level. Attack the exact comp selection, the exact options, and the exact adjustments.

What gets ignored after a collision

Some value-related issues show up before a vehicle is totaled. If repair decisions involved replacement parts, documentation about original equipment can matter in broader claim discussions. For a practical overview, this resource on OEM auto parts information for Kona explains how part type disputes can affect the quality and economics of an insurance claim.

Recent repairs can also be overlooked. If you installed new tires, completed major service, or replaced expensive factory components shortly before the loss, the software may not give that evidence much weight unless you force the issue with records.

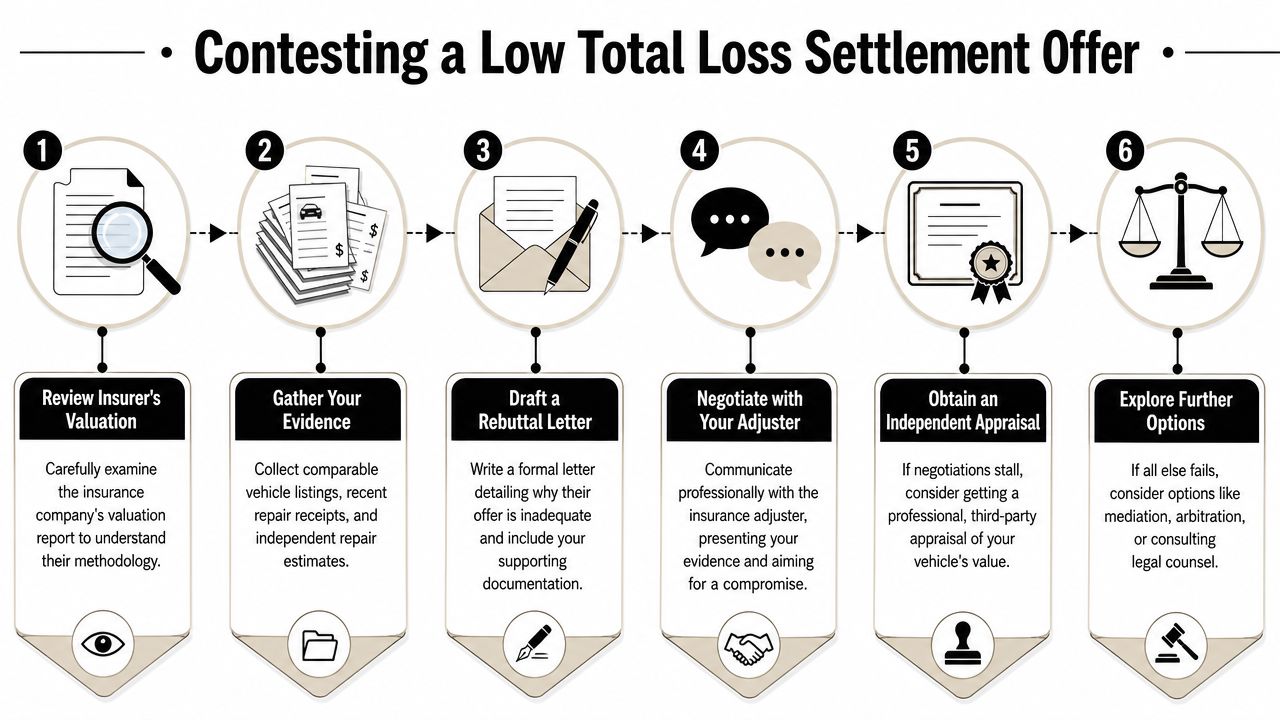

How to Contest a Low Total Loss Offer

If the offer is low, your first move is simple. Don't sign a release, cash a check that could waive rights, or transfer title until you understand the valuation basis. Once you give up your advantage, it's harder to fix a bad number.

Start by demanding the full valuation report, not just the settlement summary. You want the comparable vehicles, the adjustments, the condition ratings, the option list, and any taxes or fees the report includes or excludes. Read it like an auditor, not like a customer.

Build your response in writing

Phone calls are useful for quick clarification. Real disputes need a paper trail.

A strong written rebuttal usually does three things:

- It identifies each problem in the insurer's report.

- It attaches better evidence.

- It states the value range you believe reflects the true replacement market.

If you want a clean template for documenting settlement terms later in the process, this download free settlement agreement resource can help you understand how these documents are structured.

Use an independent appraiser when the dispute is technical

If the vehicle is modified, unusually equipped, high-value, or hard to replace, a standard carrier report may never get you where you need to be. For special-use, high-value, or modified vehicles, standard methods are often inadequate because the key question becomes whether the benchmark should be generic market value or actual replacement cost for that specific configuration, as discussed in this overview of appraisal issues for unusual vehicles.

That's where an independent appraiser becomes useful. Their job is to value the vehicle itself, not defend the insurer's software.

One option in this space is Total Loss Northwest, which provides independent total loss appraisals and appraisal clause support for disputed valuations.

A quick explainer on the process helps here:

Know when to invoke the appraisal clause

Many auto policies contain an appraisal clause. When you and the insurer disagree on value, that clause may allow each side to hire an appraiser, with a neutral umpire resolving any remaining gap.

That changes the posture of the dispute. You're no longer asking the insurer to please revise its own number. You're moving the valuation question into a structured process built for disagreement.

If the dispute turns on technical valuation, the appraisal clause often gives you the cleanest path out of a circular argument with the adjuster.

Assembling Evidence to Prove Your Vehicle's True Value

Weak evidence gets ignored. Specific evidence moves numbers. When you challenge a low total loss offer, your goal is to prove that the insurer's report does not reflect the actual local replacement market for your vehicle.

The strongest package usually combines local comparables, vehicle-specific documentation, and proof of pre-loss condition. If one type of evidence is thin, another can carry more weight, but the best disputes are built from several pieces that point in the same direction.

What makes evidence persuasive

Comparable listings need to be more than the same badge on the hood. A strong comp should be local, recent, and closely matched for trim, mileage, drivetrain, equipment, and overall presentation. Dealer listings are often more persuasive than random marketplace posts because they usually provide VIN-linked equipment details and clearer pricing.

Photos matter more than often realized. If you have clean pre-loss photos showing paint, body panels, interior condition, wheels, glass, and dashboard condition, you can push back against lazy condition deductions with something concrete.

Your vehicle valuation evidence checklist

| Evidence Type | What to Look For and Why It Matters |

|---|---|

| Comparable vehicle listings | Local dealer or marketplace listings for the same year range, make, model, trim, drivetrain, and similar mileage. These show what replacement vehicles are actually being offered for in your area. |

| Original window sticker or build sheet | Confirms factory packages, trim-level content, and optional equipment that generic reports often miss. |

| Maintenance records | Oil service history, brake work, suspension work, timing service, battery replacement, and other upkeep support a stronger condition argument. |

| Major repair receipts | Recent tires, transmission work, engine work, or other substantial repairs can support a higher real-world replacement value than a bare software estimate suggests. |

| Pre-loss photographs | Interior and exterior photos help dispute unsupported condition downgrades. Date-stamped images are especially useful. |

| Title and history documents | Clean title status and consistent ownership records can help confirm the vehicle's market position. |

| Dealer emails or written purchase quotes | Useful when local inventory is thin and dealers can confirm what a comparable replacement would cost. |

| Aftermarket or specialty documentation | For modified or unusual vehicles, receipts and installation records help establish why standard comparables are incomplete. |

How to present it

Don't send a pile of documents with no explanation. Organize the evidence into a short written summary. Match each document to a flaw in the insurer's report.

For example, if the report used a lower trim, attach your build sheet. If the report made a condition deduction, attach photos and service records. If the report used distant comps, attach closer ones and note why they're better matches.

That's how you turn information into an advantage.

Take Control of Your Vehicle Market Valuation

The insurer's first number feels final because it arrives in a formal report with a deadline attached. It isn't final. It's a valuation position, and some of those positions are built on weak comps, stale market data, and unsupported deductions.

Vehicle market valuation only works when it answers the right question. What would it cost to replace your vehicle with a comparable one in your actual market, based on the vehicle you really owned, not a stripped-down version of it? If the insurer didn't answer that question correctly, the offer deserves to be challenged.

Your advantage comes from specifics. Better comps. Better documentation. Better proof of condition. And when the disagreement becomes technical, an independent appraisal can move the dispute out of the insurer's black box and into a process with clearer rules. If you're weighing that option, this explanation of what an appraisal for a car is and why you need one is worth reading.

You don't need to accept a low number just because software produced it. You need to test it, document the problems, and push the valuation back toward the actual market.

If you're facing a low total loss offer and need a defensible value backed by real comparables, Total Loss Northwest provides independent auto appraisals and appraisal clause support for Washington and Oregon vehicle owners, along with diminished value support nationwide.