The envelope shows up when you're still dealing with the crash, the body shop, missed work, and the mental replay of what happened. Inside is an accident settlement form that looks routine. It isn't routine.

It's the point where people accidentally give away money, rights, and their strategic advantage.

I've seen insurers package a low offer inside paperwork that looks harmless. A release, a check, a friendly note from the adjuster, maybe a line that says they're trying to “help you move forward.” What they're really trying to do is close the file cleanly and cheaply. Your job is different. Your job is to make sure the number reflects the full damage, and that the form doesn't take more than the deal is worth.

What Is This Form and Why Does It Matter So Much

When individuals refer to an “accident settlement form,” they are typically discussing a Release of Liability or a settlement agreement. That document is not a receipt. It is a contract.

Once you sign it, you usually give up the right to ask for more money for that accident. That includes problems you already know about and, in many forms, problems you don't know about yet.

What the insurer wants

The insurer wants finality. They want your signature on a document that says the matter is over.

That's why these forms often sound broad. They don't just say they're paying for the bumper or the emergency room visit. They're usually drafted to shut down every related claim tied to the crash.

Practical rule: If the form says “full and final settlement,” read that as “no second chance.”

What you should care about

You need to know three things before that pen touches paper:

- What claim is being released. Is it only property damage, or property damage plus bodily injury?

- Who is being released. The other driver, the insurer, related companies, other potentially responsible parties.

- Whether the payment fully covers your loss. Not just the part the insurer chose to value.

A lot of people sign too early because the document looks administrative. It isn't. It is the legal endpoint of the claim.

If you want a plain-English reference that helps you understand injury-side paperwork and claim issues, Northern Wisconsin personal injury legal resources can help you organize what questions to ask before signing anything.

Why this matters more than people think

The biggest mistake I see is passivity. People assume the form arrives after the “hard part” is over. In reality, the form is where the hard part becomes permanent.

Read it like someone negotiating a contract, not like someone processing mail. If the offer is wrong, the form is wrong. If the vehicle value is wrong, the form locks in the wrong number. If the injury picture isn't complete, the form can shut the door before the full damage is known.

That's why you should treat the accident settlement form as the most important document in the claim. Because it is.

Decoding the Fine Print Before You Sign

Most forms bury the most important language in plain sight. The dangerous part isn't usually hidden in tiny font. It's hidden behind legal phrases that sound standard.

The pressure is real because pre-litigation settlements resolve 95% of U.S. claims, yet 35% of claimants who sign quickly regret it as injuries show up later, and New York courts uphold 98% of signed releases according to Brown & Crouppen's settlement process overview. Once signed, those releases are hard to unwind.

Phrases that should stop you cold

If you see these terms, slow down.

- Release of all claims. This usually means exactly what it says. Not one claim. All claims tied to the crash.

- Known and unknown injuries. That language is there for a reason. It protects the insurer if your symptoms get worse later.

- Full and final settlement. No reopening because your treatment changed or the repair supplement grew.

- Indemnification. This can create future obligations if another party later seeks payment connected to the same accident.

A few examples of how this language works in real life:

“Releasor forever discharges any and all claims arising out of the accident.”

That means the claim doesn't come back because you later discover more damage.

“Including all known and unknown bodily injuries and property damage.”

That means the form is trying to cover surprises too.

Check the form for basic accuracy first

Before you even evaluate the dollar amount, verify the document is correct. Insurers process a lot of claims. Errors happen, and errors matter.

Here's the checklist I'd use before discussing value.

| Document Type | Why You Need It | Where to Get It |

|---|---|---|

| Police report | Confirms date, location, drivers, and initial fault details | Law enforcement agency that responded |

| Claim number and policy details | Ties the release to the correct file and insurer | Adjuster or insurer correspondence |

| Repair estimate or total loss valuation | Shows what the insurer is actually paying for vehicle damage | Body shop, insurer valuation report, appraiser |

| Medical records and bills | Verifies injury treatment tied to the accident | Treating providers and billing departments |

| Wage loss proof | Supports missed work or reduced earnings | Employer payroll or HR records |

| Photos of damage and scene | Helps confirm accident details and severity | Your phone, witnesses, towing records |

What to verify line by line

Read every page, and specifically verify:

- Names are correct. Yours, the driver's, and the vehicle owner's if different.

- Date of loss is correct. One wrong digit can create confusion later.

- Claim or policy numbers match the accident you're settling.

- The release scope is limited or broad. Know which one you're signing.

- Property damage and injury claims aren't being mixed together unless that's intentional.

- The amount written into the form matches the negotiated amount.

If the adjuster says, “It's standard,” that tells you nothing. Standard for whom? Standard to close a file fast, maybe.

The form should reflect the exact agreement. If it doesn't, send it back and force a revision.

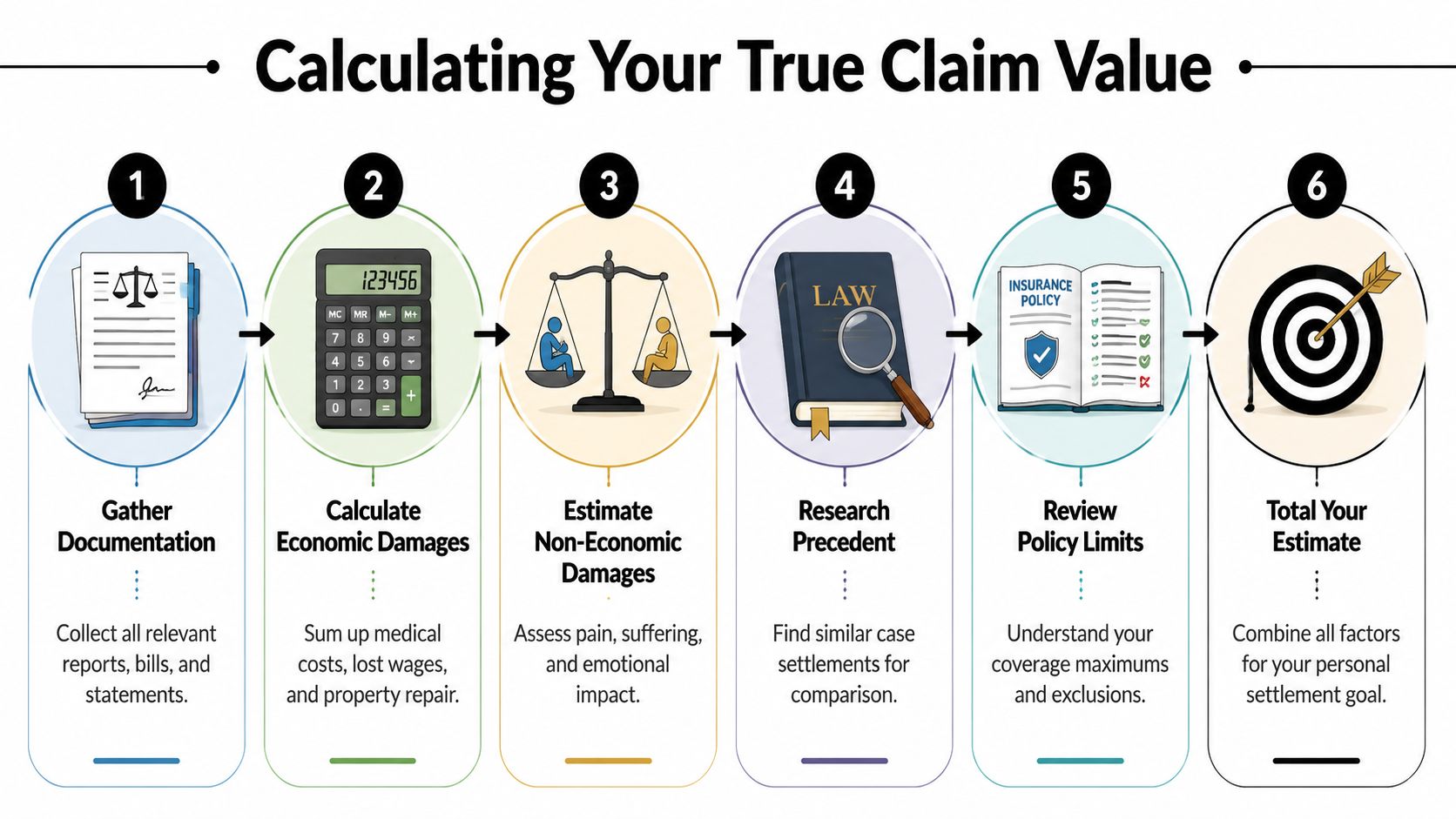

Is the Settlement Amount Fair? Calculating Your True Value

Insurers love starting from their number. That's your first mistake if you let them. Start from your loss.

A fair settlement has to account for what the crash cost you, not what their software decided to spit out on the first pass. That means adding up your economic damages, valuing pain and suffering in a grounded way, and not forgetting the vehicle-side losses that people miss all the time, especially diminished value and a bad Actual Cash Value total loss figure.

Start with the hard costs

Economic damages are the foundation. These are the losses you can document.

That usually includes:

- Medical bills tied to the crash

- Lost wages if you missed work

- Property damage to the vehicle

- Out-of-pocket costs connected to the claim

For injury valuation, the multiplier method is a common formula. It uses economic damages as the base and applies a 1.5 to 5 multiplier based on severity. A commonly cited example is that $20,000 in bills for a moderate injury with a multiplier of 3 could justify $60,000 for pain and suffering on top of the economic damages, as explained in this guide to calculating car accident settlements.

Then account for the losses insurers like to minimize

People often leave money behind.

If your car was repaired, it may still be worth less than it was before the crash. That's diminished value. A clean-history vehicle with accident history is not the same asset it was before. Buyers know that. Dealers know that. Insurers know that too, even if they act surprised when you bring it up.

If your car was totaled, the fight shifts to Actual Cash Value. That number should reflect a real market value for your specific vehicle, not a lazy comp set and canned adjustments. If you need a framework for challenging that number, this guide on how to calculate fair market value is a useful reference point.

A better way to think about your number

Don't ask, “Is this offer bad?” Ask, “What would it cost to make me whole?”

Use a simple worksheet:

- Medical and wage losses

- Vehicle repair or total loss value

- Rental and related transportation costs

- Diminished value if repaired

- Pain and suffering

- Any future treatment concerns already identified

If your recovery includes rehab, don't treat that as background noise. Continued care can be a major part of the claim, and understanding the role of physical therapy after a car accident can help you document why the insurer's “you should be done by now” argument often falls apart.

The insurer's first valuation is a negotiating position. It is not a verdict on what your claim is worth.

A fair number comes from records, market evidence, and complete accounting. Not convenience.

Common Pitfalls and Why You Never Accept the First Offer

The first offer is usually designed to test whether you know what you're doing. If you accept it fast, the insurer learns something important. They learn they didn't need to pay more.

That's why I'm blunt about this. You should assume the first offer is incomplete until you prove otherwise.

The most common ways people undercut their own claim

Some mistakes happen because people are overwhelmed. Others happen because adjusters are trained to move the file toward closure.

Watch for these traps:

- Signing without review. That's one of the worst moves you can make. Unrepresented claimants settle for 30% to 50% less than represented peers, according to Daeryun Law's analysis of accident settlement forms.

- Settling before treatment is clear. If you don't understand the medical picture, you can't price the claim correctly.

- Ignoring diminished value. A repaired car with accident history may still have lost market value even if the body shop did solid work.

- Cashing a check tied to final language. If the payment is framed as final settlement, stop and verify the legal effect before depositing it.

- Letting the adjuster define the categories of damage. They may focus on repairs while excluding other legitimate losses.

The adjuster is not your friend. They are a negotiator for their employer.

Pressure tactics are part of the process

Insurers often create urgency. They may say the offer is fair, standard, or time-sensitive. They may imply that asking questions will just delay payment.

That's not your problem. Accuracy comes before speed.

If you want a second opinion on the broader question of whether to take the first number on the table, Olson & Sons personal injury guidance gives a useful outside perspective on why quick acceptance often benefits the insurer more than the claimant.

A lot of drivers also negotiate poorly because they walk into the conversation without a strategy. If you need a practical framework before pushing back, review this guide on how to negotiate with an insurance adjuster.

What smart pushback looks like

You don't need theatrics. You need documentation and discipline.

State what's missing. Attach support. Counter in writing. Force the adjuster to respond to actual evidence instead of broad statements.

Here's a helpful explainer if you want to hear negotiation points laid out plainly:

A polite claimant who accepts vague math gets paid on vague math.

The insurer's first number is the opening move. Treat it that way.

Your Power to Negotiate Using the Appraisal Clause

Most online advice about an accident settlement form gets stuck on one point: read before you sign. Fine. Of course you should read before you sign.

However, that advice does not solve the core problem in a total loss or diminished value dispute. The underlying issue is that the insurer's valuation may be inaccurate, and an incorrect valuation poisons the whole settlement.

That's where the Appraisal Clause matters.

Why this clause matters so much

This tool is badly underused. Existing online guides often skip it, even though Novian Law's discussion of settlement gaps notes that 68% of total loss claims in markets like Washington and Oregon involve disputes over vehicle value, and insurer software undervalues vehicles by 20% to 30% in that context.

That should tell you two things.

First, valuation fights are common. Second, you're not being unreasonable if the number looks off.

What the Appraisal Clause does

The clause is built into many policies. It provides a structured way to resolve disputes over the amount of loss.

In plain English, it usually works like this:

- You and the insurer disagree on value.

- Each side selects an appraiser.

- If the appraisers disagree, an umpire gets involved.

- A binding value decision can follow from that process.

That matters because it shifts the dispute away from an adjuster leaning on proprietary software and toward actual market analysis.

If you want to understand how this policy mechanism works in more detail, review this explanation of the insurance appraisal clause.

How to use it before signing the accident settlement form

Do this in order.

- Read your policy. Search for “appraisal” or “amount of loss.”

- Put the dispute in writing. Don't rely on phone calls.

- Identify what's wrong with the valuation. Bad comps, missing options, unsupported condition adjustments, wrong trim, ignored local market data.

- Do not sign the release while value is disputed. Once you sign, your negotiating power may disappear.

- Demand a corrected figure or formally invoke appraisal if the policy allows it.

If the settlement offer is built on a bad vehicle value, arguing over the release language alone won't fix the problem. You have to fix the number first.

Why I'm so opinionated about this

Because I've watched too many owners sign away a bad ACV or a missing diminished value claim just because the insurer acted like the software result was neutral. It isn't neutral. Software depends on inputs, comp selection, and adjustment choices. People make those choices, and people can skew them.

The Appraisal Clause is one of the few tools that forces a different process. Use it when the valuation is wrong. It gives you a level of influence that “please reconsider” emails never will.

Finalizing the Settlement and What Happens Next

Once the money is right, the paperwork still matters. Review the final accident settlement form the same way you reviewed the first version. Don't assume the corrected number magically fixed the document.

Make sure the final form reflects the actual agreement. If the dispute involved vehicle value, the release and payment terms should match the updated number exactly. If property damage and injury claims are being handled separately, the document should say that clearly.

Before you sign the final version

Use a short closing checklist:

- Confirm the settlement amount matches the negotiated result

- Confirm the claim being released is only what you intend to release

- Check for changed language inserted in a revised draft

- Keep copies of everything before sending it back

Send the signed form in a way you can document. Certified mail, secure upload portal, or tracked email chain. You want proof of delivery.

After the form goes back

Then you wait for payment processing, lien handling if applicable, and final check issuance. The exact timing varies by claim, but don't go silent. If payment stalls, ask what document or approval is missing and get a written answer.

Also remember this: settlement money can involve tax questions depending on what the payment covers. That's not something to guess about. If you have concerns, ask a tax professional before spending around assumptions.

In a high-volume state like California, the settlement range shows why detail matters. A California settlement value analysis notes that the median car accident settlement is around $295,000, while most non-catastrophic cases settle for $15,000 to $100,000. That spread is exactly why every line item matters. Vehicle value, medical support, wage loss, and release language all affect where you land.

If the insurer delays unreasonably, changes terms after agreement, or refuses to honor policy language, a complaint to your state Department of Insurance may be worth considering. Keep that as a pressure tool, not a first impulse.

You don't need to be a lawyer or appraiser to get this right. You need patience, records, and the discipline not to sign bad paper for bad money.

If your insurer is lowballing a total loss or ignoring diminished value, Total Loss Northwest helps drivers challenge bad valuations with independent appraisals and Appraisal Clause support. If the number on the settlement form doesn't match the actual market value of your vehicle, get the valuation fixed before you sign away your rights.