You've got a damaged vehicle, a settlement offer on the table, and a sinking feeling that the number doesn't match the actual market value of your car. That reaction is common in total loss and diminished value claims, especially when the insurer leans on software-driven valuations that miss trim level, condition, mileage context, recent upgrades, or your local market.

Most drivers start by searching Insurance appraiser near me and immediately run into a mess. Half the results are for home appraisals, some are for general claims work, and very few explain what helps in an auto dispute. If your claim involves a total loss or diminished value, you need a specialist who knows vehicle valuation, insurance procedure, and how to push a weak offer into a formal review process.

When You Need an Appraiser What the Appraisal Clause Is

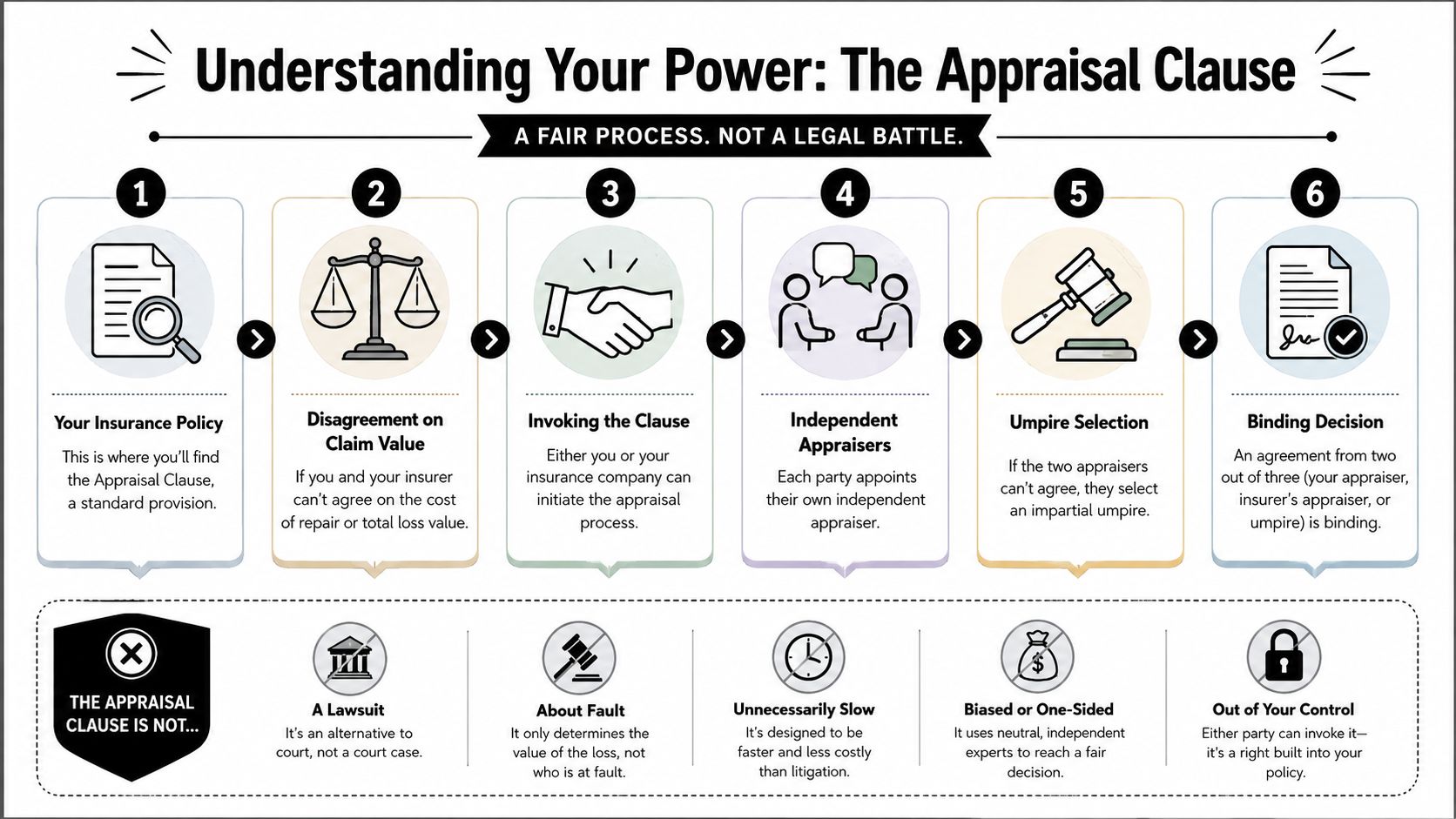

The most important tool in this situation is the Appraisal Clause in your policy. It isn't a lawsuit. It isn't a courtroom fight. It's a contract provision built into many policies to resolve a disagreement over value.

When you and the insurance company disagree on what your vehicle is worth, or what the loss amount should be, the clause lets each side choose an independent appraiser. If those appraisers don't agree, they bring in an umpire. A decision agreed to by two of the three becomes binding.

Why drivers misunderstand it

A lot of people assume appraisal is some extreme move that only happens after lawyers get involved. That's backwards. The Appraisal Clause is often the cleaner path because it focuses the dispute on value, not on legal theater.

Premier Public Adjusters notes that the clause is a standard, low-friction contract provision that can be invoked within 20 days of a written demand, with timelines for appraiser selection and umpire appointment built into the process in many cases, including 20 days for appraiser selection and 15 days for appointing an umpire in the framework they describe in their overview of insurance appraisal and umpiring.

That matters because insurance carriers often start from valuation platforms and internal procedures that aren't built to advocate for you. Appraisal changes the conversation. Instead of arguing with a call center representative about a printout, you move the dispute into a defined process with independent people reviewing value.

Practical rule: If the dispute is about the number, not coverage itself, appraisal is often the first serious pressure point.

What it does in real life

For an auto owner, invoking appraisal usually does three things:

- It formalizes the disagreement. You're no longer just objecting on the phone.

- It shifts the evidence standard. Vehicle condition, comparable sales, options, and market support start to matter more.

- It strengthens your position. The insurer has to deal with a structured process instead of hoping you accept the first offer.

If you haven't looked closely at the insurer's number yet, this guide on evaluating your accident insurance offer is a useful starting point before you respond. And if you want a plain-English breakdown of how the clause works in an auto claim, this explanation of the insurance appraisal clause is worth reading.

When to use it

Appraisal is usually worth considering when:

- The total loss value looks low and the comps don't resemble your vehicle.

- The diminished value offer is missing or dismissed even though your car lost market appeal after the accident.

- The insurer keeps repeating the same number without addressing your actual evidence.

- You're getting pushed toward acceptance before you've had a real valuation review.

If that sounds familiar, you're not overreacting. You're at the point where a qualified appraiser can change the outcome.

Finding a Qualified Auto Insurance Appraiser

Typing Insurance appraiser near me into Google sounds logical, but it often sends drivers to the wrong category of professional. You don't need someone who appraises houses, estate contents, or fine art. You need someone who understands collision damage, market comps, total loss methodology, and diminished value.

That distinction matters because auto claims are technical in a different way. A vehicle appraiser has to understand option packages, prior condition, aftermarket parts, title history, repair quality, and local market behavior. A general appraiser can miss all of that.

Avoid the generalist trap

One of the biggest problems in search results is category confusion. The underlying issue has been noted in job and industry content around appraisal roles. Searches often surface generalists, while total loss and diminished value require auto-specific expertise, especially when the appraiser needs to invoke the clause properly and support a real market value position, as reflected in this discussion tied to insurance appraiser search intent and role specialization.

Here's the simple filter. If the person can't explain diminished value without drifting into home claims language, keep looking.

Where to look instead

A better search process is narrower and more practical:

- Use auto-specific wording. Search for “independent auto appraiser,” “total loss appraiser,” or “diminished value appraiser,” not just insurance appraiser.

- Check whether they handle appraisal clause disputes. Some appraisers only write reports. Others are involved in the dispute process.

- Look for claim-type fit. A person who does classic car valuations may not handle insurer-facing total loss disputes well.

- Ask whether they work in your state. Regional market familiarity matters in Oregon and Washington.

If you want a cleaner starting point than a broad directory search, this page on finding an independent auto appraiser near me narrows the focus to the right specialty.

What a real specialist should understand

An auto-focused insurance appraiser should be comfortable with:

| Claim type | What the appraiser needs to know |

|---|---|

| Total loss | Comparable vehicle selection, adjustments, market support, condition analysis |

| Diminished value | Post-repair stigma, vehicle history impact, severity of damage, resale consequences |

| Appraisal Clause dispute | Written demand process, report support, insurer negotiation, umpire readiness |

A weak appraiser gives you a document. A strong appraiser gives you a position the insurer has to answer.

There's also a practical back-office side to claims work. If you're curious how insurers and agencies streamline intake, communication, and routine claim support, this overview of automated support for insurance shows the kind of operational systems many insurance businesses now use. That's useful context because speed on their side doesn't always mean accuracy on yours.

One factual point should reassure you here. This isn't some fringe service. The independent appraisal business is established enough that firms in the sector generate substantial revenue and support large teams, which is one reason drivers across many markets can find help instead of handling value disputes alone. I'll get into that in the process section where it belongs.

How to Vet Credentials and Ask the Right Questions

Once you have a few names, slow down. At this stage, drivers either hire a real advocate or pay for a polished voice on the phone.

The right appraiser won't rely on vague confidence. They'll explain how they value a vehicle, what documents they need, how they handle insurer disagreement, and where the limits are. If someone starts with promises instead of method, that's a warning sign.

Credentials matter, but not by themselves

Look for auto-industry training and valuation-specific experience. Certifications such as I-CAR or A-CVP can be useful signals because they suggest exposure to collision repair standards or claims and valuation discipline.

Still, a certificate on its own doesn't win a dispute. The better question is whether the appraiser can connect technical knowledge to an insurer-facing report that holds up under scrutiny.

Use this checklist when you call.

- Ask what kinds of claims they handle most. If they mainly do homes, boats, or general property, they're not the right fit for a vehicle loss dispute.

- Ask whether they work both total loss and diminished value files. Some appraisers are strong in one lane and weak in the other.

- Ask how they build comparable support. You want to hear about condition, trim, options, local market relevance, and source quality.

- Ask whether they participate in the appraisal clause process. A report writer who disappears after delivery may not help much if the claim turns contested.

- Ask how they deal with insurer pushback. Their answer should sound procedural and evidence-based, not emotional.

Questions that expose the weak ones

Some questions are especially useful because bad appraisers hate answering them clearly.

Can I see a sample redacted report?

If the report is thin, generic, or hard to follow, that's what your insurer will see too.What documents do you need from me before you start?

A serious appraiser will want the insurer's valuation, photos, VIN details, condition info, and any repair or damage records that matter.What happens if your value and the insurer's appraiser don't match?

They should be able to explain the negotiation path and the possibility of an umpire without sounding rattled.How do you charge?

You need clarity before signing anything. Flat fee, hourly, or another structure. Get it in writing.

Ask this directly: “If the carrier challenges your report point by point, how do you defend it?”

Red flags to treat seriously

A few things should make you walk away fast:

- Guaranteed outcomes. No honest appraiser can promise a specific settlement number.

- No report sample. If they won't show structure, they may not have one.

- No clear scope. You should know whether they inspect, research, write, negotiate, or all of the above.

- One-size-fits-all language. Diminished value and total loss are not interchangeable assignments.

- No regional awareness. Market value arguments fall apart when the appraiser doesn't understand your area.

A good appraiser sounds measured. They won't sell certainty. They'll sell process, documentation, and defensible reasoning. That's exactly what you want.

The Appraisal Process Costs and Timelines

Once you hire an appraiser, the claim usually starts feeling less chaotic. There's a sequence to follow, and that alone helps. You stop reacting to insurer emails and start building a valuation file that can stand on its own.

This is also where many drivers realize they aren't doing anything unusual. The independent appraisal field is an established part of the claims world. According to ZoomInfo's company profile data, firms such as Insurance Appraisal Services operate at substantial scale, with $21.4 million in revenue and 201 to 500 employees, which reflects broad demand for neutral valuation work in disputed claims across the market, as noted in this industry profile of Insurance Appraisal Services.

What usually happens first

The early stage is document-heavy. Your appraiser typically wants the insurer's valuation report, policy language if appraisal is being invoked, vehicle details, photographs, condition records, and any repair-related paperwork that helps explain damage or prior value.

Then comes review and valuation. In a total loss file, that means checking whether the insurer used poor comps, weak adjustments, or bad assumptions about equipment and condition. In a diminished value file, the appraiser studies how the accident history changes the vehicle's resale position even after repairs.

If you want a realistic sense of what fees can look like before you commit, this page on car appraisal cost gives a useful frame for how appraisers commonly structure charges.

Typical work stages

The exact pace varies, but the workflow often looks like this:

| Stage | What happens |

|---|---|

| Intake | You sign an agreement and send records |

| Review | The appraiser studies the insurer's value basis |

| Inspection or file analysis | Vehicle condition and damage support are documented |

| Valuation | Comparable market data and adjustments are developed |

| Report delivery | You receive the written appraisal |

| Dispute handling | The report is used in negotiation or formal appraisal |

That process can move quickly when the documents are clean. It can also slow down if the insurer delays, if the vehicle history is unusual, or if the case moves to umpire involvement.

What costs should look like

Fees vary with claim complexity and with the appraiser's billing structure. Some charge a flat fee. Others charge hourly. The important part isn't picking the cheapest option. It's understanding what's included.

Ask whether the fee covers only the report or also covers communication with the insurer, appraisal clause participation, and possible follow-up. A low upfront fee can become expensive if every phone call and document response gets billed separately.

The cheapest report is often the one the insurer ignores most easily.

How to keep the timeline moving

You can shorten delays by giving the appraiser a complete file upfront.

- Send the insurer's valuation report early. That's usually the document being challenged.

- Include VIN and option details. Small equipment differences can affect value.

- Provide condition evidence. Maintenance records, photos, and recent work matter.

- Organize accident documents. Tow records, repair estimates, and photos help explain severity.

The smoother your documentation, the faster your appraiser can build a report that pressures the carrier.

Oregon and Washington Claim Specifics

Oregon and Washington drivers face the same broad problem as everyone else. The insurer wants to settle the file efficiently. But local claim handling still matters because market conditions, vehicle demand, and regional practice all shape how a valuation argument lands.

That's one reason local appraisal experience matters in the Pacific Northwest. This isn't a new market. Insurance Appraisal Services was founded in Portland, Oregon, in 1975 and expanded to Seattle by 1985, reflecting a long-running regional demand for third-party appraisal work, according to the company's LinkedIn profile history.

Why Pacific Northwest experience changes the file

An appraiser working in Oregon or Washington should understand local resale realities. A vehicle's value in Portland or Seattle doesn't always track neatly with a generic database assumption. Weather, commuter patterns, truck and SUV demand, and regional buyer preferences can all affect how persuasive a comparable sale really is.

That matters even more with diminished value claims. The question isn't just whether the car was repaired. The question is how buyers in your market respond to a vehicle with an accident history. A local appraiser is usually in a better position to explain that in a way that sounds grounded instead of abstract.

Practical differences drivers should pay attention to

Rather than trying to memorize legal jargon, focus on what changes your outcome:

- Total loss disputes turn on valuation support. The label isn't enough. The comps and adjustments decide whether your argument holds.

- Diminished value needs auto-specific proof. Generic claims language won't do it.

- Repair quality still matters. Even a well-repaired vehicle can suffer market stigma after an accident.

- Regional familiarity helps. Local market knowledge can tighten the report and reduce insurer objections.

In Oregon and Washington, the strongest appraisal files usually combine clean valuation support with someone who understands the market the car would actually sell in.

If you're sorting out your coverage position alongside a collision claim, it can help to talk to Professional Insurance Advisors about collision so you understand how the coverage side and the value side fit together. That won't replace an appraisal, but it can make the overall claim picture easier to read.

Next Steps After Your Appraisal Is Complete

Once your appraiser finishes the report, you finally have something insurers have to engage with. Not a complaint. Not a guess. A supported valuation position.

In many cases, that report goes to the insurer or to the carrier's appraiser as the basis for negotiation. If the numbers get close enough, the matter resolves there. If they don't, the process can continue through the formal appraisal track and, if necessary, an umpire.

What happens after the report lands

The insurer has to decide whether to revise its value, challenge your appraiser's support, or proceed through the policy's dispute mechanism. That's why report quality matters so much. A strong report is organized, specific, and hard to dismiss with canned language.

The best outcome is often a negotiated resolution before the umpire stage. That saves time and usually means both sides recognized where the defensible value landed. But if the gap remains, the umpire process exists for a reason. It keeps the dispute moving.

What you should expect from your side

Stay available. Your appraiser may need follow-up documents, clarification on condition, or confirmation on options and history. Small details can matter late in the process, especially when the insurer starts challenging line items instead of the whole value.

Keep your expectations disciplined too. The goal isn't to “win” with an unrealistic number. The goal is to force the settlement onto a fair market basis. That's what gets paid.

When the process is working

You'll know the appraisal process is doing its job when the conversation changes. The insurer stops repeating the original offer and starts addressing evidence. That's the shift you wanted from the beginning.

If you're dealing with a total loss offer that doesn't make sense or a diminished value claim that isn't being taken seriously, Total Loss Northwest handles certified independent auto appraisals for Oregon and Washington drivers and can invoke the Appraisal Clause in the right cases to support a fair market-value dispute.