You've got a damaged car, a claims adjuster on the phone, and a settlement number that doesn't match reality. You know what your vehicle was worth before the crash. You know what similar vehicles sell for. But the insurer's valuation arrives with a neat printout and a low number, and suddenly you're expected to accept it.

That's where Auto Appraisal Washington becomes practical, not theoretical. A proper appraisal gives you a way to challenge a weak valuation with evidence, method, and a process the insurer has to take seriously. In Washington, that matters even more now because the law has become much clearer for drivers who need to dispute actual cash value or the amount of loss on a damaged vehicle.

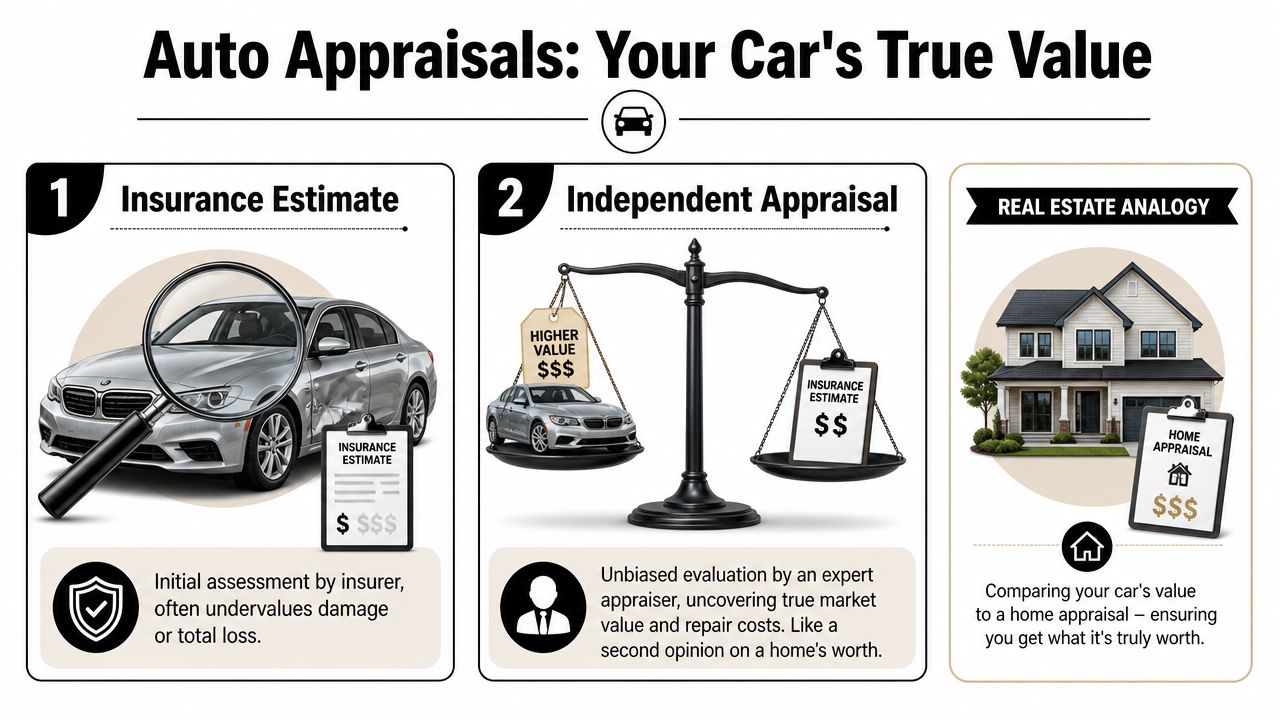

Your Car Is Worth More Than the Insurer Says

The call usually sounds routine. The adjuster says the vehicle is a total loss, or says the repair figure is set, and then gives you a number as if it's settled. You look at the valuation and spot the problems right away. Wrong trim. Bad comparable vehicles. Missing options. No meaningful discussion of condition. Maybe the report ignores recent work, repaired prior damage, or the fact that your vehicle sits in a thin market where good comps are hard to find.

That frustration is justified.

An independent appraiser changes the conversation. Instead of arguing feelings, you submit a structured valuation built on market support, condition analysis, and documentation. That's often the difference between “I disagree” and “Here's why your number doesn't hold up.”

Washington drivers are seeing more of these disputes because the insurance market itself has grown. According to the National Association of Insurance Commissioners, total direct premium written in-state has increased 81% since 2015 in Washington, which means a larger claims environment and more valuation disputes that need a standardized resolution path, as shown in the NAIC Washington market trends report.

Practical rule: The first number from the insurer is not the final word on your vehicle's value.

If you're still at the front end of the claim, get organized before you respond. Gather photos, the valuation report, repair estimates, option lists, maintenance records, and the declarations page for your policy. If you need a basic roadmap for the claims side before the valuation fight starts, this guide to filing an auto insurance claim is a useful starting point.

What works is evidence. What doesn't work is arguing with an adjuster from memory while their software printout sits in the file.

Understanding Auto Appraisals in Washington State

A car appraisal works a lot like a real estate appraisal. The question isn't what someone hopes the property is worth. The question is what the market supports, after adjusting for the facts that make that specific property different from the next one. Vehicles work the same way.

The need for an Auto Appraisal Washington typically stems from one of two problems. Either the insurer says the vehicle is a total loss and the value is too low, or the vehicle was repaired and its market value dropped because it now carries an accident history.

Total loss appraisal

A total loss appraisal focuses on pre-loss value. The appraiser reconstructs what the vehicle was worth immediately before the accident. That means looking at real market exposure, vehicle configuration, mileage, condition, title history, and the quality of the comparable vehicles being used.

Insurer valuations often go sideways. The software may pull broad comps that look similar on paper but aren't competitive substitutes. A base trim gets compared to an upgraded trim. A rough example gets treated like a clean one. A local scarcity issue gets flattened into a generic number.

Diminished value appraisal

A diminished value appraisal asks a different question. If the vehicle has been repaired, what is it worth now compared with what it would have been worth had it never been wrecked? Buyers discount repaired collision vehicles. Some do it aggressively. The right appraisal measures that loss in marketability and resale value.

For a closer look at how that type of claim works, see this explanation of a Washington diminished value appraisal.

Why insurer numbers are often low

The problem usually isn't one bad data point. It's a stack of weak assumptions.

- Comparable selection issues. The insurer may use vehicles that aren't comparable in trim, equipment, or condition.

- Condition shortcuts. Reports often apply broad adjustments without enough support from photos, records, or inspection detail.

- Thin-market blindness. Rare trims, enthusiast vehicles, specialty vehicles, and unusual configurations don't fit neatly into generic valuation systems.

- History over-discounting or under-discounting. Prior repairs, accident history, and title flags need to be handled carefully. Sloppy treatment pushes the result in the wrong direction.

A solid appraisal isn't a prettier printout. It's a defensible answer to the question the insurer has to pay on.

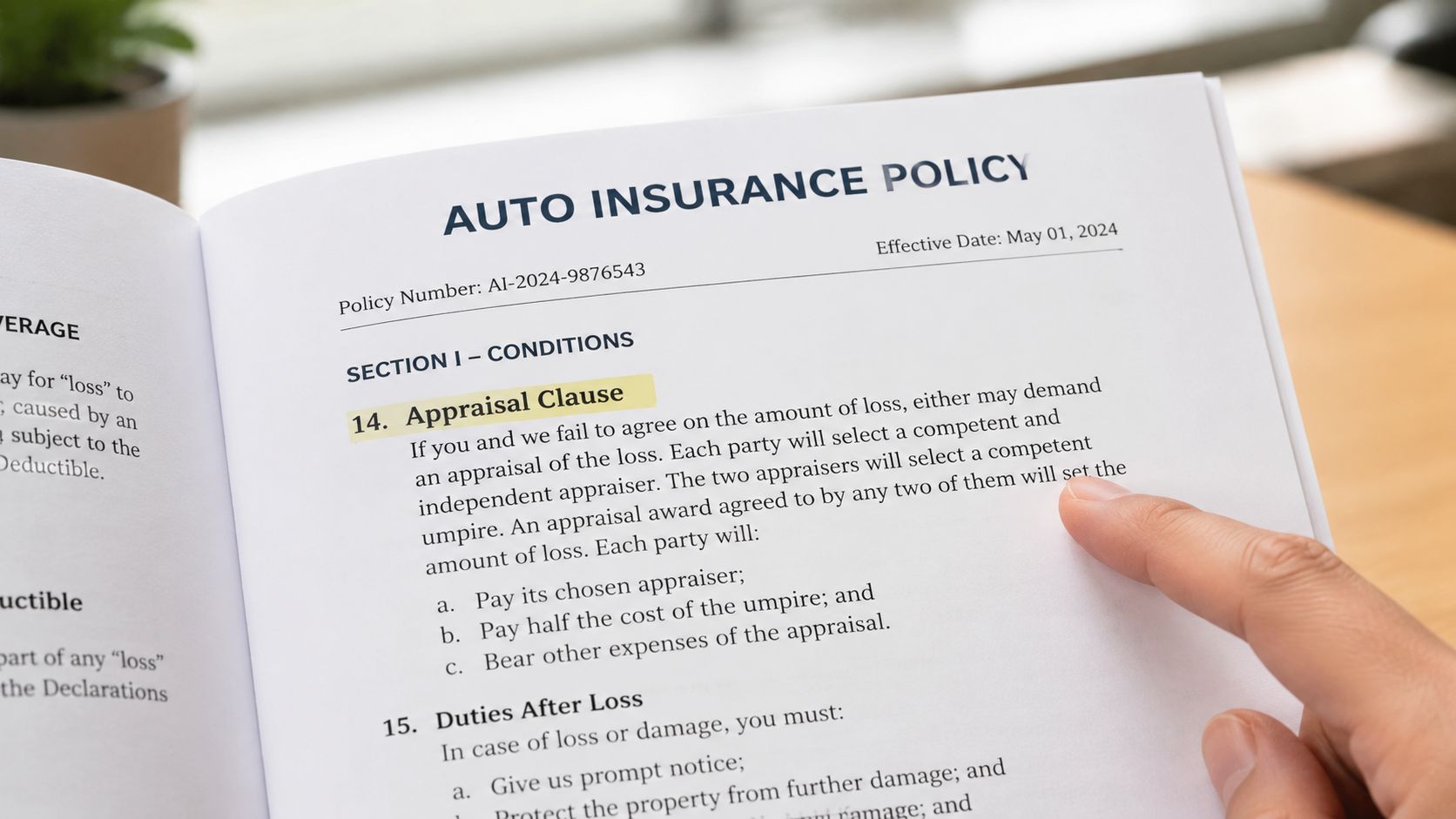

The Appraisal Clause Your Secret Weapon in Washington

The strongest tool in many Washington vehicle disputes isn't an angry phone call. It's the appraisal clause in the policy.

That clause is the mechanism that lets a value dispute move out of the insurer's internal estimate process and into a structured resolution process. In plain terms, if you and the insurer disagree about value, the appraisal clause can force the dispute into an evidence-based format instead of leaving you stuck arguing with the same valuation system that produced the low offer.

What changed in 2026

Washington made this much clearer through RCW 48.18.620, effective January 1, 2026. For automobile policies with first-party physical-damage coverage issued or renewed on or after that date, the law requires a right to appraisal for disputes over actual cash value and amount of loss. It also gives the process teeth. Once an appraisal award is issued, the insurer must pay it within 15 days under the statute, as set out in RCW 48.18.620.

That matters because vague policy language used to create hesitation. Drivers often knew the valuation was wrong but weren't sure whether appraisal was available, practical, or enforceable. Washington has now made the pathway much more explicit for qualifying policies after that effective date.

Why this changes leverage

Before a codified process, many disputes stayed informal too long. The adjuster held the file, the software held the number, and the policyholder carried the burden of proving something was off without a clean procedural route. The 2026 law shifts that dynamic.

Here's the key point. Appraisal is about value. It is not a free-form fight about every issue in the claim. That focus is a strength. It narrows the dispute to what your vehicle was worth or what the loss amount should be.

If you want a plain-language breakdown of how the policy mechanism works in practice, this page on the auto insurance appraisal clause is a helpful reference.

A short overview helps if you've never seen the process before:

What drivers get wrong

Many people wait too long because they think they need to “negotiate harder” first. Sometimes negotiation works. Often it doesn't. If the insurer's valuation model is the problem, another phone call won't fix the model.

Don't confuse a valuation dispute with a customer service problem. One needs evidence and procedure, not just persistence.

The Step by Step Appraisal Process

A low valuation usually does not get fixed by one more phone call. It gets fixed by forcing the dispute into the right procedure, on paper, with support that can hold up if the insurer pushes back.

Step one review the policy

Start with the policy itself. Read the appraisal language, the loss settlement terms, and any definitions tied to actual cash value or amount of loss. Do not rely on a call-center summary of your rights.

For Washington drivers, timing matters. Check when the policy was issued or renewed and whether the dispute falls within the scope of RCW 48.18.620. That statute gives many policyholders a clearer path to compel an appraisal process, but only if the policy and claim fit the rule.

The goal here is simple. Confirm that you are dealing with a valuation dispute and that the contract gives you a procedure to force a decision.

Step two notify the insurer in writing

Verbal objections get lost. A written demand creates a record and starts the clock on the insurer's response.

Keep it short and direct:

I disagree with your valuation of my vehicle and formally invoke the appraisal provision in my policy for the dispute regarding actual cash value and/or amount of loss. Please confirm receipt of this demand and provide your designated appraiser's contact information.

Include the claim number, VIN, date of loss, and the insurer's valuation report if you have it. Send it by email so there is a time-stamped record, and save the sent message.

If the adjuster replies with delay, confusion, or a statement that appraisal is unavailable, ask them to point to the exact policy language supporting that position. Under the 2026 Washington framework, vague resistance carries less weight than it used to.

Step three choose your appraiser carefully

Your appraiser needs to do more than disagree with the insurer's number. They need to document condition, verify trim and options, review the insurer's comparables, find better market support where needed, and explain every meaningful adjustment.

That work matters because insurers often rely on standardized valuation systems. Those systems can miss package differences, prior condition, unusual local market scarcity, or the effect of documented upgrades. A competent appraiser closes those gaps with evidence.

Ask practical questions before you hire anyone:

- What kinds of claims do you appraise most often? Total loss, diminished value, collector vehicles, or mixed assignments.

- What records do you review? Valuation reports, photos, repair invoices, service records, build sheets, title history, and market listings all matter.

- How do you handle adjustments? Mileage, condition, options, prior damage, and regional market differences should be explained, not guessed at.

- Will you work through the full appraisal process if the insurer contests the number? Some people sell reports. Fewer will stand behind them in an actual clause dispute.

A cheap report can cost you more than it saves if it cannot survive scrutiny.

Step four let the appraisers try to agree

Once both appraisers are appointed, they exchange information and try to reach an agreed value. This part is often less dramatic than drivers expect. It is usually a file battle, not a courtroom battle.

Good appraisers narrow the dispute fast because they focus on the specific defects in the insurer's valuation. Wrong trim level. Bad comparables. Unsupported condition deductions. Missed options. Improper local market assumptions. If those problems are documented clearly, the range between the two numbers often shrinks.

Sometimes the appraisers reach agreement without needing an umpire. Sometimes they do not. Either result is normal.

Step five use the umpire if needed

If the appraisers cannot agree, the dispute goes to an umpire under the policy procedure. The umpire decides the value issue the appraisers could not resolve.

Choose this step with realistic expectations. The umpire is not deciding whether the adjuster was rude, whether claim handling was slow, or whether every part of the loss was handled perfectly. The umpire is there to decide value.

That is why your file has to be clean. The stronger submission usually comes from the side that can show exactly how the number was built and exactly why the opposing number fails.

Keep your file tight

During the process, stay disciplined.

- Save every email and letter. Written records matter if the insurer changes position later.

- Keep the insurer's valuation report and comparables. You need to see what they relied on before you can attack it.

- Gather documents that prove condition and equipment. Photos, service records, window stickers, invoices, and upgrade receipts can change value.

- Answer reasonable requests quickly. Delay on your side gives the insurer room to stall.

- Keep the dispute centered on value. Appraisal works best when the issue stays narrow and supported.

What a Defensible Appraisal Report Includes

Not every appraisal report is worth handing to an insurer. Some are little more than a conclusion with no real support behind it. A defensible report shows its work.

For diminished value and total loss assignments, the strongest methodology is a manual, market-data-based reconstruction of value, not a generic software estimate. One Washington appraisal provider describes combining vAuto market analysis, NADA archival valuation, Carfax history, repair invoices, and photo documentation to reconcile market exposure, condition adjustments, and title history in a way that can challenge insurer valuations on uncommon trims and specialty vehicles, as described in this Washington diminished value methodology overview.

The core ingredients

A report should answer two questions. First, what data was used. Second, why that data supports the final number.

Here's the checklist I'd use to judge whether a report is likely to hold up:

| Component | Why It Matters |

|---|---|

| Market comparable analysis | Shows what similar vehicles are actually offered or sold for, instead of relying on a black-box output |

| Vehicle identification details | Confirms trim, options, drivetrain, packages, and configuration so the wrong comps don't control the value |

| Mileage adjustment logic | Explains whether mileage differences matter and how they were handled |

| Condition analysis | Distinguishes clean examples from rough ones and supports adjustments with inspection notes or photos |

| Carfax or history review | Addresses accident history, title concerns, and reportable events that affect market reaction |

| Repair invoices | Helps evaluate quality of prior or post-loss repairs and supports diminished value analysis |

| Photo documentation | Lets the reader verify condition, damage severity, repairs, and equipment |

| Archival valuation support | Adds another benchmark when current market listings alone don't tell the full story |

| Written methodology | Shows how the appraiser reached the conclusion so the report can be tested and defended |

What weak reports usually miss

Weak reports tend to fail in predictable ways.

- No adjustment reasoning. The number changes, but the report never explains why.

- Bad comp selection. The appraiser picks convenience comps instead of competitive substitutes.

- No history analysis. Prior damage or title issues get ignored or handled casually.

- Thin documentation. There are few photos, limited records, and no real trail to follow.

The report has to be readable by someone who disagrees with it. If they can't follow the logic, they won't respect the result.

Specialty vehicles need more care

A standard commuter car can sometimes be valued from a broader comp pool. A collector car, custom truck, motorcycle, RV, or specialty unit can't. Those files require tighter comparable selection and more thoughtful adjustment work because the market is thinner and the differences between examples matter more.

Costs Timelines and What to Expect

Drivers usually ask two questions right away. What will this cost me, and how long will it take?

The honest answer is that pricing and timing vary by vehicle type, claim type, documentation quality, and whether the insurer's appraiser approaches the process seriously. Standard daily-driver disputes are often simpler than specialty-vehicle files with thin market data, modifications, or disputed condition issues. If you want a practical baseline on fee structure, this overview of auto appraisal cost is a useful reference point.

What affects cost

The fee usually reflects how much work the appraiser must do, not just the fact that a report exists.

- Vehicle complexity. A rare or modified vehicle usually requires harder comp research.

- Claim posture. A straightforward valuation review is different from a live appraisal-clause dispute.

- Record quality. Clean documentation lowers friction. Missing records increase labor.

What affects timing

The legal process sets some structure, but the pace still depends on how fast the parties move. Your side can speed things up by sending complete records early and making a clean written demand. The insurer can slow things down if it drags its feet selecting an appraiser or responding to the evidence.

Once an appraisal award is issued in a qualifying Washington claim, the insurer must pay it within the statutory deadline discussed earlier. That deadline matters because it turns the end of the process into something enforceable, not open-ended.

A good way to think about the appraisal fee is simple. You're paying for a supported valuation position, not just a number on paper.

Washington Auto Appraisal FAQs

Do I need a lawyer to use the appraisal clause

Usually, no. Appraisal is a valuation process, not automatically a lawsuit. Many drivers can invoke it directly if the dispute is about value or amount of loss. If the case also has separate coverage issues, bad-faith concerns, or unusual policy disputes, legal advice may still make sense.

What if the insurer says the report already speaks for itself

That's common. It doesn't end the issue. If the valuation is weak, the question is whether the report is defensible, not whether it exists. A polished insurer report can still rely on poor comps, broad assumptions, or unsupported condition calls.

What does the umpire actually do

The umpire resolves the gap the two appraisers can't close. In practice, that means reviewing the disputed valuation issues, examining the support behind each side's position, and deciding where the evidence leads. The umpire is not there to reward whoever talks louder.

Does this work for leased or financed vehicles

Yes, the valuation question still matters. The ownership structure changes who gets paid and how funds are applied, but it doesn't make an inaccurate value acceptable. If the insurer undervalues the vehicle, the financial structure around the car doesn't fix that mistake.

Is appraisal worth it for classic or custom vehicles

Often, yes. In fact, these are some of the files where appraisal matters most. Appraisal is not just for standard cars. It is a procedural tool for high-value, collector, custom, heavy-equipment, motorcycle, and RV vehicles where the insurer's data model may be structurally weak, as noted in this appraisal clause discussion for specialized vehicles.

Can appraisal help with amount-of-loss disputes even when the car isn't totaled

Yes, if the dispute is about the amount of loss rather than only pre-loss value. That can matter when repair scope, damage valuation, or itemized loss components are contested. The details of the policy language and claim posture still matter.

What usually hurts a driver's case

Three things show up over and over:

- Waiting too long. Delay makes records harder to gather and positions harder to defend.

- Hiring a weak appraiser. A thin report won't carry a serious dispute.

- Arguing without documentation. Strong claims files beat strong opinions.

If your Washington claim feels undervalued, don't guess your way through it. Total Loss Northwest provides certified independent auto appraisals for total loss and diminished value disputes, including appraisal-clause matters, so drivers have a documented valuation position they can use.