You open the estimate, read the total loss number, and your stomach drops. The insurer says that's what your vehicle was worth. You know it isn't. You've maintained it, upgraded it, kept records, and now an adjuster using software you've never seen is telling you what your car was worth the day before the crash.

That moment is where a lot of drivers get pushed into a bad decision. They assume the offer must be close enough, or that fighting it will take a lawyer, months of stress, and more energy than they have. Insurers count on that. They know many owners will take a weak offer just to move on.

If you're in Oregon or Washington and you're dealing with a low total loss offer, you need to treat this like a contract dispute with evidence, deadlines, and advantage. Some bad faith insurance practices are obvious. Others look like routine claims handling until you slow down and document what the company is doing. The biggest mistake is staying passive.

Your Total Loss Offer Is Low Now What

A driver gets rear-ended, the car is declared a total loss, and the insurer sends over a valuation report. The comparables are wrong. Trim level is off. Mileage adjustments don't make sense. Options are missing. Condition is flattened into a generic rating. Then the adjuster says some version of, “This is our standard market valuation.”

That's where people get trapped.

Your policy isn't a favor. It's a contract. You pay premiums, follow claim procedures, and cooperate. In return, the insurer owes you more than a fast response. It owes you good faith and fair dealing. That means a fair investigation, a fair valuation, and a fair explanation. When the company cuts corners, hides behind vague language, or pressures you to accept less than the vehicle's actual value, the problem isn't just annoyance. It may be one of the bad faith insurance practices drivers run into every day.

What to do in the first 48 hours

Don't argue on the phone and don't accept the number verbally.

Do this instead:

- Ask for the full valuation report: Get every page, including comparable vehicles, option list, condition ratings, and adjustments.

- Move communication to writing: Email is better than phone calls. If they call, send a follow-up email summarizing what was said.

- Preserve your own file: Photos, service records, upgrade receipts, prior listings, and anything that shows pre-loss condition and market value.

- Learn how lowball offers are built: This breakdown of a lowball insurance settlement offer will help you spot where the insurer may be shaving value.

Practical rule: If an insurer can't explain its number clearly in writing, don't trust the number.

If you need to push back formally, a structured letter helps. A practical starting point is this CasePulse demand letter resource, especially if you need to organize your facts, losses, and supporting documents into something the adjuster can't brush aside.

What not to do

A lot of owners sabotage their own claim without realizing it.

| Misstep | Why it hurts you |

|---|---|

| Accepting “pending review” language at face value | It lets delay drag on without forcing a firm position |

| Sending partial evidence | The adjuster fills gaps in their favor |

| Relying on phone conversations | You lose the paper trail |

| Treating the first offer like a final fact | It's often just the insurer's opening position |

You don't need to panic. You need to get organized and stop letting the insurer control the frame of the dispute.

What Is Insurance Bad Faith Legally Speaking

Think of insurance like hiring a bodyguard. You pay them ahead of time so they'll protect you when trouble shows up. If trouble arrives and your bodyguard walks away, stalls, or starts helping the other side, that isn't just disappointing service. That's a breach of the job you hired them to do.

That's the basic idea behind insurance bad faith.

In plain English, bad faith happens when an insurer unreasonably refuses to do what the policy and the law require. It goes beyond a routine disagreement over value. A contract dispute says, “We disagree.” A bad faith claim says, “The insurer acted without proper cause, handled the claim unfairly, or used its position to dodge obligations.”

One legal example that matters

A clearly defined form of bad faith is the unreasonable failure to settle within policy limits. Justia's explanation of insurance bad faith describes it this way: the insurer rejects a reasonable settlement demand within policy limits, and that refusal leads to an excess judgment the insured has to pay personally. To prove it, the claimant must show the offer was within policy limits, the insurer refused without proper cause, and that refusal directly caused the judgment above those limits.

That example usually comes up in liability claims, but the principle matters in total loss fights too. The key issue is reasonableness. Insurers don't get to hide behind process while making decisions that aren't grounded in a fair evaluation.

The difference between hard bargaining and bad faith

Not every low offer is automatically bad faith. Some adjusters are just wrong. Some reports are sloppy. Some disputes are genuine.

But there's a line.

When the insurer delays, misstates coverage, ignores evidence, or refuses to support its position with a real investigation, it stops looking like negotiation and starts looking like misconduct.

Use this simple test:

- A legitimate dispute usually comes with a specific written explanation, supporting documents, and a willingness to review new evidence.

- Bad faith behavior usually comes with stonewalling, recycled talking points, missing reasoning, shifting explanations, or pressure to accept less before you can verify the valuation.

Why drivers should care about the legal label

Because labels create advantage.

If you call everything “bad faith,” you weaken your own position. If you identify the exact conduct, document it, and tie it to the claim file, you become much harder to ignore. That's how owners stop sounding emotional and start sounding dangerous to a careless insurer.

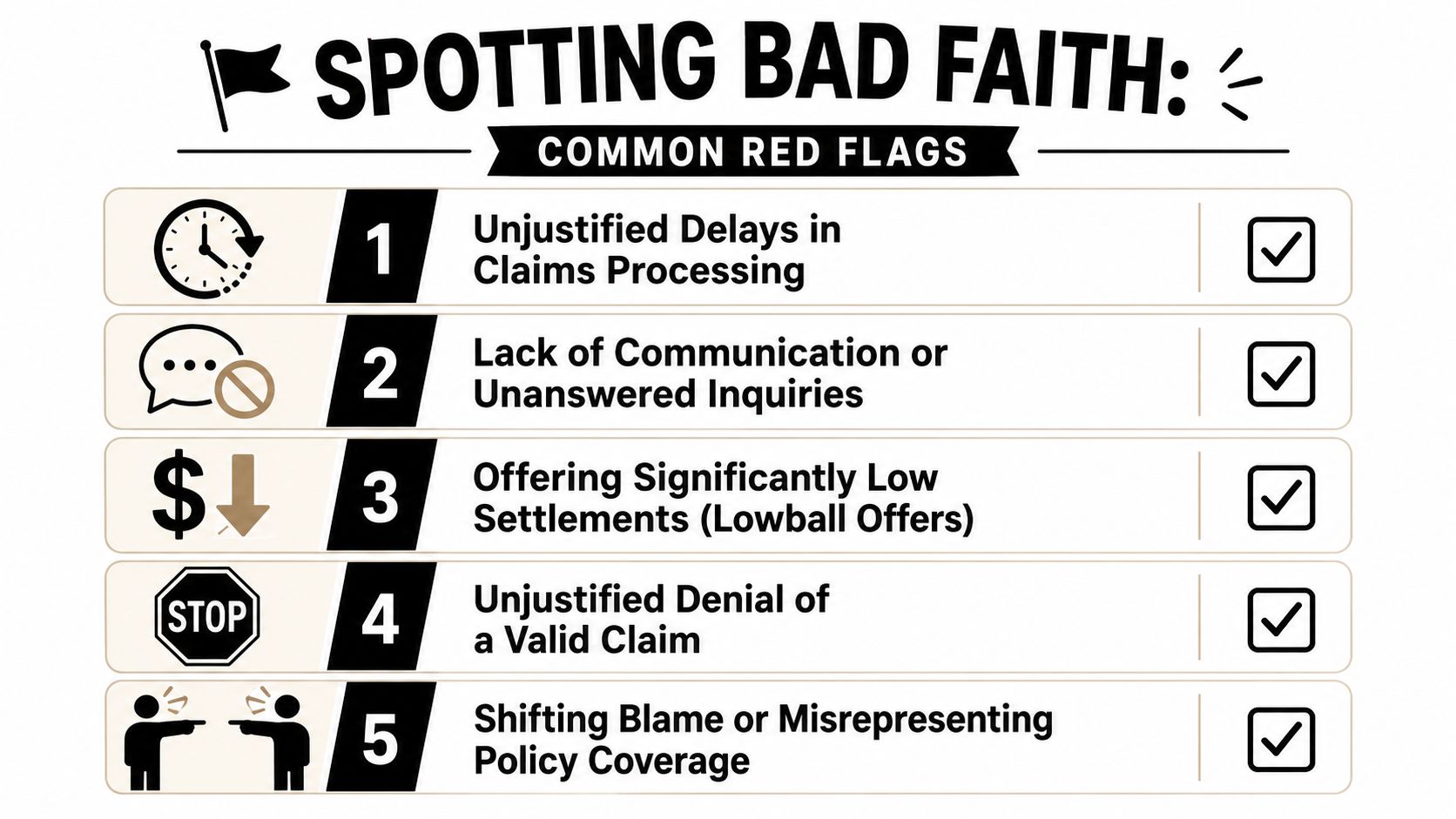

Common Red Flags of Bad Faith Insurance Practices

You don't need a law degree to spot bad faith insurance practices. You need a checklist and enough discipline to compare what the insurer is doing against what a fair claims process should look like.

Start with this.

Delay that serves no real purpose

One of the clearest warning signs is delay. Eglet Law's discussion of insurance bad faith identifies a specific benchmark: failure to affirm or deny coverage within a reasonable time after receiving a claim. It also notes a common tactic, requesting unnecessary paperwork or reports that aren't required to process the claim.

That matters in total loss cases because delay creates pressure. You still need transportation. Storage fees may be running. Your financing doesn't disappear. The insurer knows time works in its favor.

Silence, vagueness, and missing answers

An adjuster who won't answer direct written questions is telling you something. So is an insurer that keeps saying it is “reviewing” the file but never addresses your evidence.

Watch for this pattern:

- Repeated non-answers: You ask why a comparable was used. They reply with boilerplate about market valuation.

- No explanation of adjustments: Mileage, options, trim, or condition changes appear in the report with little or no support.

- Shifting positions: The reason for the offer changes depending on who you talk to.

If every answer gets less specific the more precise your question becomes, assume the claim handling is weak.

Lowball valuations dressed up as objective software

This is common in auto claims. The report looks official because it came from a platform like CCC ONE or Mitchell, but software doesn't make a valuation fair. Garbage in still produces garbage out.

Bad signs include:

- Wrong vehicle configuration

- Missing packages, aftermarket additions, or major options

- Poor comparables from different markets or weaker condition

- Condition ratings that ignore records and photos

- Unexplained downward adjustments

For drivers dealing with other consumer disputes in Washington, the broader mindset is similar. This guide on legal advice on predatory lending in Washington is useful because it shows how abusive practices often hide inside technical paperwork and one-sided processes. Insurance carriers use different tools, but the power imbalance feels familiar.

Denials without a real investigation

A denial isn't automatically bad faith. A denial without a serious investigation is a problem.

If the insurer ignores your maintenance history, skips obvious market evidence, or refuses to address errors you pointed out in writing, it may be building a paper shield rather than conducting an honest review.

The common thread in bad faith insurance practices is simple. The company acts like speed and cost control matter more than accuracy.

Bad Faith Insurance Laws in Oregon and Washington

Oregon and Washington both regulate unfair claim handling. The exact legal routes differ, but the basic message is the same: insurers aren't free to play games with communication, investigation, valuation, or settlement practices.

In Oregon, drivers often hear about unfair claim settlement standards under state law. In Washington, unfair practices are also addressed through insurance regulations and consumer protection tools. You don't need to memorize the citations on day one. You need to understand that low-quality claim handling may be more than “frustrating.” It may be unlawful.

Why the law matters even if you never sue

Most claims don't start in a courtroom. They start with a file, a timeline, and whether the insurer believes you can prove its handling was unreasonable.

That's why legal standards matter. They shape how supervisors, compliance teams, outside counsel, and regulators evaluate a claim. They also shape settlement bargaining positions.

A broader national survey shows how seriously some states treat bad faith. According to the United Policyholders national bad faith survey, statutory frameworks in some states allow insureds to recover punitive damages up to three times their actual damages, with Colorado cited as an example under its Consumer Protection Act. That doesn't mean Oregon or Washington use the same formula in every case. It does show that bad faith is not treated as a minor paperwork issue.

What Oregon and Washington drivers should focus on

Don't get lost in legal theory. Focus on conduct.

| Claim handling issue | Why it matters |

|---|---|

| Misrepresenting coverage or claim standards | It can distort your decisions and force a cheap settlement |

| Unreasonable delay | It pressures you financially and weakens your bargaining position |

| Failure to investigate | It signals the insurer chose a result before reviewing the facts |

| Unfair settlement offers | It may reflect a valuation process designed to suppress payout |

If your dispute involves whether the vehicle should have been treated as a total loss in the first place, review how a constructive total loss works. That issue often sits upstream of valuation and can affect the entire claim path.

Bottom line: The insurer doesn't get a free pass because its report looks technical. If the handling is unfair, state law may give that unfairness real consequences.

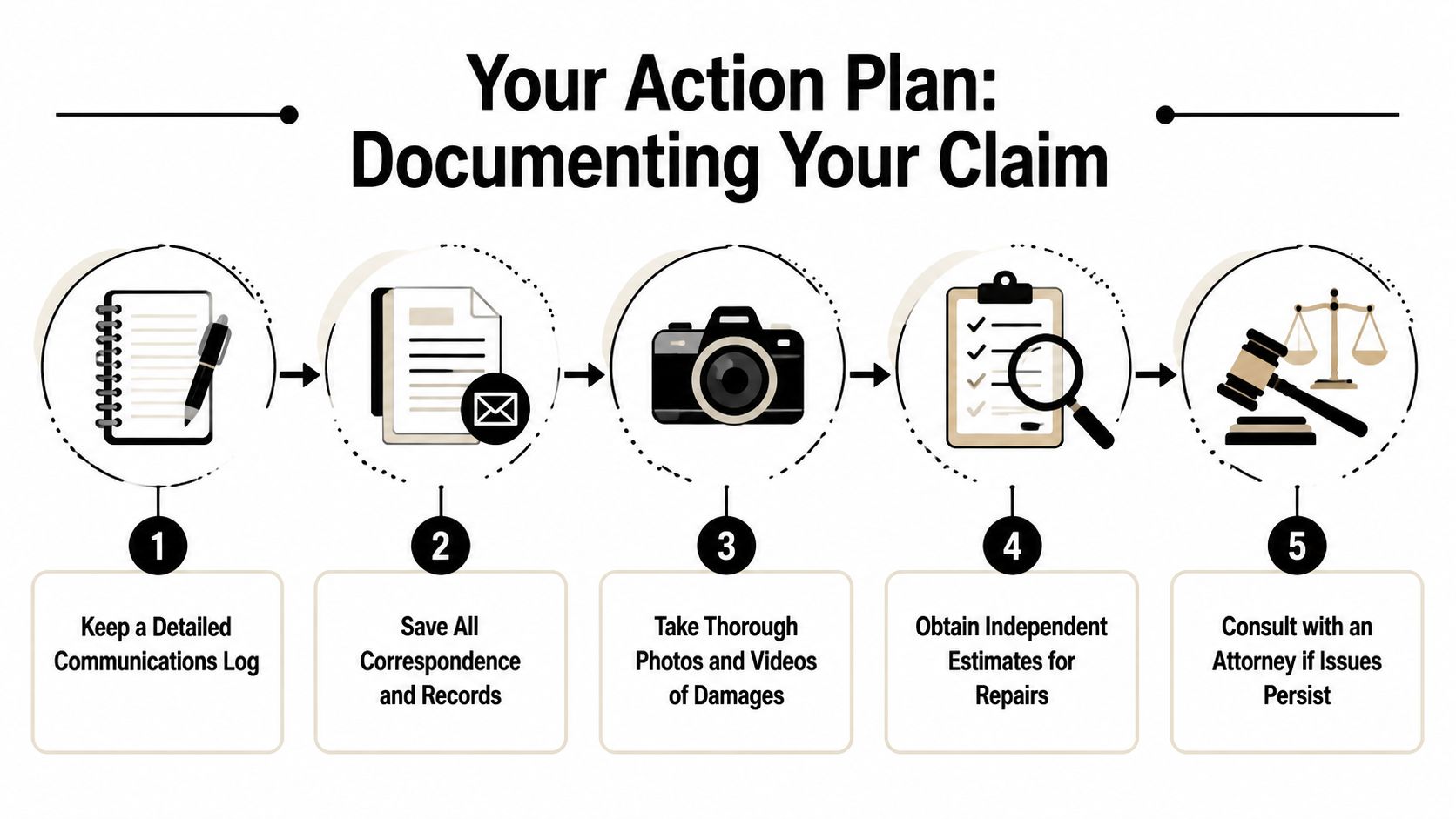

Your Step by Step Action Plan to Document Everything

Bad faith claims are won or lost on documentation. Not emotion. Not outrage. Not what the adjuster “basically said.” If it isn't preserved, it may as well not have happened.

Start building your file today.

Build one master claim file

Use one folder, digital or physical, and keep everything there. Don't scatter evidence across voicemail, text threads, email folders, and your camera roll.

Your file should include:

- The policy documents: Declarations page, relevant endorsements, and any policy language on valuation or appraisal.

- The valuation package: Every report, comparable sheet, adjustment page, and settlement letter.

- Your evidence of value: Maintenance records, receipts, photos, window sticker, listings for similar vehicles, and proof of upgrades.

- Every communication: Emails, letters, notes from calls, voicemail summaries, and claim portal screenshots.

Keep a communication log like a professional

Make a simple running log with date, time, person, title, phone number, and summary. If the adjuster says your options were included, note it. If they promise a callback by Friday, note it. If they ask for documents you already sent, note that too.

This log does two jobs. It refreshes your memory, and it exposes patterns. Repeated delays and repeated requests for the same materials stop looking accidental once they're laid out in order.

A clean timeline is often more persuasive than an angry letter.

Force important points into writing

If the insurer calls, follow up with an email. Keep it short and factual.

For example:

- Confirm the conversation: State the date and who you spoke with.

- Summarize the insurer's position: Include what they said about value, comparables, or claim status.

- Request a written response: Ask them to confirm the basis for disputed points.

Vague oral statements often disappear later, which presents a challenge.

Ask targeted questions, not broad complaints

Don't write, “Your offer is unfair.” Write questions the insurer has to answer.

Examples:

- Which comparable vehicles were adjusted for trim and options, and how?

- Why was this vehicle condition rating assigned despite service records and photos?

- What evidence supports the mileage adjustment?

- What specific documents are still missing, if any?

Get your own independent support

Insurers rely on their own valuation systems. You should rely on independent evidence.

That can include:

- Market listings for similar vehicles in your region

- Independent repair or condition opinions

- An appraiser who knows total loss disputes

- Pre-loss photos and ownership records

A strong file does something important. It changes the conversation from “I feel lowballed” to “Here are the specific defects in your valuation and the record of how you handled this claim.”

If the insurer still stalls after that, you're no longer guessing. You're building a case.

Using the Appraisal Clause to Fight Lowball Offers

If you own a totaled vehicle in Oregon or Washington, the Appraisal Clause is often your best move when the insurer's number is wrong. Not maybe. Often.

Why? Because it takes the valuation fight out of the adjuster's comfort zone.

Insurers like disputes they control. They control the software, the vendor inputs, the claim notes, and the pace of review. The Appraisal Clause interrupts that. It creates a formal process where each side selects an appraiser, and the dispute moves toward an independent value determination under the policy terms.

Why this matters more than arguing with the adjuster

A lowball total loss offer usually doesn't get fixed because you had a better phone call. It gets fixed when the insurer is forced to defend its number in a process it can't casually steer.

The history of bad faith litigation shows what happens when insurers refuse to honor contractual duties. In 2001, toxic mold became a major catalyst for bad faith litigation, with approximately 5,000 cases filed directly against insurance companies for refusing to uphold their obligations, according to the Wikipedia overview of insurance bad faith. The lesson is simple. When claim handling breaks down systematically, policyholders push back through contract rights and litigation.

The Appraisal Clause is one of those contract rights.

What the clause actually does

It doesn't automatically prove bad faith. It does something more practical. It provides an advantage concerning value.

Here's what it changes:

- The insurer's internal valuation stops being the only number on the table

- An independent appraiser can challenge bad comparables and bad adjustments

- The process becomes structured instead of informal

- You stop begging for reconsideration and start invoking a policy right

If you want a clearer picture of how this process works, review this explanation of the insurance appraisal clause.

When to use it

Use it when the dispute is about value and the insurer isn't correcting obvious defects. Especially if the report shows wrong trim, missing features, poor comparables, or condition adjustments that don't match reality.

For negotiation tactics around settlement pressure, this guide on strategies to negotiate fair compensation is also useful. It isn't about total loss appraisal specifically, but it does reinforce a point I agree with completely: negotiation gets stronger when you stop reacting emotionally and start pushing with documented positions.

The Appraisal Clause is the moment you stop asking the insurer to be fair and start requiring a fair valuation process.

If your dispute is over value, don't waste weeks arguing in circles. Read the policy. Find the clause. Use it.

Frequently Asked Questions on Bad Faith Claims

Is a low offer automatically bad faith

No. A low offer can be incompetence, weak data, or a real dispute. It starts looking like bad faith when the insurer won't explain the number, ignores evidence, delays decisions, or keeps using a flawed valuation after you've shown the flaws.

How do I prove the insurer failed to investigate properly

Use evidence, not conclusions. Jeffress Law's discussion of bad faith practices points to the kind of proof that matters: correspondences showing skipped steps, records of ignored expert reports, and timestamps of unreturned calls. In an auto claim, I'd add written proof that the insurer overlooked vehicle options, used bad comparables, or failed to address condition records you provided.

Can I sue my own insurance company

In many situations, yes, depending on the policy, the claim type, and state law. First-party bad faith usually involves your own insurer handling your claim unfairly. But suing shouldn't be your first move in a value dispute if the policy gives you a contractual tool like appraisal. Use the cleaner, faster advantage first when it fits.

What if the other driver's insurer is the problem

That's a different posture. Third-party claims can still involve unfair tactics, but the legal duties and remedies may differ from a claim against your own carrier. The practical advice stays the same. Keep everything in writing, document every delay, and don't accept vague explanations.

Should I keep talking by phone

Only if you immediately memorialize the call in writing. Phone calls benefit the insurer unless you turn them into a dated record.

What's the single biggest mistake drivers make

They assume the insurer's report is objective because it looks technical. A polished report can still be wrong. A repeated wrong number doesn't become fair just because the adjuster repeats it politely.

If your total loss offer doesn't match the actual market value of your vehicle, get independent help before you sign away your advantage. Total Loss Northwest handles total loss and diminished value appraisals for Oregon and Washington vehicle owners, including Appraisal Clause disputes that take the valuation fight out of the insurer's software and back into a fair process.