You open the claim email expecting a reasonable number. Instead, you get a settlement that doesn't come close to replacing your vehicle, covering proper repairs, or accounting for what the accident did to its market value.

That moment catches a lot of drivers off guard. They assume the insurer already ran the numbers correctly, or that arguing back means hiring a lawyer and preparing for a long fight. In practice, many disputes start with something simpler. The carrier used a weak condition rating, pulled poor comparable vehicles, missed factory options, or ignored diminished value altogether.

The stakes are not small. In 2024, the average auto liability claim for property damage reached $6,770, while the average bodily injury claim reached $28,278, according to the Insurance Information Institute's auto insurance facts. Millions of policyholders go through the dispute process each year for the same reason. The first number wasn't the right one.

If you're dealing with a low offer, you need local insurance dispute help that treats this like a valuation problem first and a negotiation problem second. The same practical mindset shows up in other kinds of claim conflicts too, including Florida insurance claim disputes, where policyholders often have to push back when the carrier's position doesn't match the actual loss.

Your Guide to Local Insurance Dispute Help

Individuals contact dispute help after one of three things happens.

The car is declared a total loss, but the valuation is built on vehicles that aren't really comparable. The repair estimate looks incomplete, and hidden damage is being brushed aside. Or the adjuster says the vehicle was repaired, so there's no meaningful diminished value claim left to discuss.

All three scenarios create the same problem. The insurer presents its number as if it's objective, but the file may rest on bad inputs. Once those inputs go unchallenged, the offer starts to look more official than it deserves.

What drivers usually miss

A low offer doesn't always come from open bad faith. More often, it comes from shortcuts.

A condition report may rate your car lower than it should. A valuation report may use sale listings from outside your actual market. A total loss worksheet may omit trim level details, packages, upgrades, recent mechanical work, or custom parts. For Oregon and Washington drivers, that local market issue matters. Seattle isn't the same as Spokane. Portland isn't the same as Bend. A bad comparison set can drag the number down fast.

A settlement figure is only as good as the vehicle data behind it.

Where control starts

You don't need to accept the first number just because it arrived on company letterhead. You need to slow the process down, get the valuation documents, and check whether the insurer's file reflects your actual vehicle and your actual loss.

That's the core of effective local insurance dispute help. Not venting. Not guessing. Building a cleaner, stronger valuation record than the one the carrier started with.

How to Assess Your Insurer's Lowball Offer

Before you argue, inspect the file. Good disputes begin with a careful review, not an angry phone call.

A practical framework for resolving disputes follows five phases: assessing the claim, exchanging documents, determining risk, assessing a realistic settlement, and negotiating, with early evidence gathering doing much of the heavy lifting according to Degan's discussion of early case resolution in insurance defense. In auto claims, that first phase matters more than most drivers realize.

Read the valuation like an appraiser would

Start with the insurer's report, not their summary email. Ask for the condition report, valuation report, comparable vehicle list, and any total loss worksheet used to support the offer.

Then check these points:

- Vehicle identity: Verify year, make, model, trim, drivetrain, engine, mileage, and VIN-related equipment.

- Options and packages: Confirm factory packages, premium audio, safety tech, wheel upgrades, towing packages, appearance packages, and specialty equipment.

- Condition ratings: Look closely at how the report grades interior, exterior, tires, paint, and prior condition.

- Comparable vehicles: Review whether the comps are comparable in mileage, trim, market area, and condition.

- Adjustments: Watch for large downward adjustments that aren't explained clearly.

A surprising number of disputes turn on ordinary mistakes. Wrong trim. Missed package. Unfair condition deduction. Comparable vehicles that were never strong comps to begin with.

Compare local market reality

Don't rely only on national listings or broad search results. Pull local and regional vehicles that match your car as closely as possible. Focus on dealer listings, specialty marketplaces if the vehicle is unusual, and market areas where someone in your region would realistically shop.

That gap between policy language and real-world protection shows up in other lines of insurance too. A useful example is this breakdown of New York homeowners insurance gaps, which shows how coverage often looks broader in theory than it works in practice. Auto disputes have the same pattern. The paperwork sounds extensive until you test the assumptions underneath it.

Decide whether this is a negotiation issue or an appraisal issue

If the carrier made a small clerical mistake, a corrected submission may solve it.

If the whole valuation feels built to defend a low number, you're no longer just correcting facts. You're dealing with a structural dispute over value. That's when stronger measures, including a formal demand and possibly the Appraisal Clause, become the smarter path.

Practical rule: If the insurer's report would still be unfair even after fixing one or two obvious errors, treat it as a valuation dispute, not a routine adjustment issue.

Assembling Your Evidence for a Stronger Claim

A weak file invites a weak answer. If your documents are scattered across text messages, photo folders, and half-finished emails, the insurer controls the story.

A strong dispute file does the opposite. It organizes the loss so clearly that the carrier has to respond to evidence, not just to your frustration.

Build the claim file before you write the demand

Start by gathering everything that proves what happened, what was damaged, and what the vehicle was worth before and after the loss.

Keep these items together in one folder:

- Police report: Get the full report, not just the exchange sheet.

- Photos and video: Include scene photos, damage close-ups, wheel and suspension angles, interior photos, and pre-loss photos if you have them.

- Repair estimates: Don't stop at the carrier's estimate. Get independent estimates when needed.

- Ownership and option proof: Window sticker, purchase records, service records, receipts for upgrades, and financing or sales documents can help establish configuration and pre-loss condition.

- Communication log: Track every call and email with dates, names, and what was said.

- Expense records: Rental, towing, storage, and out-of-pocket costs should be itemized and saved.

This same discipline helps in other property disputes too. A practical roof insurance claims guide is useful because it shows the same basic truth. Claims become harder to dismiss when the evidence is chronological, visual, and complete.

Write a demand letter that does one job well

A demand letter shouldn't sound dramatic. It should sound organized.

Benchmark data indicates 70-80% of disputes are resolved pre-litigation when demand letters are professionally prepared and supported by documentation, and providers won 88% of resolved cases in Q1 2024 through formal, evidence-backed challenges according to Georgetown's Independent Dispute Resolution process data.

Your letter should include:

- The claim number, date of loss, and vehicle information.

- A short statement of what you dispute.

- The specific errors in the insurer's valuation or estimate.

- The documents you're attaching.

- The amount or correction you're requesting, stated clearly.

- A deadline for written response.

- A notice that you reserve all contractual rights under the policy.

I am disputing the current valuation of my vehicle because the report does not accurately reflect the vehicle's trim, equipment, condition, and comparable market data. Attached are supporting records, photographs, repair documentation, and market comparables for review. Please provide a written response after reviewing the enclosed materials and confirm whether the carrier will revise its valuation or proceed under the policy's dispute provisions.

Keep the tone firm and usable

Don't fill the letter with accusations you can't prove. Don't threaten legal action in every paragraph. And don't bury your best points under a long story about how stressful the accident has been.

The letter works when it gives the adjuster, supervisor, or defense-side reviewer a clean file to act on. That's what moves a claim.

Using the Appraisal Clause to Get Fair Value

This is the part many drivers never hear about until they've wasted weeks arguing with an adjuster.

Most policyholders know they can complain. Far fewer understand that their own policy may contain a built-in mechanism for resolving disputes about value. That mechanism is the Appraisal Clause.

Why this tool changes the leverage

The biggest reason appraisal matters is simple. It shifts the dispute away from the insurer's internal valuation process and toward an independent valuation process.

Data highlighted by Merlin Law Group's discussion of insurance coverage disputes points to a major neutral appraiser gap. 68% of diminished value claims are denied initially, yet only 12% of policyholders seek a neutral third-party appraiser before escalating the dispute. For higher-value vehicles, diminished value can exceed $15,000. That gap is exactly why so many drivers stay stuck in the same loop of emails, callbacks, and repeated low offers.

If your dispute is really about value, appraisal is often more effective than endless debate with the person defending the original number.

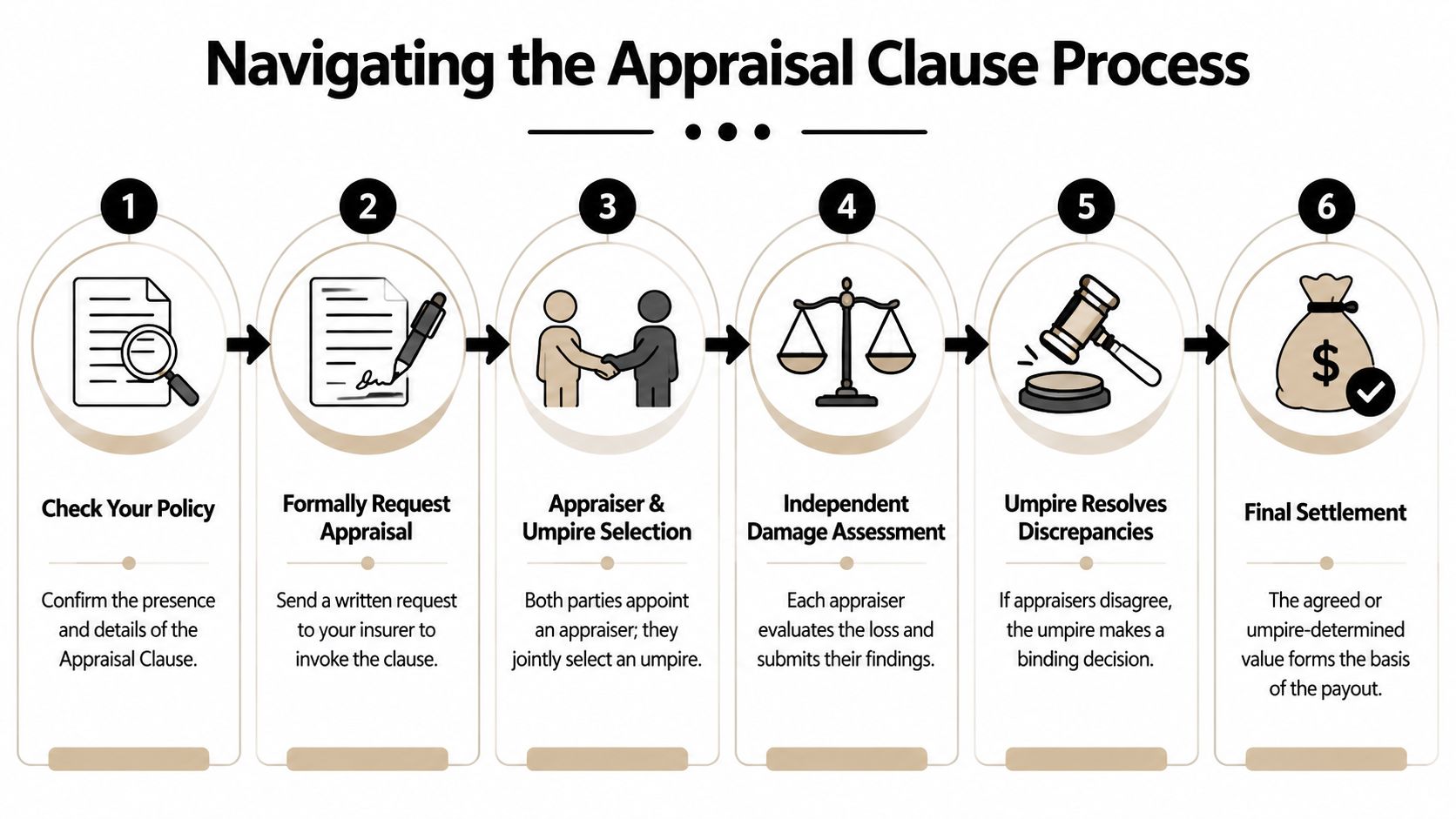

How appraisal usually works

The policy language varies, so read your own contract carefully. In general, the process works like this:

- You make a written demand for appraisal under the policy.

- Each side selects an appraiser.

- Those appraisers evaluate the loss and try to reach agreement.

- If they disagree, an umpire resolves the remaining gap.

- The resulting value becomes the basis for settlement under the policy terms.

This overview of the insurance appraisal clause process is useful if you want to see how the moving parts fit together before sending your written demand.

Here's the process in a simple visual format.

What the Appraisal Clause does better than ordinary negotiation

Negotiation still matters, but negotiation inside the insurer's preferred framework often leads nowhere. The same report gets defended by a different representative, and the same software-driven assumptions stay in place.

Appraisal forces a different question. Not, “Will the adjuster reconsider?” but, “What is the actual value supported by an independent appraiser?”

That's especially important in Oregon and Washington total loss and diminished value disputes, where local market conditions, specialty vehicles, and post-accident stigma can't always be captured by a standard valuation workflow.

A short video can also help if you want a plain-language view of how the process plays out in practice.

If the carrier keeps inviting you to “submit more information” but never leaves its own number behind, appraisal is often the cleaner path.

Finding and Working With a Certified Appraiser

Once you decide to invoke appraisal, the next decision matters a lot. You need the right professional, not just the first person who says they handle disputes.

Some drivers assume any adjuster, body shop, or general claims consultant can fill this role. That's not how strong appraisal work is built. You want someone who understands total loss valuation, diminished value methodology, market comparables, policy language, and the practical habits of the carriers they're dealing with.

Know who you're hiring

A certified auto appraiser focuses on vehicle value and valuation evidence. That's different from a public adjuster model and different from a repair-only perspective.

Ask direct questions:

- What kinds of claims do you handle most often? Total loss, diminished value, or both?

- What vehicles are you comfortable valuing? Daily drivers, collector cars, modified vehicles, luxury brands?

- How do you build your comparable market set?

- Do you inspect records and option content in detail, or mostly review the insurer's file?

- Have you worked appraisal clause disputes with major carriers before?

- What deliverables do I receive? Report, comparable analysis, rebuttal support, written demand support, appraisal attendance?

If you're comparing options, this page on hiring an independent car appraiser gives a useful reference point for what a specialized appraisal service should cover.

Watch for weak signs early

Some warning signs show up fast.

An appraiser who quotes a result before reviewing the file is guessing. An appraiser who can't explain how they separate repair cost issues from market value issues may not be the right fit. And anyone who treats appraisal as a form letter instead of a case-specific valuation process is likely to leave money on the table.

The best appraisers don't start by promising a number. They start by asking for the policy, the valuation report, the photos, and the supporting records.

Typical appraisal process timeline and costs

Costs and timing vary by vehicle, claim type, and how hard the insurer fights the valuation. Still, the workflow usually follows a recognizable pattern.

| Phase | Typical Timeline | Estimated Cost |

|---|---|---|

| Initial file review | A few business days | Varies by appraiser and claim complexity |

| Vehicle and document analysis | Several days to a few weeks | Often bundled into appraisal service |

| Written demand or appraisal invocation support | Depends on policy response timing | Varies |

| Appraiser-to-appraiser exchange | Several days to a few weeks | Varies |

| Umpire involvement if needed | Longer than direct agreement | Additional cost may apply |

| Final report and settlement support | After valuation is finalized | Varies |

The key trade-off is straightforward. A specialized appraiser costs money up front, but accepting a weak settlement can cost far more if the carrier's number never reflected the actual market value of the vehicle.

Navigating Disputes in Oregon and Washington

Local insurance dispute help should be local in more than name. Oregon and Washington drivers need to think about market conditions, carrier response habits, and when to push a complaint beyond the insurer's internal process.

One benchmark is useful here. The South Carolina Department of Insurance states that most insurance issues can be resolved within 30 days if the consumer contacts the company directly first, and when state intervention is required, insurance entities often must respond within 7 days according to the South Carolina Department of Insurance consumer information. That doesn't create Oregon or Washington law, but it is a practical timing benchmark. If your file is dragging well past ordinary response windows, something is wrong.

What to do first in a local dispute

Start with the carrier. Put the dispute in writing. Ask for the valuation support documents. Identify the specific errors. Request a written response.

If the issue involves post-repair loss in value, it helps to understand how a formal diminished value auto claim is built, especially when the insurer acts as if proper repairs ended the conversation. They didn't. Repairing the vehicle and valuing the market stigma are different issues.

When to escalate

Escalation makes sense when one of these patterns shows up:

- The insurer delays without substance: You get repeated acknowledgments but no real review.

- The file keeps circling the same bad report: Different representatives defend the same flawed valuation.

- The carrier ignores contract rights: Your appraisal request, demand package, or supporting records aren't being addressed directly.

- The loss has specialty features: Collector, custom, or high-end vehicles often need a more technical valuation process.

Oregon and Washington practical steps

For drivers in either state, keep the process disciplined:

- Save every email and upload confirmation.

- Keep a call log with names, dates, and next steps promised.

- Ask for all valuation documents in writing.

- Send your dispute package as a single organized submission.

- If internal review stalls, contact your state insurance regulator and ask about the complaint process.

- If the policy supports appraisal and value is the dispute, consider invoking it instead of waiting for another adjusted offer.

State complaint systems can help restart a stagnant file. But when the core disagreement is valuation, a regulator complaint and an appraisal strategy often serve different functions. One pushes responsiveness. The other pushes fair value.

Take Control and Get What You Are Owed

The insurance company's first offer isn't the final word. It's an opening position based on the file they built, and sometimes that file is incomplete, rushed, or tilted by weak valuation methods.

The drivers who improve their outcome usually do three things well. They inspect the insurer's report closely. They build a clean evidence file. And when the dispute is really about value, they use the Appraisal Clause instead of spending month after month arguing inside the insurer's own process.

That's where local insurance dispute help becomes useful in the real sense of the phrase. Not generic advice. Not empty reassurance. Actual guidance on when to negotiate, when to document harder, and when to move the dispute into appraisal with an independent appraiser.

If you're in Oregon or Washington and the offer doesn't match the vehicle you owned or the loss you suffered, slow the claim down and make the insurer defend its number. Good documentation changes the conversation. A strong appraiser can change the result.

Pay attention to the trade-off. The cheapest path upfront is often the most expensive path at settlement. A careful, contract-based challenge may take more effort, but it gives you a real chance to recover the value the first offer missed.

If you need help challenging a low total loss or diminished value offer in Oregon or Washington, Total Loss Northwest provides certified independent auto appraisals built for appraisal clause disputes. When the carrier's valuation software misses the actual market value of your vehicle, having a specialist who knows how to document and defend that value can make the claim process far more effective.