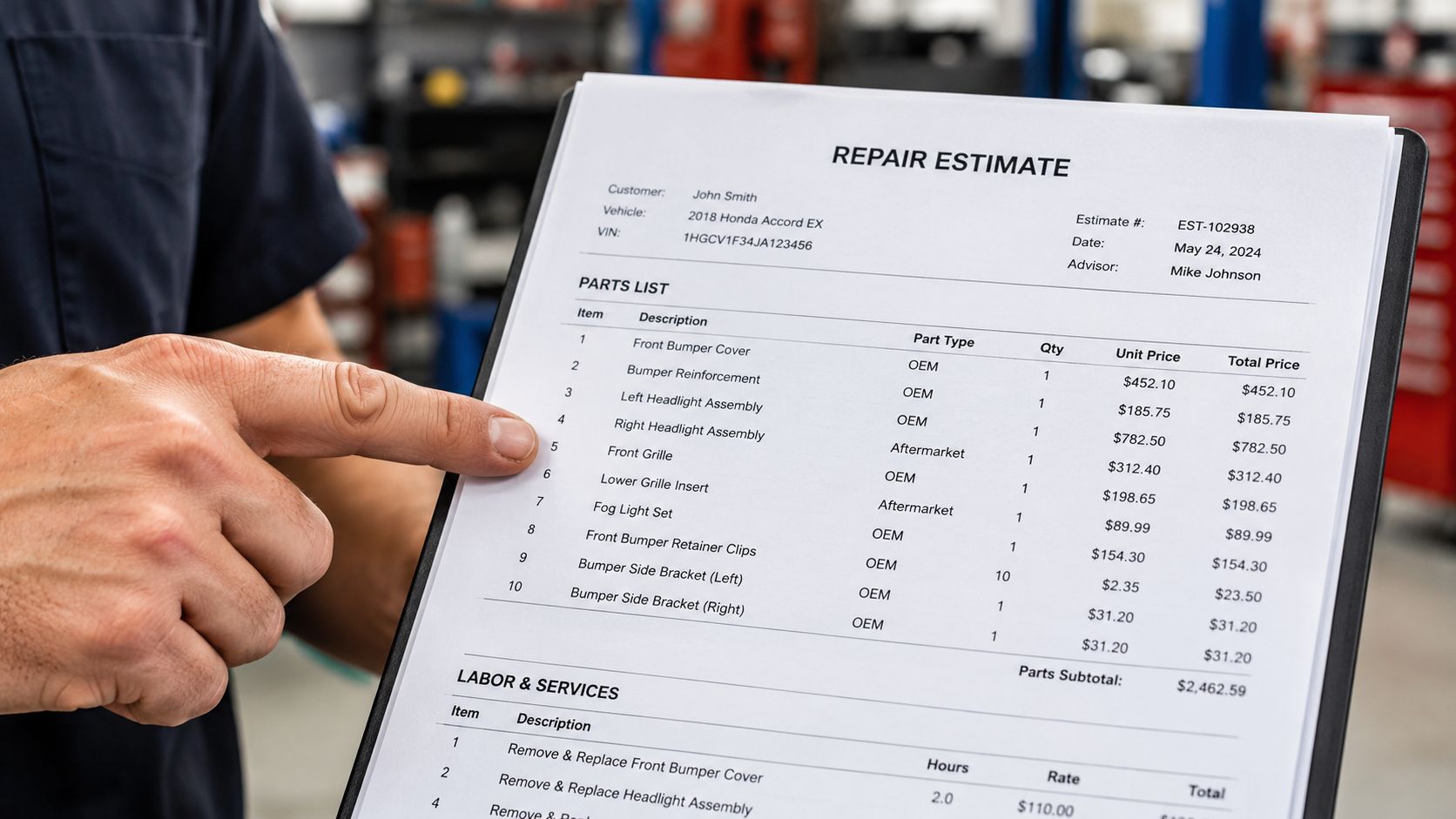

You open the insurance estimate after the accident and start scanning line items. The labor looks confusing enough, then you see parts marked OEM, A/M, and sometimes LKQ. That's the moment most owners realize the crash didn't end when the tow truck left. It changed into a money fight.

The insurer is trying to control repair cost. You're trying to protect the car you owned before someone hit it. Those goals are not the same.

If you're sorting through aftermarket parts vs OEM, don't treat it like a minor paperwork detail. Part choice affects repair quality, safety-system performance, resale value, diminished value, and sometimes whether the insurer repairs the car at all or pushes it toward a total-loss decision. That's why this issue matters far beyond the body shop.

Your Accident Was Just the Beginning

A common scenario goes like this. Your vehicle gets hit. You report the claim, send photos, and wait for the estimate. A few days later, the insurer sends over a repair sheet that looks official enough to discourage questions. Buried in the parts list are replacements that didn't come from your vehicle's manufacturer.

Most owners pause at that point for a good reason. They assumed the insurer would pay to put the car back the way it was. Instead, the estimate often reflects the insurer's preferred cost strategy, not the owner's long-term financial interest.

That's the core conflict in aftermarket parts vs OEM. The insurer sees a repair file. You see a vehicle you may keep for years, trade in later, or defend in a diminished value claim after the repair is done.

Your car doesn't lose less value because the insurer found a cheaper bumper cover.

That estimate can shape more than the repair. If the insurer uses lower-cost non-OEM parts, the total repair bill may look low enough to avoid a total loss. That can leave you driving a heavily damaged vehicle that was repaired to a cheaper standard than you expected. On the back end, if you sell or trade the car, buyers and appraisers won't ignore the accident history or the quality of the repair.

Owners get boxed in. The adjuster says the parts are “comparable.” The shop says it can install what the insurer approves. Meanwhile, no one is focused on your resale position, your ADAS calibration risk, or the advantage you may lose on a future claim.

You need to read the estimate like a valuation problem, not just a repair authorization.

Understanding Your Repair Estimate Parts List

Your estimate decides more than how the car gets repaired. It shapes what the insurer pays now, what the vehicle is worth later, and how hard you may have to fight if the numbers point toward a diminished value claim or a disputed total loss.

Read the parts codes line by line. Insurers and shops use shorthand, and that shorthand carries real financial consequences.

OEM parts

OEM parts come from the vehicle manufacturer or its approved supply chain for that model. On an estimate, this is usually the clearest category because the part is tied to the factory standard your vehicle had before the loss.

That matters for more than fit. If your file later turns into a diminished value dispute, OEM documentation gives you a cleaner record to show an appraiser, a buyer, or an opposing carrier. It is easier to defend the vehicle's pre-loss quality when the replacement parts match the manufacturer's intended specification.

Aftermarket parts

Aftermarket parts come from third-party manufacturers. The label alone does not tell you enough. You need the brand, the supplier, and the exact part designation.

Some aftermarket parts perform acceptably. Some create alignment issues, finish problems, sensor placement concerns, or questions during resale. Insurance companies like them because they lower the repair bill on paper. That lower bill can also affect claim strategy by keeping the estimate below a total loss threshold.

Edmunds explains that repair shops use aftermarket parts for practical reasons such as cost and availability, and some shops view certain products as comparable depending on the application (Edmunds on aftermarket versus manufacturer car parts). Your concern is narrower and more important. You need to know whether the specific part on your estimate protects your vehicle's value.

For a broader industry view on supplier considerations, see making informed parts choices for distributors.

Certified aftermarket and non-certified aftermarket

A certified aftermarket part has met a testing standard set by a certification program. That gives you more support than an unidentified third-party part, but it does not guarantee the same long-term result as OEM on your specific vehicle.

A non-certified aftermarket part deserves extra scrutiny. Ask for the manufacturer name, the certification status, and the written warranty. If the estimate only lists a vague part type, you do not have enough information to approve the repair intelligently.

Recycled or LKQ parts

LKQ means like kind and quality and usually refers to a used OEM part taken from another vehicle. This category can make sense for some components, especially if the donor part is clean, undamaged, and properly documented.

Condition decides everything here. Prior repairs, hidden cracks, corrosion, and wear can turn an apparently cheap replacement into a value problem later. If the insurer proposes LKQ parts, ask about the donor vehicle, mileage, condition grading, and whether the part has been refinished before.

If the claim later turns on whether the vehicle should have been totaled, or whether the valuation software understated your payout, review this breakdown of a CCC auto valuation report.

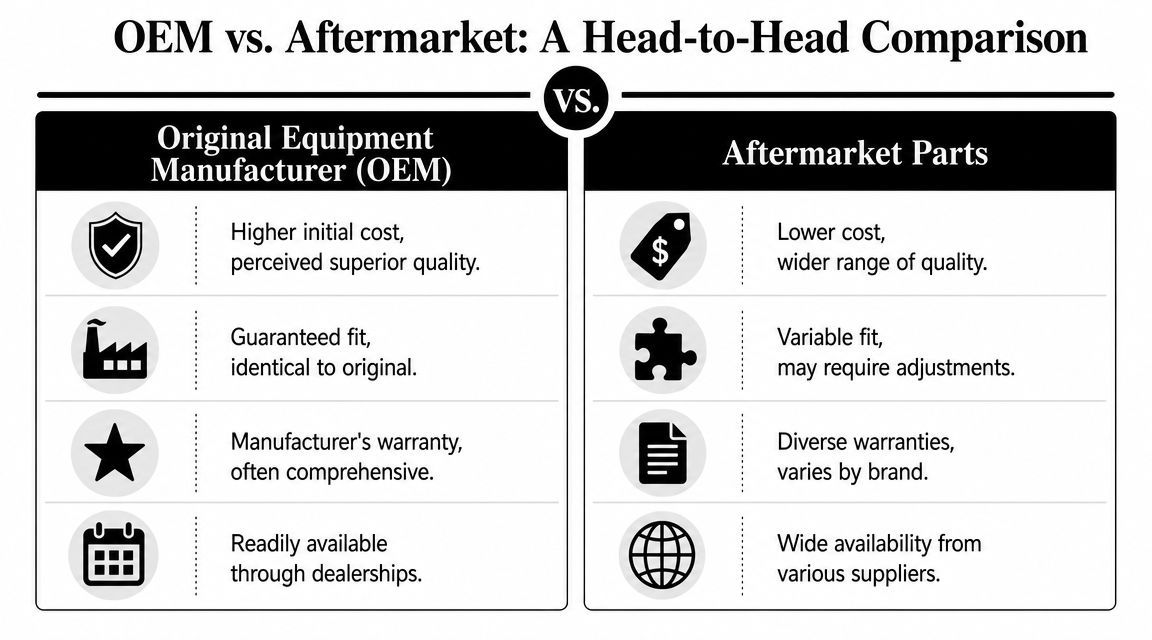

Comparing OEM vs Aftermarket Parts

An insurer saves money the moment your estimate swaps factory parts for cheaper alternatives. You carry the risk if those parts fit poorly, affect calibration, weaken the repair record, or drag down resale value later. That is the right frame for comparing aftermarket parts vs OEM.

| Attribute | OEM Parts | Aftermarket Parts |

|---|---|---|

| Cost | Higher upfront price | Lower upfront price |

| Fit and compatibility | Most predictable match to factory specs | Varies by maker and part tier |

| Quality consistency | More consistent | Wide variation |

| ADAS and calibration risk | Lower risk for compatibility issues | Higher risk if geometry or tolerances differ |

| Warranty | Usually clearer and more straightforward | Depends on brand and supplier |

| Availability | Can be limited by dealer inventory or backorders | Often easier to source from multiple suppliers |

| Impact on owner confidence | Stronger for resale and repair documentation | More likely to raise buyer questions |

Cost

OEM usually costs more upfront. That is why insurers push aftermarket parts so aggressively. Lower part prices reduce the repair estimate, and a lower estimate can help the insurer control the claim.

Your job is to decide whether that lower number protects your vehicle's value. In many cases, it does not.

A cheaper part only saves money if it installs correctly, performs correctly, and does not create extra labor, delays, or a weaker repair file. If it causes fitment problems, return handling, refinishing corrections, or recalibration issues, the early savings disappear fast.

Practical rule: Judge part choice by total claim impact, not the sticker price on one line item.

Quality and fit

OEM parts are built for your vehicle. Aftermarket parts are built to compete on price, availability, or both. That does not make every aftermarket part bad. It does mean quality can swing from excellent to unacceptable depending on the manufacturer and the component.

This matters most on visible panels and parts that must line up precisely. A bumper cover that needs extra shaping, a hood with uneven gaps, or a headlamp assembly that sits slightly off is not a small issue. It changes how the car looks, how the repair is documented, and how a future buyer judges the accident history.

That resale penalty is exactly why owners later pursue an automobile diminished value claim after repairs are finished.

Safety and technology

The financial risk gets worse on modern vehicles with driver-assistance systems. Cameras, radar units, parking sensors, brackets, grilles, windshields, and bumper components all depend on exact placement. A part can bolt on and still be wrong.

Rocco's Collision warns that current vehicles rely on tightly calibrated cameras, radar, and panel geometry, so replacement parts that differ from factory specifications can create safety-system and calibration problems (Rocco's Collision on OEM vs aftermarket safety concerns).

Pay special attention to:

- Front bumpers and grilles that affect radar and sensor positioning

- Windshields used with camera-based safety systems

- Headlamps and tail lamps that require exact mounting and alignment

- Brackets, clips, and trim pieces that control sensor location

If the part affects ADAS, structural performance, visible fit, or airbag-related components, my recommendation is simple. Push for OEM.

Availability, warranty, and real-world claim math

Aftermarket parts often win on availability because more suppliers produce them. Fleetio notes that aftermarket parts generally offer broader sourcing options, while OEM parts tend to provide more predictable compatibility and more consistent quality across the board (Fleetio on aftermarket vs OEM tradeoffs).

That speed advantage matters less than insurers claim. A part that arrives quickly but needs modification, return handling, or repeat labor can become the most expensive line item on the estimate.

Warranty language also deserves scrutiny. OEM warranty terms are usually easier to trace. Aftermarket coverage can depend on the brand, supplier, and installer. If something fails later, that complexity becomes your problem unless the repair shop and insurer put clear commitments in writing.

If you work in repair supply or want a distributor-focused perspective on evaluating these tradeoffs, GFX has a useful piece on making informed parts choices for distributors.

My advice is direct. Use OEM for safety-related parts, structural parts, visible exterior panels, lighting, sensor-related components, and any repair on a newer, high-value, or brand-sensitive vehicle. Aftermarket parts may reduce the insurer's cost today. They can also reduce your vehicle's value when it matters most.

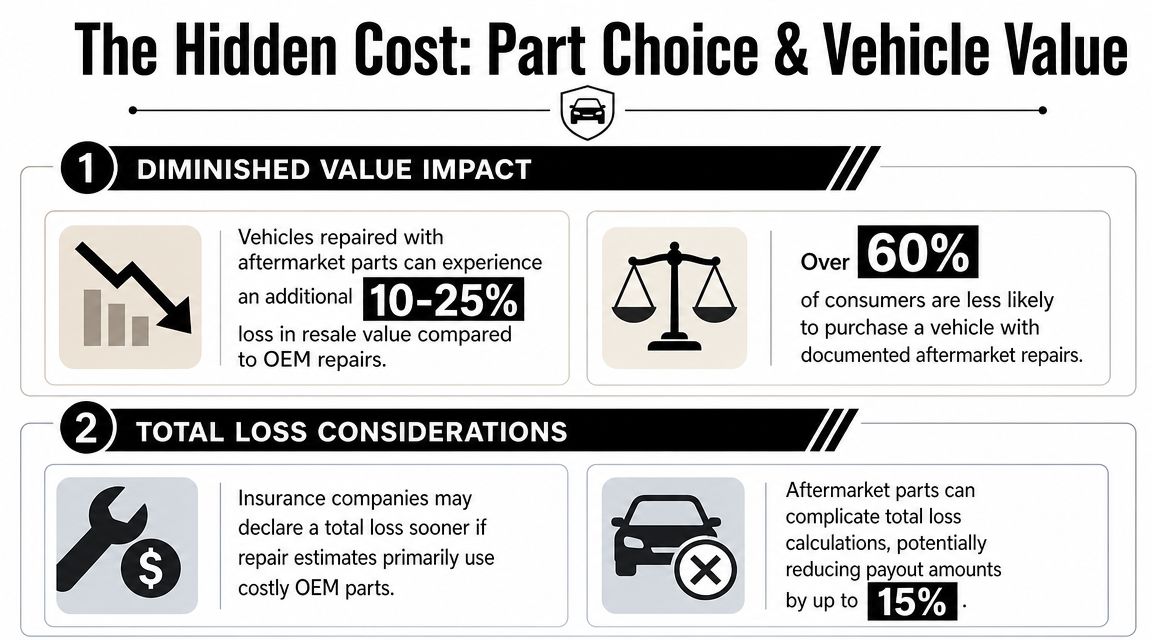

How Part Choice Affects Diminished Value and Total Loss

This is the part most articles miss. The fight over parts isn't just about what gets bolted onto the car. It's about what the car is worth after the claim is over.

Diminished value gets worse when the repair record gets weaker

A vehicle with an accident history already faces a resale penalty. Buyers worry about hidden damage, repair quality, future problems, and safety. If the repair file also shows non-OEM replacement parts, that concern usually gets worse, not better.

That's especially true on newer vehicles, luxury vehicles, collector vehicles, and cars with visible panel work. A buyer may not know every technical detail, but they understand the difference between “repaired with factory parts” and “repaired with aftermarket parts.”

That distinction can support a stronger argument for loss in market value. If you're dealing with that issue, this overview of an automobile diminished value claim explains how owners pursue compensation after an accident repair.

Part choice can influence whether the insurer repairs or totals the vehicle

Insurers compare repair cost against vehicle value. If they can lower the estimate enough, they may avoid a total-loss payout and instead authorize repair. One way they do that is by using cheaper parts.

That means an estimate built around aftermarket components can push the claim in a different direction than an OEM-based estimate would. The owner may end up keeping a severely damaged vehicle because the insurer's version of the repair budget stayed under its threshold.

That's not a small accounting difference. It changes the future of the claim.

Here's what I see owners miss: if the insurer keeps the car repairable by reducing part cost, the owner may inherit the long-term downside. You keep the accident history. You keep the resale hit. You keep the questions from future buyers. You also keep the risk that the finished repair won't carry the same market confidence as a factory-correct rebuild.

ADAS issues create both safety and value problems

As covered earlier, modern vehicles depend on precise sensor and camera integration. This issue becomes even more important in diminished value analysis because a repair that raises doubt about calibration integrity often harms buyer confidence.

A replacement bumper, grille, windshield, or fender can fit physically and still create trouble if the geometry differs enough to affect sensor alignment. That's why part choice can hurt you twice. First in the shop, then in the marketplace.

If a buyer thinks the safety systems may not perform exactly like they did before the crash, the vehicle becomes harder to defend at sale or trade.

From an appraiser's standpoint, that's the hidden cost in aftermarket parts vs OEM. The insurer saves money on the front end. The owner may lose money on the back end.

Navigating Insurance Policies and State Laws

Most policies give the insurer some room to specify non-OEM parts. That doesn't mean the insurer gets unlimited discretion, and it doesn't mean you should accept vague answers.

Read the policy language, not the adjuster's summary

Look for terms like Like Kind and Quality, LKQ, quality replacement parts, or policy endorsements that address OEM coverage. The exact wording matters. Some policies explicitly allow non-OEM parts unless you purchased an OEM endorsement. Others are narrower.

Ask for the insurer's position in writing. Ask them to identify each non-OEM part they intend to use and why they believe it meets policy standards for your vehicle.

If the adjuster gives you a verbal assurance that a part is “equivalent,” that's not enough. You want the part type, manufacturer, source, and warranty details documented.

State rules can change the leverage

Some states require disclosure or consumer notice before non-OEM parts are used. Some impose labeling requirements on estimates. Some have stronger expectations around consent or part identification than owners realize.

That means you need to check your own state's insurance and repair rules, not rely on generic claim-center scripts. If your state gives you notice rights, use them. If your state requires part disclosure, demand it. If your lease, finance agreement, or factory warranty creates OEM-related obligations, raise that immediately.

What to ask for in writing

Use a short paper trail. Don't overcomplicate it.

- Part identification: Ask for the exact designation of every replacement part, including OEM, aftermarket, certified aftermarket, or recycled.

- Supplier information: Request the brand or vendor name for each non-OEM line item.

- Warranty terms: Ask who stands behind the part and what happens if fitment or finish issues appear after delivery.

- Calibration responsibility: Ask who pays if the part creates a need for additional scans, aiming, or recalibration.

- Repair standard: Ask the shop whether it would choose the same part if insurance pricing were not controlling the estimate.

The insurer's estimate is not the final word. It's an opening position.

Owners give up their advantage when they treat the estimate like a finished verdict. It isn't.

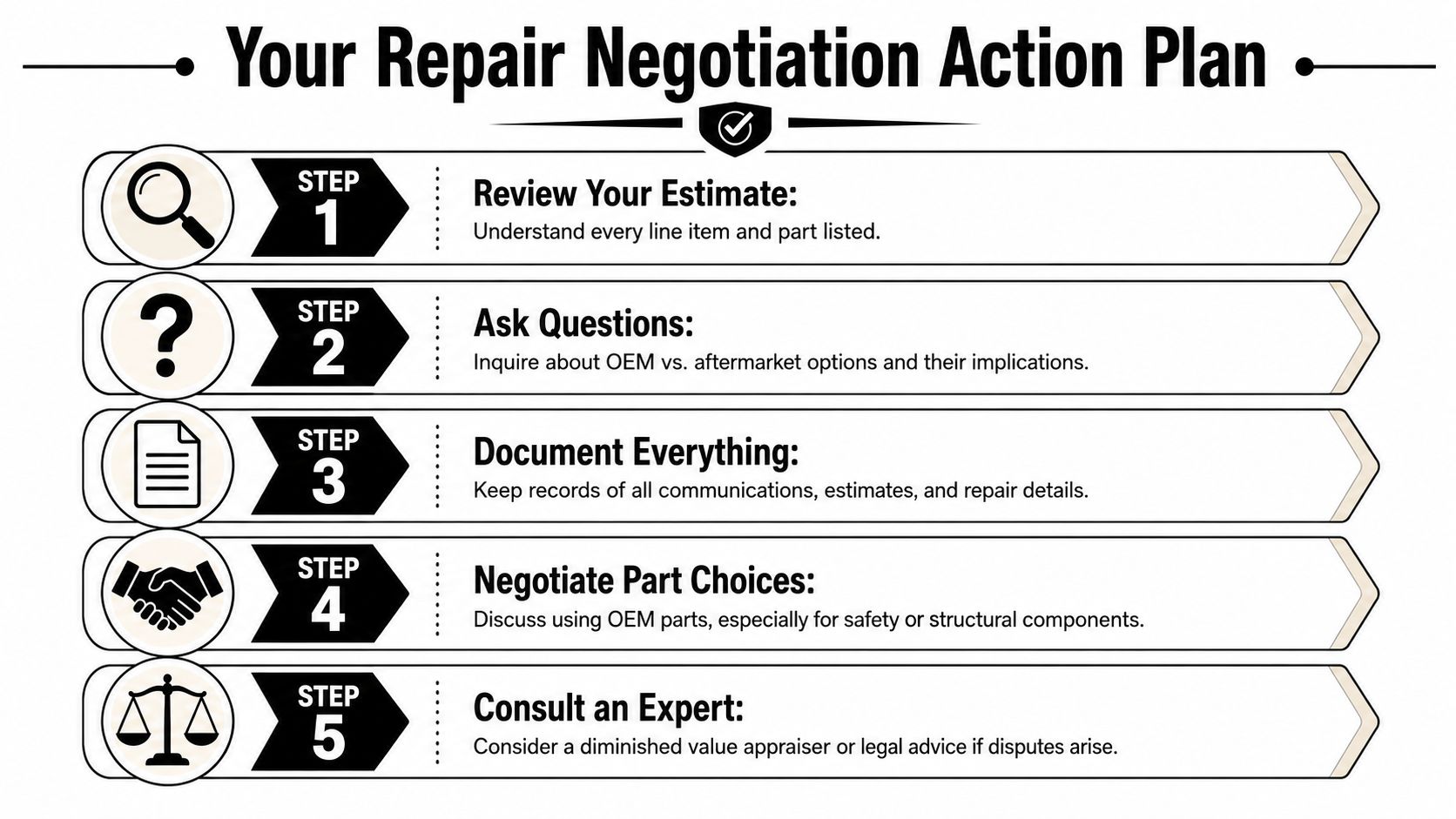

Your Action Plan for Negotiating Repairs

Once you get the estimate, move fast and stay organized. Don't argue in circles. Build a file.

Start with the estimate itself

Read every parts line, not just the total at the bottom.

- Flag abbreviations: Mark OEM, A/M, LKQ, recycled, reconditioned, or remanufactured entries.

- Separate visible from non-visible parts: A clip isn't the same as a bumper reinforcement, headlamp, or radar bracket.

- Highlight safety-related components: Anything tied to impact absorption, steering, lighting, airbags, sensors, cameras, or radar deserves extra scrutiny.

Then question the shop, not just the insurer

A good collision shop will usually tell you where the estimate is weak. Ask direct questions.

What aftermarket brands are listed? Has the shop used them before on your exact model? Did those parts require extra labor to fit? Would the shop personally recommend OEM for any item on the sheet?

You're not asking the shop to pick a fight with the insurer. You're asking the shop to tell you the truth about repair risk.

Keep your pressure points focused

Don't make this a philosophical argument. Tie your objection to the part and the consequence.

Use points like these:

- Factory fit matters for visible panels and trim alignment.

- System calibration matters if the vehicle has ADAS features.

- Warranty concerns matter if the car is newer, leased, or still covered.

- Resale and diminished value matter because the accident already reduced market appeal.

Put everything in writing

Send follow-up emails after calls. Confirm what was said. Save revised estimates. Keep parts invoices if you can get them. Photograph the damaged area before repairs and the repaired area afterward.

If the dispute grows, documentation gives you an advantage. If the insurer reverses course later, your file will show what they initially proposed and why you objected.

One practical option when the claim turns into a valuation dispute is to involve an independent appraiser. For owners in Oregon and Washington, Total Loss Northwest handles diminished value and total loss appraisal work tied to claim disagreements. That's useful when the repair estimate and the vehicle's actual financial loss no longer match.

When to Insist on OEM and Invoke Your Appraisal Clause

Your car is repaired, looks acceptable in the shop parking lot, and the insurer calls the claim resolved. Then you try to sell it, trade it, or settle a diminished value dispute, and the cheaper parts choice shows up in the numbers.

That is when you stop treating OEM as a preference and start treating it as asset protection.

Insist on OEM parts when the vehicle is under factory warranty, leased, high-value, collector-grade, or damaged in an area tied to ADAS hardware, sensor aiming, structural fit, or highly visible panel alignment. Those are the claims where a cheaper part can cost you twice. First at repair. Then again when the vehicle is appraised after the accident.

Insurers frame part choice as a repair-cost issue. Owners should frame it as a value issue. If an aftermarket hood, bumper cover, lamp, bracket, or trim piece affects fit, finish, calibration, or buyer confidence, it can weaken your diminished value position and support a lower total loss figure later. A file that shows OEM was appropriate, but denied, gives you a stronger argument that the insurer protected its payout instead of your vehicle's market value.

If the carrier refuses proper repairs or undervalues the loss, use the contract you already paid for. The appraisal clause lets you bring in an independent appraiser to argue value and loss on evidence, not insurer software. Review how the appraisal clause in auto insurance works and when to invoke it.

Independent appraisal matters most when the dispute is no longer about a single part on an estimate. It is about what the wrong part choice does to resale value, diminished value, or a total loss settlement. That is where owners lose real money.

When the insurer's estimate protects its numbers more than your vehicle, independent appraisal becomes a financial necessity.

That is the answer to aftermarket parts vs OEM. The decision affects safety, repair quality, your position in a claim, and the amount of money you recover.

If your insurer is using aftermarket parts to push down repair costs, reduce your diminished value claim, or avoid a fair total loss settlement, Total Loss Northwest can help you challenge the numbers with an independent appraisal. Their work focuses on real market value, not insurer-friendly assumptions, so you have solid support when the estimate or payout does not reflect what your vehicle lost.