You're probably here because the insurance company has already given you a number, an online calculator gave you another number, and neither one feels grounded in the true loss you're dealing with. Your car may be in the body shop, already declared a total loss, or repaired but now carrying an accident history that drags down its resale value.

That confusion is exactly where most drivers get trapped. A typical auto accident settlement calculator can be useful for a rough personal injury estimate. It is not built to tell you what your vehicle claim is worth. That gap matters most in Oregon and Washington, where total loss disputes and diminished value fights often turn on local market data, not generic formulas.

What Is an Auto Accident Settlement Calculator

An auto accident settlement calculator is usually an online tool that asks for basic inputs such as medical bills, lost wages, and sometimes property damage. It then applies a formula to estimate what a claim might settle for. These tools became common in the early 2000s, and their limits are well documented. One review notes that insurers' offers are often 25% low, and calculators frequently undervalue total loss claims by $2,000 to $10,000 according to Express Legal Funding's settlement calculator analysis.

That tells you what these tools are. Just as important is what they are not.

They are not valuation reports. They are not market appraisals. They are not a substitute for evidence when the insurer's number is wrong. If your claim involves a total loss, a repair-related loss in market value, or a vehicle with unusual market demand, the calculator is working outside its lane.

What these calculators usually do well

They can help with a rough first-pass estimate of an injury claim when you want to organize the obvious categories of loss:

- Medical expenses: bills tied to treatment after the crash

- Lost wages: income missed while recovering

- Basic property damage: a broad placeholder, not a detailed valuation

For a general injury overview, a practical resource like this Hawaii car accident settlement guide can help you understand how settlement components are commonly framed.

Where they break down fast

Key blind spots show up on the vehicle side of the claim:

| Claim issue | What the online calculator does | What it misses |

|---|---|---|

| Total loss | Uses broad assumptions | Local comparable vehicles, trim, condition, options, market demand |

| Repaired vehicle | Usually ignores it | Diminished value from accident history |

| Specialty or high-value vehicle | Treats it like an average car | Collector demand, custom features, regional scarcity |

A calculator can give you a number. It can't tell you whether the insurer used weak comparable vehicles, ignored your car's condition, or skipped a recoverable vehicle loss entirely.

If the insurer has focused your attention on pain and suffering while sliding past the vehicle valuation, that isn't accidental. It's a common way valid property-related losses get buried.

How Settlement Calculators Estimate Your Claim

A driver gets rear-ended in Portland, misses work for a week, racks up urgent care bills, and opens an online calculator expecting a usable settlement range. The tool asks for medical costs, lost income, and how badly the injury affected daily life. It gives a number that looks orderly and confident. That number is usually built from a blunt injury formula, not a full claim valuation.

Most public calculators use the multiplier method. They total your documented economic damages and apply a factor, often between 1.5 and 5, to estimate pain and suffering, as outlined in Gunter Injury Law's overview of the multiplier method.

The two buckets that drive the estimate

The first bucket is economic damages. These are the losses you can usually prove with records. Medical bills, wage loss, and sometimes a broad property-damage figure get entered here.

The second bucket is non-economic damages. That covers pain, physical limitations, disruption to routine, and similar harm that does not come with a fixed invoice.

How the formula works in practice

Most calculators follow the same sequence:

- Add up economic losses

- Assign a severity multiplier

- Apply that multiplier to estimate non-economic damages

- Combine the numbers into a settlement range

That structure is why these tools feel credible. A claim that is messy in real life gets reduced to a few entries and one multiplier choice.

Typical examples tied to this method put soft-tissue injuries in a lower settlement band and fractures in a higher one, depending on treatment history, documentation, and how the calculator scores severity. If you want to compare how injury-focused tools present that logic, this guide to calculate your injury claim shows the same consumer-facing approach.

Where the estimate starts to drift from the real claim

The formula is simple. The judgment calls behind it are not.

A multiplier changes based on the records entered, the way symptoms are described, gaps in treatment, fault arguments, and the adjuster's view of how convincing the file looks. Two people with similar crashes can get very different outputs because the calculator is only as good as the assumptions behind it.

That matters in the Pacific Northwest because many claims have a vehicle-value fight sitting beside the injury claim. Online calculators usually treat property damage as one line item. They do not examine whether the insurer lowballed the total loss, used weak comparable vehicles, ignored options and condition, or left out a post-repair market loss. If the dispute is really about vehicle value, start with how carriers calculate actual cash value in auto insurance claims. That is where underpayment often starts.

Practical rule: Use a calculator to get a rough injury range. Do not use it to decide whether a total loss offer or repaired-vehicle payout is fair.

The Problem with Insurer-Biased Calculators

The public-facing calculator is only half the story. Inside the insurance company, adjusters often rely on proprietary systems that look objective from the outside but are built to standardize payouts in the carrier's favor.

One of the best-known examples is Colossus. According to Michigan Auto Law's review of Colossus, it's used by over 80% of U.S. insurers, processes 750 injury codes and 10,720 rules, and evidence indicates it can undervalue claims by 30% to 40% compared to jury awards.

Why the insurer's software number is not neutral

This software doesn't sit down and ask, “What is fair?” It asks, “What does the ruleset allow based on the data entered?”

That distinction matters. If the input is incomplete, the output is lower. If the injury doesn't have strong diagnostic proof, the system can treat it as less serious. If the claim includes future care issues, local jury tendencies, or vehicle-specific market loss, those nuances may not be reflected at all.

The lowball pattern drivers miss

Insurers benefit when the claim is reduced to categories their software handles well and stripped of everything else. In practice, that often means:

- Soft injuries get discounted: claims without strong imaging or specialist records can be scored down

- Future consequences get flattened: software tends to favor what is already documented over what is reasonably expected

- Vehicle value issues get sidelined: true market loss, especially diminished value, is often outside the software's useful range

Here's the practical consequence. Drivers assume the insurer's number came from a careful market analysis or a balanced legal review. Often, it came from a rule-based system that rewards narrower inputs.

The first offer often reflects what the software could process cleanly, not what the claim is actually worth.

Why this matters even more in the Pacific Northwest

In Oregon and Washington, local market conditions can move vehicle values in ways a generic system won't catch well. Trim level, all-wheel drive demand, service history, regional comps, and post-repair stigma all matter. A standardized platform can flatten those details into averages that favor the carrier.

That's why you should treat the insurer's software output as an opening position. Nothing more.

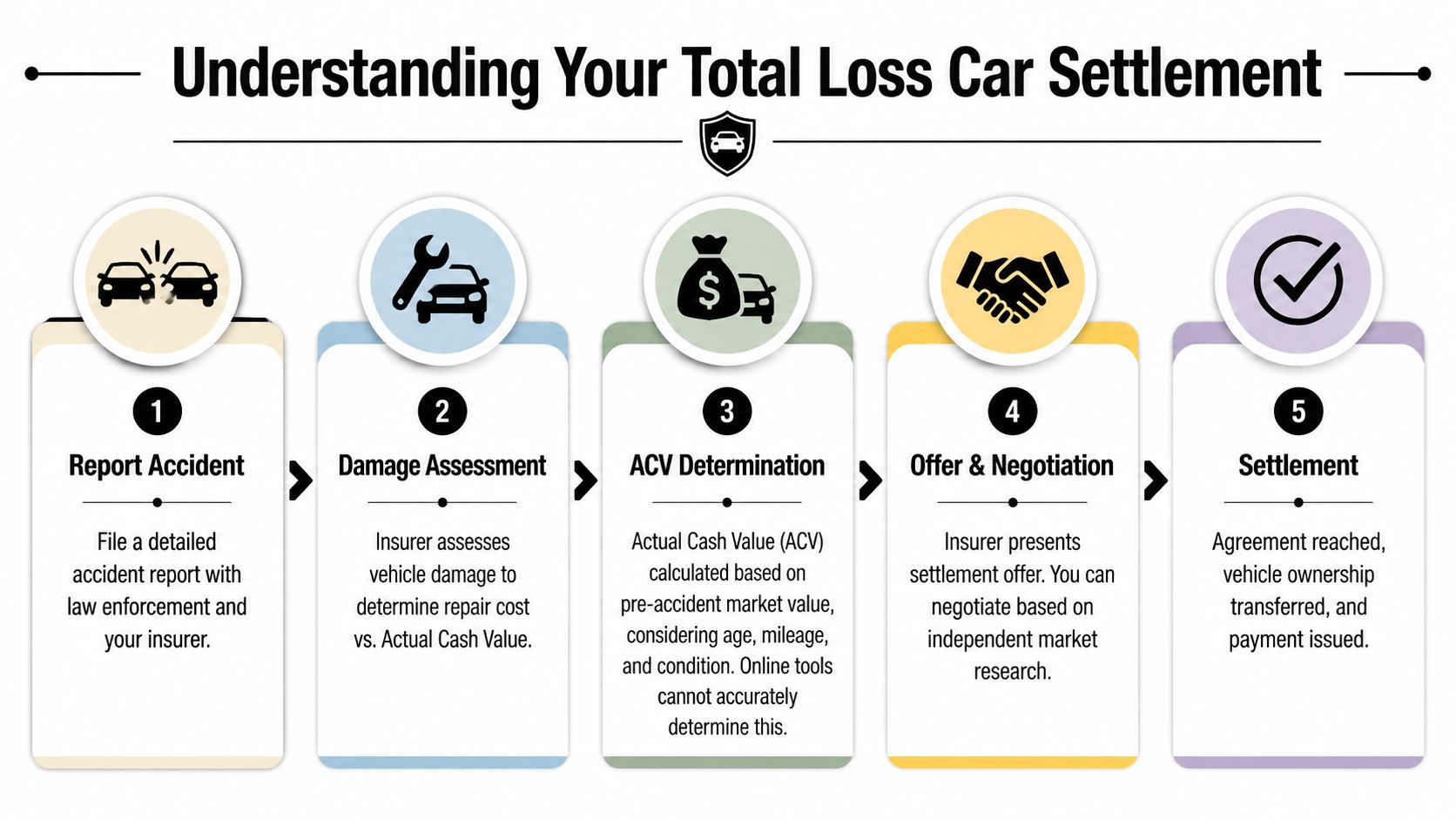

Calculating a Total Loss Vehicle Settlement

A total loss settlement is not supposed to be a guess. It's supposed to reflect Actual Cash Value, which means the value of your vehicle immediately before the crash based on the prevailing market for a comparable replacement.

That's where online calculators fail hardest. They don't know your local market. They don't know whether the insurer used weak comparables. They don't know whether your trim, mileage, condition, or options were matched correctly.

A real total loss dispute looks like a valuation fight

One published example shows how wide the gap can be. In total loss disputes, insurers often undervalue vehicles by 20% to 30%. The same source gives a concrete scenario: on a $50,000 SUV, an insurer may offer $35,000, while independent appraisers using hyper-local comps can secure $41,500+, as described in this analysis of car settlement calculator blind spots and total loss disputes.

That isn't a rounding error. It's a valuation methodology problem.

What a fair total loss calculation should include

A solid total loss review usually turns on evidence like this:

- Comparable local listings: not just broad regional averages, but vehicles that compete with yours in your area

- Trim and equipment matching: base model comps don't value a better-equipped vehicle properly

- Mileage and condition adjustments: service history, tires, body condition, and interior matter

- Pre-loss market timing: values can shift. The key date is the vehicle's market value right before the crash

A generic calculator doesn't do this work. At best, it gives a rough placeholder.

Insurer method versus market method

| Method | Typical insurer shortcut | Market-based appraisal approach |

|---|---|---|

| Comparable selection | Broad or weak matches | Hyper-local, closely matched vehicles |

| Condition review | Minimal adjustment | Specific review of pre-loss condition |

| Equipment | Some options missed | Trim and option package verified |

| Final number | System-generated offer | Evidence-backed market conclusion |

Where drivers lose money without realizing it

A lot of people focus only on the final offer and not on the assumptions underneath it. That's the mistake.

If the insurer picked poorer-condition comps, lower trims, or listings outside your buying market, the offer can look official while being materially wrong. The system may also apply deductions that feel mechanical but aren't tied to how buyers in your area would price a comparable replacement.

If you're trying to sanity-check a total loss offer, a specialized total loss car value calculator can help frame the right questions. The key word is frame. It still won't replace a real appraisal.

What to check first: Ask for the comparable vehicles the insurer used. Then verify year, trim, mileage, condition, options, and distance from your local market. Most weak total loss offers start with weak comps.

The part no online calculator can do

No public calculator can inspect your actual claim file, evaluate the insurer's chosen comps, or test whether local market data supports the offer. That work takes human judgment and documentation.

That's why total loss disputes are won with better evidence, not with a more optimistic calculator.

Uncovering Hidden Losses Diminished Value

A repaired car can still lose value even when the body work looks excellent. That loss is called diminished value. Buyers pay less for a vehicle with accident history, especially when the damage was significant enough to show up in vehicle history reports or raise concerns about structural integrity, paintwork, or long-term reliability.

Most online settlement tools ignore that entirely.

Why diminished value is a separate loss

Not-at-fault drivers are frequently shortchanged at this point. The insurer pays the repair bill, the shop finishes the work, and everyone acts like the property side of the claim is done. It isn't.

Before the crash, your vehicle had one market value. After the crash and repair, it has another. That difference can be a recoverable loss.

One source puts the issue plainly: online settlement calculators overwhelmingly miss vehicle-related diminished value, which can represent 10% to 25% of a vehicle's pre-accident value. The same source gives a useful example. A $30,000 sedan may suffer $3,000 to $7,500 in diminished value after a collision, as discussed in this overview of car accident settlement calculator gaps and diminished value.

Why Pacific Northwest owners should pay attention

In Oregon and Washington, this issue shows up constantly with late-model daily drivers, trucks, SUVs, and higher-end vehicles. If the vehicle had solid market appeal before the crash, accident history can shrink buyer demand after the repair. The better the vehicle was before the loss, the more noticeable the post-repair stigma can be.

That's especially true when the vehicle has any of the following:

- Late model status: buyers expect cleaner history on newer vehicles

- Higher resale sensitivity: popular SUVs, trucks, and premium brands often take a visible hit after reported damage

- Substantial repair history: larger repairs are harder to explain away in resale negotiations

A simple way to think about the math

Diminished value is not the repair invoice. It's not the deductible. It's not what the insurer says your car is “functionally fine” to drive.

It's the difference between these two numbers:

- What your vehicle was worth before the crash

- What the same market will pay after the repair and accident history

If you want to understand how this type of claim is evaluated, this overview of automobile diminished value is a better fit than a generic settlement estimator.

If a buyer would offer less because the accident is on record, the loss is real whether the insurer's calculator includes it or not.

What online calculators leave out

Most calculators prompt for injury-related fields. They rarely ask for VIN, trim package, prior condition, market comps, paintwork scope, structural involvement, or accident history impact on resale. Without those inputs, the tool can't calculate diminished value in any meaningful way.

That omission is not minor. It changes the total claim value.

A driver who relies on the calculator alone may think the property portion of the claim is fully resolved when a separate market-based loss still exists.

Your Next Steps in Oregon and Washington

If you're in Oregon or Washington and the number feels low, treat that instinct seriously. Vehicle claims are often under-evaluated because the process looks polished while the valuation work underneath is weak.

Start with the basics. Preserve photos. Keep repair records. Save every insurer valuation report and every comparable vehicle they relied on. If you need a solid checklist for the immediate aftermath of a crash, this practical set of Lein Law Offices car accident advice is worth reviewing.

When to push back

You should dispute the offer when any of these show up:

- The comps are poor matches: wrong trim, very different mileage, weak condition match

- The valuation ignores local demand: especially common with Pacific Northwest SUVs, trucks, and all-wheel-drive vehicles

- A repaired vehicle lost resale value: but the insurer treats the repair bill as the end of the story

The important thing is timing. Push back before you sign away the property portion of the claim.

The appraisal clause matters

Many policies contain an Appraisal Clause. It's one of the most effective tools available when the dispute is about value rather than coverage. In plain English, it creates a process for deciding what the vehicle loss is worth instead of forcing you to accept the carrier's internal number.

That matters because it moves the fight away from one-sided software and toward evidence.

This short video gives a useful overview of how these disputes unfold in practice:

A practical action plan

If you're facing a low total loss or diminished value offer in Oregon or Washington, take these steps in order:

Request the insurer's full valuation packet

Don't accept the summary page alone.Review every comparable vehicle

Wrong trim and weak mileage matches are common problems.Separate injury value from vehicle value

The auto accident settlement calculator may have helped with the first. It won't validate the second.Use the appraisal process when value is the dispute

That's often the cleanest route when negotiations stall.

The goal isn't to make the claim complicated. It's to stop the insurer from oversimplifying it.

Frequently Asked Questions

Can I use an auto accident settlement calculator for a property-damage-only claim

Not reliably. Most calculators are built around injury inputs such as medical bills, wage loss, and pain and suffering. They don't perform a market appraisal of your car, and they don't measure diminished value in a meaningful way. If the dispute is about what the vehicle was worth before the crash or what it lost after repair, you need evidence tied to the vehicle itself.

Is the insurer's calculator-generated offer final

No. It's an offer, not a verdict. If the number came from internal software or weak comparable vehicles, you can challenge it with better market evidence. That is especially important in total loss and diminished value claims, where the insurer's process may rely on assumptions that don't reflect your actual vehicle or your local market.

Are accident settlements taxable

Sometimes yes, sometimes no. The answer depends on what the payment is compensating you for and how the claim is structured. Property damage, personal injury, lost wages, and other components can be treated differently. That's a tax question, not just an insurance question, so it's smart to confirm the treatment with a qualified tax professional before you assume anything.

If your insurer is lowballing a total loss or diminished value claim, Total Loss Northwest helps drivers in Oregon and Washington challenge those numbers with certified independent appraisals. They specialize in market-backed total loss and diminished value reports and can invoke the Appraisal Clause to take biased insurer valuation software out of the driver's seat.