A car accident diminished value claim is how you get paid back for the loss in your car's market value after it's been wrecked and repaired. Think about it: even if the repairs are flawless, a car with an accident history is simply worth less to the next buyer. This claim is your legal right to get that lost money back from the at-fault driver's insurance company.

What a Diminished Value Claim Really Means for You

When you've been in an accident, your first thought is usually, "Let's just get the car fixed." But the financial hit doesn't stop once you've paid the body shop. The moment that collision is logged on a vehicle history report, your car's resale value drops, and it's a permanent drop. This is the whole point of a car accident diminished value claim—to recover the cash you've lost just because your car now has an accident on its record.

Picture this: you're looking at two identical used cars. Same make, model, year, mileage, everything. One has a squeaky-clean Carfax, but the other shows a major collision, even though it was repaired by a top-tier shop. Which one are you going to buy? Almost everyone picks the car with no accident history, or they'll demand a serious discount on the one that was wrecked.

A diminished value claim isn't about the repair bill. It's about the permanent stain on your vehicle's history that scares off future buyers and lowers its real-world market value. You have a right to be compensated for this loss.

Understanding the Real-World Impact

Insurance adjusters love to argue that good repairs make your car "whole" again, restoring it to pre-accident condition. While it might look and drive just fine, they're conveniently ignoring how the market actually works. Buyers have legitimate fears about cars that have been in a wreck:

- Lingering Doubts: Was the frame really straightened perfectly? Are there hidden issues that will pop up later?

- Future Resale Problems: They know they’ll face the same scrutiny and have to sell for less when it’s their turn.

- Safety Concerns: There's a persistent belief that once a car's structure is compromised, it’s never quite as safe as it was from the factory.

This isn't just a few hundred dollars we're talking about, especially on newer, more expensive vehicles.

Let's look at a real-world example. Say you're driving your 2018 Porsche 911 Carrera, and someone slams into your rear bumper, causing $15,000 in damage. The repairs are perfect, but that accident is now a permanent part of the car's history. In an actual North Carolina case just like this, an independent appraiser found the Porsche's market value had plummeted by $25,000—far more than the cost of the repairs. You can explore more real-world examples and see how diminished value claims vary by state.

This is exactly why getting an independent, expert appraisal is the single most important thing you can do. It takes the power away from the insurance company's self-serving formulas and forces them to deal with hard market data. It gives you the proof you need to negotiate a fair settlement for the very real money you've lost.

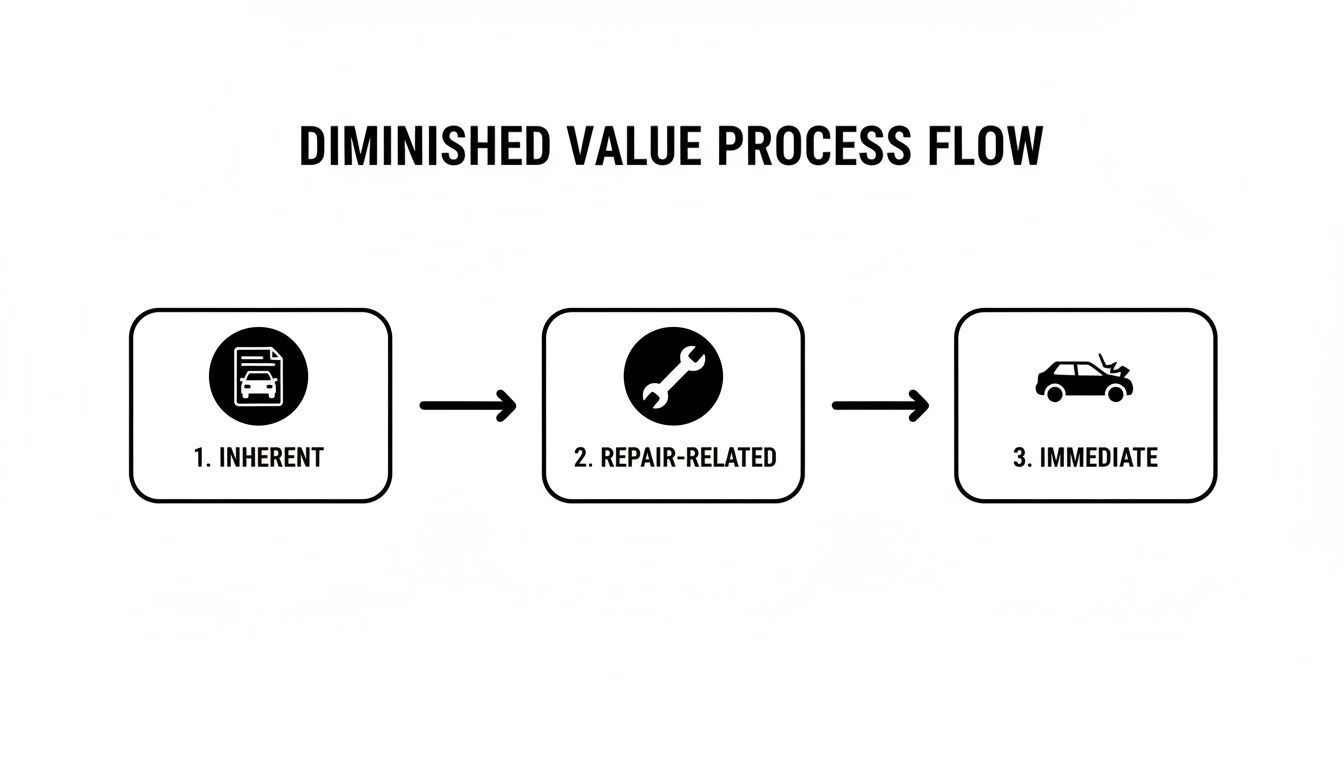

Decoding the Three Types of Diminished Value

Before you can file a successful car accident diminished value claim, you have to know exactly what kind of loss you're fighting for. "Diminished value" isn't just one thing—it’s actually an umbrella term that covers three different kinds of financial hits your car can take. Pinpointing the right one for your situation is the first real step in building a case that an adjuster will take seriously.

Inherent Diminished Value: The Unavoidable Stigma

For most people, the conversation starts and ends with Inherent Diminished Value. This is the automatic, guaranteed loss in your car's market value simply because it now has an accident history. It's a permanent stain on its record.

Think about it from a buyer's perspective. Even if the repairs are absolutely perfect and the car looks brand new, a savvy shopper will always pay less for a vehicle with a known collision history than they would for the exact same car with a clean record. That stigma is what this type of claim is all about.

Repair-Related and Immediate Diminished Value

Then you have Repair-Related Diminished Value. This is a separate hit to your car's worth that happens when the repairs are just plain bad. If the body shop cuts corners with cheap, aftermarket parts instead of factory OEM ones, or if the new paint doesn't quite match the old, the value drops even further. This loss is a direct result of shoddy workmanship.

Finally, there's Immediate Diminished Value, which is a bit less common in claims. This is the difference between your car's value right before the crash and its value sitting on the side of the road, mangled and unrepaired. It's a real loss, but since most people get their car fixed, this loss usually morphs into Inherent Diminished Value once the work is done.

Most of the time, your claim will hinge on Inherent Diminished Value. It’s the fundamental loss that exists even with top-notch repairs. If the shop also did a poor job, you might have a case for both inherent and repair-related diminished value.

To make this crystal clear, let's break down how each type works and when it comes into play.

The Three Types of Diminished Value Explained

This table gives you a quick snapshot of the different categories of diminished value and helps you identify which one applies to your vehicle after an accident.

| Type of Diminished Value | What It Means | When It Applies |

|---|---|---|

| Inherent Diminished Value | The automatic loss in value due to the vehicle's new accident history. | After perfect repairs are completed. This is the most common claim. |

| Repair-Related Diminished Value | Additional loss in value caused by low-quality repairs or non-OEM parts. | After subpar repairs are completed and evidence of poor work exists. |

| Immediate Diminished Value | The loss in value right after the crash, before any repairs have started. | Immediately following an accident, if you were to sell the car as-is. |

Seeing the numbers helps put it all into perspective.

Let's say your car was worth $30,000 before someone rear-ended you. The body shop does $5,000 worth of fantastic, factory-quality repairs. But now, because of that accident on its record, buyers are only willing to pay $26,000. That $4,000 gap is your Inherent Diminished Value.

Now, imagine that same shop used cheap parts and the new bumper’s paint is a shade off. The car might only be worth $24,000. In that case, you've got the $4,000 in inherent loss plus another $2,000 in Repair-Related Diminished Value.

Getting these definitions straight is a game-changer. When you can walk into a negotiation and clearly state which type of loss you've suffered, you show the insurance adjuster you've done your homework. It prevents them from brushing you off and forces them to address the real financial damage you've incurred.

How to Build an Ironclad Diminished Value Case

Winning a car accident diminished value claim isn’t about getting lucky. It’s about building a fortress of evidence. Your job is to hand the insurance adjuster a file so buttoned-up they have no choice but to take your demand seriously. This all starts with keeping meticulous records from the moment of the crash.

To build a strong case, you have to document every single thing related to the damage and the subsequent mechanical repair services. Every receipt, every email, every photo—they all tell a piece of your car's story and its lost value.

The whole process has a natural flow. It starts with the value lost simply because the car now has an accident history, but it can grow from there depending on other factors.

As you can see, the core of your claim is that unavoidable drop in market value (inherent DV). But, if you can also document shoddy repair work or show the vehicle's immediate post-accident state, your case gets even stronger.

Gathering Your Essential Documentation

First things first: you need to pull together a complete file. This file should prove what your vehicle was worth before the accident and chronicle every step of the repair process. The more airtight your documentation is, the less wiggle room the adjuster has to deny or lowball you.

Start by proving your car’s prior condition and value. This includes things like:

- Pre-Accident Photos: Got any pictures of your car looking great? They’re gold now.

- Maintenance Records: A full log of oil changes, tire rotations, and other services shows you took care of your vehicle.

- Original Bill of Sale: This is a great starting point for establishing the car's initial value.

Next, you need to collect everything related to the accident itself and the repairs. Leave no stone unturned.

- The Police Report: This is the official version of events and is crucial for establishing who was at fault.

- Repair Estimates: Gather all of them, even from shops you didn't end up using.

- Final Repair Invoice: This is your most important piece of paper. It details every part, every nut and bolt, and every hour of labor.

- Post-Repair Photos: Once the work is done, take a new set of detailed photos from every angle, documenting the quality of the repair.

Unmasking the Insurer's Lowball Formulas

Let's be blunt: insurance companies are not in the business of paying you top dollar. To keep payouts low and consistent, many of them lean on a deeply flawed calculation known as the “17(c) formula.”

This isn't some official rule or law; it's an internal tool they created to protect their bottom line. It’s notoriously biased against vehicle owners because it completely ignores how real buyers in the real world shy away from cars with accident histories.

The 17(c) formula is the insurance industry's secret weapon to devalue your claim. It systematically ignores real market data in favor of a self-serving calculation that guarantees a lowball offer. Understanding how it works is the key to defeating it.

The 17(c) formula, which got its start in Georgia, usually begins by capping the maximum possible diminished value at 10% of the car’s pre-accident value. From that already-low number, it applies arbitrary multipliers for damage severity and mileage, slicing your compensation down even further. In the real world, losses are often closer to 10-20% of the vehicle’s value, which shows you just how wide the gap is.

Let’s walk through a quick, and sadly typical, example:

- Vehicle Value: Your car was worth $30,000 before the accident.

- Formula Cap: Right off the bat, the 17(c) formula caps the maximum loss at $3,000 (10% of $30,000).

- Damage Modifier: The adjuster decides the damage was "moderate" and applies a subjective 0.50 multiplier. Your potential claim is now just $1,500.

- Mileage Modifier: Your car has 65,000 miles, so they apply another multiplier, say 0.60. Your final "offer" plummets to just $900.

And just like that, a real loss of several thousand dollars gets whittled down to a nuisance payment. If this feels crooked, that's because it is.

The Power of an Independent Appraisal

So, what's your best defense against these bogus formulas? An independent, certified diminished value appraisal. This isn't just a good idea—it's the single most critical step in building a successful car accident diminished value claim.

An independent appraiser doesn't rely on made-up formulas. They do the actual legwork, conducting a detailed analysis based on real-world market data.

A professional appraisal report should always include:

- A physical, hands-on inspection of the repaired vehicle.

- A deep dive into the final repair invoice to truly understand the scope of the damage.

- Local market research comparing sales data for similar cars with and without accident histories.

- Opinions and direct quotes from sales managers at area dealerships.

This report effectively throws the insurer's formula in the trash and replaces it with objective, verifiable proof of your actual financial loss. It moves the entire negotiation away from their turf and into the real world, where hard data matters. Handing an adjuster a professional appraisal fundamentally changes the dynamic and gives you the leverage you need.

You can also get a ballpark idea of your loss by using a purpose-built tool like this diminished value claim calculator: https://totallossnw.com/diminished-value-claim-calculator/

Negotiating Your Claim with the Insurance Adjuster

This is where the rubber meets the road. You’ve done your homework, gathered your evidence, and have a professional appraisal in hand. Now it’s time to formally demand what you're owed and get the insurance adjuster to pay up.

Don't let this part intimidate you. Your preparation is your power. You're no longer just another claimant; you're an informed party with a documented, legitimate financial loss.

Your first move is to send a formal, written demand letter to the at-fault driver's insurance adjuster. This isn't just a quick email asking for a check. It’s a professional package that lays out an undeniable case for your car accident diminished value claim.

Crafting a Powerful Demand Letter

Your demand letter is the foundation of your entire negotiation. It needs to be clear, professional, and straight to the point, logically presenting your argument and all the evidence you’ve collected. An emotional, rambling letter is easy to dismiss. A structured, evidence-based demand forces the adjuster to take your claim seriously from the very beginning.

Make sure your letter hits all these key points:

- Your Details: Include your full name, address, and the claim number so they know exactly who you are.

- Clear Purpose: Start with a direct statement. Something like, "This letter is a formal demand for compensation for the inherent diminished value of my vehicle" leaves no room for confusion.

- The Bottom Line: State the exact dollar amount of your loss, as calculated by your independent appraiser.

- Your Proof: Specifically list every document you're attaching, especially the independent appraisal report.

Think of your demand letter less as a request and more as a professional invoice for a debt. You're simply billing them for the market value their insured driver destroyed. Your appraisal is the itemized receipt. This mental shift puts you in the driver's seat.

Here’s a look at how to phrase the core of your letter. This isn't a word-for-word template, but it gives you the right tone and language.

Sample Demand Letter Language

"Following the collision on [Date of Accident] caused by your insured, [At-Fault Driver's Name], my [Year, Make, Model] vehicle sustained significant damages. While the physical repairs are complete, the vehicle has suffered a permanent and irreversible loss of market value because of the accident history now attached to its VIN.

As documented in the attached certified appraisal from [Appraisal Company Name], my vehicle has incurred an inherent diminished value of $4,250. This figure is based on verifiable market data and a professional analysis of comparable vehicle sales in our local area. I am formally demanding this amount as fair compensation for my loss.

Please find the following documents enclosed for your review:

- Certified Diminished Value Appraisal Report

- Copy of the Final Repair Invoice

- Copy of the Police Report"

This language is direct without being aggressive. It firmly establishes the facts and points to the evidence that backs them up.

Communicating Effectively with the Adjuster

After you send the demand, the adjuster will get in touch. Your job now is to stay firm, professional, and focused. Remember, insurance adjusters are juggling hundreds of claims. Your goal is to make it easier for them to approve and pay your claim than it is to keep fighting it. For more on this, our guide on how to deal with insurance adjusters has some great tips.

Always keep a log of every conversation. Note the date, time, the person you spoke with, and a quick summary. Even better, try to keep all important communication in writing. If you do have a phone call, send a brief follow-up email confirming what was discussed. This creates a paper trail that can be a lifesaver if a dispute comes up later.

Countering Common Pushback Tactics

Adjusters are trained to minimize payouts. They have a standard playbook of objections they use to shut down claims, so knowing what's coming is half the battle.

One of the first things you'll probably hear is, "Our high-quality repairs restored your vehicle to its pre-accident condition and value." Don't take the bait. This is your cue to pivot right back to your strongest piece of evidence.

Your response should be simple: "The quality of the repairs isn't the issue here. The issue is the permanent loss of market value due to the accident history, which is a separate and verifiable loss. As my certified appraisal shows with real market data, a car with a collision history is worth significantly less than an identical one with a clean record."

Another classic move is for the adjuster to offer a lowball settlement based on an internal formula, like the 17(c) method we talked about earlier.

Don't get dragged into an argument about why their formula is flawed. Just shut it down. Simply state, "My claim isn't based on a generic, internal formula. My demand is based on a professional, independent appraisal that reflects the actual market for my specific vehicle in my local area. That report provides all the objective data needed to support the $4,250 loss."

By constantly bringing the conversation back to your appraisal, you control the narrative. You force them to argue against your facts, not their own flawed math.

Using the Appraisal Clause to Settle a Dispute

So, you’ve sent your demand letter. You’ve patiently countered the adjuster’s lowball offers and dismantled their weak arguments. But what do you do when the insurance company just digs in its heels and refuses to pay what’s fair?

This is where most people get frustrated and give up. Don't. You have one more powerful tool in your back pocket: the Appraisal Clause.

Buried in the fine print of most auto insurance policies, this clause is basically a built-in dispute resolution system. When you invoke it, you take the decision-making power away from the stubborn adjuster and place it in the hands of a neutral panel. For a stalled car accident diminished value claim, it’s a total game-changer.

Activating the Appraisal Clause

Invoking the appraisal clause isn't a casual conversation. You can’t just mention it on the phone. It's a formal step that requires you to send a written demand to the insurance company, officially stating your intent to exercise this right under their policy.

This letter sends a clear signal: the back-and-forth negotiation is over, and you're escalating the matter.

Once you’ve sent that letter, a specific process kicks off:

- You hire your own appraiser. You'll need to select and pay for a competent, independent appraiser to argue your case. This is usually the same expert who wrote your initial diminished value report.

- The insurer hires their appraiser. The insurance company will do the same, hiring someone to represent their position.

- An umpire is chosen. The two appraisers then have to agree on a neutral, third-party expert, known as an umpire. If they can’t agree on someone, they can ask a court to appoint one.

This three-person panel is now in charge of determining the correct amount of diminished value. To get into the nitty-gritty, you can learn more about the specifics of the insurance appraisal clause in our detailed guide.

How the Panel Reaches a Binding Decision

The beauty of this process is that it’s designed to be fair. Your appraiser will present their detailed report and market analysis, and the insurance company’s appraiser will do the same. They'll negotiate first to see if they can find common ground.

If the two appraisers can't come to an agreement, the dispute goes to the umpire. The umpire acts as the tie-breaker, reviewing the evidence from both sides before making a final call.

An agreement by any two of the three parties—your appraiser and the umpire, or the insurer’s appraiser and the umpire—becomes a binding award. The insurance company is legally required to pay that amount.

This is the key. The appraisal clause cuts through the adjuster's delay tactics and forces a resolution based on expert analysis, not the insurance company's self-serving formulas. It completely levels the playing field.

Why This Is Your Ultimate Leverage

Yes, you have to pay for your appraiser and potentially split the umpire's fee, but that cost is often a small price for a fair settlement. In my experience, simply the act of formally invoking the clause is often enough to make a stubborn insurer suddenly more willing to negotiate.

They know the odds of an independent panel agreeing with their lowball number are incredibly slim.

Every crash leaves a financial scar. The Insurance Information Institute notes that diminished value claims average around $1,500 nationwide, but the actual loss is frequently much higher. Kelley Blue Book warns that a vehicle's market value can plummet by up to 30% after an accident, simply because buyers are wary of a car with a collision history. For higher-end vehicles, the National Association of Insurance Commissioners (NAIC) suggests a real-world value loss of 10-20% is typical. You can discover more about how diminished value is estimated after an accident on KBB.com.

When an adjuster is faced with your solid independent report and the very real threat of a binding appraisal, their position gets a lot weaker. They are forced to calculate the risk of losing the appraisal and being on the hook for a much larger claim, plus their own appraiser's fees. Suddenly, settling for your demanded amount starts to look like a much better business decision for them.

Answering Your Questions About Diminished Value

When you're trying to navigate a car accident diminished value claim, a lot of questions pop up. It's totally normal. Even when you grasp the big picture, the little details of your specific situation can be confusing. Let's walk through some of the most common things that trip people up.

Getting straight answers is the key to moving forward with confidence and not leaving money on the table. This is all about making sure you’re equipped to get the full compensation you deserve.

Can I Just File the Claim with My Own Insurance Company?

This is easily the most common point of confusion, and the answer is almost always a firm "no." A diminished value claim is what's known as a third-party claim. That means you have to file it against the insurance company of the driver who caused the accident.

Think of it this way: your policy is a contract with your insurer. It's designed to fix your car's condition, not to protect its market value. Insurers are very strict about this distinction, and there are very few exceptions to the rule.

The bottom line is that in nearly every state, your only route to recovering diminished value is through the at-fault driver's liability insurance. The one big exception is Georgia, which has a specific law allowing you to file against your own policy.

Is There a Time Limit for Filing My Claim?

Yes, and this is a big one. Missing this deadline means you forfeit your right to the claim, no matter how solid your case is. Every state has a legal clock ticking, known as the statute of limitations, for property damage claims. Diminished value falls right into that category.

This is the hard deadline for filing a lawsuit to recover your losses. If that window closes, you’re out of luck.

The exact time you have varies quite a bit from state to state, but you're typically looking at somewhere between two and six years from the date of the accident. The best advice? Look up your state's statute of limitations and start your claim process as soon as the repairs on your car are finished. Don't wait.

Do I Really Need to Hire a Lawyer?

For most diminished value claims, you probably don't need a lawyer. The most effective weapon in your arsenal isn't a legal threat; it's a rock-solid, certified, independent appraisal report.

This appraisal gives you the objective, expert evidence you need to build a case that's hard to argue with. Armed with that document, most people can successfully negotiate a fair settlement on their own.

That said, there are a few scenarios where getting legal help is a smart move:

- You're Dealing with a Bad Faith Insurer: If the adjuster is ignoring you, denying the claim for no good reason, or playing games, a lawyer can get their attention.

- You Were Also Injured: If you have a personal injury claim from the same accident, your attorney can often roll the diminished value claim into the larger case.

- Your Car is High-Value: For classic cars, exotics, or heavily customized vehicles where the value loss is substantial, having an attorney adds serious credibility to your demand.

What If I’m Still Making Payments on the Car?

It doesn't matter if you have a loan—you can and absolutely should file a claim. The loss in value hurts you directly, whether you own the car free and clear or not.

When your car has a loan, that loss of value eats into your equity. It can quickly put you "upside down," where you owe more on the loan than the car is actually worth. A successful diminished value settlement helps you bridge that gap and protects you financially.

Does This Apply If My Car Is Leased?

A leased car loses value just like any other. In fact, filing a car accident diminished value claim can be even more crucial when you're leasing.

Why? Because when your lease is up, you have to return the car. The leasing company will inspect it, and an accident on its history is a huge red flag. They will almost certainly hit you with penalties for "excessive wear and tear" or a direct charge for the value it lost. You'll be the one writing that check. By filing a claim now, you recover the money you'll need to cover those inevitable end-of-lease charges.

If you're in Oregon or Washington and hitting a brick wall with an insurance company, don't give up. Total Loss Northwest provides certified appraisals that give you the leverage to get what you're owed. We're in your corner. Get your expert appraisal at https://totallossnw.com.