You open the claim email, see the insurer's number, and your stomach drops. They've valued your car like it was average before the crash, average after the crash, and easily replaceable in a market that doesn't feel average at all. That reaction is common in Chicago, especially when the car was clean, well-kept, recently serviced, or harder to match than the adjuster's report suggests.

Most disputes land in one of two buckets. Total loss means the insurer says the car is not economical to repair and offers an actual cash value settlement. Diminished value means the car was repaired, but its accident history still hurts resale value. In both situations, the insurer usually starts with its own valuation process, and that first number often drives the whole conversation unless you push back with better evidence.

A good independent appraisal changes the posture of the claim. It gives you a report built around your vehicle's actual condition, equipment, service history, local market reality, and loss details. That's not just paperwork. It's a powerful tool.

If the accident has also tightened your monthly finances, it helps to look at broader protection options before the next surprise bill lands. Some drivers also review tools like get Nomu loan protection so one setback doesn't cascade into a larger financial problem.

Your Guide to Contesting a Low Insurance Offer in Chicago

The insurance company wants the claim to move fast. You need it to move correctly. Those aren't always the same thing.

When Chicago drivers search for an appraiser in Chicago, IL, they often get directories, generic listings, or pages that define appraisal without explaining how to fight a weak offer. That overlooks the core concern. You're not shopping for a random opinion. You're building a file that can stand up to an adjuster, a desk review, and, if necessary, the policy's formal dispute process.

The two fights that matter

Total loss disputes usually come down to whether the insurer used the right comparables, recognized the right trim and options, and gave proper weight to condition before the crash. If they missed prior maintenance, recent tires, premium packages, or the fact that your vehicle was cleaner than the average comp, the number can come in low.

Diminished value disputes are different. The repair may be complete, but the vehicle still carries an accident history. Buyers and dealers care about that. A proper diminished value appraisal explains the post-repair loss in market value with reasoning that's stronger than “it was in an accident, so it must be worth less.”

You do not have to accept the first number just because it arrived on official letterhead.

Where leverage comes from

An independent appraisal works best when you use it as part of a process, not as a last-minute complaint. That process usually looks like this:

- Identify the claim type: total loss or diminished value.

- Collect the file: insurer valuation, estimate, photos, repair records, policy language.

- Hire an independent appraiser: someone who works for you, not the carrier.

- Review the appraisal carefully: understand the comps, adjustments, and final conclusion.

- Submit a focused challenge: use evidence, not outrage.

- Invoke the appraisal clause if needed: move the dispute into the formal lane your policy provides.

That last step matters more than is often realized. Casual arguments get ignored. Contract-based disputes get attention.

How to Find a Qualified Independent Vehicle Appraiser

The insurer may call its valuation “independent.” That word gets stretched a lot in claims. What you need is an appraiser whose job is to assess your vehicle, not defend the carrier's first number.

Start with independence, not branding

A polished website doesn't tell you much. An insurance-friendly vendor can still look impressive online. The better filter is conflict. Ask a simple question: Who usually pays this appraiser? If a large share of their work comes from insurers, fleets, salvage channels, or parties who benefit from lower values, that matters.

For Chicago-area valuation work in real estate, FHFA data showed undervaluation disparities by neighborhood composition. Tracts with 0 to 50% White population had an undervaluation rate of 8.5%, while tracts with 80.1 to 100% minority population were undervalued at 16.9%, a ratio of 1.99, according to FHFA's UAD Aggregate Statistics analysis. That dataset is about real estate, not vehicles, but the lesson carries over cleanly. Valuation systems are not neutral just because they are standardized. Bias can be built into process, comp selection, or assumptions.

What to ask before hiring

Don't ask, “Can you do an appraisal?” Ask questions that expose whether they know insurance disputes in Illinois.

- Ask about claim type: “Do you handle both diminished value and total loss disputes, or mostly one?”

- Ask about report depth: “Will your report show comparable vehicles, adjustments, and your valuation method?”

- Ask about dispute support: “If the adjuster challenges the report, do you explain your findings in writing?”

- Ask about local market familiarity: “How do you account for Chicago-area availability, trim mix, and condition differences?”

- Ask about policy process: “Have you worked with appraisal clause disputes?”

A strong appraiser will answer directly. A weak one will stay vague, talk around methodology, or promise outcomes instead of process.

Where to look beyond a basic search

A plain search for “appraiser Chicago IL” will surface broad results, but you should also compare specialists who focus on claim disputes and independent valuation. One practical reference point is this guide to an independent auto appraiser near me, which helps frame what genuine independence should look like in an insurance setting.

You can also ask candidate appraisers for sample redacted reports. Not marketing samples. Real report structure. You want to see whether they document condition, options, market comps, and reasoning in a way an adjuster can't dismiss as hand-waving.

If the appraiser can't explain how they reached the number, the insurer won't have much trouble ignoring it.

Red flags that should end the call

Some warning signs are subtle, some aren't.

- Contingency-style language: If they sound paid by the size of the increase, be careful.

- No written methodology: A final number without support won't carry much weight.

- No distinction between claim types: Total loss and diminished value are not the same assignment.

- No willingness to defend the report: The real work often starts after delivery.

- Sales-first pitch: If the whole call is about speed and “winning,” not evidence, keep looking.

Verifying Credentials and Understanding Appraisal Costs

Once you have a short list, slow down. People often get burned during this stage. They hire the first person who sounds confident, then discover the report is too thin, too generic, or too compromised to help.

What to verify before you sign anything

Credentials matter, but only if they connect to the work being done. For a vehicle appraisal dispute, ask about hands-on automotive background, inspection experience, valuation experience, and dispute support. If someone mentions I-CAR or ASE-related training, ask what that means in practice. Can they identify prior repair quality, condition issues, equipment differences, and market-impacting details from inspection and records?

Also ask whether they do regular work for insurers. Independence isn't a slogan. It's a business model. If an appraiser relies heavily on insurance company assignments, that doesn't automatically disqualify them, but it does raise a fair question about whether they can aggressively challenge insurer valuations.

A useful side note is understanding how the insurance side itself gets trained. If you're curious how industry licensing works, getting your Illinois insurance license gives a practical look at the regulated side of the business. It won't teach you vehicle valuation, but it does help you understand that claims handling is procedural and rule-bound. That's why your challenge needs to be documented, not emotional.

Fee structures and what usually works best

You'll run into a few pricing models. Not all of them are healthy.

| Fee model | What it means for you |

|---|---|

| Flat fee | Usually the cleanest option. You know the cost upfront, and the appraiser's pay doesn't rise with the value conclusion. |

| Hourly fee | Can work for unusual files, but ask for a scope estimate so the bill doesn't drift. |

| Percentage-based fee | Creates conflict. The appraiser has a financial reason to push the number higher. That can hurt credibility. |

For most claim disputes, a flat fee is easier to defend because it avoids the appearance that the conclusion was purchased. If you want a sense of the common pricing questions consumers ask, this overview of car appraisal cost is a useful baseline.

Ask for the engagement terms in writing

Before you pay, get clear answers on these points:

- What's included: inspection, report, comp research, revision if the insurer spots a factual error.

- What's not included: court testimony, umpire work, extended negotiation.

- Delivery timeline: when you should expect the report.

- Ownership of the report: whether you can submit it directly to the insurer.

- Scope of support: whether the appraiser responds to adjuster objections.

Practical rule: You're not buying a number. You're buying a defensible opinion that can survive pushback.

Preparing Your Vehicle and Documentation for Appraisal

This part decides whether the appraiser gets a clean shot at the truth or has to fill gaps with assumptions. Gaps help the insurer. Documentation helps you.

For Chicago-area home valuation, Chicago Home Partner notes that appraisals usually take 7 to 14 days after order, rely heavily on the Sales Comparison Approach for many properties, and put weight on details beyond square footage, including permits, parking, outdoor space, HOA assessments, and effective age in its Chicago appraisal overview. The same logic applies to vehicles. A serious appraiser doesn't value your car by year, make, model, and mileage alone. Service history, trim, factory packages, condition, and documented upgrades can change the conclusion.

What to gather before the inspection

Think like you're building a case file.

| Document/Item | Why It's Important |

|---|---|

| Insurance valuation report | Shows what the carrier relied on, including weak comps or missing options. |

| Declaration page and relevant policy language | Helps identify dispute rights and appraisal clause wording. |

| Repair estimate or total loss paperwork | Gives the appraiser the loss context and insurer position. |

| Photos of the vehicle before the accident | Proves pre-loss condition and cleanliness. |

| Photos after the accident | Documents the severity and location of damage. |

| Maintenance records | Supports above-average care and mechanical condition. |

| Receipts for tires, brakes, battery, or recent major service | Shows recent investment that can affect pre-loss value. |

| Window sticker, build sheet, or option list | Confirms trim level and equipment packages. |

| Purchase documents | Helpful for identifying exact configuration and prior representations. |

| Police report, if relevant | Useful for file completeness, especially where loss circumstances matter. |

| Repair invoices for diminished value claims | Shows what was repaired and whether structural work occurred. |

| Loan or lease payoff information | Doesn't determine value, but helps you understand settlement pressure points. |

How to prepare the car itself

You're not staging the vehicle. You're making it readable.

- Clean the interior and exterior: Dirt hides condition. A clean car lets the appraiser see wear patterns, trim quality, upholstery shape, and paint condition.

- Remove clutter: Personal items make inspection harder and photos worse.

- Gather all keys and remotes: Missing keys can matter. So can the presence of original accessories.

- Have the car accessible in daylight if possible: Better visibility means better documentation.

- Don't rush the walkthrough: If the appraiser asks about service, upgrades, or prior condition, answer precisely.

Small details that often change value

Owners miss these all the time because they don't seem dramatic enough.

A premium wheel package. A hard-to-find trim. Dealer-installed accessories with receipts. A spotless interior on an older vehicle. A recent transmission service. New tires. A clean dashboard with no warning lights before the loss. Those are the details a weak valuation skips and a strong appraisal documents.

The insurer's software looks for patterns. Your appraiser looks for differences. Claims are won in the differences.

If your car was especially clean before the loss, say so and prove it. If it had prior cosmetic flaws, disclose them. Honest files are stronger than inflated ones. A good appraiser can work with imperfection. They can't work well with missing facts.

How to Read and Understand the Appraisal Report

The report matters only if you can use it. Many owners get a multi-page PDF, glance at the final number, and miss the real ammunition inside it.

The first pages tell you what kind of report you bought

Start with the assignment definition. The report should say whether it is valuing actual cash value before loss, post-repair diminished value, or another valuation problem. If that part is fuzzy, the whole report gets harder to deploy.

Then look for the method used. Most strong vehicle appraisals rely on a sales-comparison style analysis. That means the appraiser identifies comparable vehicles in the market, then adjusts for meaningful differences.

“Comparable” never means “same year, close enough.” It means similar vehicle, similar market context, and explained adjustments.

The core pieces to review line by line

A professional report usually includes these building blocks:

- Vehicle identification: VIN, trim, drivetrain, mileage, options, and relevant equipment.

- Condition analysis: interior, exterior, mechanical, prior repairs, and overall pre-loss state.

- Market comparables: vehicles used to estimate value.

- Adjustments: mileage, condition, packages, region, history, and other differences.

- Value conclusion: the final number, plus the reasoning behind it.

Peer-reviewed research in commercial real estate found average absolute valuation errors of 8.6% for apartments and 12.5% for industrial sites in this study on appraisal accuracy. The study also found appraisals can lag market direction. Different asset class, same practical lesson: valuation tools are not exact, and unsupported automated outputs can miss real-world market movement. Your independent report is valuable because it shows the reasoning, not just the conclusion.

What to compare against the insurer's paperwork

Set the insurer's valuation beside your independent appraisal and look for these mismatches:

| Report element | What to check |

|---|---|

| Trim and options | Did the insurer miss premium packages, drivetrain, tech, wheels, or tow equipment? |

| Mileage | Did they use the right odometer reading and adjust it reasonably? |

| Condition | Did they treat your well-kept vehicle like an average-condition unit? |

| Comparable vehicles | Are their comps actually similar, or just loosely related listings? |

| Geographic relevance | Did they use vehicles from a market that doesn't reflect your area? |

| Condition deductions | Are any deductions unsupported or duplicated? |

Phrases that matter when you talk to the adjuster

Use the report's language, not your frustration.

Key point: “My independent appraisal identifies comparable vehicles and explains specific adjustments that weren't reflected in the insurer's valuation.”

“The dispute is not just about the final number. It's about the comp selection, condition rating, and unsupported deductions.”

Those statements keep the conversation where it belongs. On evidence.

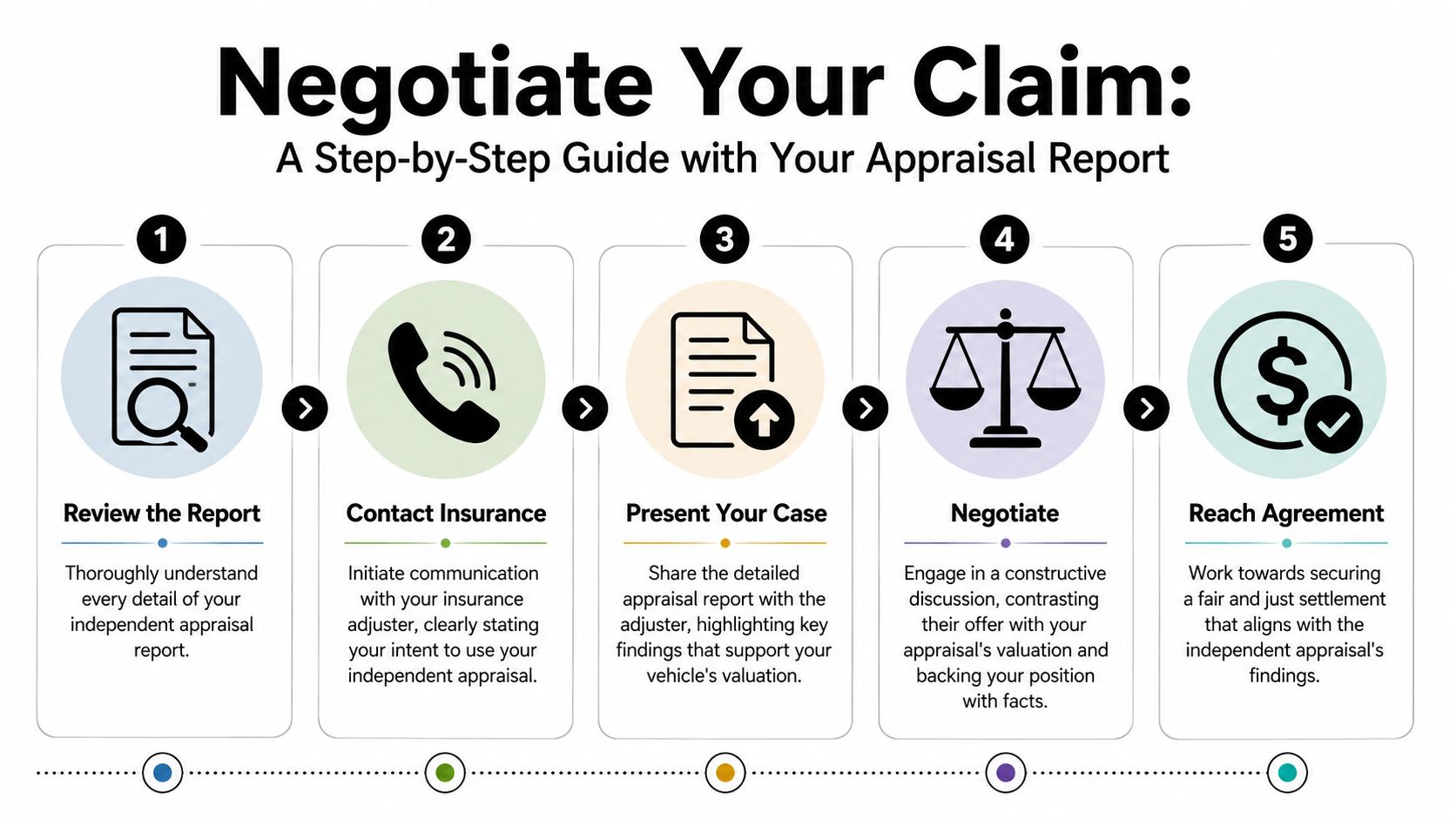

Using Your Report to Negotiate a Fair Settlement

The mistake most owners make is sending the report with a short note that says, “Please review.” That invites delay. You need a cleaner, firmer move.

Move the dispute from informal to formal

In real estate lending, Illinois REALTORS explains that when there's a low appraisal dispute, the client can request a Reconsideration of Value, usually through the lender, and that parties must stay within compliance rules in its appraisal FAQ. Auto insurance has its own version of that logic. The appraisal clause is the formal mechanism in many policies that forces the dispute into a defined process instead of a circular argument with the adjuster.

That's the key point. Not anger. Not repeated phone calls. Contract language.

A practical submission sequence

Use a short, businesslike approach.

Send the report and identify the dispute clearly

State that you disagree with the insurer's valuation and are submitting an independent appraisal that documents the vehicle's market value.Point to specific defects in the carrier's number

Mention the wrong trim, missing options, weak comparables, unsupported condition deductions, or overlooked pre-loss condition.Request written reconsideration

Ask for a written response that addresses the independent report's findings.Set a reasonable deadline for reply

Not a threat. Just a timeline.Invoke the appraisal clause if the response is inadequate

This changes the file from routine handling to a contractual dispute track.

One option drivers sometimes use for this kind of work is Total Loss Northwest, which focuses on diminished value and total loss appraisal disputes and explains how independent reports are used in negotiations.

Sample language you can adapt

Keep it plain.

I dispute the valuation issued on my claim. I have obtained an independent appraisal that identifies comparable market vehicles, condition differences, and valuation adjustments not reflected in your report. Please review the enclosed appraisal and respond in writing. If we cannot resolve this valuation dispute based on the evidence, I request that we proceed under the appraisal clause of the policy.

That wording does three things. It states disagreement, supplies evidence, and signals you know the next procedural step.

What usually doesn't work

These moves feel satisfying, but they rarely help:

- Arguing only from replacement cost: what you found online today isn't enough by itself.

- Sending emotional emails: anger makes it easier for the adjuster to dismiss you.

- Talking in generalities: “My car was nicer” is weak without records and photos.

- Threatening legal action too early: that often freezes productive discussion before you've used the contractual tools available.

What tends to work better

Be direct, specific, and repetitive in the right way. Keep pointing back to the report's comp selection, condition analysis, and documented support. If the adjuster won't engage with the substance, that's often your signal to stop debating and invoke the clause.

If you're dealing with a low total loss or diminished value offer and need an independent opinion built for an insurance dispute, Total Loss Northwest provides vehicle appraisal support focused on documented market value, detailed reports, and appraisal-clause-based claims handling.