You get the call from the adjuster. The car is repaired, or the insurer has declared it a total loss, and the number they give you doesn't match what you know the vehicle was worth. You maintained it. You added parts. You know what similar vehicles sell for in your area. None of that seems to show up in the offer.

That's the point where many Washington drivers get stuck. They assume the insurer's software is the final word, or they argue with the adjuster without bringing in evidence that can change the result. Both paths usually go nowhere.

A fair settlement starts when someone independent values the vehicle the way the market does, not the way a claims system does. In Washington, that matters more than is commonly understood.

The Post Accident Problem Most Drivers Face

The pattern is familiar. A driver gets hit, the body shop does the work, and then the insurance company says the file is wrapped up. Or the vehicle is totaled and the adjuster sends over a valuation packet full of comparables that don't look comparable at all. Different trims. Different condition. Different equipment. Sometimes vehicles from markets that don't reflect what buyers are paying where you live.

The driver pushes back. The adjuster repeats the same number in a different format. That's where frustration turns into lost money.

Why this hits Washington drivers harder

Washington has an older vehicle fleet than the country overall. The average age of vehicles on the road in the state is 14.3 years, compared with the national average of 12.2 years, according to Autos Drive America's Washington vehicle age data. Older vehicles often carry a bigger valuation dispute after an accident because condition, maintenance, rarity, and local demand matter more than a generic pricing model admits.

A clean older truck with documented upkeep isn't the same as a neglected one. A well-kept import with low miles for its age won't trade like the rough examples an insurer may pull into a report. The software doesn't always see what the market sees.

Practical rule: The moment an insurer's number feels disconnected from the real market, stop arguing opinions and start building evidence.

What usually doesn't work

Drivers often make the same mistakes:

- Relying on emotion: “I know what my car was worth” may be true, but it won't carry a claim by itself.

- Sending random online listings: One or two ads can help with context, but they rarely stand up as a complete valuation.

- Assuming repairs fixed the value problem: Repairing damage fixes the car. It doesn't automatically fix the loss in resale value tied to the accident history.

- Taking the first offer to get it over with: Quick closure often costs more than people think.

What does work

The cases that move are the ones backed by a defensible appraisal. That means documented condition, repair analysis, market comparison, and a report prepared by someone whose job is valuation, not claim cost control.

That's where Washington vehicle experts come in. Not as repair people. Not as lawyers. As independent appraisers who know how to turn “this offer feels wrong” into something an insurer has to answer.

Who Are Washington Vehicle Experts Exactly

A lot of people hear “vehicle expert” and think mechanic, collision shop, or dealer. That's not the role.

Washington Vehicle Experts in this context are independent appraisers who focus on vehicle valuation for total loss and diminished value disputes. Their job is to determine what the vehicle was worth before the loss, or how much market value it lost after repairs, using evidence that can hold up in negotiation and, if necessary, formal dispute resolution.

Not a mechanic, not an adjuster

A mechanic answers, “What does it take to fix this car correctly?”

An insurance adjuster answers, “What will the company pay under this claim?”

An independent appraiser answers, “What is this vehicle worth in the market, based on condition, damage, repairs, and comparable sales?”

Those are three different questions. People get shortchanged when they treat them as if they're the same.

Diminished value in plain English

Diminished value is the loss in fair market value between a vehicle's pre-accident condition and its post-repair condition, even if the repairs are flawless, because an accident history can reduce buyer appeal, as explained in this diminished value appraisal overview. Certified appraisers follow USPAP, the Uniform Standards of Professional Appraisal Practice, so the report is built to be credible rather than casual.

The easiest way to understand it is to compare two similar houses. Same neighborhood. Same layout. Same square footage. But one had a major fire and was repaired. A buyer will still weigh that history. Vehicles work the same way.

What a real appraiser actually does

A competent appraiser doesn't guess. They inspect records, review repair documentation, evaluate severity, account for options and condition, and compare against actual market evidence. In some diminished value work, professionals use tools such as vAuto and inspect the vehicle in person through a qualified technician, as discussed in the same source noted above.

If you're trying to understand what a dedicated valuation specialist does in these claims, this independent car appraiser overview gives a useful breakdown.

Here's the practical difference between a strong appraisal and a weak one:

| Approach | What it looks like |

|---|---|

| Weak valuation | Generic pricing, broad assumptions, little attention to options, condition, or repair quality |

| Strong appraisal | Market-backed comparables, documentation review, repair analysis, and a written methodology |

A good appraiser doesn't promise a number on day one. They promise a process that can be defended.

That distinction matters. If someone leads with guarantees instead of method, keep looking.

The Appraisal Clause Your Secret Weapon

Most policyholders don't realize they may already have a contractual way to challenge a bad insurance valuation. It's called the Appraisal Clause. In Washington, that clause often appears in auto policies and gives you a formal route to dispute the insurer's number with an independent appraiser.

Washington also recognizes diminished value claims in the right circumstances. Washington diminished value guidance discussing WAC 284-30-391 and the Right to Appraisal explains that vehicle owners can use an independent certified appraiser to challenge an insurer's valuation software.

Why this clause matters

The Appraisal Clause changes the conversation. Instead of debating line by line with an adjuster who keeps returning to the same internal number, you trigger a process the insurer has to respond to under the policy terms.

That's not being aggressive. It's using the contract as written.

The insurer picks its appraiser. You pick yours. If the two appraisers agree, that usually resolves the valuation issue. If they don't, they can move to an umpire process depending on the policy terms.

For a plain-language look at how that works, this auto insurance appraisal clause guide is worth reviewing.

How to invoke it the right way

There's a tendency to overcomplicate this. Keep it direct and keep it in writing.

- Read your policy and locate the appraisal language.

- Send written notice to the insurer invoking the clause. Be clear, specific, and professional.

- Retain your appraiser and provide the claim documents quickly.

- Stop debating unsupported numbers with the adjuster once the process is underway.

- Let the valuation evidence do the work.

A common mistake is threatening legal action before using the appraisal route that's already available. Sometimes litigation is necessary, but often the appraisal process is the cleaner first move because it narrows the dispute to value.

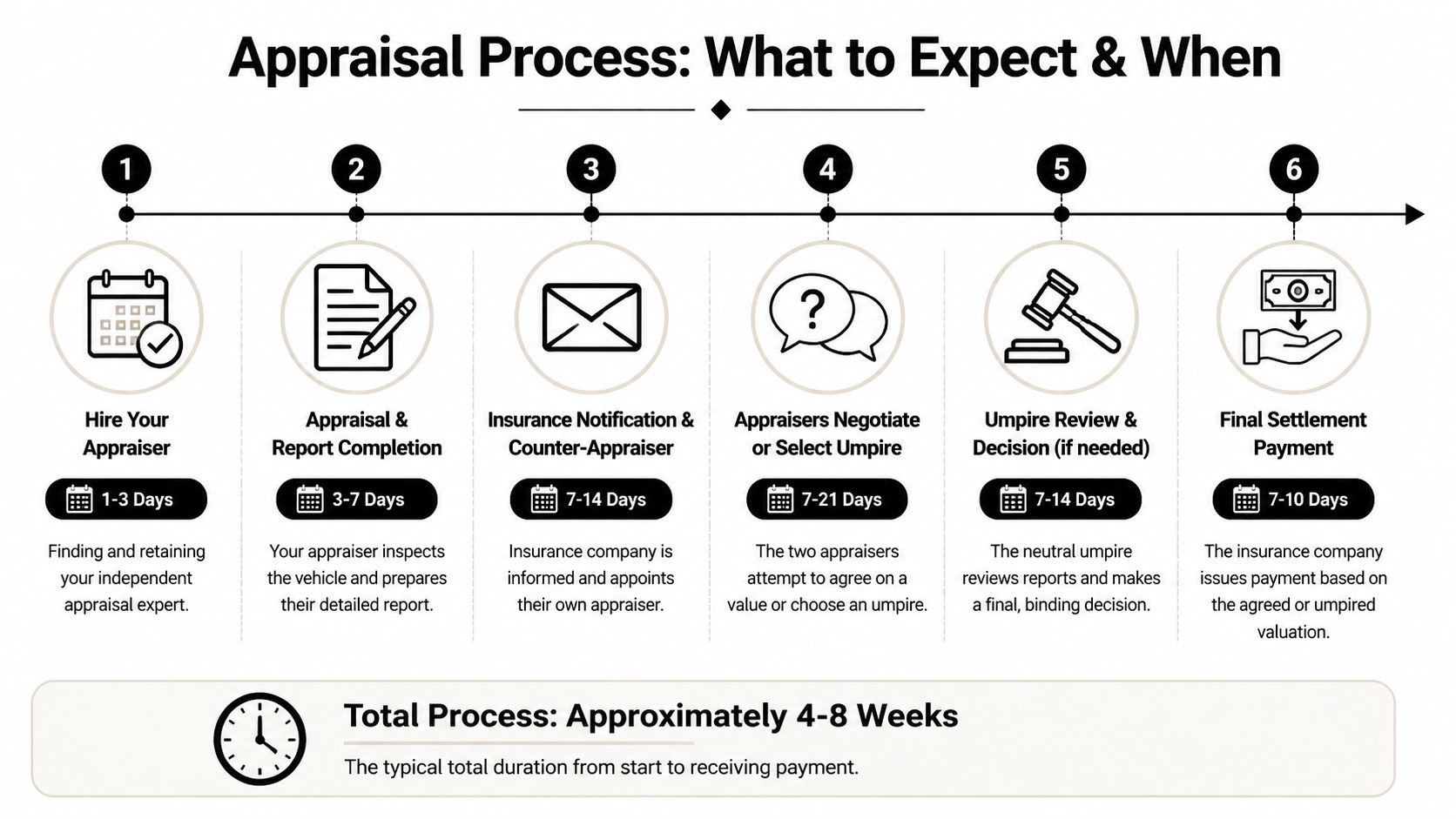

Here's a visual overview of the process:

What insurers count on

They count on delay. They count on confusion. They count on the driver assuming the first number is based on neutral market reality.

It often isn't.

If the insurer's offer comes from software and your challenge comes from evidence, you've changed the leverage in the file.

That's what the Appraisal Clause is for. It doesn't guarantee your preferred outcome. It does force the dispute into a process where unsupported shortcuts have less room to hide.

Gathering Your Evidence for a Strong Case

A strong appraisal starts before the appraiser writes a word. It starts with what you hand over. If your file is thin, even a good appraiser has less to work with. If your file is organized, the report gets sharper fast.

The core document checklist

Bring the basics first:

- Insurance valuation report: This shows exactly how the insurer reached its number, including the comparables and adjustments they used.

- Police report or collision report: It helps pin down loss facts, date, and vehicle involvement.

- Repair estimate: This shows damage scope, parts replacement, structural work, and severity indicators.

- Final repair invoice: On a diminished value claim, the completed invoice matters because it shows what was done.

- Photos of the damage: Before-repair images are often more revealing than the estimate alone.

- Post-repair photos: These help document finish quality and visible condition after the work.

The records that often make the difference

The next layer is where many files either strengthen or collapse.

- Maintenance records: Regular service helps establish condition before the accident.

- Receipts for upgrades or recent work: Tires, suspension, engine work, accessories, and OEM options can matter if they affect market value.

- Ownership history details: If the car had unusually clean history or enthusiast-level care, the appraiser needs that context.

- Comparable listings you've found: These won't replace a formal market analysis, but they can help point the appraiser in the right direction.

A short note from you also helps. Not a rant. Just facts. State what the vehicle was used for, any standout condition points, and anything the insurer's report appears to miss.

Why each piece matters

Insurers often reduce a vehicle to database fields. Your evidence adds the details the market prices in.

If the estimate shows structural repairs, that can affect diminished value more than cosmetic work. If records show exceptional upkeep, that can matter in a total loss dispute. If the insurer used weak comparables, your appraiser needs the report in hand to explain why.

Keep everything in one folder, name the files clearly, and send them as a complete package. The faster your appraiser can see the whole file, the faster they can identify where the insurer's number breaks down.

Typical Timelines and What to Expect

People usually want one answer here. “How long will this take?” The honest answer is that it depends on the policy, the insurer's responsiveness, the quality of the documents, and whether the appraisers agree early or need an umpire.

Still, the process tends to follow a recognizable rhythm. You'll do better if you expect phases rather than one dramatic decision.

A practical timeline

The visual above lays out a typical range. In many claims, the full process runs approximately 4 to 8 weeks based on the timeline provided in the infographic brief for this article.

That's not a legal deadline. It's a practical expectation.

Here's how those stages usually feel from the client side:

| Phase | What usually happens |

|---|---|

| Initial engagement | You hire the appraiser, sign documents, and send the claim file |

| Inspection and report | The appraiser reviews condition, damage, market data, and prepares the valuation |

| Insurer response | The insurer acknowledges the appraisal demand and appoints its side |

| Negotiation | The appraisers compare methods, comparables, and conclusions |

| Umpire stage if needed | A neutral decision-maker reviews the dispute |

| Payment | The insurer issues settlement based on the agreed or decided value |

Where delays usually show up

The appraisal itself often moves faster than the claim department. Delays usually come from missing records, slow insurer replies, or disputes over comparables and methodology.

Repair-related diminished value claims can also slow down if the vehicle hasn't been fully repaired yet. A proper diminished value analysis often requires the repairs to be completed first so the appraiser can evaluate the actual result, not a hypothetical one.

Client expectation: Fast isn't always better. Accurate is better. A rushed report can give the insurer an easy target.

What outcomes are realistic

The goal is a fairer number, not a magic number. Sometimes the evidence supports a major correction. Sometimes it supports a modest one. Sometimes the insurer's original figure is wrong in several places but not by as much as the owner hoped.

That's normal.

A serious appraiser won't treat every file like a guaranteed windfall. They'll tell you where the value case is strong, where it's vulnerable, and whether the likely gain justifies the effort. That kind of honesty is a good sign, not a lack of confidence.

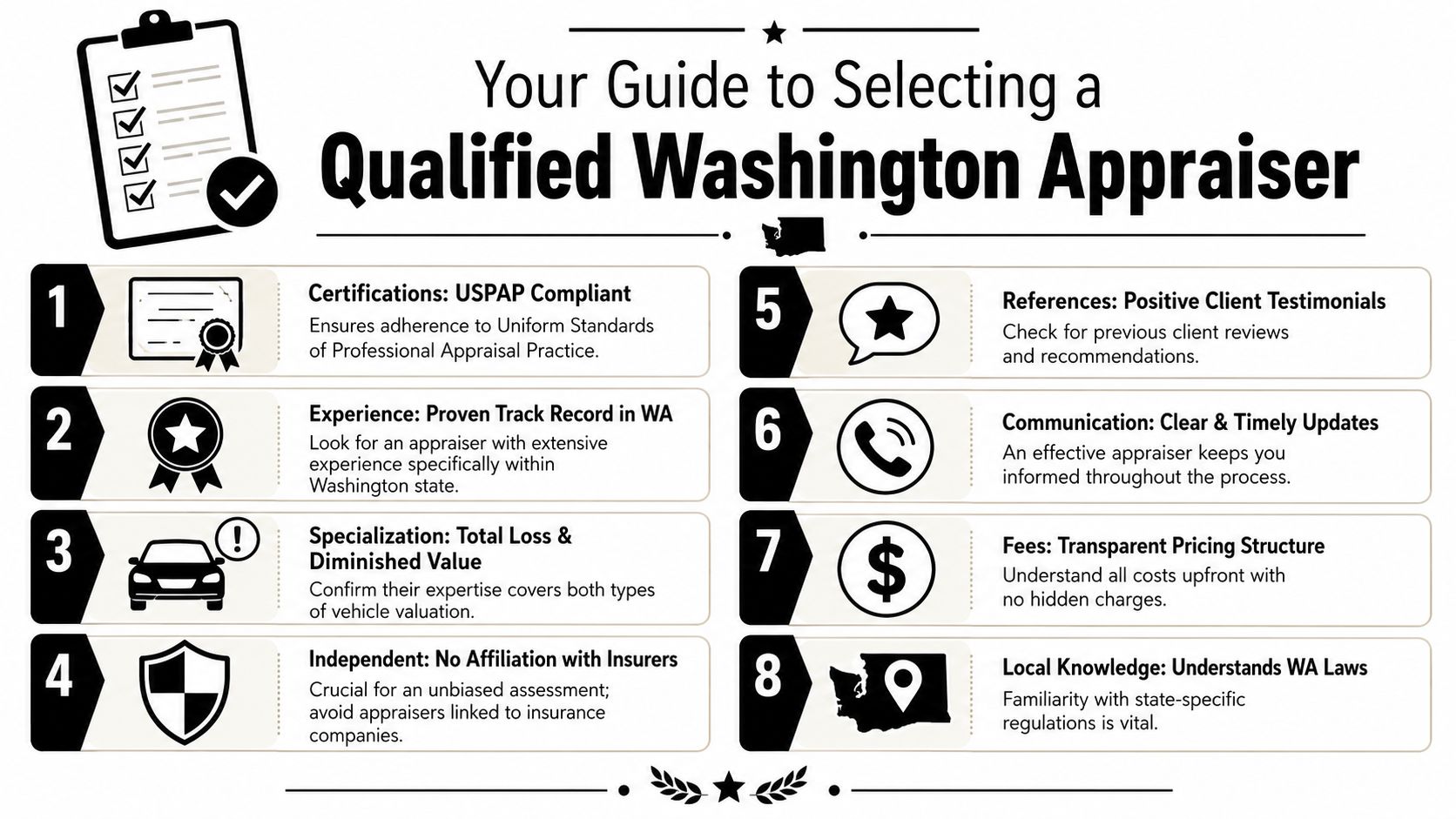

How to Choose the Right Washington Appraiser

Often, a lot of people get burned twice. First by the insurer's number. Then by hiring the wrong person to challenge it.

Washington drivers don't get much public guidance on this. As noted by the Washington State Independent Auto Dealers Association consumer page, there's a gap in public information around diminished value outcomes and how consumers should use the Appraisal Clause. That means you need to vet the appraiser yourself instead of assuming the market has already sorted the good from the bad.

Green flags to look for

If you're searching for Washington vehicle experts, focus on process, independence, and communication.

- USPAP compliance: If they can't explain their standards, that's a problem.

- Washington claim experience: State-specific familiarity matters because policy language and claim handling practices matter.

- Specialization in total loss and diminished value: General automotive knowledge isn't enough by itself.

- Transparent method: They should explain how they analyze market data, condition, damage, and repair quality.

- Clear fee structure: You should know what you're paying for before the file starts.

- Responsiveness: A strong appraiser keeps the client informed and answers direct questions directly.

If you're comparing local options, this independent auto appraiser near me page is an example of the kind of specialized service category you should be looking for.

Red flags that should stop you

Some warning signs are easy to miss when you're stressed and trying to move quickly.

- Guaranteed outcomes: No one credible can promise a result before reviewing the evidence.

- Formula-only approach: Be cautious if they lean heavily on the 17c formula without discussing real market support.

- No inspection discipline: If they don't care about repair records, photos, condition, or comparable quality, the report may be weak.

- Insurer ties that compromise independence: The value of the appraisal is its neutrality.

- Vague answers about credentials: If you have to drag basic qualifications out of them, move on.

A quick comparison

| Green flag | Red flag |

|---|---|

| Explains method | Talks in slogans |

| Reviews documents in detail | Wants to price the claim immediately |

| Works from market evidence | Relies on canned formulas |

| Sets realistic expectations | Promises easy wins |

A good appraiser gives you confidence because their process is solid. A bad one tries to give you confidence by overselling.

Frequently Asked Questions About Vehicle Appraisals

Do I have to pay for the appraisal upfront

Usually, you should expect to discuss fees at the start and understand the billing terms before work begins. Ask exactly what the fee covers, whether there are added costs if the dispute goes further, and what happens if an umpire is needed. If the answer is fuzzy, that's your answer.

Can I pursue diminished value if the car was repaired well

Yes. A proper repair addresses physical damage. It doesn't erase the accident history from the vehicle's market perception. Buyers, dealers, and valuation systems often treat a repaired accident vehicle differently from one with a clean history.

What if the at-fault driver was uninsured

That depends on your policy language and coverage. In Washington, diminished value may be recoverable under uninsured motorist coverage in certain circumstances, as referenced earlier in the article. The first step is to review the policy and confirm whether the appraisal route applies to your coverage dispute.

Can an older car still have a valid claim

Absolutely. Older doesn't mean worthless. Some older vehicles are basic transportation. Some are unusually clean, hard to replace, enthusiast-owned, or fitted with valuable options and recent work. The question is market value and market loss, not just age.

Should I accept the insurer's first offer while I'm deciding

Be careful. Once you settle and release the claim, reopening the value dispute may be difficult or impossible. If the number looks low, pause before signing anything final.

Is this only for luxury or collector cars

No. High-value and collector vehicles often have larger disputes because the market is narrower and insurer software can miss key details. But everyday drivers also get undervalued, especially when condition, maintenance, or local demand aren't reflected correctly.

What if my appraiser and the insurance appraiser disagree

That's exactly why the appraisal process exists. If the gap can't be resolved directly, the next step may be an umpire under the policy terms. The stronger your documentation and method, the stronger your position.

What should I do first after reading this

Do these three things in order:

- Pull your policy and find the appraisal language.

- Collect your documents into one organized file.

- Talk to an independent appraiser before arguing further with the insurer.

That sequence saves time and reduces avoidable mistakes.

If you're dealing with a low total loss offer or a diminished value claim in Washington, Total Loss Northwest helps vehicle owners challenge biased insurance valuations with independent appraisals and Appraisal Clause support. They handle total loss and diminished value disputes across Washington and Oregon, using market-backed reports designed for real negotiation.