If you searched for a car accident in Fort Worth yesterday, you're probably not looking for broad safety tips. You're trying to figure out what happens next. Your car may be at a tow yard. Your neck may feel worse today than it did at the scene. The insurance company may already be calling.

That's the part most articles miss.

The news tells you where the crash happened and whether traffic backed up. It usually doesn't tell you how to protect your health, your paperwork, or the value of your vehicle. And if your car is newer, high-value, custom, or worth more to you than the insurer wants to admit, the true fight often starts after the wreck is over.

Understanding the Recent Fort Worth Accident Context

A recent Fort Worth crash reported as happening “yesterday” on westbound I-30 involved at least five vehicles and one passenger death, according to CBS Texas coverage of the I-30 Fort Worth crash. If that's the event you were searching for, you're not overreacting by looking for answers. A multi-vehicle freeway crash changes lives fast, even when the first reports sound brief.

Fort Worth drivers deal with a lot more collision exposure than many people realize. Fort Worth recorded 12,865 total traffic crashes in 2024, which averages about 35 crashes per day, and those crashes led to 116 deaths and more than 6,600 injuries. The same source says Fort Worth ranked fourth among Texas cities for total crashes in 2024, behind Houston, Dallas, and El Paso, which puts any one-day wreck inside a very busy urban traffic environment. Those figures come from Fort Worth crash statistics summarized here.

What that means for you

If your wreck happened yesterday, you're not dealing with some rare bureaucratic event. Police, tow operators, body shops, adjusters, and claims departments all have routines for this. That's the good news.

The bad news is that routine doesn't always work in your favor.

Insurance companies process crashes every day. You probably don't. That experience gap matters. They know how to move a claim toward a fast close. You need to know how to keep that from becoming a cheap close.

Practical rule: Treat the first version of your claim as incomplete. Early reports are for emergency response, not for proving the full value of your injury claim or vehicle loss.

When a fatal crash leaves unanswered questions

If your family is dealing with a death after a Fort Worth wreck, there may be medical and forensic questions that standard public reporting won't answer. In those situations, resources like Texas Autopsy Services in Tarrant County can help families understand independent post-loss options.

For the rest of us, the immediate concern is simpler and more urgent. Protect your body, your words, and your car's value before the claim starts drifting in the wrong direction. If you want a sense of how the claims timeline can unfold after a wreck, this guide on the average time for car accident settlement is a useful baseline.

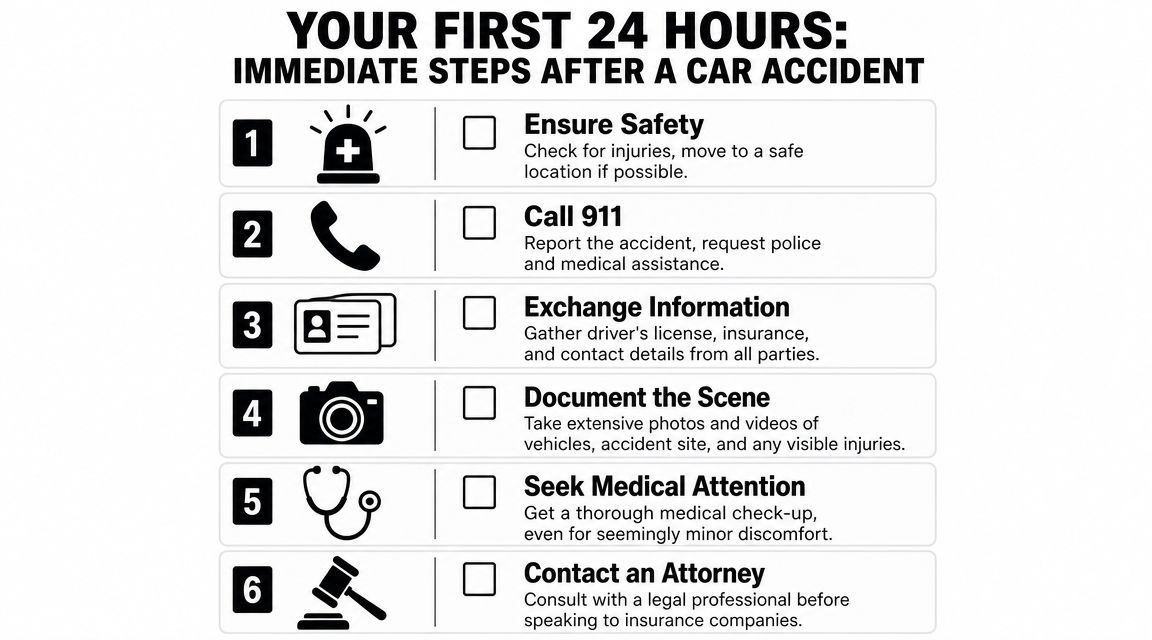

Your First 24 Hours What to Do Immediately

The first day matters more than many realize. Not because you need a perfect claim file in a few hours, but because the mistakes people make in the first day keep costing them weeks later.

Start with safety and medical care. Then control communication.

Your non-negotiable checklist

Get checked by a medical professional.

Even if you walked away. Even if you think you're fine. Pain often shows up later, and gaps in treatment give insurers room to say you weren't hurt.Report the crash to your insurer.

Give the basic facts. Time, place, vehicles involved, police response, visible damage. Keep it factual.Do not give the other insurer a recorded statement right away.

Their job is to evaluate exposure. Your off-the-cuff wording can get used against you.Preserve the vehicle before repairs start.

Take photos first. Lots of them. Damage looks different before teardown than after.Track every out-of-pocket cost immediately.

Towing, rides, meds, rental, parking, co-pays. Small expenses become annoying disputes when they aren't documented.Write down what happened while it's still fresh.

Lane position, traffic flow, what you saw, what you heard, what the other driver said.

A more general post-crash checklist like Oldham Law's Florida accident guide is worth reviewing because the practical first steps are similar no matter where the crash happened.

Here's a quick visual summary you can follow.

What to say and what not to say

Use short sentences with insurers. “I was involved in a crash yesterday in Fort Worth.” “Police responded.” “My vehicle is not drivable.” “I'm seeking medical evaluation.” That's enough to open the claim.

Don't guess about speed. Don't speculate about fault. Don't say “I'm okay” if you haven't been examined. Don't minimize damage just because the bumper is still attached.

If you're hurt, say you're being evaluated. If you don't know, say you don't know. A clean factual record beats a polite guess every time.

If you need a broader walk-through after the immediate chaos settles, this guide on steps after a car accident is a good next read.

How to Get Your Official Fort Worth Accident Report

Getting the report sounds simple until you try to do it while juggling a body shop, a rental, and a sore back. Here's the straightforward version.

First, know that the officer at the scene may give you a report number or incident number. That is not always the same thing as the final Texas Peace Officer's Crash Report, commonly called the CR-3. The CR-3 is the document insurers, attorneys, and claim handlers usually care about.

Why report delays happen

Fort Worth and Tarrant County handle a heavy crash load. In 2022, Fort Worth had 13,401 total motor vehicle accidents, and Tarrant County recorded 28,997, according to Stephens Law's summary of Fort Worth and Tarrant County crash statistics. With that kind of volume, the reporting system is standardized, but it can still take time for the final paperwork to become available.

That delay is normal. Don't panic if it isn't ready the next morning.

The practical way to request it

Use this sequence:

- Start with the information you already have. Bring the date, approximate time, location, names of drivers, and the responding agency if you know it.

- Check with the Fort Worth Police Department records process. If city police handled the crash, their records channel may help you locate the case reference tied to the incident.

- Look for the CR-3 through the Texas system. If the report has been filed into the state system, that's often the version people need for claims handling.

- Save the report exactly as received. Don't mark it up. Keep one clean copy as your master version.

Why you shouldn't wait too long

The crash report won't tell the whole story, but it gives your claim a backbone. It identifies parties, vehicles, location, and the investigating officer's initial observations. If there's an error, you want to catch it early while memories are still fresh and supporting evidence is easier to gather.

Also, don't make the mistake of assuming the insurer already has the best copy. Sometimes they do. Sometimes they don't. You want your own file, your own documents, and your own timeline.

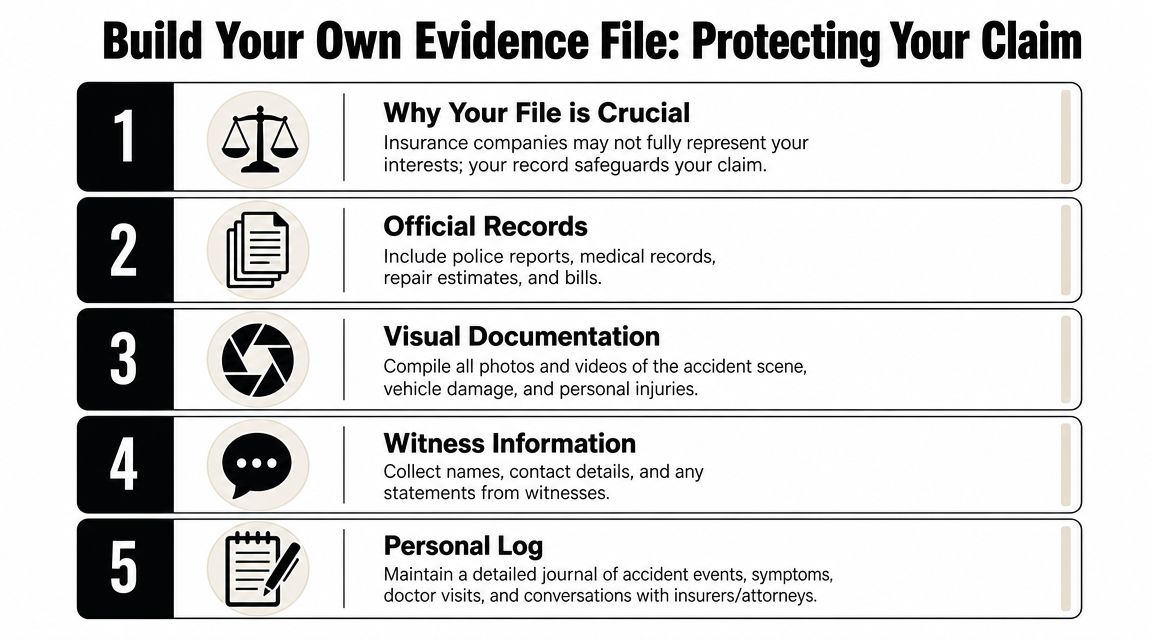

Building Your Own Evidence File to Protect Your Claim

The insurance company's file is not your file.

That distinction matters. Their file is built to evaluate what they owe. Your file should prove what you lost. If you leave the record-building to the adjuster, don't act surprised when important details never make it into the valuation.

What belongs in your file

Create one folder, physical or digital, and keep everything there. Not some of it. Everything.

Scene proof

Photos of every vehicle, wide shots of the roadway, lane markings, debris, skid marks, weather, traffic signals, and any obstructed views.Vehicle damage records

Shoot every corner of your car, the VIN sticker, wheel damage, interior damage, deployed airbags, warning lights, and under-hood damage if visible.Medical paperwork

Discharge instructions, visit summaries, imaging referrals, prescriptions, work restrictions, and every bill you receive.Money spent because of the wreck

Towing invoices, storage charges, rental receipts, ride-share trips, pharmacy receipts, and replacement child seat purchases if relevant.Communication logs

Save emails, voicemails, claim numbers, adjuster names, and the date and time of every call.

The journal people skip

Keep a simple daily log. Nothing fancy. A note on your phone works.

Write down how you feel when you wake up, where it hurts, what activities you can't do, what appointments you had, and whether symptoms got better or worse. If the crash affected your sleep, work routine, lifting, driving, or childcare, note that too.

That journal does two jobs. It helps your doctor see the pattern, and it keeps your claim from turning into a vague memory by the time settlement talks start.

The best evidence is boring. Dates, names, receipts, photos, and short notes beat emotional summaries every time.

Photos need progression, not just one day

Take photos more than once.

A lot of people document the scene and stop there. Bad move. Damage assessment evolves during teardown. Bruising can appear later. Swelling changes. Repair shops discover hidden structural issues after disassembly. If your car is repaired, keep before, during, and after photos.

Use this quick reference table to keep your file complete:

| Item | Why it matters | When to save it |

|---|---|---|

| Police or incident info | Anchors the timeline | Same day |

| Vehicle photos | Preserves visible damage | Same day and during repairs |

| Medical records | Connects symptoms to treatment | After every visit |

| Receipts | Supports reimbursement | As each expense happens |

| Call log | Prevents “we never said that” disputes | After every insurer call |

If your wreck was a car accident in Fort Worth yesterday, start the file today. Memory fades fast. Digital evidence disappears faster when phones break, apps auto-delete, or repair shops move vehicles around.

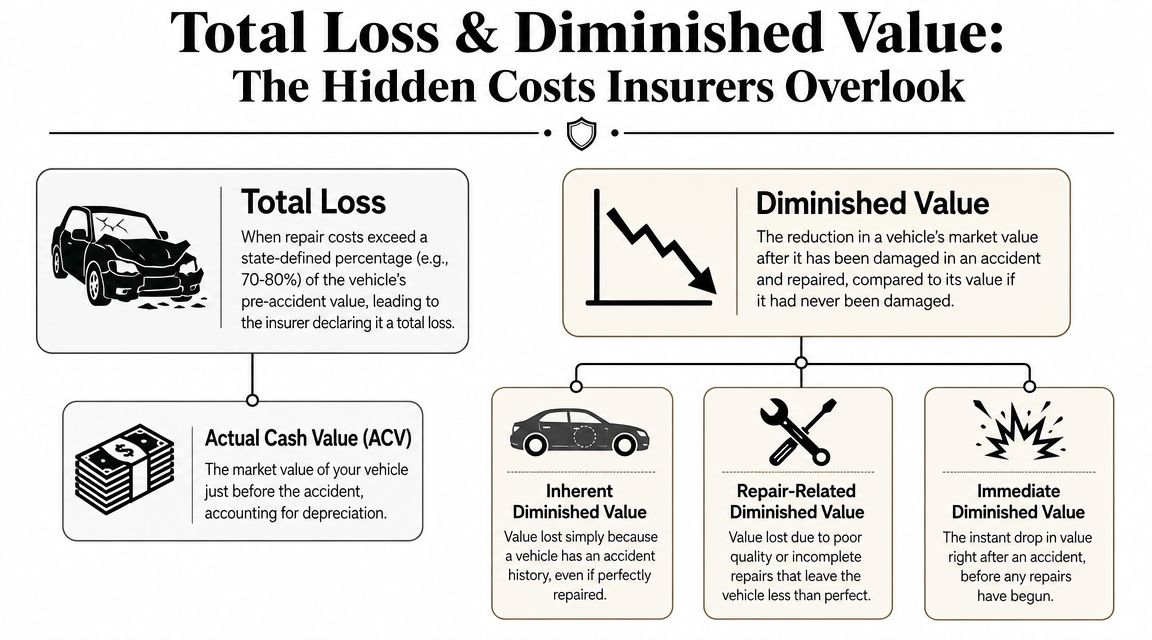

Total Loss and Diminished Value The Money Insurers Skip

In this scenario, many people lose real money without realizing it.

If your car is badly damaged, the insurer may call it a total loss. That means they decide the vehicle should be valued and paid out rather than repaired. The fight then becomes the car's actual cash value, which is supposed to reflect the vehicle's pre-accident market value.

If the car is repaired instead, you may still have a separate problem. That problem is diminished value.

Why diminished value is real

Two identical used cars sit for sale. Same year, same trim, same mileage, same color. One has a clean history. The other had a significant collision and was repaired.

Which one sells easier?

The clean-history car. Almost every time.

That gap is diminished value. Even excellent repairs don't erase accident history from vehicle databases or buyer concern. Buyers care. Dealers care. Appraisers care. Trade-in managers care. You should care too.

Total loss fights are usually valuation fights

When insurers total a car, owners often focus on whether the vehicle can be repaired. That's not usually the main issue. The main issue is whether the insurer's value is too low.

Their valuation may lean on internal systems, comparable vehicles that aren't suitable for comparison, condition assumptions you'd never agree with, or option lists that miss features your car had. If the offer feels light, there's a reason to slow down and inspect the basis for it.

Here's the cleaner way to understand:

- If the car is totaled, challenge the market value if the offer doesn't match your vehicle.

- If the car is repaired, look at whether the crash history reduced resale or trade-in value.

- If the car is special, meaning newer, luxury, collector, rare trim, custom, or exceptionally clean, the risk of a bad valuation gets worse.

The information gap is real

A lot of public crash coverage stops at injuries, closures, and fault investigation. That's useful in the moment, but it leaves drivers exposed on the money side. As noted by TxDOT's Fort Worth district incident context and consumer guidance gap, there's a meaningful lack of plain-English guidance around total loss and diminished value claims, even though those issues can cost owners thousands.

That gap is exactly why so many people accept a bad number too early.

A repaired car can still be worth less. A totaled car can still be undervalued. Those are separate problems, and both deserve scrutiny.

The trap to avoid

Don't assume the first number is the fair number.

Adjusters often sound confident because they work inside a system. Confidence is not proof. Ask for the valuation report. Review the comparables. Check trim, mileage, condition, prior options, aftermarket equipment, and local market fit. If anything is off, the entire settlement figure may be off.

When to Call an Independent Appraiser for Your Vehicle

You don't need an independent appraiser for every fender bender. You do need one when the value dispute is big enough to matter.

Call one when the insurer's number doesn't match reality, when the car is hard to value, or when the claim involves diminished value that nobody wants to discuss clearly. Independent appraisers work for the vehicle owner, not the carrier, and that changes the conversation fast.

Clear signs it's time

Consider getting an independent appraisal if any of these apply:

- Your vehicle is late-model or high-value. Newer vehicles and premium trims often suffer larger real-world value disputes after a crash.

- The damage is substantial. Bigger repairs usually create bigger arguments over post-repair value or total loss value.

- The offer feels low compared with the actual market. If you've looked at comparable vehicles and the insurer's figure doesn't line up, trust that instinct and verify it.

- Your car is custom, collector, or unusually clean. Standard valuation systems often miss what makes these vehicles worth more.

- You're invoking the appraisal clause. Many policies include an appraisal clause that gives both sides a formal path to resolve value disagreements.

Don't wait until you've boxed yourself in

The worst time to question value is after you've signed releases, transferred title, or let the repair process wipe out important evidence. Push back early. Ask for documentation. Preserve photos. Keep your estimate set. If needed, consult an independent car appraiser before the claim hardens into a number the insurer treats as final.

You don't need to be combative. You need to be organized, skeptical, and willing to challenge a weak valuation with better evidence.

If your insurer is lowballing your total loss or ignoring diminished value, Total Loss Northwest helps vehicle owners fight for a fair number through independent appraisals and appraisal clause support. If your claim value doesn't add up, get the valuation reviewed before you accept it.