The call usually goes the same way. Your adjuster tells you the vehicle is a total loss, sounds sympathetic for about thirty seconds, then sends a valuation report that doesn't come close to replacing what you had. You start checking listings. Everything similar costs more. Now you're angry, rushed, and worried you're about to get pushed into a bad settlement because you need a car.

That reaction is justified.

I've seen this from the appraiser's side. Drivers assume the insurance company's number must be official, final, or backed by some flawless system. It isn't. It's an offer built from a method, and methods can be wrong. If the method is wrong, the number is wrong.

Fair Market Vehicle Valuation is the battleground in a total-loss claim. If you understand how that value should be built, you stop arguing from emotion and start arguing from evidence. That changes everything.

Your Car Is Totaled What Happens Next

A total-loss claim moves fast on purpose. The insurer wants the file closed, the storage yard cleared, and your settlement accepted before you've had time to study the report. Most drivers are still dealing with the crash itself when the valuation arrives.

The first number often feels insulting because it usually is lower than what it would cost to get back into a comparable vehicle. That gap is where disputes start. It's also where many people give up too early.

The first offer is not the last word

Your adjuster may talk as if the valuation report is a finished product. It isn't. It's the insurer's position. You're allowed to challenge it, ask how it was built, question the comparable vehicles, and dispute missing options, bad condition ratings, and weak market data.

Your policy is a contract. If the value is disputed, the contract usually gives you a process to challenge it.

You do not need to accept a low number just because it arrived in a polished PDF.

What usually goes wrong right away

Drivers get boxed in by a few common pressures:

- Time pressure: You need transportation now, so the insurer counts on speed working in its favor.

- Information imbalance: The carrier has a report, software, and claim staff. You have a damaged car and a headache.

- False confidence in the report: People assume a computer-generated number must be accurate.

- Fear of sounding difficult: Many drivers worry that pushing back will somehow hurt their claim.

Push that last one out of your head. Challenging a valuation is normal claim handling.

Here's the practical sequence after a total loss is declared:

- Ask for the full valuation report and read every line.

- Do not accept verbally just to “keep things moving.”

- Check the comparables against your actual vehicle.

- Document what the report missed such as trim, packages, condition, recent work, and local market reality.

- Prepare to dispute the value in writing.

Confidence matters here

The insurer's playbook depends on you treating the report like a verdict. It's not a verdict. It's an opening position. If the number won't buy a similar vehicle in your market, you challenge it and make them defend the method.

What Is Fair Market Vehicle Valuation Really

Forget the jargon for a second. If your house were destroyed, you wouldn't accept a number based on what an investor might pay in a distressed bulk deal. You'd care about what it would cost to replace that house on the open market. Your vehicle works the same way.

Fair Market Vehicle Valuation is about what a willing buyer would pay for your vehicle in the open market. In total-loss claims, that idea is tied to Actual Cash Value, or ACV. The important part is not the acronym. The important part is the market the insurer uses to build the number.

Retail value is the benchmark

Industry guidance has long treated retail-market prices as the proper benchmark for ACV. IRMI explains that when a valuation dataset includes wholesale transactions or other non-retail sources, the estimate becomes “contaminated” because it can impair the promise to pay ACV. Read that point in IRMI's discussion of settling total vehicle claims.

That matters because wholesale and auction data can drag a valuation down. A dealer's acquisition number is not the same as your replacement cost in the retail market. Those are different transactions with different economics.

A guidebook number is not enough

A lot of drivers get trapped by “book value” thinking. Kelley Blue Book, NADA, Edmunds, and similar tools can help you orient yourself, but none of them should end the discussion by themselves. Fair market value is a conclusion built from evidence, not a magic number pulled from one database.

A proper valuation looks at the actual vehicle and the actual market. If you want a solid primer on the mechanics, review this breakdown of how to calculate fair market value.

Here's what that means in plain English:

- Your trim matters. Base, mid, and premium trims do not sell the same.

- Your options matter. Factory tech, towing, safety, performance, and appearance packages affect value.

- Your condition matters. Clean interior, straight panels, documented maintenance, and strong tires affect buyer behavior.

- Your local market matters. A good comparable in one region may be a bad comparable for your claim.

Practical rule: If the insurer values your car like an average example, and your vehicle was better than average, the offer is wrong.

The right question isn't “What does a website say my car is worth?” The right question is “What would it take to replace my vehicle with a comparable one in my market, based on real retail evidence?”

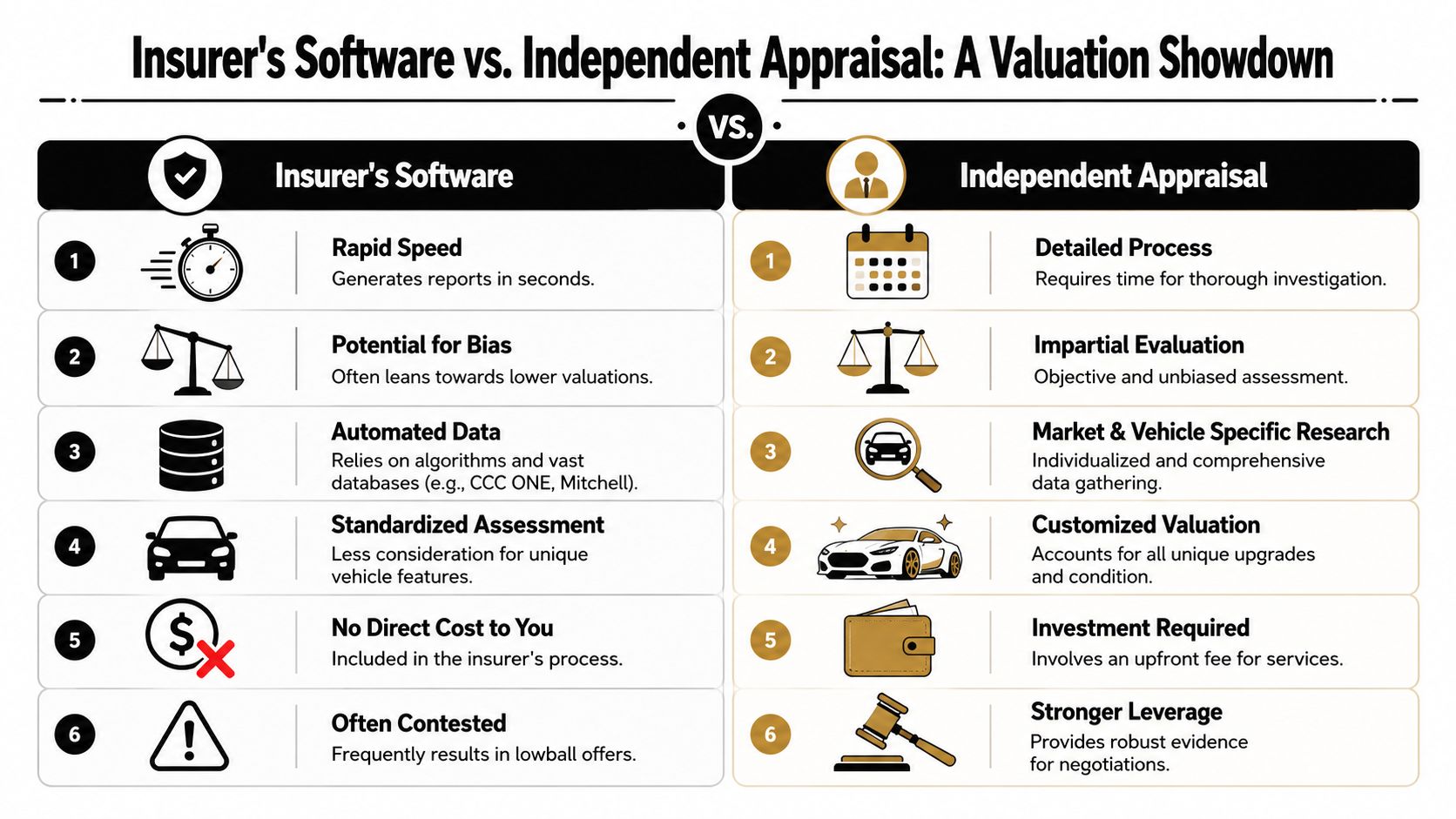

The Insurer's Software Versus an Independent Appraisal

Insurers like automation because it's fast, scalable, and cheap for them. Accuracy comes second. That's the uncomfortable truth behind many low total-loss offers.

When your report is built through valuation software, the software doesn't know your car the way an experienced appraiser does. It knows fields, codes, adjustments, and rules. If those inputs are wrong, the output is wrong too.

What insurer software gets wrong

For total-loss claims, fair market value is typically estimated from comparable sales or listings and then adjusted for mileage, options, and condition. The problem is that even a small error in mileage or option coding can move the final ACV materially, which is exactly why valuation disputes happen, as discussed in Sage's overview of fair market value.

That sounds technical, but the practical failures are basic:

| Insurer software issue | Why it hurts your claim |

|---|---|

| Wrong trim coding | It values a lower-spec vehicle than the one you owned |

| Missed options | It strips value from equipment buyers actually pay for |

| Generic condition adjustments | It ignores unusually clean or well-maintained vehicles |

| Weak comparable selection | It compares your car to poor substitutes |

| Opaque calculations | It's hard to see how the final number was built |

A lot of these reports also hide behind “standard methodology.” Standard doesn't mean fair. It often means standardized enough to move files quickly.

To see how these reports are commonly built and challenged, look at this explanation of CCC auto valuation.

What an independent appraisal does differently

An independent appraisal is slower because it's supposed to be slower. Someone has to inspect the facts, verify the trim and options, evaluate the pre-loss condition, and locate stronger comparables.

That process should include:

- Vehicle-specific review: Year, make, model, trimline, equipment, mileage, and condition are checked against the actual car.

- Market-specific research: Comparable vehicles should reflect the market where replacement would happen.

- Transparent adjustments: Differences between the comps and your vehicle should be explained, not buried.

- Support for dispute resolution: A written appraisal gives you evidence, not just complaints.

Here's a checklist worth following before you push back.

If you want a broader explanation of how valuation disputes unfold, this video is useful:

My advice as an appraiser

Don't argue with software by saying the offer “feels low.” Argue with it by showing exactly where it missed the vehicle, the market, or both.

A black-box report can produce a number quickly. It cannot defend that number well when the wrong comps, wrong options, or wrong condition calls are exposed.

That's why a second opinion isn't overreacting. In many claims, it's the first serious step.

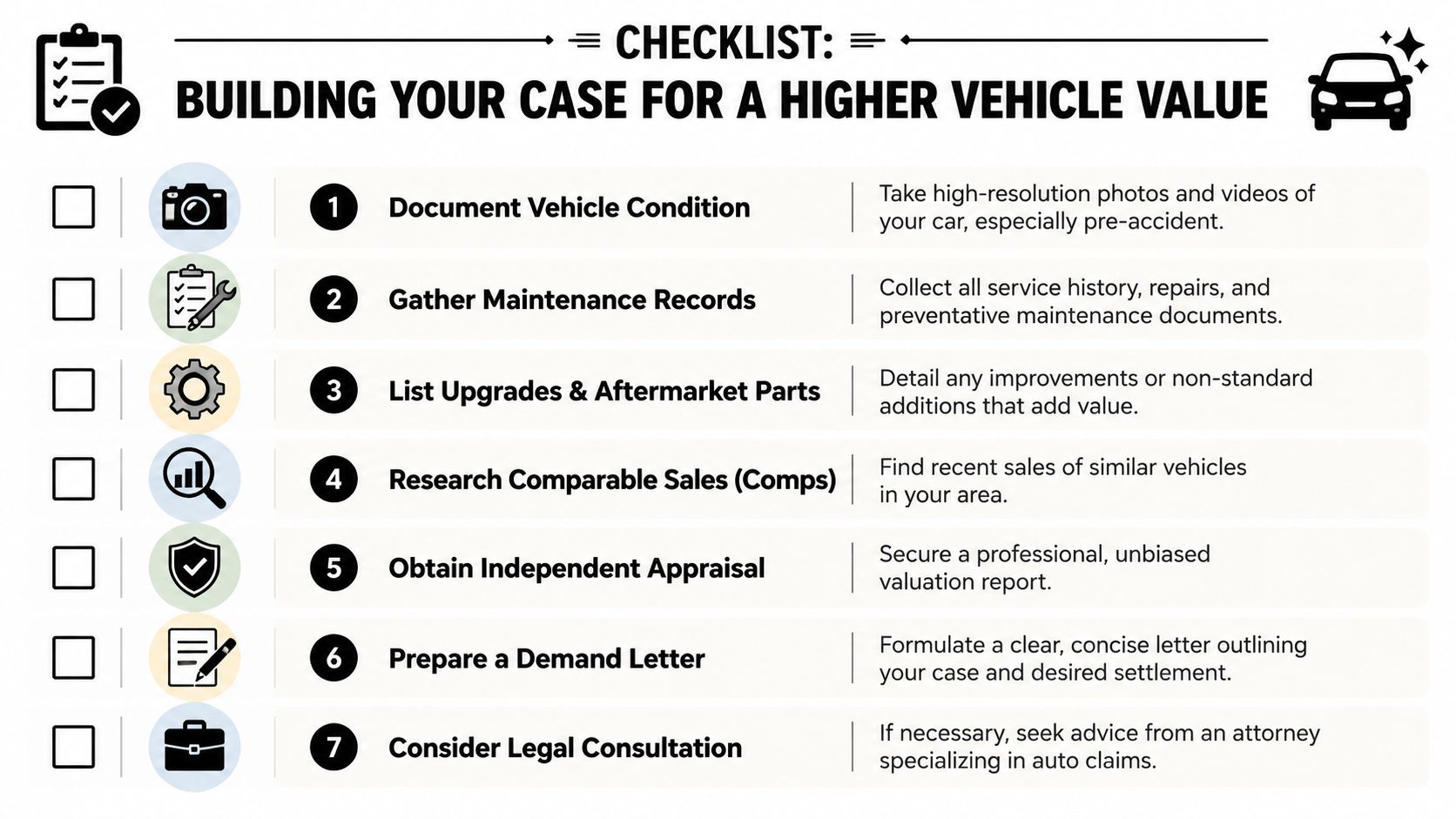

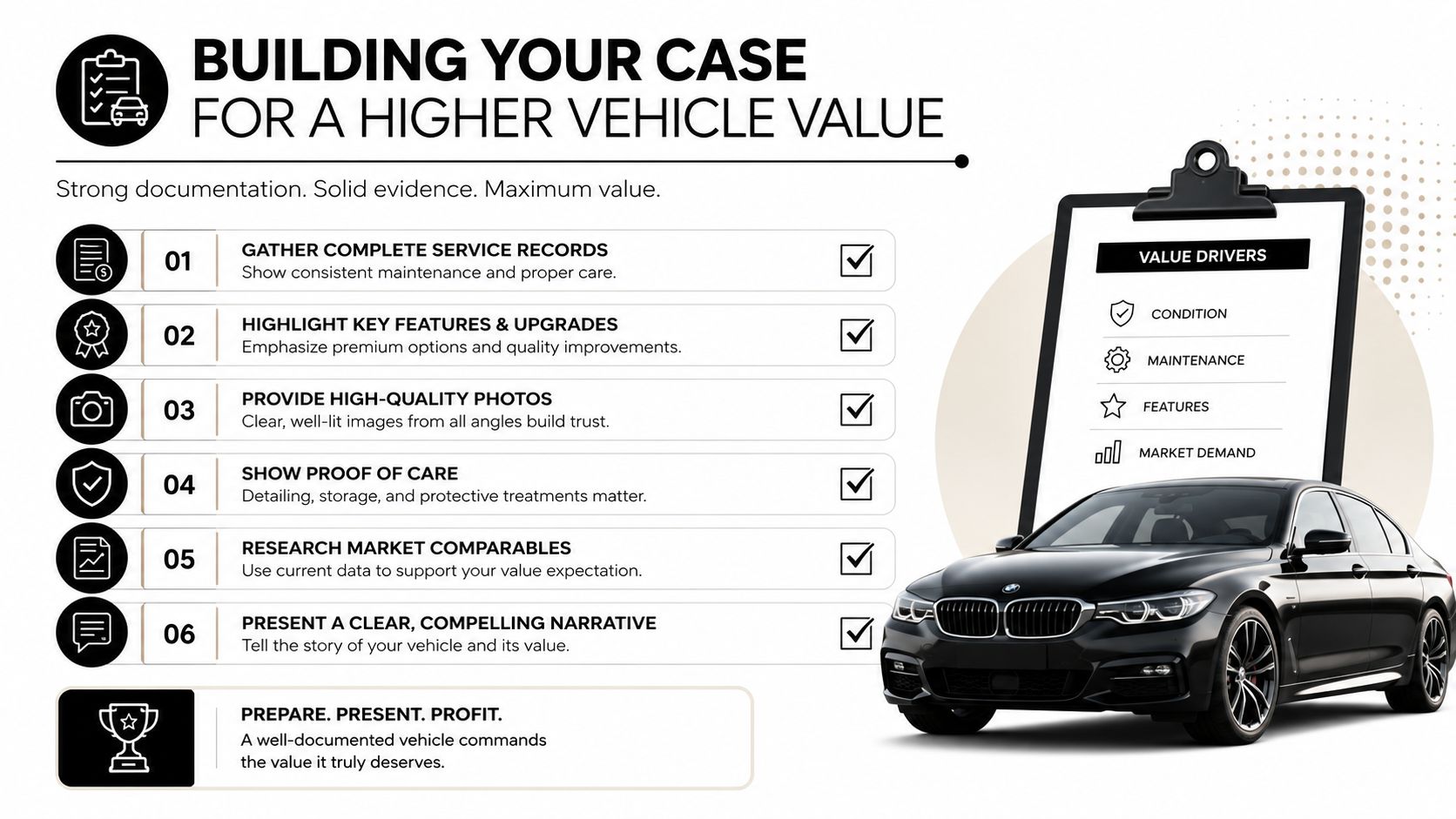

Building Your Case for a Higher Vehicle Value

Most drivers find their position strengthened or weakened at this crucial point. If you only tell the insurer your car was “really clean” or “loaded,” you won't get far. You need proof.

Modern valuation tools rely on detailed inputs including year, make, model, trimline, mileage, condition, and additional options, according to Consumer Reports' car value estimator. That's why two vehicles that look identical to a casual observer can produce different values. Documentation wins these arguments.

Build your file like an appraiser would

Start gathering anything that proves your vehicle was better equipped, better maintained, or better presented than the insurer assumed.

Prioritize these items:

- Photos before the loss: Exterior, interior, wheels, seats, dash, cargo area, and odometer.

- Service records: Oil changes, major maintenance, brakes, tires, suspension work, battery replacement, and dealer service history.

- Option proof: Window sticker, original sale paperwork, VIN decoder information, or manufacturer build sheet.

- Upgrade receipts: Wheels, tires, audio, towing equipment, bed covers, performance parts, or appearance packages.

- Comparable listings: Retail listings for similar vehicles in your area.

Don't let “average condition” sink the value

Insurance reports often flatten vehicles into average buckets because average is easy. Your job is to show your vehicle wasn't average if it wasn't.

A clean file can support arguments like these:

- The report missed a higher trim.

- The report omitted factory or dealer-installed equipment.

- The condition adjustment was too harsh.

- The mileage entry was wrong.

- The selected comparables were weaker than the actual market.

If you need a simple way to think about presentation, some of the same habits that help preserve resale value also help you document condition after a loss. This guide on expert tips to sell your car is useful because it shows what buyers notice first, which is often what valuation reports undervalue.

What to send with your dispute

Keep your response organized. Don't dump random screenshots into an email.

Use a clean packet with:

- A short letter stating the insurer's valuation is inaccurate.

- A list of factual errors in the report.

- Documents proving trim, options, condition, and maintenance.

- Your stronger comparable listings.

- A request for revision or appraisal.

That format tells the adjuster you're not guessing. You're building a record.

How to Invoke the Appraisal Clause in Your Policy

Your adjuster keeps repeating the same number. You keep sending proof. Nothing changes.

Stop treating that as a negotiation. It is a value dispute under your policy, and the policy usually gives you a procedure to force that dispute out of the adjuster's inbox and into appraisal.

The Appraisal Clause exists for this exact fight. If you and the insurer disagree on the amount of loss, each side selects an appraiser. If those appraisers cannot agree, an umpire is brought in. The issue is the vehicle's value, not who caused the crash.

Why this clause matters

Insurance companies want valuation disputes handled on their timeline, inside their system, with their report as the starting point. That keeps pressure on you to accept less and move on.

Appraisal changes the terrain. It puts the claim into a contract-based process with defined roles and a record. You stop asking the insurer to be more reasonable. You require them to follow the policy they sold you.

Independent valuation also matters because software misses things. Thin market data, rare trims, heavy option packages, strong condition, recent work, and local retail pricing can all be undervalued by mass-market reports. Appraisal gives those facts a formal place to be considered, as explained in Appraisal Engine's discussion of fair market value in insurance claims.

How to find and use it

Get your declarations page and full policy. Search for:

- Appraisal

- If we disagree

- Amount of loss

- Dispute resolution

Then read the clause carefully. Deadlines, notice requirements, and who pays each appraiser can vary by carrier and state.

If you want a plain-English breakdown of the process before you send your notice, review this explanation of the insurance appraisal clause process.

What your written demand should say

Keep it tight. The goal is clarity, not drama.

Your letter or email should say:

- You dispute the insurer's total-loss valuation.

- You are invoking the Appraisal Clause under the policy.

- You request the insurer identify its appraiser.

- You are naming your appraiser now, or will do so promptly.

- Future communication about value should go through the appraisal process.

Send it in a way you can document. Email is fine if the claim is already being handled by email. Save the message, attachments, and reply.

One sentence can change the posture of the claim: I dispute your valuation and hereby invoke the Appraisal Clause in my policy regarding the amount of loss.

When to bring in an independent appraiser

Bring in an independent appraiser once the insurer has had a fair chance to fix obvious errors and still refuses. That is usually the point where more back-and-forth wastes your time.

Use one early if the vehicle is unusual. Specialty trims, collector vehicles, modified trucks, luxury packages, EVs with volatile market pricing, and exceptionally clean examples often get flattened by standard valuation systems.

Total Loss Northwest is one example of a company that provides certified independent appraisals for total-loss and diminished-value disputes and can assist a policyholder with the appraisal-clause process.

Avoiding Common Valuation Pitfalls

Bad outcomes usually come from a handful of repeat mistakes. The details change, but the pattern doesn't.

Pitfall one is accepting too fast

The insurer offers a number. You're tired, need a replacement car, and worry delay will make things worse. So you say yes before checking the report carefully.

That's the easiest money an insurer saves all week.

If you need time, say you're reviewing the valuation and aren't accepting it yet. Keep the claim moving without surrendering your rights.

Pitfall two is using the wrong claim theory

Not every value dispute is a total-loss dispute. If your car was repaired instead of totaled, the issue may be diminished value, meaning the vehicle lost resale value because it now carries an accident history. Drivers miss that claim all the time because they focus only on repairs.

A totaled vehicle raises replacement-value issues. A repaired vehicle may raise post-repair market-loss issues. Know which problem you have.

Pitfall three is trusting generic tools for non-standard vehicles

Mainstream valuation tools often fail when the vehicle isn't ordinary. That includes collector cars, heavily optioned luxury trims, modified trucks, and many EVs. CarEdge notes that used EV prices have shown sharp year-over-year swings through 2024 because of incentives and technology changes, which means a generic comparable can badly misstate the loss. See CarEdge's discussion of fair market value of a car.

That matters because software does fine with average inventory. It struggles when the vehicle's buyer pool, equipment, or market behavior doesn't fit the template.

A short warning list

- Don't argue from emotion only. Frustration is valid, but evidence moves claims.

- Don't send weak comps. A bad comparable can hurt more than help.

- Don't ignore fees and market friction in your own analysis. Real replacement costs don't exist in a vacuum.

- Don't assume the adjuster caught every option. They often don't.

If the car was unusual, your dispute needs to be stronger than a screenshot from a pricing site.

Your Next Steps Toward a Fair Settlement

You don't need to master the whole insurance industry. You need a clean action plan and the discipline to follow it.

Start with the basics and do them in order.

The five moves that matter

Reject the offer in writing

Be polite and firm. State that you dispute the valuation and do not accept the current amount.Request the full valuation report

If you don't have the complete report, get it. You can't challenge what you haven't read.Audit the report line by line

Check trim, mileage, options, condition, and comparable vehicles. Look for anything that pushes the value down unfairly.Build your evidence packet

Organize photos, service records, option proof, receipts, and better comps into one file.Decide whether to escalate to appraisal

If the insurer won't make a fair correction, invoke the contract process and hire independent help.

Stay focused on replacement reality

The only number that matters is the one supported by the actual market for a comparable replacement vehicle. Everything else is noise.

If you want a broader consumer overview while you sort through policy language and claim choices, this guide on understanding your insurance options can help you frame the bigger picture without losing sight of the valuation fight in front of you.

You are not asking for a favor. You are asking the insurer to honor the policy based on a defensible value.

The driver who gets paid fairly is usually the one who stays organized, keeps everything in writing, and stops treating the carrier's first number like a final answer.

If you're dealing with a low total-loss offer and need an independent valuation, Total Loss Northwest can help you challenge the insurer's number with a certified appraisal and, when appropriate, move the dispute through the Appraisal Clause process.