You're probably reading this with your heart still pounding, your car half on the shoulder, and your phone full of missed calls. If you searched car accident fort worth today, you don't need recycled safety slogans or vague insurance advice. You need a calm plan that protects your body, your claim, and the value of your vehicle before someone else controls the story.

The biggest mistake drivers make after a crash isn't only what happens at the scene. It's what they fail to preserve in the first few minutes. Damage gets moved, witnesses leave, road conditions change, and the insurer starts building a file before you've even caught your breath. If you were not at fault, that early window matters just as much for your financial recovery as it does for your immediate safety.

Your Guide for What Happens After a Crash in Fort Worth

Fort Worth crashes aren't rare interruptions. They're part of the city's daily traffic reality. Recent coverage often tells you where a wreck happened, how long lanes were blocked, and when traffic started moving again. That reporting is useful for commuters, but it usually stops right where your real problems begin. As CBS Texas noted in local crash coverage, the missing piece is what a not-at-fault driver should do to protect their financial interests after the scene clears.

That's the gap that matters.

If your vehicle may end up repaired, you need to think about diminished value from minute one. If the damage is severe enough for a total loss fight, you need clean proof of condition, impact, and market relevance before the tow truck takes your car away. Those are not later problems. They start at the curb.

What most drivers get wrong

It's often assumed the process goes like this: stay safe, call insurance, get repairs, move on. That's how people get boxed into weak claims.

A better approach is this:

- Protect health first: injuries can appear after the adrenaline fades, and timely care creates a clean record.

- Preserve evidence second: photos, positions, debris, weather, and witness names disappear fast.

- Control the claim narrative third: if you let the police summary, tow yard intake, or insurer database do all the talking, you lose your advantage.

If you need a practical recovery resource after the scene, this guide on prompt care after a car accident is worth reviewing because early treatment decisions often affect both your recovery and your claim file.

The crash ends. The claim fight starts.

Keep one thing straight. You are not just handling an accident. You are preserving evidence for a valuation dispute that may show up days later. If you want a more complete post-crash roadmap, review these steps after a car accident while the details are still fresh.

Prioritize Safety and Call for Help

Fort Worth recorded 12,865 total traffic crashes in 2024, averaging roughly 35 crashes per day, according to Fort Worth crash statistics. That volume means one thing. You need a default response that works under stress.

First five minutes

Do these in order:

Check for injuries

Ask yourself if you can move safely. Then check passengers. Then check the other vehicle if you can do it without stepping into danger.Get out of active danger

If the cars can be moved safely, move them out of traffic. If they can't, stay put, turn on hazards, and get to a safer position away from moving vehicles if possible.Call for help

Call 911 if anyone may be hurt, traffic is blocked, a vehicle is disabled in a dangerous location, or the scene feels unstable. If it's minor and no one appears injured, follow local reporting guidance and still document everything.

What to tell dispatch

Keep it clean and brief.

- Your location: street, direction of travel, nearest intersection, or landmark.

- The scene: number of vehicles, whether lanes are blocked, whether anyone appears injured.

- Immediate hazards: leaking fluid, smoke, debris, or a vehicle in a live lane.

Don't start explaining fault. Dispatch needs logistics, not your theory of the crash.

Do not admit fault. Stress makes people apologize for things they didn't cause. Keep your words factual and minimal.

What to avoid on scene

You don't need to be cold. You do need to be disciplined.

- Don't argue: angry roadside debates help no one and can escalate fast.

- Don't speculate: avoid guessing speed, distance, light timing, or what the other driver “must have” been doing.

- Don't minimize pain: saying “I'm fine” too early can come back to haunt you if symptoms appear later.

A calm, controlled scene protects more than your safety. It prevents bad statements from becoming permanent claim problems.

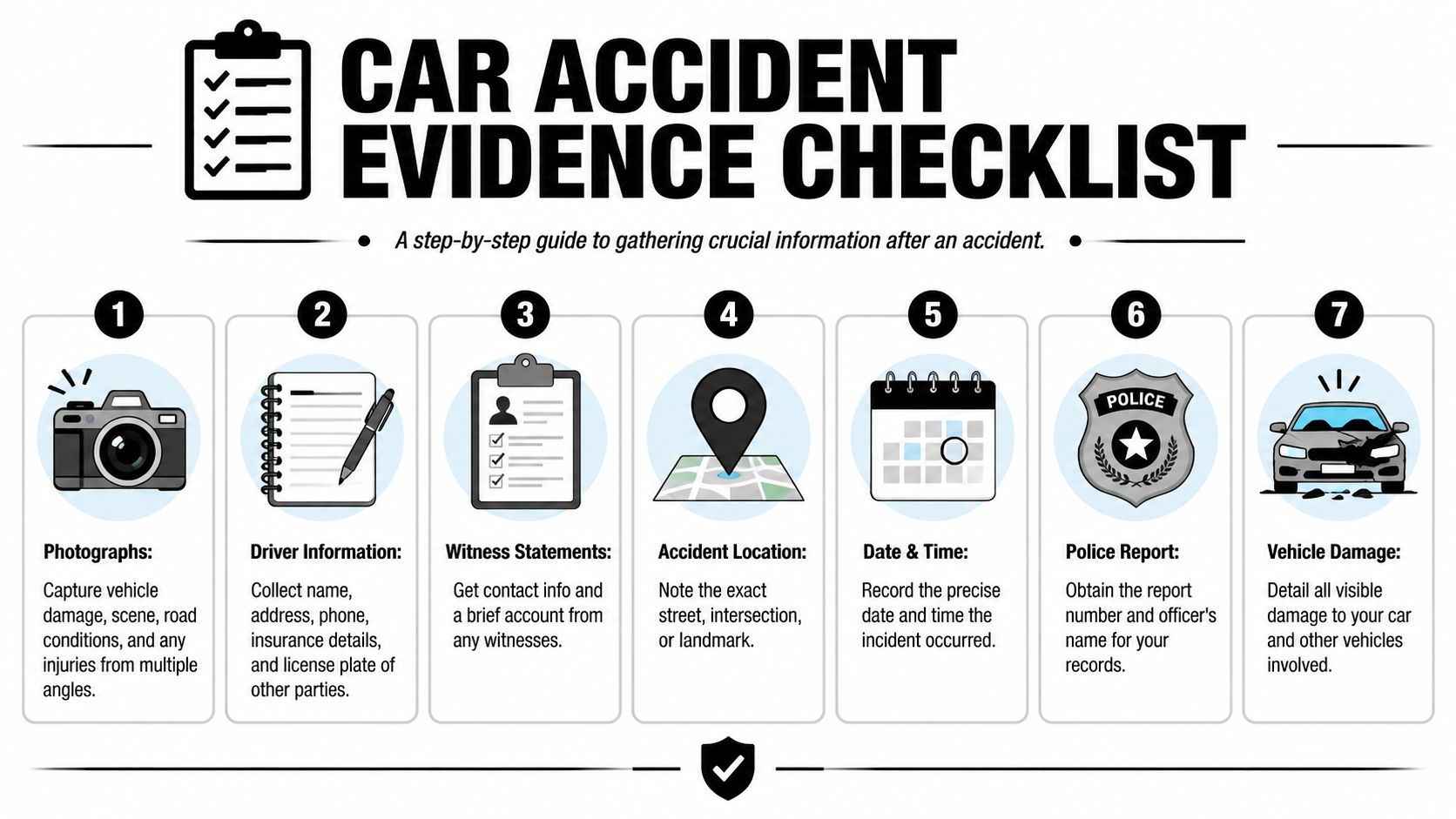

Document Everything to Build Your Case

The crash scene is the only time you get the raw version of the evidence. A few hours later, cars are towed, skid marks fade, witnesses leave, and the insurer starts building its file. If you want a fair diminished value or total loss outcome, build your own file first.

The photo list that actually helps later

A couple of bumper photos will not protect you. You need shots that show damage, context, and pre-loss condition.

Start wide. Get the full roadway, lane layout, traffic signals, signs, debris, and where the vehicles ended up. Then step closer and photograph each side of every vehicle involved. Finish with tight shots of impact points, broken lights, scraped wheels, deployed airbags, leaking fluids, bent suspension parts, and anything pushed out of alignment.

Do one more thing drivers skip all the time. Photograph the parts of your car that were not damaged.

Get clean shots of straight body panels, paint condition, wheel faces, tire condition, glass, seats, dash, mileage, and any upgraded trim or options. Those photos stop an insurer from acting like your car was rough before the crash or pretending higher-value equipment was never there.

Write down the facts before your memory softens

Make notes in your phone while the sequence is still clear.

Record the exact location, time, direction each vehicle was traveling, what lane you were in, what traffic control was present, and what you saw just before impact. Add details that disappear from the record later, such as sun glare, standing water, road work, blocked sightlines, or a vehicle that changed lanes suddenly.

Keep it factual. Do not turn your notes into an argument about fault.

Here's a quick visual walkthrough that reinforces the evidence mindset:

Witnesses and paper trails matter more than drivers think

If someone saw the crash, get their name and contact information before they leave. A short text from a neutral witness can carry more weight than a long explanation from either driver.

Save every document connected to the car after impact. That includes tow tickets, storage invoices, rideshare receipts, body shop intake photos, and any notice showing when and where the vehicle was moved. In a total loss dispute, those records help prove condition, custody, and timing. In a diminished value claim, they help show the severity and continuity of damage from day one.

Take photos as if the adjuster, body shop, and appraiser will never see the car in its original post-crash state. Sometimes they will not.

If the insurer starts pressing you early, slow the conversation down and stick to your evidence. This guide on how to deal with insurance adjusters after a crash will help you avoid careless statements that weaken the value of your claim.

Handle Police and Insurance Reporting Correctly

The first official versions of your crash will usually come from two places. The police report and the insurance file. Both matter. Neither is automatically perfect.

Dealing with police at the scene

When officers arrive, stick to observable facts. Tell them what you saw, where you were, and what happened in sequence. If you don't know something, say you don't know. Don't fill gaps just to sound certain.

Useful facts include:

- Where you were traveling

- What traffic control was present

- Where impact occurred

- Whether you noticed injuries or hazards

What doesn't help is roadside argument. The officer is creating a working summary, not issuing a final truth certificate for your insurance claim.

If you receive a report number, save it immediately in your phone and screenshot it. Small administrative details get lost all the time after a stressful crash.

The first call to your insurer

Report the crash promptly. But don't turn that call into a free-form interview.

Use a simple script:

“I'm reporting a collision. It happened at this date, time, and location. These vehicles were involved. Police responded. My car has damage, and I'm still assessing injuries and documentation.”

That is enough to open the claim.

Then stop talking unless they ask for basics. You do not need to estimate repair cost, guess fault allocation, or describe injuries in final terms on day one. Early statements often age badly because symptoms develop, repairs uncover more damage, and liability evidence changes.

Recorded statements and adjuster pressure

Adjusters may sound casual. Don't mistake that for neutrality. Their file notes matter.

If you're getting pushed into broad statements, slow it down. Review your documentation first. If you want a practical overview of those conversations, read this guide on how to deal with insurance adjusters.

A few hard rules:

- Never guess: if you're unsure, say so.

- Don't downplay injuries: pain often shows up later.

- Don't accept the adjuster's phrasing: use your own words.

- Don't let urgency force errors: fast reporting is good, sloppy reporting is expensive.

The first insurance conversation should open the file, not close your options.

If the police report later contains errors or omissions, your photos, witness contacts, and notes become your correction tools. That's why the earlier documentation work matters so much.

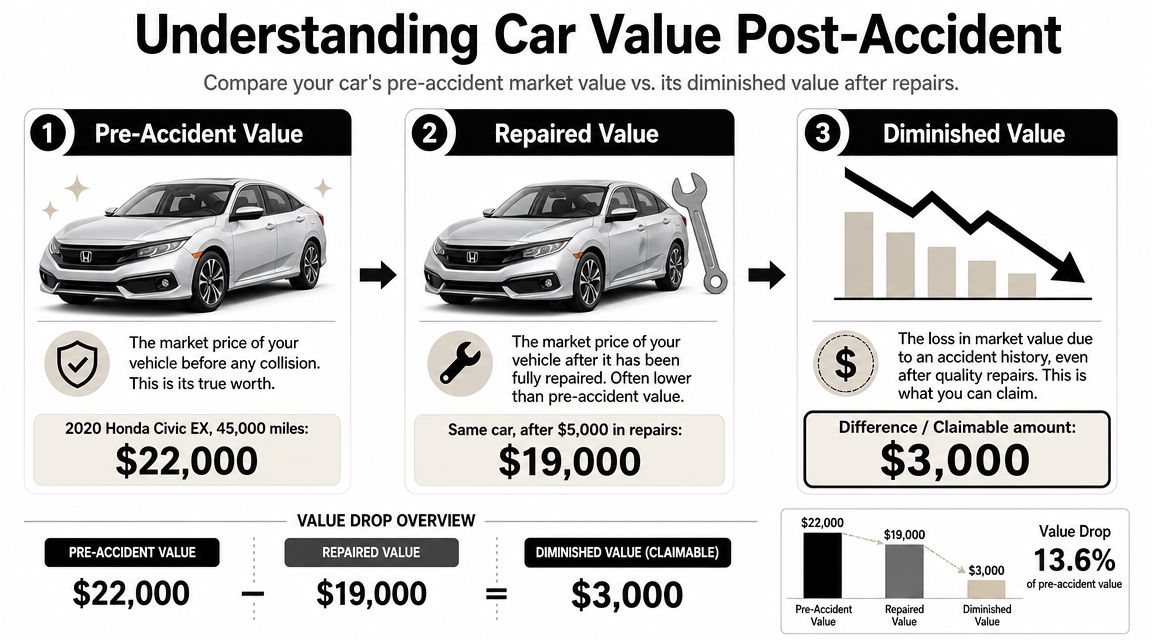

Protect Your Car's Value from a Lowball Settlement

Most drivers get blindsided. They assume the insurer's number is objective because it came from software, a report, or a desk adjuster with a template. It isn't necessarily objective. It's just the insurer's opening position.

Fort Worth's 2024 crash severity profile included 106 fatal crashes and 391 suspected serious injuries, according to TxDOT's 2024 city crash table. In a high-severity environment, carriers often rely on automated valuation models to process claims quickly. That's exactly why independent appraisals matter when a total loss offer looks thin.

Two value problems drivers confuse

A repaired car and a totaled car create different claim fights.

| Claim type | What the dispute is really about | What supports your side |

|---|---|---|

| Diminished value | Your vehicle is repaired, but the market now values it less because it has an accident history | Pre-loss condition photos, repair documentation, trim and options, severity of damage |

| Total loss | The insurer says the vehicle isn't worth repairing and offers Actual Cash Value | Comparable local vehicles, condition proof, mileage context, options, recent maintenance and upgrades |

If your car is repairable, don't let anyone tell you the issue ends when the body shop finishes. A repaired vehicle can still suffer a market stigma. Buyers and dealers care about accident history.

If your car is totaled, inspect the insurer's valuation line by line. Look for bad comparable vehicles, missing options, wrong trim, condition downgrades, or listings from irrelevant markets.

Why insurer numbers come in low

I've seen the same failure points repeatedly:

- Bad comparables: wrong trim, wrong equipment, wrong geography.

- Condition downgrades: the report assumes average or rough pre-loss condition when the car was clean.

- Missing value adds: recent tires, major service, factory packages, and uncommon options get overlooked.

- Compressed timelines: the file gets processed fast, and nobody stops to ask whether the number matches the actual replacement market.

That's why your evidence package matters so much. The scene photos, undamaged panel photos, maintenance records, and repair documentation all support value.

Don't ignore cosmetic condition evidence

Even smaller condition details can matter when valuing a car. If your vehicle had exceptional paint, corrected finish quality, or unusually strong cosmetic presentation before the crash, that supports a better pre-loss condition argument. This explainer on the paint correction process and cost is useful background because appearance condition can affect how a vehicle compares against average market listings.

The insurer's valuation is not the final word. It's a draft you're allowed to challenge.

If the offer still doesn't make sense, get help from someone who knows how to read valuation reports and compare them against the actual market. A strong place to start is understanding the role of independent car appraisers. A proper appraisal can remove a lot of guesswork and put real evidence back into the negotiation.

Essential Fort Worth Accident Resource List

A crash scrambles your memory fast. Save the contacts below before you need them. The right call in the first hour can protect your safety, preserve the paper trail, and stop small reporting mistakes from hurting a total loss or diminished value claim later.

Fort Worth Post-Accident Contact Sheet

| Resource | Contact Information / Link | Why it matters |

|---|---|---|

| Fort Worth Police non-emergency | Look up the current non-emergency line through the City of Fort Worth Police Department directory | Use it for follow-up when 911 is not appropriate, especially if you need officer information or report guidance |

| Texas crash report access | TxDOT Crash Report Online Purchase System | Get the official report as soon as it posts. You will use it to confirm parties, location, and report details before the insurer frames the file their way |

| Fort Worth traffic incident information | Fort Worth current traffic accidents dataset, as noted earlier | Use it to check whether an incident is still showing as active or recently cleared |

| City towing oversight | Search the City of Fort Worth for towing and transportation board resources | Check local towing oversight information before you agree to storage, release, or tow-related charges you do not understand |

| Your insurer claim department | Use the number on your ID card or insurer app | Open the claim promptly, give basic facts only, and save the claim number, adjuster name, and call time |

Create a phone note called “Crash File.” Paste in the links, claim number, tow yard name, body shop contact, and the date you requested the police report.

That note becomes your control panel. It keeps you from missing deadlines, losing documents, or accepting a weak valuation because the file got ahead of you.

Frequently Asked Questions After a Fort Worth Accident

Fort Worth logged 13,401 total motor vehicle accidents in 2022, averaging about 37 crashes per day, according to Fort Worth accident statistics for 2022. That consistency is why these questions come up over and over.

What if the other driver is uninsured or underinsured

Open a claim with your own carrier right away and ask what coverages may apply under your policy. Keep your documentation tight. Fault evidence, photos, and witness information matter even more when coverage is limited and every dispute gets sharper.

Do I have to use the body shop the insurer suggests

No. You can choose your repair shop. The insurer may recommend a network shop, but you are not required to hand over control just because they prefer a vendor relationship. Pick a shop that documents repairs well and communicates clearly.

What's the difference between diminished value and total loss

A diminished value claim applies when the car is repaired but worth less afterward because of the accident history. A total loss claim applies when the insurer decides the vehicle should be valued and paid rather than repaired.

Those are separate issues. Don't let anyone blur them.

What if symptoms show up later

Get evaluated as soon as symptoms appear and tell the provider they began after the collision. Delayed pain is common. Delayed documentation is a problem.

What if the insurer's valuation seems wrong

Challenge it. Ask for the valuation report, read the comparable vehicles, verify trim and options, and look for errors. If the report doesn't reflect your car or your local market, say so in writing and support it with records and photos.

Should I accept the first offer

Not if you don't understand what the offer leaves out. Fast settlements often favor file closure, not accuracy. Review the numbers before you sign anything.

If your insurer is lowballing a total loss or ignoring diminished value after a Fort Worth crash, Total Loss Northwest is worth contacting. They specialize in independent auto appraisals and appraisal clause disputes, which is exactly what you need when the carrier's number doesn't match the actual market value.