The call or email lands, and your stomach drops.

Your insurer says your vehicle is a total loss. Then the offer arrives. It's lower than what you know your car was worth, lower than what similar vehicles are selling for, and nowhere close to what it will take to replace it without coming out of pocket. You're already dealing with the crash, the rental mess, the missed time, and now they want you to accept a number that feels pulled from thin air.

You're not stuck with that first offer. In Oregon, a low total loss offer is often the beginning of the conversation, not the end of it. If you need a Total Loss Expert Oregon drivers can rely on, the right move is to treat this like a valuation dispute, not a favor request. That mindset changes everything.

The Insurance Offer Is In What Happens Now

The same mistake is often made in the first day or two. They assume the adjuster's number must be close enough, or they panic and sign because they need the money fast. That's understandable. It's also exactly how lowball settlements stick.

A common pattern looks like this: your car is hauled away, the insurer calls it a total loss, and then they send a valuation report filled with “comparable” vehicles that don't match yours. Different trim. Different condition. Different mileage. Sometimes the report ignores recent work or options that matter in the market. You object, and the response sounds polished but final. It isn't final.

If you've ever dealt with insurers on other kinds of claims, the playbook feels familiar. The same pressure tactics show up in auto losses that people see when fighting low-balled property claims. The names change, but the pressure is the same: move fast, trust their math, and don't push back.

The first decision matters

Your first job is simple. Don't treat the initial offer as a verdict. Treat it as a draft.

That means slowing the process down long enough to review the valuation, preserve your documents, and understand what happens after a vehicle is declared a loss. If you need a quick primer on the overall process, this guide on what happens when your vehicle is totaled is a useful starting point.

Practical rule: If the offer feels low, you don't need to “prove they're cheating” before you object. You only need a reason to question the valuation.

What a total loss expert actually does

A seasoned total loss appraiser doesn't just say, “that seems unfair.” They build a market-based challenge. They review the valuation method, the vehicle details, the comparables, and the omissions. Then they turn your frustration into evidence.

That's the difference between complaining and winning. One gets logged in the claim notes. The other forces movement.

What Is a Total Loss in Oregon Anyway

“Total loss” doesn't mean your vehicle is obliterated. It means the economics of repair have crossed a legal line.

In Oregon, a vehicle is legally declared a total loss when repair costs reach or exceed 80% of its Actual Cash Value, combined with its salvage value, under the state's framework explained in Oregon's total loss threshold rules. That threshold matters because it tells you when the carrier should stop talking about repair and start paying based on value.

Actual Cash Value is where the fight usually starts

Actual Cash Value, usually shortened to ACV, is supposed to reflect what your vehicle was worth right before the crash. It isn't a fixed book number. It depends on factors like age, mileage, make, model, condition, and location, as described in the same Oregon threshold explanation above.

That's why two vehicles that look similar at first glance can land at different values. Condition matters. Equipment matters. Local market matters. A clean, well-kept vehicle with documented maintenance and desirable options often deserves more than a generic software valuation suggests.

Why insurers and owners often disagree

The carrier wants a neat valuation file. You need a replacement-level number grounded in the actual market. Those aren't always the same thing.

Here's where things go sideways:

- Mismatch on comparables. The insurer may use vehicles that are not comparable to yours.

- Missed condition adjustments. A vehicle with excellent upkeep can get treated like an average one.

- Ignored equipment. Trim, packages, wheels, tires, audio, safety tech, and other features may not be fully captured.

- Weak local relevance. Listings from a different area may not reflect what your market supports.

A total loss valuation is only as good as the vehicle description and market data behind it. If either one is sloppy, the offer is shaky.

The practical takeaway

If your claim has already been labeled a total loss, stop arguing about emotions and start looking at inputs. The legal threshold determines when the vehicle qualifies. The ACV determines what you get paid. Once the insurer has crossed into total loss territory, the battle is about value.

That's why a Total Loss Expert Oregon drivers hire is usually focused less on crash damage and more on valuation accuracy. The wreck got the vehicle into the total loss category. The appraisal fight decides whether the settlement is fair.

Your Secret Weapon The Appraisal Clause

Most drivers don't realize they already have an advantage sitting inside their own policy.

The Appraisal Clause is one of the strongest tools in a total loss dispute because it lets you challenge the insurer's valuation through an independent appraiser instead of begging the adjuster to rethink the file. This isn't a lawsuit. It's closer to a required second opinion built into the contract.

In Oregon, most auto policies include this clause, and if the independent valuation comes in even slightly higher than the insurer's offer, the insurer is generally required to reimburse the appraiser's fee, as explained in this guide to the appraisal clause for Oregon and Washington total loss disputes.

Why this changes the balance of power

Without the appraisal clause, you're stuck arguing with the same party that created the number you're challenging. That's a bad setup. The insurer has the report, the software, and the confidence that individuals will give up.

The appraisal clause interrupts that pattern.

Instead of saying, “please look again,” you're saying, “I'm invoking my contractual right to an independent valuation.” That language matters. It turns the conversation from persuasion into process.

If you want a fuller breakdown of how it works in practice, this explanation of the auto insurance appraisal clause lays out the mechanics clearly.

Why Oregon drivers should use it sooner, not later

The reimbursement rule is what makes Oregon especially favorable. You're not gambling on a huge swing just to justify the cost. If the independent appraisal beats the insurer's number by even a small amount, the fee reimbursement rule can kick in.

That changes the math for everyday drivers, not just collectors.

- Daily driver owners can challenge weak ACV reports without assuming they're throwing good money after bad.

- Custom vehicle owners can get valuation input from someone who understands modifications.

- Collector vehicle owners can push back against generic comparables that flatten rarity and condition.

The insurer's first number has authority because it arrives first, not because it's automatically correct.

My advice

If the offer feels off and the vehicle mattered to your finances, don't spend two weeks arguing in circles with an adjuster. Review the policy. Confirm the clause. Then move the dispute into appraisal before the file hardens and the pressure ramps up.

That's the point where a total loss claim stops being a stressful phone call and becomes a structured valuation challenge.

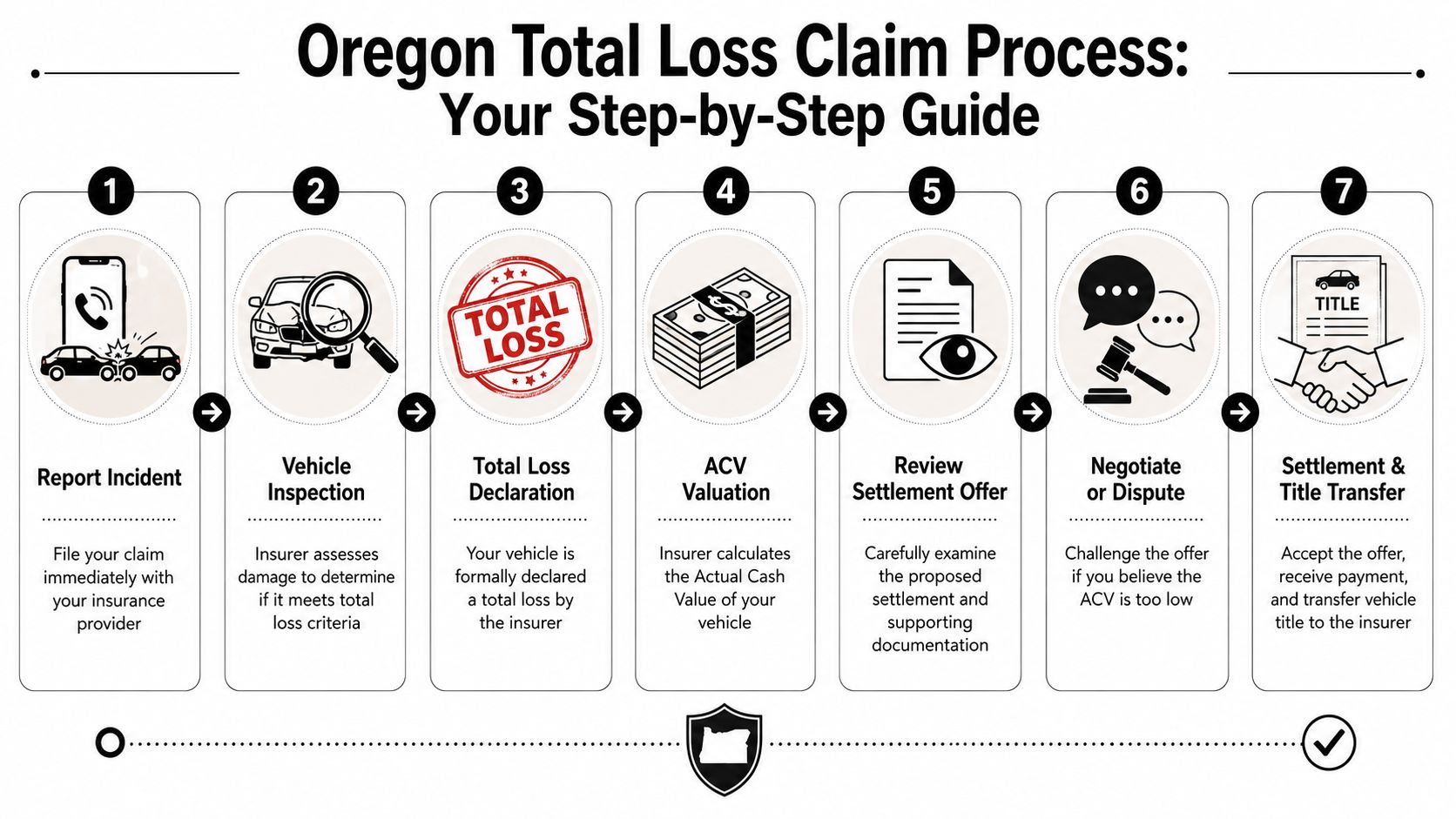

The Total Loss Claim Process Step-by-Step

A lot of drivers freeze because the process feels murky. It isn't. Once you know the sequence, the claim becomes manageable.

Start with the basics and stay organized from day one.

Step 1 Hold your position

If you receive an offer that looks low, don't accept it out of panic. Don't tell the adjuster you “guess that's fine” on a recorded call. Don't sign release documents until you understand what's being paid and what's being left out.

A rushed acceptance is the cleanest exit the insurer can get.

Step 2 Ask for the valuation report and support

You need the documents behind the number. Request the valuation report, the comparable vehicles used, the condition ratings, and any adjustments they made.

Read it slowly. Check trim level, drivetrain, mileage, options, pre-loss condition, and whether the comparables are even credible. A bad report often exposes itself once you stop skimming.

Step 3 Build your own file

Start gathering the records that show what your vehicle was worth before the crash. Service history, recent receipts, photos, feature lists, and anything that shows the true condition belong in one folder.

At this point, many owners finally see the difference between their real car and the insurer's generic version of it.

Step 4 Put your objection in writing

Keep this simple and direct. Tell the insurer you dispute the valuation and want the claim reviewed. If you're invoking the appraisal clause, say so clearly and in writing.

Email is usually the cleanest channel because it creates a date-stamped record. Be polite. Be firm. Don't write a rant.

Put every meaningful objection in writing. Phone calls disappear into claim notes you may never see.

A short video can help if you're trying to get your bearings before sending that notice:

Step 5 Get an independent appraiser involved

This is the moment to bring in a professional. A skilled appraiser doesn't just search random listings. They evaluate the vehicle description itself, test the insurer's comparables, and build a value conclusion that can stand up in a dispute.

If your vehicle was unusual, upgraded, collector-grade, or better than average for its age, this step is even more important.

Step 6 Review the appraisal outcome carefully

Once the independent valuation is prepared, compare it against the insurer's offer line by line. Don't focus only on the headline number. Look at whether fees or other claim components were omitted.

The strongest disputes aren't just “your number is too low.” They're “your number is too low for these specific reasons, and here is the corrected value basis.”

Step 7 Close the claim on full terms

When the settlement is corrected, confirm exactly what the payment includes before signing off. Make sure the paperwork matches the agreed valuation and any added amounts that were part of the dispute.

Use this process checklist as your working map:

| Step | What to do | Why it matters |

|---|---|---|

| 1 | Pause before accepting | Keeps you from locking in a weak settlement |

| 2 | Request the valuation file | Lets you inspect the insurer's logic |

| 3 | Gather records and photos | Supports condition, features, and upkeep |

| 4 | Object in writing | Creates a paper trail and triggers review |

| 5 | Hire an independent appraiser | Brings in market-based valuation support |

| 6 | Compare reports closely | Identifies where the offer falls short |

| 7 | Confirm final terms | Prevents last-minute omissions |

The process isn't pleasant, but it is workable. Once you stop reacting and start documenting, the claim gets less intimidating.

Your Fair Settlement Documentation Checklist

When people say, “I have proof my car was worth more,” what they usually mean is they have a few memories and maybe a receipt. That's not enough. You need organized support.

The good news is the right file isn't complicated. It's just specific.

What to gather before you dispute value

Use this checklist and assemble everything in one place before you send a long objection email.

| Document/Item | Why It's Important |

|---|---|

| Title or registration | Confirms the exact vehicle identity and ownership details |

| Insurance policy declarations and policy language | Helps confirm whether an appraisal clause applies |

| Insurer valuation report | Shows the comparables, assumptions, and errors you may challenge |

| Crash report or claim number information | Keeps claim details aligned across documents |

| Pre-accident photos | Proves condition, appearance, and installed features |

| Odometer reading or recent service paperwork showing mileage | Supports accurate mileage at the time of loss |

| Maintenance records | Shows upkeep and supports above-average condition |

| Receipts for recent repairs | Documents money spent shortly before the loss |

| Receipts for tires, wheels, audio, accessories, or upgrades | Helps prove added value and equipment the insurer may ignore |

| Original window sticker, build sheet, or purchase documents | Identifies trim, packages, and factory options |

| Loan or lease payoff information | Clarifies what must be satisfied from settlement funds |

| Notes from calls and copies of emails | Creates a record of what the insurer said and when |

What people forget most often

Two things get missed constantly.

- Photos taken before the crash often show condition better than any written description.

- Receipts for recent work matter because they show the vehicle wasn't neglected.

Keep your file boring and clean. PDFs, labeled photos, dated receipts, and a simple timeline beat a chaotic stack of screenshots.

A strong documentation package doesn't guarantee a fight. It often prevents one by showing the insurer you're prepared.

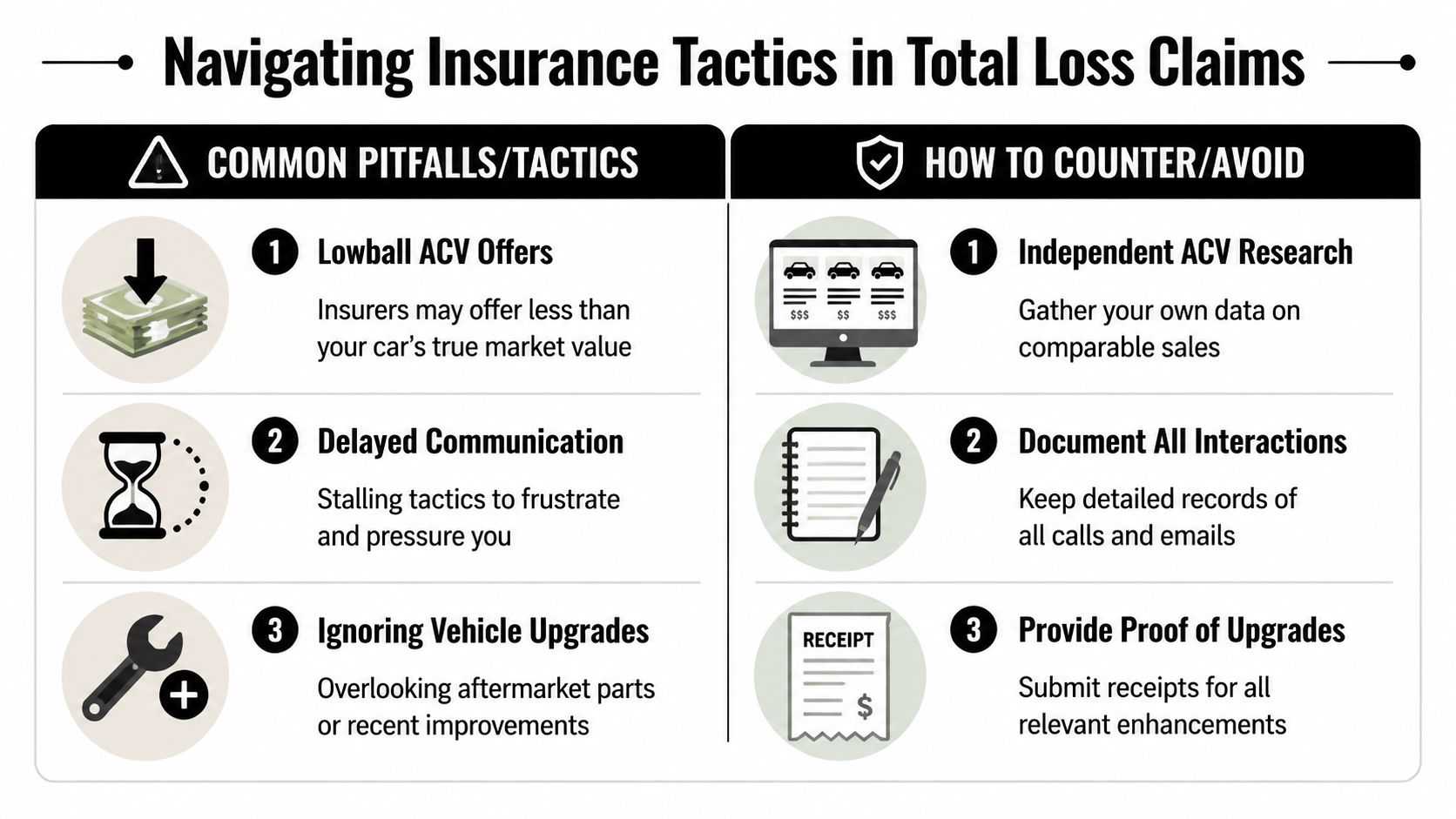

Common Pitfalls and Insurance Company Tactics

Insurers count on confusion. They don't need you to agree enthusiastically. They just need you to go along.

That's why the most expensive mistakes in a total loss claim usually happen early, when the owner is tired, rushed, and trying to be reasonable.

The traps I see most often

Some are obvious. Some are subtle.

- Verbal acceptance. You say something casual on the phone, and the adjuster treats it like agreement.

- Cashing too fast. You deposit the check before confirming what rights you may be giving up.

- Arguing without documents. You insist the offer is wrong but send nothing concrete.

- Focusing only on the headline number. You miss fees or related amounts that should be part of the payout.

- Letting delays wear you down. Repeated “we're reviewing it” responses are designed to make a low offer feel easier to accept.

The one-cent rule is more powerful than it sounds

For Oregon drivers with higher-value, collector, or custom vehicles, one of the smartest strategies is also one of the least understood.

A little-known approach described in this discussion of Oregon total loss disputes and the one-cent rule is that any increase in the settlement can trigger appraiser fee reimbursement, and that this increase can also be employed to push for Tax, Title, and Licensing fees that may be left out of the initial offer. The point isn't that a tiny increase is meaningful by itself. The point is that it opens the door.

If I were advising an owner of a valuable vehicle, I'd tell them not to think small. If the appraisal process establishes any increase at all, use that advantage to challenge omissions that matter.

Don't negotiate like the only issue is the base value. In many disputes, the bigger miss is what the insurer left outside the offer.

How to counter the pressure

You don't need to out-talk the adjuster. You need to out-document the file.

| Tactic | Best response |

|---|---|

| “This is our standard valuation” | Ask for the report and inspect every input |

| “Those comps are the best available” | Compare trim, condition, mileage, and equipment |

| “We've already reviewed it” | Send a written dispute with specific corrections |

| “You can always call back later” | Set deadlines and keep communication in writing |

| “That fee isn't part of the settlement” | Challenge omissions with appraisal leverage where applicable |

The insurer has a system. You need one too. That's what a Total Loss Expert Oregon strategy really is. Not outrage. Structure.

What to Expect Pricing Timelines and Real Results

People usually ask the same two questions once they realize they can fight back. What will this cost, and how long will it take?

The honest answer is that pricing and timing vary by vehicle type, documentation quality, and how hard the insurer digs in. A straightforward daily-driver dispute usually moves faster than a collector vehicle dispute with unusual equipment, limited comparables, or complicated ownership paperwork.

Cost concerns are real, but Oregon changes the risk

Nobody wants to spend money chasing a maybe. That's fair.

What makes Oregon different is the reimbursement protection discussed earlier. When the independent valuation comes in even above the insurer's offer, that can shift the fee burden back to the insurer under the appraisal-clause framework already noted above. That's why many owners who would otherwise stay quiet decide the dispute is worth pursuing.

If you're trying to understand whether the offer passes a common-sense market test before you escalate, this guide on how to calculate fair market value is useful groundwork.

Timelines depend on how prepared you are

The fastest claims aren't always the smallest disputes. They're the best-documented ones.

A well-run challenge usually has these traits:

- The owner responds quickly with records, photos, and corrections.

- The objection is written clearly instead of scattered across phone calls.

- The vehicle description is complete so the appraiser isn't forced to reconstruct basic facts.

- The insurer sees a real dispute file rather than a vague complaint.

When those pieces are missing, the process drags. Not because the valuation question is impossible, but because nobody has framed it properly.

What real improvement looks like

I'll be blunt. You should expect one of two outcomes.

Either the insurer adjusts the settlement because the challenge is well supported, or the dispute reveals that the original number was stronger than it looked. Both outcomes are useful. One puts more money in your pocket. The other gives you a defensible answer instead of a nagging suspicion that you got rolled.

I'm not going to invent flashy case studies or fake payout jumps. What I can say is this: owners with clean records, accurate vehicle details, and a serious appraisal strategy tend to put themselves in a far better position than owners who rely on phone calls and frustration.

That's the result. Clarity, advantage, and a settlement you can justify.

FAQs About Oregon Total Loss Claims

Do I have to sue my insurance company to challenge a total loss offer

Usually, no. A valuation dispute can often be handled through the policy's appraisal process. That's one reason the appraisal clause matters so much. It gives you a structured path that is different from filing a lawsuit.

Can I challenge the offer if the vehicle was already taken to a salvage yard

Yes, in many cases you still can. The physical location of the vehicle doesn't automatically settle the value question. What matters is preserving the records, photos, options, condition details, and the insurer's valuation file.

What if I still owe money on the car

Then the lienholder or lender usually has to be paid from the settlement first. If the settlement is too low, that's even more reason to challenge it. A weak ACV number can leave you short when the payoff is handled.

Can I keep the totaled vehicle

Sometimes owners choose to retain the salvage, but that changes the economics and paperwork. If you're considering that route, ask exactly how the insurer is valuing the salvage portion and what title consequences follow. Don't assume keeping the vehicle is a bargain.

Is the insurer required to use my comparables

Not automatically. But they do have to deal with a credible, independent valuation challenge if you invoke the proper process. Good comparables, clean documentation, and a serious appraiser can force a much stronger review than a casual complaint.

What kinds of vehicles benefit most from a total loss expert

Three stand out.

- Well-maintained daily drivers that are worth more than average examples.

- Modified vehicles where upgrades were overlooked or flattened into generic value.

- Collector or specialty vehicles where ordinary software-driven reports often miss the market.

What if the insurer's increase is tiny

That can still matter. As noted earlier, the reimbursement trigger can turn a small increase into a useful advantage, especially when other claim components were omitted. In higher-value cases, the smart play is often to press beyond the token increase and force the discussion onto everything the carrier failed to include.

Should I keep talking by phone with the adjuster

Use the phone when needed, but confirm important points in writing. Email is cleaner. It creates a record. It reduces “misunderstandings” that somehow always seem to favor the insurer.

How fast should I act

Fast enough that the file doesn't drift, but not so fast that you accept a bad number. The right pace is deliberate. Get the report, gather your records, review the details, and object before the claim gets wrapped up on the insurer's timetable.

What does a Total Loss Expert Oregon owner actually need from me

Usually, the basics done well. The valuation report, photos, receipts, service records, mileage, option details, and a clear timeline. The stronger your file, the less room the insurer has to shrug off the dispute.

If your offer looks light, don't wait for the adjuster to rescue the claim. Push the valuation onto solid ground and make the insurer answer the actual market, not a convenient shortcut.

If your insurer's total loss offer doesn't match what your vehicle was worth, get help from Total Loss Northwest. They handle total loss and diminished value appraisals across Oregon and Washington, invoke the appraisal clause, and build market-based valuations designed to challenge lowball offers. If you want a fair settlement instead of a fast underpayment, they're the team to call.