Most car accident lawyers charge nothing upfront and work on a contingency fee, usually taking about one-third of the settlement, with common ranges around 33.3% to 40%. If your case settles early, the fee is often near the lower end. If it requires litigation or trial, the percentage usually rises.

You're probably here because the insurance company already made an offer and it feels low. Or you're staring at repair estimates, medical bills, missed work, and a damaged car, wondering whether hiring a lawyer will help or just take another chunk of money out of your pocket.

That's the right question.

Many inquire, “How much does a car accident lawyer cost?” The better question is, “Will hiring a lawyer increase what I take home?” Those are not the same thing. A lawyer can be a smart financial move in an injury claim and a bad economic fit for a property-damage-only dispute. If you don't separate those two situations, you can make an expensive mistake.

The Real Question After a Car Accident

The call usually comes fast. The insurance adjuster sounds confident, gives you a number, and acts like the matter is almost finished. Meanwhile, you are dealing with doctor visits, missed work, a wrecked car, or all three. The price question shows up right there: is hiring help going to leave you with more money, or just another bill attached to the crash?

The first cost concern usually misses the bigger issue

A lot of drivers focus on what a lawyer charges before they look at what the claim is worth. That is backward.

The smart financial question is whether professional help increases your take-home amount after fees, costs, and medical bills are paid. In injury cases, the answer is often yes because the dispute is not just about one repair estimate. It can involve treatment, lost income, pain, future care, and arguments over fault. The American Bar Association explains that personal injury lawyers commonly use contingency fees, which is why many injured clients can get legal help without paying upfront in this overview of contingency fees.

If your injuries are still developing, get proper care first and keep records. Resources like Highbar Physical Therapy for car accident injuries can help you understand the kinds of treatment issues that often affect both recovery and claim value.

A body injury claim and a car value dispute need different tools

Here, many people waste money.

If the case involves physical injuries, ongoing care, wage loss, or a fight over who caused the crash, a lawyer can earn the fee by increasing the value of the claim and protecting you from a bad settlement. If the dispute is only about property damage, such as a total loss valuation or diminished value claim, paying a lawyer a percentage may cut too significantly into the result. In that situation, an independent appraiser is often the better buy because the issue is valuation, not litigation strategy.

Use that distinction. It saves money and prevents the common mistake of hiring the wrong kind of help for the wrong kind of claim.

How Car Accident Lawyers Get Paid

You call a lawyer after a crash and hear, “You pay nothing up front.” Good. But that still leaves the question that matters. How does the lawyer get paid, and how much of your settlement will you keep?

For car accident cases, the usual setup is a contingency fee. The lawyer gets a percentage of the money recovered through a settlement or verdict. If there is no recovery, there is usually no attorney fee. The Cornell Legal Information Institute explains the basic difference between hourly and contingency billing in its overview of attorney's fees.

Hourly billing, flat fees, and retainers exist, but they are far less common for injury claims tied to a car accident. Those models show up more often in limited legal tasks, unusual disputes, or matters outside standard personal injury work.

The other fee types you may hear about

Here is the practical comparison.

| Fee Type | How It Works | Best For |

|---|---|---|

| Contingency fee | Lawyer is paid from a settlement or verdict if the case succeeds | Personal injury claims after a car accident |

| Hourly rate | Client pays for time spent on the matter | Limited-scope legal work or unusual disputes |

| Flat fee | One set price for a defined task | Simple document review or a narrow service |

| Retainer | Client deposits money upfront and legal work is billed against it | Ongoing legal matters outside typical injury claims |

For an injury claim, contingency is usually the right model because it removes the up-front cash barrier and puts some risk on the law firm. That matters if you are already dealing with medical bills, missed work, and pressure from the insurance company.

The catch is simple. A contingency fee tells you how the lawyer gets paid. It does not tell you what your net recovery will be.

That distinction matters. A lawyer can be worth the fee in a body injury case because legal work may increase the total recovery enough to leave you with more money after fees, costs, and liens. In a property-damage-only dispute, that math often breaks the other way. If the fight is over total loss value or diminished value, an independent appraiser is often the cheaper and smarter hire.

Ask this early: Is the stated percentage the full fee arrangement, or will case costs, medical liens, and other deductions also come out of my share?

That answer matters more than the slogan on the firm's homepage.

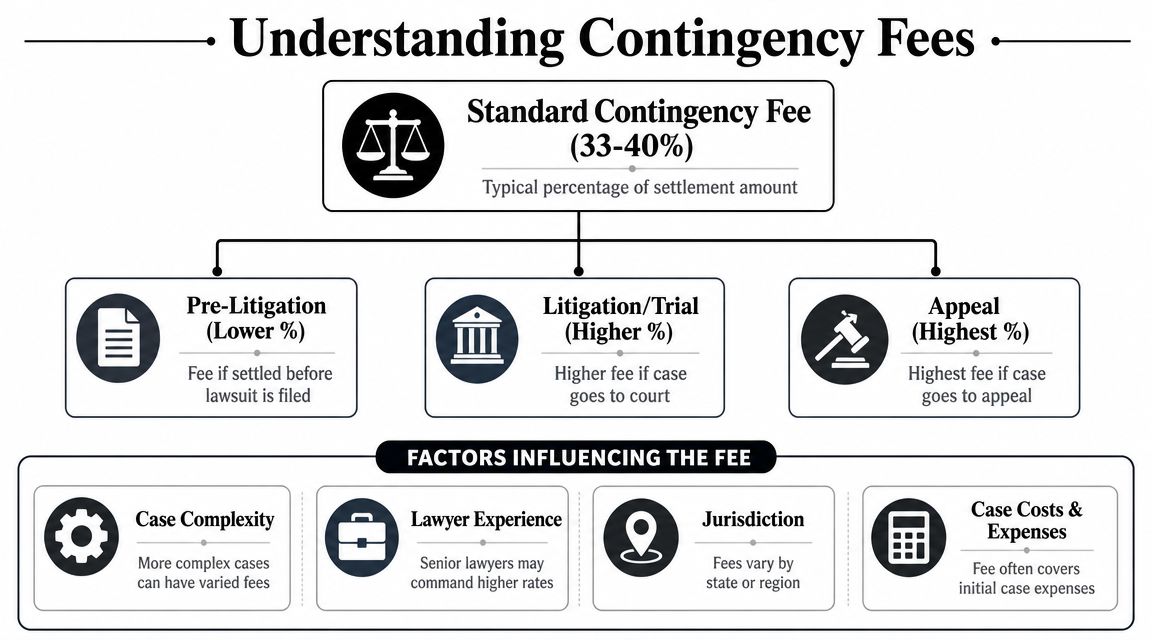

Decoding the Standard Contingency Fee

A contingency fee isn't one fixed number. It's a range, and that range tells you how much work the lawyer expects the case to require.

In major personal-injury markets, the benchmark is roughly 30% to 40% of the recovery. A one-third fee is common when a case settles before litigation, while a higher percentage is typical if the case moves into litigation or trial, according to this breakdown of car accident lawyer fees.

Why the percentage goes up

The fee rises when the work gets heavier and the risk goes up.

A pre-litigation case may involve gathering records, proving damages, and negotiating with the insurer. A litigated case can require filing suit, written discovery, depositions, expert coordination, motion practice, and trial prep. That means more lawyer time, more staff time, and more money advanced before the firm sees a return.

Here's the clean way to consider this:

- Early settlement cases: Often near the lower end of the range

- Lawsuit filed: Often higher because the workload expands

- Trial-bound disputes: Usually at the upper end because the firm is taking on more risk and labor

The fee is a risk-adjusted price

This is the part many clients miss. Your legal bill in an accident case usually isn't a simple service fee. It's a risk-adjusted share of the gross recovery.

That matters because some claims are worth fighting through hard resistance from the insurer, and some aren't. If the only disputed issue is a modest vehicle valuation number, giving up a large slice of the result may not make economic sense. If the claim includes injury, treatment, wage loss, and uncertainty over fault, contingency pricing often makes much more sense.

The fee percentage is not just a price tag. It's a signal about how hard the lawyer expects the fight to be.

When you compare lawyers, don't shop on percentage alone. Ask what triggers an increase, when it applies, and whether the contract states it clearly in writing.

The Hidden Costs Beyond the Percentage

The biggest misunderstanding in this entire topic is simple: people hear “one-third” and assume that's the whole cost.

It usually isn't.

Case expenses are often separate from the lawyer's percentage. Those costs are commonly advanced by the firm and then deducted from the recovery later. According to this guide on accident lawyer costs and expenses, they can include court filing fees, expert-witness retainers, deposition costs, and medical-record retrieval fees.

What can get deducted besides the fee

These are the charges that often surprise clients at the end:

- Court-related charges: Filing fees and other litigation expenses tied to the lawsuit process

- Experts: Accident reconstruction professionals or other specialists when liability or damages are disputed

- Depositions: Costs for taking testimony and getting transcripts

- Records and reports: Medical-record retrieval, police reports, and similar documentation

A straightforward claim that settles early may keep these costs modest. A disputed case can generate far more deductions because proving the claim takes more work and more outside help.

Why this matters for net recovery

The gross settlement is not your payout.

Your actual recovery is reduced by the attorney fee, then by case expenses, and in many cases by medical liens or reimbursement claims. That's why a fee quote by itself doesn't tell you enough.

If you're comparing options on a vehicle-only dispute, you should also compare them against non-lawyer solutions. For example, if your issue is strictly valuation, it helps to understand car appraisal cost before agreeing to hand over a percentage of the entire recovery.

The contract matters more than the pitch

Don't accept vague language. You want a written fee agreement that clearly separates:

- Attorney percentage

- Case expenses

- How those expenses are deducted

- Whether liens or reimbursements may also reduce your check

A lot of firms market the easy part. “No fee unless you win” sounds reassuring. It is reassuring. But it doesn't answer the question you care about most, which is how much money lands in your bank account when everything is over.

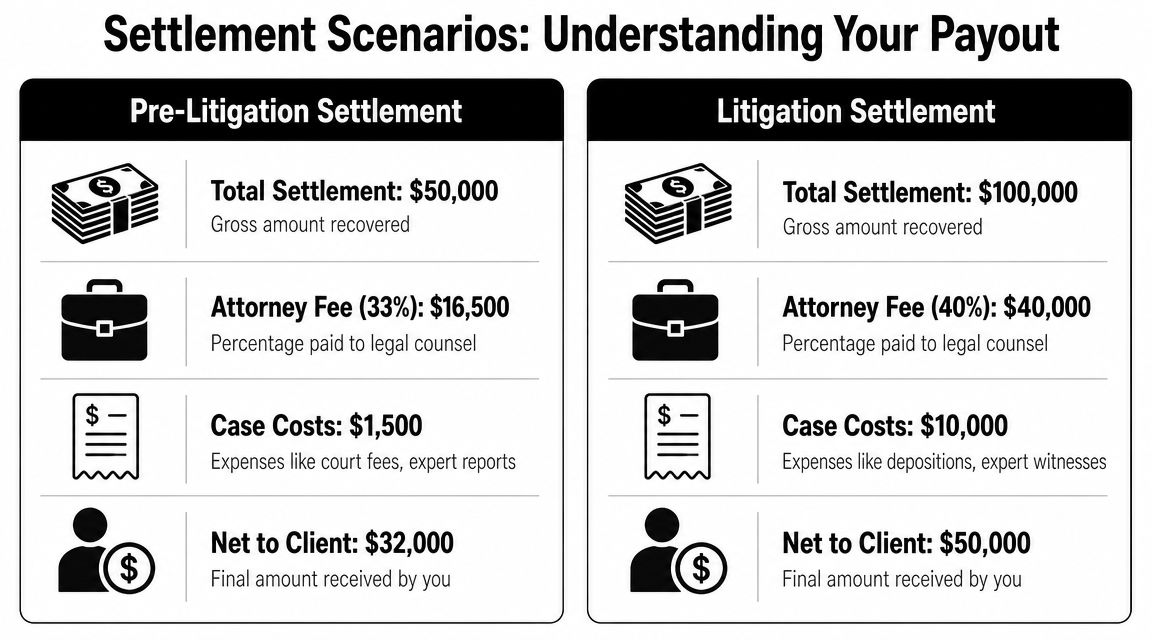

Putting It All Together Sample Scenarios

A fee percentage means nothing until you run the full math.

A client who signs a one-third contingency agreement can still walk away unhappy if the case is small, the expenses are high, or the dispute never should have been handed to a lawyer in the first place. The only number that matters is your net recovery, the amount left after the fee, case costs, and any medical paybacks.

The examples below show how to judge the economics the right way.

Scenario one with a smaller settlement

Start with a smaller injury claim that settles for $30,000. A one-third fee takes about $10,000 off the top. Then come the other deductions. Filing costs may be zero if the case settles early, or higher if the claim drags on. Medical reimbursements can shrink the final check again. The client's real payout is whatever remains after all of that.

This kind of case can still justify hiring a lawyer. If the attorney pushed the insurer from a weak offer to a fair injury settlement, the client may still come out ahead even after the fee.

But here is the hard truth. If the dispute is only about the value of the car, a lawyer often costs too much relative to the amount in play. In a property-damage-only claim such as total loss or diminished value, paying a percentage of the recovery can be the wrong financial move.

A better benchmark is whether a lower-cost valuation tool or expert could solve the problem without taking a share of the entire claim. The timeline matters too, because a long claim can increase pressure to accept less. This guide on how long it can take to settle a car accident claim helps frame that tradeoff.

Scenario two with a larger recovery

Now look at a larger case. Cornell Law School's Legal Information Institute explains that contingency fees are commonly set as a percentage of the recovery, which means a bigger settlement can produce a much larger attorney fee even before case expenses are added, as described in its overview of contingent fee arrangements.

That usually makes more sense in a serious injury case than in a vehicle-only dispute. Large medical bills, disputed liability, future treatment, wage loss, and the risk of litigation can all justify paying for legal work that increases the value of the claim.

The key question stays the same. Did the lawyer increase the client's take-home amount enough to outweigh the fee and costs?

For a visual explanation of how settlements get divided, this short video is useful:

The right takeaway

Judge the price by the result, not the percentage.

If a lawyer increases your net recovery on an injury claim, the fee is justified. If your problem is limited to proving what the car was worth, an independent appraiser is often the smarter financial choice.

That is the standard to use.

How to Discuss Fees with a Potential Lawyer

Clients often walk into a consultation trying to impress the lawyer or prove they have a good case. That's backward. You're interviewing them too.

You need direct answers about money, process, and timing. If a lawyer gets slippery when the conversation turns to fees, move on.

Questions worth asking word for word

Use this list and don't soften it:

- What is your contingency fee percentage? Ask for the exact percentage and whether it changes if a lawsuit gets filed.

- When does your fee increase? You want the trigger spelled out, not described vaguely.

- What case expenses are separate from your fee? Make them name the categories.

- How are those costs deducted from the settlement? This affects your net recovery.

- Are medical liens handled as part of your representation? If yes, ask how that affects the final disbursement.

- Can you walk me through a sample settlement breakdown? If they can't explain the math clearly, that's a problem.

- How long might a case like mine take? Timing affects strategy, advantage, and your own financial planning. This overview of how long it can take to settle a car accident claim helps frame that conversation.

What a good answer sounds like

A good lawyer doesn't hide behind legal jargon. They explain the fee in plain English, tell you what expenses may be advanced, and show you how the payout is distributed.

A bad answer sounds polished but vague. You'll hear lots of confidence and very little detail.

Red flags you shouldn't ignore

- They rush the fee agreement

- They won't discuss deductions clearly

- They avoid giving example math

- They treat every case like it fits the same template

“What do I take home if the case resolves well?” is the question that cuts through the sales pitch.

If they answer that cleanly, keep talking. If they don't, keep shopping.

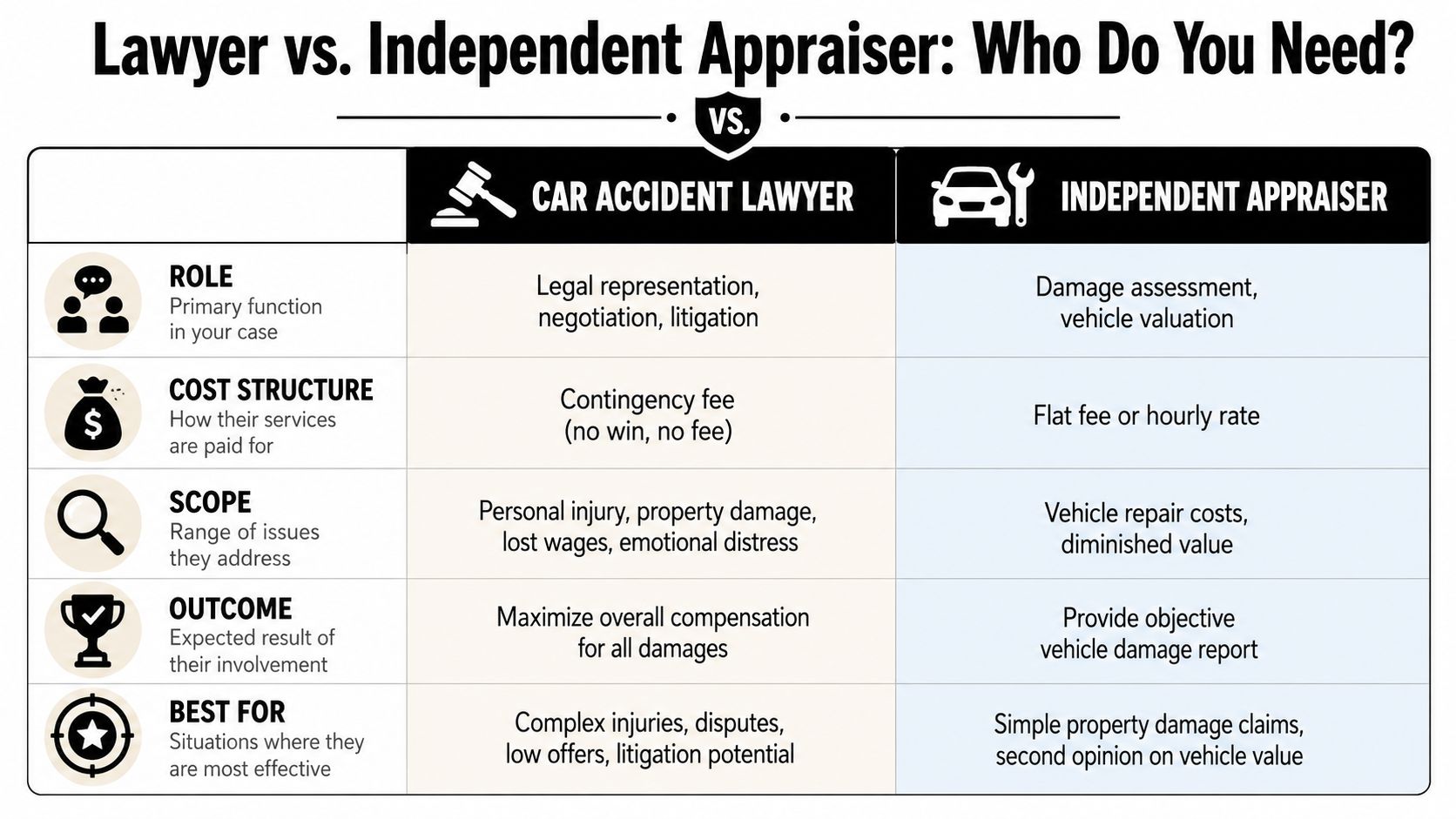

Next Steps Lawyer vs Independent Appraiser

A lot of drivers make the wrong hire in this situation.

A lawyer is often the right call when the crash caused physical injuries, there's a real dispute over fault, or the claim involves broader damages like treatment and lost income. In those situations, legal influence matters. Negotiation strategy matters. The possibility of litigation matters.

An independent appraiser is often the better economic choice when the dispute is only about the vehicle.

When a lawyer earns the fee

Hire a lawyer when your claim looks like this:

- You were injured: The case involves medical treatment, pain, disruption, or wage loss

- Fault is disputed: The insurer is trying to shift blame or downplay liability

- The claim is complex: Multiple parties, serious damages, or litigation risk are in play

- The insurer is fighting hard across the board: Not just on vehicle value, but on the full claim

In those cases, contingency pricing often makes sense because the lawyer is pursuing a larger and more complicated recovery.

When an appraiser is the smarter first move

Start with an independent appraiser when your problem looks like this:

- Total loss dispute: The insurer undervalued your vehicle

- Diminished value claim: The car lost market value after repairs and the insurer is minimizing it

- No meaningful injury claim: The issue is economic damage to the vehicle, not bodily injury

- You need an objective valuation report: The fight is about what the car is worth, not courtroom advantage

That's especially true if you own a high-value, collector, custom, or unusually optioned vehicle. In those cases, a professional valuation can be more useful than legal posturing.

If you need that kind of help, it's worth understanding what independent car appraisers do before you sign a contingency agreement that may swallow a large share of a property-only recovery.

My blunt advice

Don't hire a lawyer just because the insurance company annoyed you. Hire a lawyer when the claim requires legal pressure.

If the fight is only about the number attached to your car, start by fixing the valuation problem. That approach is often cleaner, faster, and more cost-effective than handing over a percentage of the result.

Your goal isn't to hire the most impressive professional. Your goal is to keep the most money.

If your insurer is lowballing a total loss or diminished value claim, Total Loss Northwest gives you a better starting point than a generic legal consultation. They specialize in independent vehicle appraisals for Oregon and Washington owners, with diminished value support in all 50 states, and they focus on the number that matters most in a property-damage dispute: what your vehicle is worth.