The email usually lands after the tow bill, the rental hassle, the body shop calls, and the waiting. You open the settlement offer hoping the hard part is over, then see a value that doesn't come close to replacing your vehicle or accounting for what it lost after the crash.

That moment matters because many drivers treat the insurance number like a verdict. It isn't. It's the insurer's position. If the number is wrong, you can challenge it, and the strongest way to do that is with a Local Independent Appraiser who works for you and knows how to move the dispute out of the insurer's software and into a formal appraisal process.

Your Insurance Offer Is Low Now What

A low offer usually arrives dressed up as a finished decision. It may include comparable vehicles, condition adjustments, or a tidy explanation that makes the number look settled. But in practice, that first number is often just the opening move.

Drivers tend to react in one of three ways. They accept it because they need the money fast. They argue with the adjuster themselves and get nowhere. Or they start gathering listings online, only to learn that random ads rarely beat a formal valuation report.

Why the first offer feels so final

Insurance companies send offers in a format that feels official. That's by design. The number may come from valuation software, database pulls, and internal review steps that are invisible to you. What's missing is your own expert in the room.

A local independent appraiser changes the posture of the claim. Instead of you saying, “I think this is too low,” you now have a qualified professional saying, “Here is the actual market-supported value, and here is how I reached it.”

When the dispute becomes evidence versus evidence, the conversation changes fast.

This is especially important when the broader vehicle market has been unstable. If you want context on how volatile pricing can distort expectations and replacement costs, this piece on understanding used car market chaos is useful background. It helps explain why a canned number from a system may not reflect what people are dealing with on the ground.

What to do before you answer the insurer

Don't rush to reject the offer emotionally. Do a few specific things first.

- Save every document: Keep the valuation report, photos, repair estimate, policy, and every adjuster email.

- Check the vehicle details: Wrong trim, missed options, prior condition errors, and mileage mistakes can all drag value down.

- Ask whether this is a total loss or diminished value dispute: The strategy is related, but the report you need can differ.

- Review your policy language: You're looking for the appraisal provision, often called the Appraisal Clause.

If the number is low, your next move shouldn't be more arguing. It should be building a stronger position with an appraiser who can document the value properly.

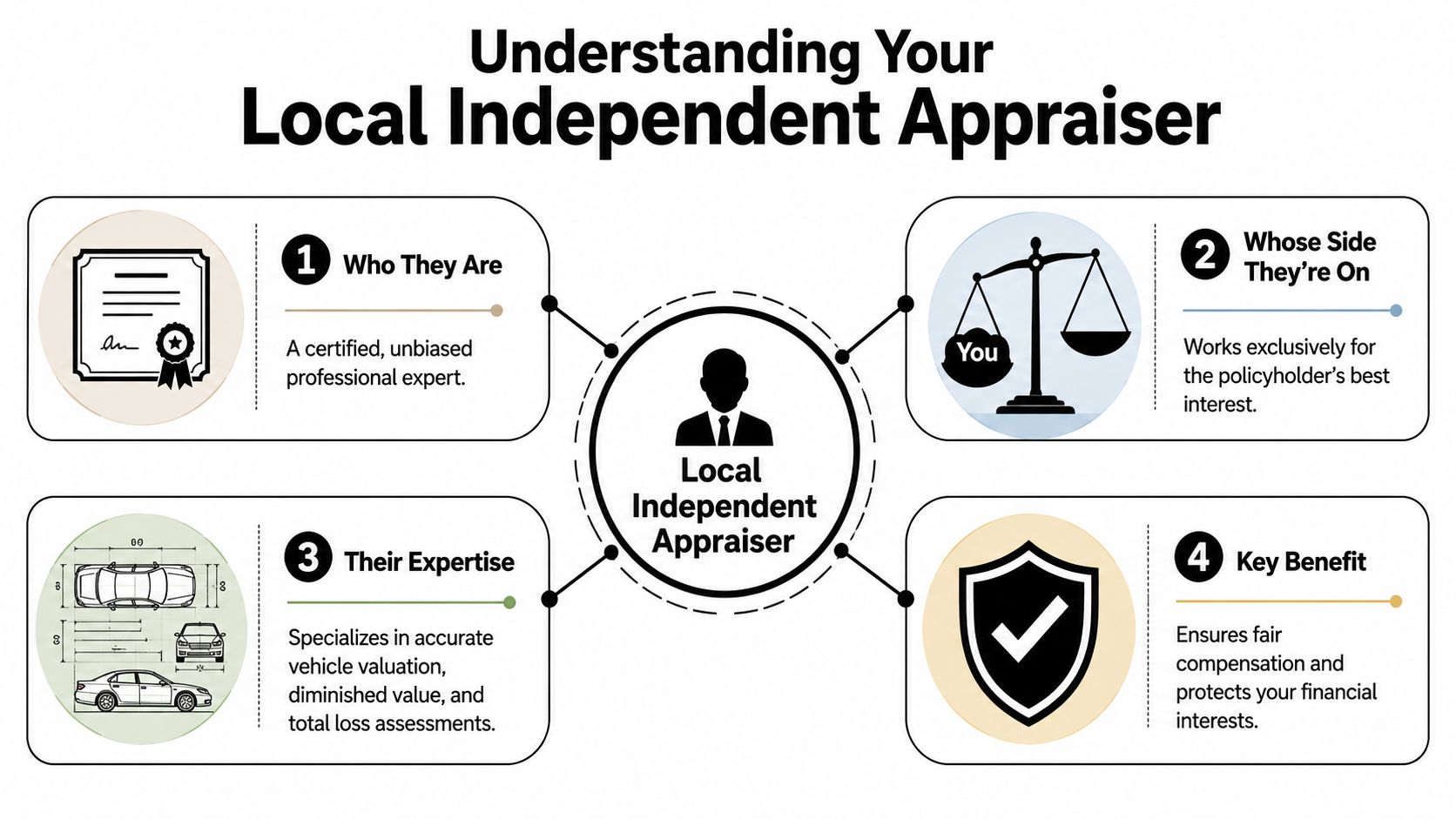

What Exactly Is a Local Independent Appraiser

A local independent appraiser is a certified valuation professional who works for the vehicle owner, not the insurance carrier. In an auto claim, that matters more than is commonly understood.

“Independent” means there's no financial tie to the insurer's outcome. The appraiser is not trying to protect claim severity numbers, internal benchmarks, or software outputs. The assignment is simple. Determine fair market value, diminished value, or total loss value based on evidence.

“Local” is where many claims are won or lost.

Why local knowledge changes the number

Existing content often misses a key point. Local expertise in repair quality and market-specific vehicle depreciation rates directly impacts the accuracy of a diminished value calculation, and repair quality varies significantly by region, which means a non-local appraiser can miss legally significant depreciation factors in the valuation, as discussed in this appraisal discussion on local market knowledge.

In plain terms, the same accident history can affect two similar vehicles differently depending on where they'll be bought and sold. Some markets discount prior damage more aggressively. Some buyers care more about branded repairs, paintwork quality, or where the work was done. A local appraiser knows those patterns because they work inside that market.

What a real appraiser actually does

This isn't just plugging data into a calculator. A qualified appraiser reviews the facts of the loss, inspects condition and equipment, researches relevant comparables, and prepares a report that can stand up in negotiation.

Typical work includes:

- Vehicle-specific analysis: Trim, options, mileage, condition, aftermarket additions, prior history, and repair quality all matter.

- Market research: Comparable sales need to be comparable, not just same make and model.

- Claim-focused reporting: The report has to address the actual dispute, whether that's total loss value or post-repair diminished value.

- Procedural support: In appraisal clause cases, the appraiser also needs to know how the dispute process works, not just how to value a car.

If you want an example of a firm that focuses specifically on these disputes, independent car appraisers can show the kind of services that exist in this niche.

Practical rule: If the appraiser can't explain how local repair reputation affects resale in your area, they're probably not local enough for the job that matters.

The Independent Appraisal vs The Insurer Valuation

Most claim disputes come down to one issue. Whose number controls? The insurer's number often comes from a process optimized for speed and consistency. An independent appraisal is built for accuracy in a specific claim.

That difference isn't academic. It changes what gets counted, what gets ignored, and how hard the final number is to challenge.

Where the methods split

An insurer valuation often starts with software outputs, preset condition assumptions, and a limited comparable pool. That can be efficient. It can also flatten the details that make your vehicle worth more or make your market behave differently.

An independent appraisal is slower because it should be. The appraiser investigates the actual car, the actual damage history, and the actual local market.

| Factor | Insurer's Valuation | Independent Appraisal |

|---|---|---|

| Primary goal | Resolve the claim within the insurer's process | Determine supportable market value for the specific vehicle |

| Method | Often software-driven with standardized inputs | Manual research and expert judgment |

| Comparable vehicles | May rely on broad or imperfect matches | Seeks truly comparable vehicles in the relevant market |

| Vehicle condition | Can be generalized or inconsistently adjusted | Reviewed in detail, including options and prior condition |

| Repair quality impact | May be underweighted in diminished value disputes | Specifically evaluated when relevant |

| Local market knowledge | Often limited by database scope | Central to the opinion of value |

| Who it serves | The insurance company's claim operation | The policyholder who hired the appraiser |

| Use in disputes | Supports the insurer's initial position | Supports negotiation, appraisal clause disputes, and contested settlements |

What works and what doesn't

What works is specificity. A report that identifies the wrong trim level, missing packages, omitted recent comparables, or poor condition adjustments can force movement. What doesn't work is sending the adjuster a pile of online listings with no explanation of why they match your vehicle.

A common mistake is arguing only from emotion. “I can't replace my car for that” may be true, but it won't move a formal dispute. “Your report used mismatched comparables, missed equipment, and failed to account for local post-repair stigma” is a different kind of argument. That's one an appraiser can document.

Why this matters in total loss and diminished value cases

Total loss cases usually turn on replacement-oriented market value. Diminished value cases turn on post-repair stigma and how buyers react to damage history. In both settings, the insurer's system may produce a neat answer without capturing the full market reality.

That's why a local independent appraiser isn't just another opinion. In the right procedural posture, it becomes the valuation evidence that can displace the insurer's own.

How the Appraisal Clause Gives You Power

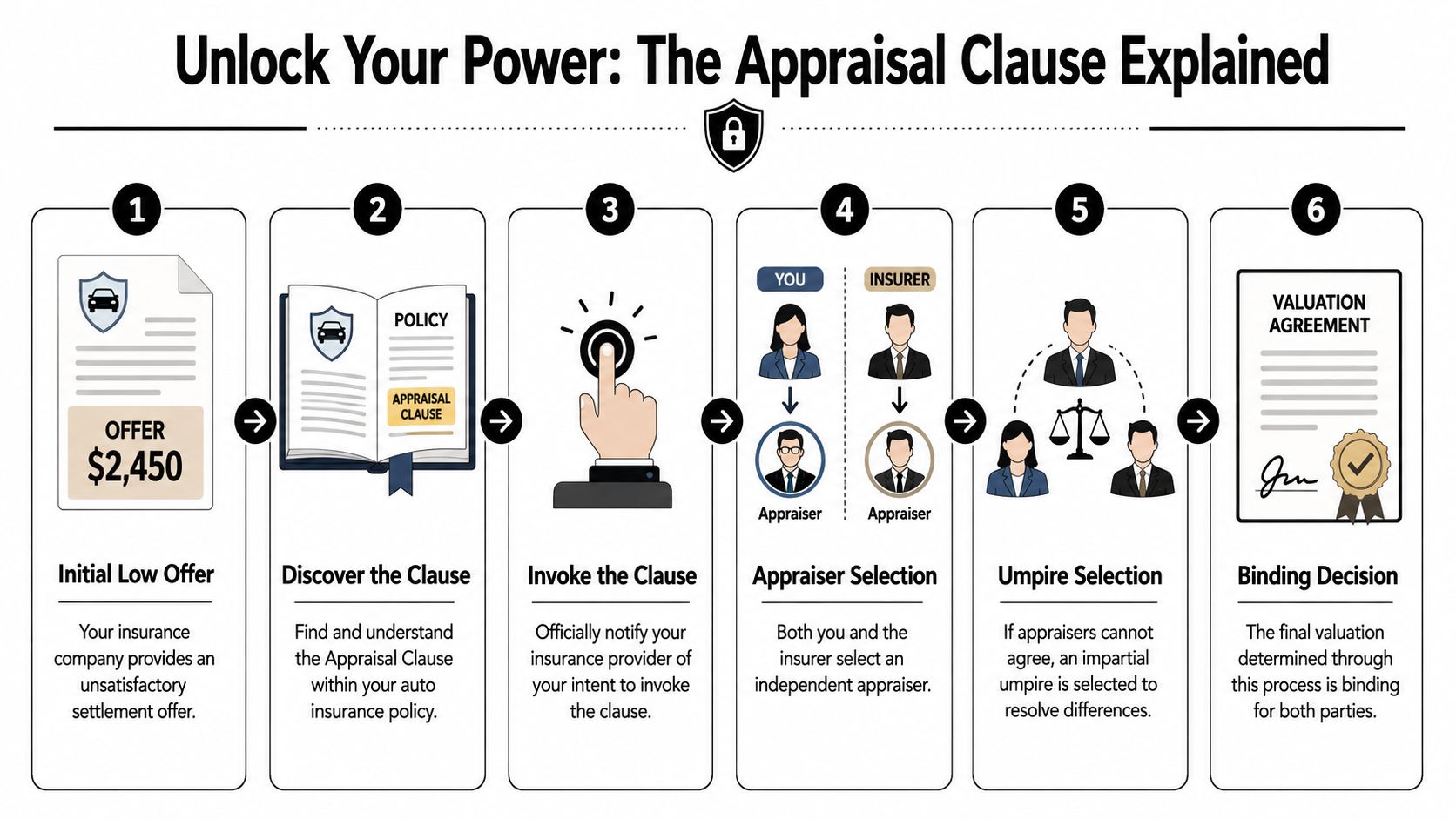

Most policyholders don't realize their own policy may contain the tool that changes the whole fight. The Appraisal Clause is the mechanism that lets you formally challenge the insurer's valuation and require a structured dispute process.

This is the inside game most generic claim guides skip. They tell you to negotiate harder, ask for reconsideration, or send more comps. None of that has the force of invoking the policy provision that moves the dispute out of the insurer's software lane.

What the clause actually does

The critical point is this: the Appraisal Clause is the specific legal mechanism allowing independent appraisers to override biased insurer algorithms in auto claims, a procedural reality general consumer guides often miss, as noted in this discussion of questions to ask an appraiser.

Once invoked under the policy terms, the process usually works like this:

- You notify the insurer that you dispute the valuation and are invoking the appraisal provision.

- You select your appraiser.

- The insurer selects its appraiser.

- The two appraisers review the loss and try to agree on value.

- If they don't agree, they select an umpire.

- The decision reached through that process becomes binding under the policy terms that apply.

Here's a visual walkthrough of the process:

Why insurers take this more seriously

An adjuster can brush off a complaint email. It's much harder to brush off a formal invocation of contract rights. Once appraisal is triggered, the claim stops being just an internal negotiation and becomes a defined dispute process with designated experts.

That shift matters because it removes the insurer's valuation software from center stage. The conversation becomes expert appraisal, rebuttal, negotiation, and if needed, umpire review.

A lot of claimants think they need the insurer's permission to challenge value. They usually don't. They need to use the process already written into the policy.

Where people go wrong

The biggest mistakes are procedural:

- Waiting too long: Some drivers argue for weeks without checking whether the policy already gives them a better route.

- Hiring the wrong appraiser: General valuation knowledge isn't enough. The appraiser has to understand clause disputes.

- Sending vague notice: The insurer should receive a clear written invocation tied to the policy language.

- Treating the umpire as an afterthought: In some disputes, the umpire becomes essential.

If you're dealing with a contested valuation and need to understand the neutral third-party role in this process, appraisal clause umpire is the exact issue to study.

Finding and Hiring the Right Appraiser

Once you decide to challenge the insurer's number, the next risk is hiring someone who sounds credible but can't carry a disputed claim. Not every appraiser is equipped for total loss or diminished value work, and not every appraiser knows how to operate inside an appraisal clause dispute.

What qualifications actually matter

Becoming a certified appraiser requires a minimum of 200 hours of instruction and 2,500 hours of experience over no fewer than 24 months, according to the Appraiser Qualifications Board, which is why trained appraisers can produce reports built to hold up in negotiations and formal disputes, as outlined by The Appraisal Foundation's career requirements guide.

That doesn't mean every licensed or certified appraiser is right for your claim. You want someone whose day-to-day work includes valuation disputes, not someone who only does occasional reports.

Questions worth asking before you hire

Ask direct questions. If the answers are fuzzy, move on.

- How often do you handle total loss or diminished value claims? You want repetition, not theory.

- Have you worked inside the appraisal clause process before? The report and the strategy have to fit the procedure.

- What market data do you rely on? A serious appraiser should be able to explain their comparable research approach.

- Do you understand local repair reputation and regional resale behavior? This matters in diminished value cases.

- Can your report be used in negotiations or legal settings if needed? Some reports are written well. Others are written to survive scrutiny.

One practical way to evaluate pricing logic across specialized appraisal fields is to look at how other industries frame complexity, documentation, and expert time. This overview of professional watch appraisal costs is outside auto claims, but it's a useful reminder that good appraisal work is skilled analysis, not commodity paperwork.

Red flags you shouldn't ignore

A few warning signs show up over and over:

- Guaranteed outcomes: No honest appraiser should promise a result before reviewing the file.

- No local footprint: If they can't speak intelligently about your area, they may miss market effects that matter.

- Thin reports: A short conclusion with no support won't carry much weight.

- No procedural knowledge: If they only talk about “sending a report” and not how the dispute advances, that's a problem.

One example of a specialized provider in this space is Total Loss Northwest, which handles independent auto appraisals for total loss and diminished value disputes in Oregon and Washington. That's the kind of specialization you're looking for, whether you hire them or another firm.

The right appraiser doesn't sell confidence. They show process, market knowledge, and a report structure that can survive pushback.

Expected Costs Timelines and Outcomes

Hiring an appraiser costs money. That's the part drivers hesitate on, especially after towing, rentals, deductible issues, and missed work. But the right way to look at the fee is simple. You're not buying paperwork. You're buying a valuation position strong enough to challenge the insurer's number.

What the cost usually means

Appraisal fees vary with claim type, vehicle complexity, and how far the dispute has already progressed. A straightforward review is different from a contested appraisal clause matter involving extensive comparable research and negotiations with the insurer's appraiser.

The work also reflects the level of expertise involved. The median annual wage for property appraisers and assessors was $65,420 in May 2024, and professionals handling more complex legal valuation matters often earn more because the work carries higher stakes and requires stronger report discipline, according to the U.S. Bureau of Labor Statistics occupational outlook.

If you want a realistic sense of how firms structure these fees in auto claims, car appraisal cost is the practical question to research before you commit.

How long it takes

Most credible appraisals aren't instant. The timeline depends on how quickly documents arrive, whether the vehicle can be inspected, and how complex the market research is. If appraisal clause procedures are already active, timing can also depend on the other side's response.

Typical timing factors include:

- Document availability: Delays usually start when the policy, insurer valuation, photos, or repair records are incomplete.

- Vehicle type: Common daily drivers are easier to comp than modified, collector, or unusual vehicles.

- Claim posture: A report for negotiation is one thing. A formal dispute with appraiser-to-appraiser exchange takes longer.

What outcomes to expect

The honest answer is that no appraiser can promise a result. What you should expect is a stronger claim file, a more defensible value position, and a process that forces the insurer to engage with evidence instead of asking you to trust its internal number.

Good outcomes usually look like one of these:

- A revised settlement before full dispute escalation

- A negotiated number between appraisers

- An umpire-supported value if the appraisers don't agree

- A clearer answer on whether the insurer's offer was defensible after all

Not every case produces a dramatic swing. Some produce a modest correction. Some confirm the original offer was closer than the owner thought. The value of the process is that you stop guessing and start working from a professional opinion.

Your Next Step to a Fair Settlement

If your insurance offer is low, the mistake is treating the situation like a customer service problem. It's a valuation dispute. That means the solution isn't more frustration, more phone calls, or more guessing from online listings.

The smarter move is to bring in a Local Independent Appraiser who can assess the vehicle in the context that matters: your market, your claim type, and your policy rights. When the appraisal clause applies, that appraiser doesn't just give you another opinion. They help move the dispute into the one process that can legally displace the insurer's preferred number.

Independent appraisal is not some fringe tactic. It sits inside a profession with real economic weight. The U.S. real estate appraisal industry, which includes independent appraisers, has a market size of $10.3 billion as of 2026, underscoring how central independent valuation is in high-stakes financial and legal matters, according to IBISWorld's industry overview.

Review your policy. Find the appraisal language. Get your file organized. Then talk to an appraiser who knows how insurance valuation disputes work.

You don't have to accept a number just because it arrived in an official-looking email.

If you're dealing with a low total loss or diminished value offer, Total Loss Northwest provides certified independent auto appraisals and appraisal clause support for drivers who need a market-based valuation instead of an insurer-driven number.