The email usually lands at the worst time. Your car is sitting in a tow yard or body shop. You're already arranging rides, missing work, or arguing with storage fees. Then the insurer sends a number that doesn't match the vehicle you owned, the condition you maintained, or the money you put into it.

That first number is often where people feel trapped. It isn't.

A proper Agreed Value Appraisal gives you a structured way to push back with evidence instead of frustration. If you own a collector car, a modified vehicle, or a high-value daily driver, it can help establish value before a loss ever happens. If you're already in a total loss dispute, the same appraisal discipline becomes the backbone of a stronger claim response.

The Lowball Offer That Changes Everything

It is often evident within seconds when a total loss offer is off.

The adjuster may sound confident. The valuation report may look official. But you look at the number and immediately know they didn't account for the trim package, the condition, the recent work, the custom equipment, or the fact that your vehicle wasn't some average rough example pulled from a generic database.

That moment changes the claim. Up to that point, you may have assumed the process would be mostly administrative. After the low offer arrives, you realize it's a valuation fight.

What usually goes wrong

I've seen the same pattern over and over. The insurer treats a vehicle as interchangeable with weaker comparables. They adjust downward for condition in ways that don't reflect reality. They miss permanent upgrades. They rely on a software-driven valuation that looks polished but leaves out what buyers in the market focus on.

If you're in that position now, one practical rule applies immediately:

Never accept the first number just because it arrived on insurer letterhead.

That's also why resources like DFox Law's guide to insurance offers resonate with so many drivers. The basic point is simple. Early offers are negotiation positions, not sacred valuations.

The appraisal shifts control back to you

An Agreed Value Appraisal is the opposite of guesswork. It documents the vehicle, its condition, its equipment, and the market support behind the value. It gives you something far more useful than “I think my car is worth more.”

It gives you a file that can stand up to review.

That matters because adjusters don't respond to emotion. They respond to documentation, policy language, and credible valuation support. Once you move the discussion from “I disagree” to “Here is the evidence,” the claim changes tone fast.

If your offer feels low, trust that instinct. Then replace frustration with process.

Agreed Value vs ACV vs Stated Value Explained

These three terms get mixed together constantly, and that confusion costs people money. The policy label matters because it affects what happens when the vehicle is stolen or declared a total loss.

The simple way to think about it

It's about pricing a valuable item before it disappears versus arguing about it afterward.

With Agreed Value, the number is negotiated in advance and written into the policy. With Actual Cash Value, the insurer decides the vehicle's value at the time of loss. With Stated Value, the number you listed may not be the amount you receive.

That last part surprises a lot of people.

Practical rule: If you want certainty, don't assume a declared number on a policy automatically means a guaranteed payout.

As this explanation of agreed value vs actual cash value makes clear, post-loss valuation disputes usually happen when the policy leaves room for them.

Vehicle valuation methods at a glance

| Valuation Method | How Value is Determined | Typical Payout on Total Loss | Best For |

|---|---|---|---|

| Agreed Value | Insurer and owner agree on a value before the loss | Generally the full agreed amount on a covered total loss | Collector, custom, rare, and high-value vehicles |

| Actual Cash Value | Insurer determines value at the time of loss, often using depreciation and comparables | What the insurer says the vehicle was worth at the time of loss | Standard daily drivers under ordinary auto policies |

| Stated Value | Owner states a value when coverage is written | May still be the lower of the stated amount or ACV | People who want a higher cap than standard ACV, but not full agreed value certainty |

Where drivers get burned

The critical distinction is this: agreed value is a pre-negotiated amount paid on a covered total loss, while a stated value policy may still allow the insurer to pay the lower of the stated amount or the actual cash value at the time of loss, as explained in The Zebra's guide to agreed value vs stated value.

That means Stated Value often acts more like a ceiling than a promise.

Here's the practical takeaway:

- If your vehicle is ordinary and easy to value, ACV may be workable, though you can still end up arguing over condition and comparables.

- If your vehicle is unusual, ACV is often where problems start.

- If your policy says stated value, read the settlement language carefully.

- If you need a locked number, you're looking for agreed value, not a loose description that sounds similar.

Why an appraisal matters even before a claim

People often ask, “If my car is appraised, doesn't that guarantee the payout?” Not by itself. An appraisal supports the value, but the policy language controls how the claim is paid.

The appraisal is evidence. The policy is the contract.

When those two line up under an agreed value structure, you have clarity before the loss instead of an argument after it.

When You Absolutely Need an Agreed Value Appraisal

Some vehicles are poor candidates for generic valuation from day one. If yours falls into one of these groups, an Agreed Value Appraisal isn't extra paperwork. It's protection.

Collector and classic vehicles

A clean collector car doesn't behave like a commuter sedan in the valuation world. Condition, originality, provenance, options, and market demand matter more than standard depreciation logic.

If you wait until after a loss to explain those details, you're already negotiating from behind.

Custom and modified builds

Standard insurer valuations often fail quickly. A modified truck, overland rig, show car, performance build, or specialty van may contain real value in permanently attached equipment that a generic report won't capture unless someone documents it carefully.

VFIS notes that for specialty vehicles, an appraisal helps establish an agreed value that accounts for the base vehicle plus permanently attached equipment, and insurers may use a repairability threshold of up to 60% of agreed value to determine if the vehicle is a total loss in some cases, which is why accurate appraisal support matters so much (VFIS guidance on assigning an agreed value).

High-value daily drivers

Not every appraisal case involves a weekend-only classic. Some newer vehicles deserve the same level of valuation care because trim, condition, rare packages, low production, or market scarcity make them poor fits for ordinary book-value treatment.

If replacing your exact vehicle would be difficult, that's a warning sign.

Drivers already facing a total loss dispute

If you're in Oregon or Washington and the insurer has already delivered a low total loss number, an appraisal becomes a claim tool even if you didn't set agreed value before the accident.

Look at your situation through these questions:

- Is the insurer ignoring options or equipment you can document?

- Did you maintain the vehicle well compared with the comparables they used?

- Are the comps poor matches on condition, trim, mileage, or configuration?

- Would replacement in your market cost more than the offer suggests?

If you answered yes to any of those, you likely need a professional valuation response, not another phone call repeating the same complaint.

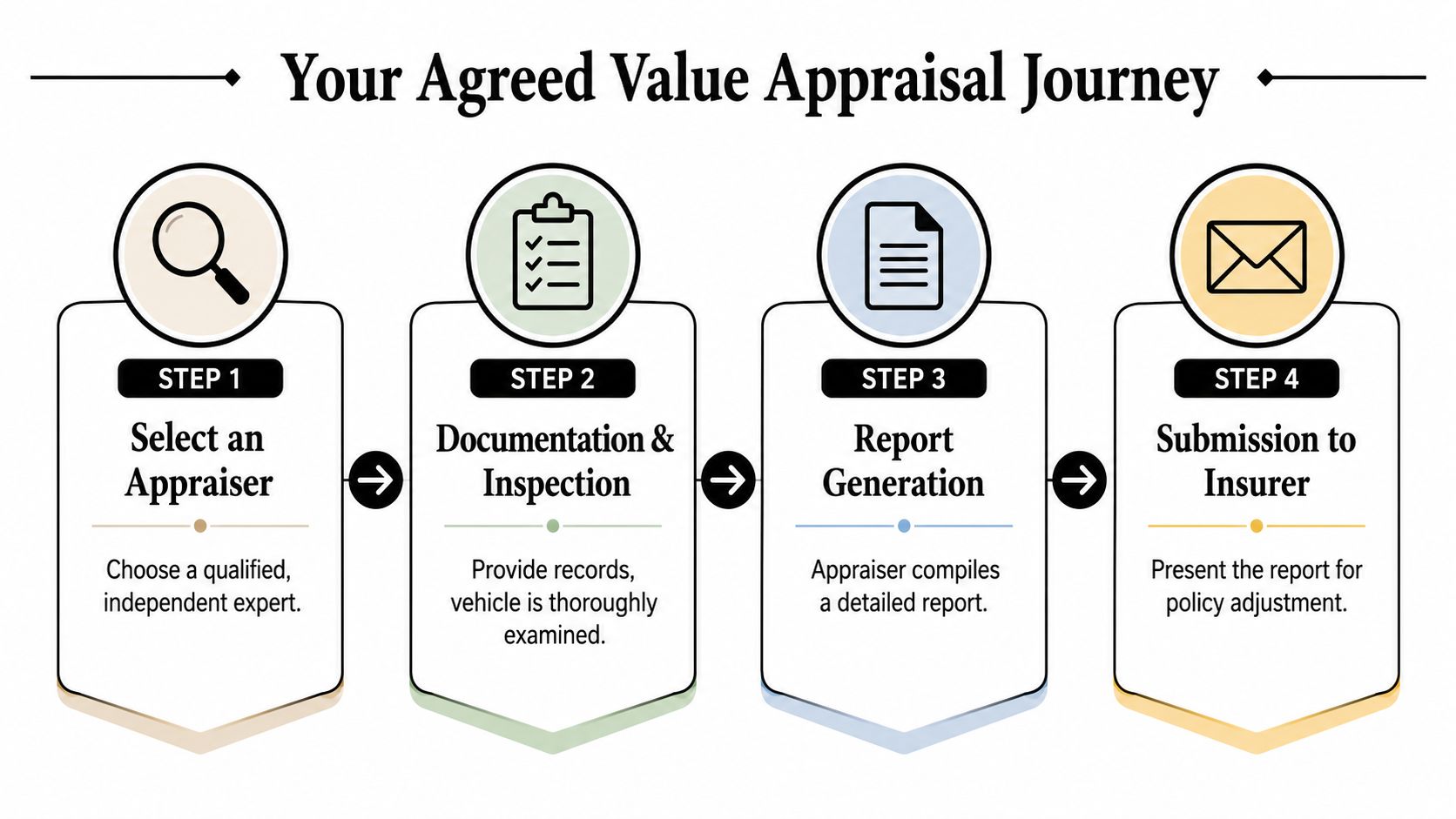

The Professional Appraisal Process Step by Step

Most clients expect the appraisal process to be complicated. It usually isn't. The hard part is not the procedure. The hard part is making sure the right details get captured and supported.

A good overview of what a car appraisal is and why you need one helps frame the process, especially if this is your first valuation dispute.

Step 1 Select the right appraiser

Start with independence and relevant experience. You want an appraiser who understands total loss disputes, policy valuation issues, condition grading, and market-supported vehicle analysis.

Ask direct questions:

- Do you handle disputed insurance valuations

- Do you inspect custom equipment and permanent modifications

- Do you produce reports suitable for appraisal clause disputes

- Do you work with clients in my state and claim context

If the answers are vague, keep looking.

Here's the visual flow most vehicle owners follow:

Step 2 Gather the documents that actually matter

Receipts help, but they aren't the whole file. The strongest appraisals combine ownership records, service history, equipment proof, and photos that show real condition.

Bring together:

- Purchase records if you have them

- Service and maintenance invoices that show care and recency

- Modification receipts for wheels, suspension, audio, engine work, bodywork, storage systems, or specialty equipment

- Photographs showing exterior, interior, engine bay, undercarriage if relevant, odometer, VIN, and closeups of notable features

- Prior listings or build sheets that identify options and packages

Step 3 Inspection and condition analysis

The inspection can be in person or, in some situations, structured remotely. The appraiser isn't just taking pictures. The appraiser is documenting value-bearing facts.

That includes finish quality, panel fit, upholstery condition, wheel and tire quality, glass, trim, mechanical presentation, attached accessories, and signs of exceptional maintenance or neglect.

The strongest report doesn't just say the vehicle is clean. It shows why that conclusion is supportable.

This walkthrough helps many people understand what an appraiser is evaluating in practice:

Step 4 Report generation and submission

Once the evidence is assembled, the appraiser prepares the report. That document should translate the vehicle from “my car” into an insurer-ready valuation file.

If you're using the appraisal to set coverage before a loss, the report goes to the carrier or agent for underwriting review. If you're in a dispute after a loss, the report becomes part of your challenge to the insurer's number.

That's where precision matters. A weak report is an opinion. A strong report is a position.

Using Your Appraisal to Win Your Insurance Claim

A professional appraisal only helps if you use it correctly. Sending it as an attachment with a short email saying “please reconsider” usually isn't enough.

The report works best when it's tied to the contractual tools already inside the policy. One of the most important is the insurance appraisal clause process, which can move a valuation dispute out of the adjuster's hands and into a more structured process.

Why the contract matters

Agreed value has weight because it is fundamentally contractual. In commercial property, agreed value became a formalized insurance mechanism in policy language after ISO simplification in 1986, shifting the process to a declarations-page selection plus a Statement of Values filing, and if that annual update is missed the policy can revert to coinsurance, as outlined in Independent Agent's explanation of the agreed value option.

That commercial history matters even if you're dealing with a vehicle claim. It shows what agreed value is really designed to do. Replace uncertainty at loss time with a documented pre-loss agreement.

What a strong appraisal changes in a dispute

When the insurer relies on black-box valuation software, your appraisal introduces facts the software may have flattened or ignored:

- Vehicle-specific condition

- Permanent equipment and modifications

- Better-matched comparables

- Local market realities

- Evidence tied to the exact unit, not an average example

At that point, the adjuster is no longer dealing with a complaint. They're dealing with contradictory valuation evidence.

How to use the report strategically

If you're disputing a total loss offer, take these steps:

- Read the valuation report carefully. Identify missed options, bad comparables, unsupported condition adjustments, and factual errors.

- Submit the appraisal with a focused dispute letter. Keep it factual and tie each disagreement to evidence.

- Request policy-based review. If the policy allows appraisal, use that procedure rather than getting stuck in endless calls.

- Stay organized. Every communication, report, photo set, and correction should be saved in one claim file.

One option in Oregon and Washington is Total Loss Northwest, which provides certified independent auto appraisals for total loss disputes and appraisal clause cases. Whether you use that firm or another qualified appraiser, the point is the same. Use an independent report that can survive scrutiny.

Anatomy of a Bulletproof Appraisal Report

Clients often ask what they should expect to receive at the end of the process. The answer should never be “just a number.”

A credible appraisal report is a layered document. Each section does a job. Together, they show how the value was reached and why that conclusion is defensible.

The front section

The opening pages should identify the vehicle clearly and eliminate ambiguity. That usually includes VIN, year, make, model, trim, odometer reading, and the effective date of value.

This section should also state the final concluded value in plain language. No one should have to hunt for the answer.

The factual core

The report proves its worth. The appraiser lays out what the vehicle is, what condition it's in, and what features materially affect value.

Look for:

- Detailed equipment identification including factory options and permanent additions

- Condition commentary supported by photos, not empty adjectives

- Ownership and maintenance context when it affects value perception

- Damage status or pre-loss condition discussion if the report relates to a claim dispute

A report becomes persuasive when every conclusion can be traced back to something visible, documented, or market-supported.

The market support section

This is the part insurers pay close attention to. The report should explain how comparable vehicles were selected and why those comparables are comparable.

A solid market section usually includes:

| Report Element | Why It Matters |

|---|---|

| Comparable vehicles | Shows what similar units are asking or trading for |

| Adjustment logic | Explains differences in condition, equipment, or configuration |

| Photo exhibits | Helps validate the appraiser's condition conclusions |

| Certification and signature | Shows accountability and professional authorship |

Weak reports tend to dump a few listings into a PDF and call it done. Strong reports explain the reasoning.

What professional language looks like

A bulletproof report sounds measured. It doesn't oversell. It documents.

You'll often see language like this:

“The subject vehicle presents in above-average condition for its type and configuration, with documented equipment and condition characteristics not reflected in the insurer's comparable set.”

That kind of wording matters because it stays disciplined. It doesn't rant. It builds a case.

Your Agreed Value Appraisal Questions Answered

Individuals typically hesitate for practical reasons, not conceptual ones. They want to know whether the appraisal is worth it, how long it takes, and what happens if the insurer keeps pushing back.

What does an agreed value appraisal cost

Costs vary by vehicle, report scope, and whether the appraisal is for underwriting, a total loss dispute, or an appraisal clause matter. The better way to think about cost is relative to exposure.

In commercial property, one published New York example says a $3 million Brooklyn office building might pay an additional $1,800 to $5,400 per year for agreed value coverage while a major claim could otherwise produce coinsurance penalties exceeding $100,000, which illustrates the general principle that certainty often costs far less than the risk it removes (The Coyle Group's discussion of agreed value in commercial property).

The vehicle takeaway is qualitative but important. If the insurer is low on value, the money left on the table can dwarf the cost of competent appraisal work.

How long does it take

That depends on how quickly you can provide records, photos, receipts, and access to the vehicle. Straightforward files move faster. Complicated claims take longer because the support has to be stronger.

If you're already in a total loss claim, don't wait to start. Storage pressure and claim deadlines rarely help your negotiating position.

Can't I just use online price guides

For ordinary vehicles in ordinary condition, guides can provide a rough starting point. They are not a substitute for a professional appraisal when the vehicle is unique, modified, unusually clean, rare, or being undervalued in a live insurance dispute.

Price guides don't inspect your vehicle. They don't weigh your specific equipment. They don't explain why a bad comparable should be rejected.

What if the insurer ignores the appraisal

That happens. An appraisal report does not force cooperation by itself. What it does is give you evidence to support escalation through the policy's dispute process.

If the carrier won't engage fairly, the next move is usually procedural, not emotional. Review the policy, preserve your documentation, and move toward formal valuation resolution if available.

If you've been hit with a low total loss offer, or you want to set value correctly before a claim ever happens, Total Loss Northwest handles independent auto appraisals for drivers in Oregon and Washington dealing with total loss and appraisal clause disputes. The work is straightforward: document the vehicle, build the valuation file, and give the insurer something they have to answer with facts.