The email lands fast. The adjuster says the car accident settlement form is routine, the offer is ready, and signing will “move things along.”

Slow down.

That form is usually the moment people give away the most money. Not because they agreed to a bad number on purpose, but because they treated the document like paperwork instead of what it is: the final checkpoint where injury claims, vehicle value, and future rights all get locked in. If your car was repaired, totaled, customized, or worth more than the insurer's software says, this is the point where your power to negotiate either survives or disappears.

I'm going to be blunt. If you sign first and ask questions later, you've already lost your best negotiating position.

What Is a Car Accident Settlement Form Really?

A car accident settlement form is usually a release. The insurer may call it a settlement agreement, release of claims, or release of liability. Different label, same function. You sign it, they pay, and your claim closes.

That sounds clean and simple. It isn't.

This form is the document that usually ends your right to ask for more money later. That matters because car accident claims vary widely. The average collision-related car accident claim was $5,992 for property damage alone, while claims involving bodily injuries reached an average of $24,211, according to average car accident settlement data. Once you sign, those figures stop being general market context and start becoming your permanent outcome.

What the form usually does

It's common to focus on the dollar figure and ignore the language around it. That's backwards. The legal language is the part with real teeth.

A settlement form often covers:

- Your injury claim if you were hurt

- Your property damage claim for the vehicle

- Rental, towing, and related losses tied to the crash

- Any future claim tied to the same accident if the release is broad enough

Why this matters for your car

If your vehicle was repaired, the form may close out more than the repair bill. It can also wipe out your ability to later argue that the car lost market value because it now carries accident history.

If your vehicle was declared a total loss, the same form can finalize a value that came from software, not from a true market review. Once that release is signed, the fight over what the car was worth is usually over.

Practical rule: Never treat a settlement form like a receipt. It's a contract that can end both known claims and claims you haven't fully identified yet.

The right mindset before you read it

Read the form with one question in mind: What rights am I giving up that aren't fully paid yet?

That includes obvious items like medical bills. It also includes less obvious items, especially for vehicle owners:

| Issue | What people assume | What the form often does |

|---|---|---|

| Vehicle repairs | “This just pays the body shop” | It may close all vehicle-related claims |

| Total loss value | “I can challenge the number later” | You may waive that right |

| Diminished value | “I'll deal with resale loss later” | You may release it now |

| Future problems | “I'll reopen the claim if needed” | Usually not after signing |

You don't need panic. You need discipline. The right response to a settlement form is not “Where do I sign?” It's “What exactly am I releasing, and has every part of this claim been valued correctly first?”

Key Clauses to Scrutinize in Your Settlement Form

The most expensive words in a car accident settlement form are often the ones people skim.

Insurers write these forms to close files. You need to read them to protect value. If a sentence looks broad, assume it is. If it sounds final, it probably is.

Release of all claims language

This is the clause that does significant damage when it's too broad.

“The undersigned releases and forever discharges any and all claims, known or unknown, arising out of the accident.”

Plain English: you're not just settling the dispute you understand today. You may also be waiving claims you haven't fully measured yet, including vehicle-related losses that weren't carved out.

That's why the negotiation shouldn't start with the form. It should start earlier, in the demand phase, where your losses are itemized and supported. A structured demand letter should include economic damages and property damage backed by certified appraisals. According to guidance on motor vehicle accident settlement demands, invoking the Appraisal Clause during that phase can boost total loss settlement value by 20-40% before a final release is drafted.

Indemnification language

Some forms contain language that sounds harmless because it doesn't mention your payout directly.

“The releasor agrees to indemnify and hold harmless the released parties from any further claims arising from the incident.”

That means if another bill, lien, or claim shows up later, the insurer may try to shift that problem back onto you. This clause deserves attention, especially if treatment is ongoing or billing is still unsettled.

No admission of liability language

This clause is common and usually not the clause that costs you money, but you should still understand it.

“This settlement is a compromise of disputed claims and is not an admission of liability by any party.”

Plain English: they're paying to end the claim, not admitting fault. That's standard. Don't waste your energy fighting this line if the issue is undervaluation.

Property damage wording that looks narrower than it is

Some releases appear to address vehicle damage only, but the wording reaches further.

Watch for phrases that combine vehicle damage with “all related losses,” “any consequences of repair,” or “all claims arising from ownership or use of the vehicle after the loss.” Those phrases can swallow diminished value issues.

If the insurer is pricing your car using a disputed actual cash value method, learn how that number gets built before you sign. A useful reference is this breakdown of actual cash value in auto insurance.

What to check line by line

Use this quick review before you sign anything:

- Scope of release. Does it say property damage only, or all claims of every kind?

- Known and unknown claims. If that phrase appears, stop and read even more carefully.

- Vehicle-specific carveouts. If diminished value or valuation disputes aren't excluded, assume they're being released.

- Payment description. Does the amount clearly tie to a category of loss, or is it a lump sum meant to wipe everything out?

- Names of released parties. Some forms release more people and companies than you expected.

If a clause is hard to explain in one plain sentence, don't sign it that day.

Legal wording isn't there to impress you. It's there to define what you can never come back for.

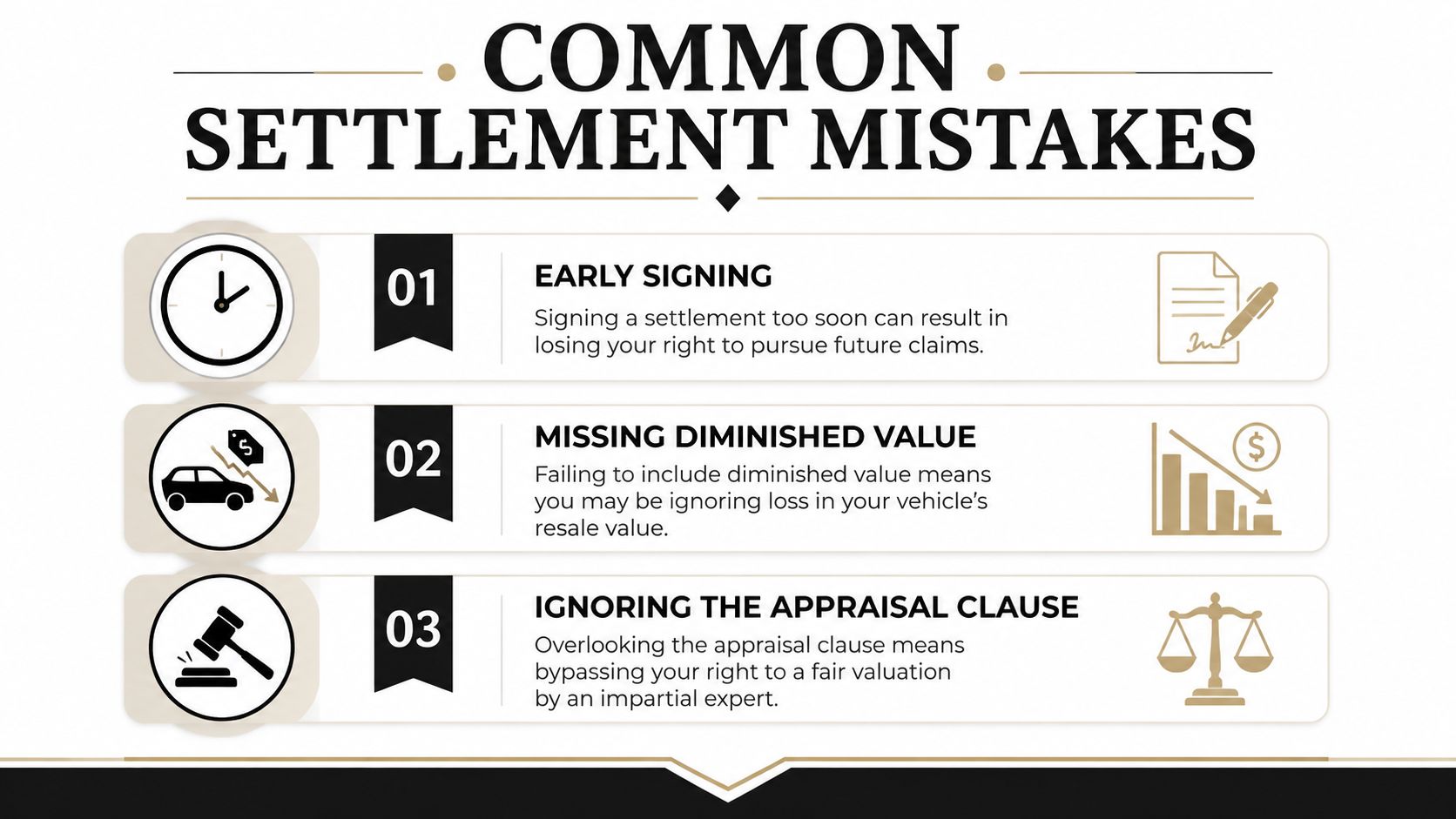

Avoid These Critical Mistakes Before You Sign

Most bad settlements don't happen because people are careless. They happen because people are overwhelmed, busy, sore, without a car, and tired of dealing with the adjuster.

That's exactly when insurers have the advantage.

According to analysis of settlement form risks, 70% of unrepresented claimants accept undervalued deals, 42% sign prematurely, and insurers' software can lowball total loss values by 15-30% below actual cash value. Those aren't minor errors. Those are claim-shaping mistakes.

Mistake one: signing because the adjuster sounds confident

Adjusters do this every day. You don't. So when they say the form is standard or the offer is fair, people assume delay is pointless.

It isn't.

Confidence from the insurer is not proof of accuracy. It's often just proof that they want the file closed before you question the valuation, the repair history impact, or the wording in the release.

Mistake two: treating the first vehicle number like a fact

A total loss number can look precise because it comes with line items, condition ratings, and comparable vehicles. But a polished report can still be wrong. Software can miss local market realities, upgrades, scarce trims, or vehicle-specific demand.

If you want a plain-language legal perspective on why first offers deserve skepticism, this guide for accident victims on settlement is worth reading.

Mistake three: separating injury timing from vehicle timing

People often think, “I'll settle the car now and deal with everything else later.” Sometimes that works if the paperwork is narrowly drafted. Sometimes it wipes out more than expected.

The danger is not just speed. It's speed plus broad language.

A better decision filter

Before you sign, answer these questions:

- Has every part of the claim been valued, not just the visible damage?

- Do I know whether the release is broad or limited?

- Has anyone independent reviewed the vehicle number?

- Am I signing to solve the claim, or just to end the stress?

If your answer to any of those is no, you're not ready.

The worst time to evaluate a settlement is when you're desperate for the process to be over.

What smart delay looks like

Delay doesn't mean ghosting the insurer. It means staying organized and refusing to finalize before the numbers and the language make sense.

Use a short checklist:

- Ask for the valuation support. Get the report, comparable vehicles, and condition adjustments.

- Ask what exactly the form releases. Don't accept vague reassurance over the phone.

- Keep communication in writing whenever possible.

- Separate urgency from finality. You can respond promptly without signing immediately.

A fast claim isn't a good claim if the number is wrong and the release is broader than you realized.

How to Fight for Your Vehicle's True Value

Your vehicle claim is not just a side issue attached to the accident. It's its own negotiation, and a standard car accident settlement form often treats it like an afterthought.

That's a mistake, especially if the car was repaired or totaled.

Diminished value is real, even after proper repairs

A repaired car can drive well and still be worth less on the open market because buyers see accident history and pay less. That loss is diminished value.

Standard settlement forms often fail to address future diminished market value, which can be a 10-30% drop in resale value. A 2023-2024 study found 68% of policyholders regretted signing a general release due to overlooked diminished value claims, with average losses of $4,200 per vehicle in markets like WA and OR, according to analysis of release forms and overlooked diminished value claims.

That regret makes sense. Once the release is signed, many owners realize they settled the repair invoice but not the market stigma.

Repair quality matters, but so do repair parts

Vehicle value doesn't turn on one issue. It's affected by repair history, severity, panel replacement, structural work, and the kind of parts used.

If you're sorting through repair documentation and trying to understand how parts choices affect market perception, this explanation of the difference between OEM and aftermarket is useful context.

A buyer notices those details. So do appraisers. You should too.

Total loss offers can miss the real market

When a car is totaled, the insurer usually presents a number that looks objective. But “objective” often means software-generated, not market-tested against what your specific vehicle would command.

That's where owners get trapped. They assume the total loss amount reflects reality because it includes adjustments and comparable listings. But if the comparables are weak or the condition adjustments are tilted, the final number can still be off.

For a better grasp of the market side, review how to calculate fair market value for a vehicle.

Here's a helpful visual overview before you accept any vehicle payout:

What to gather before you negotiate vehicle value

Don't argue from frustration. Argue from documentation.

Bring together:

- Your valuation report or the insurer's report with your notes

- Photos and repair records that show the vehicle's condition before and after the accident

- Trim, options, mileage, and upgrade documentation

- Comparable listings that match your vehicle in region, condition, and equipment

- Repair invoices and parts documentation if the car was fixed and you're evaluating diminished value

A vehicle value dispute is not won by saying “that offer feels low.” It's won by showing why the number doesn't match the market.

If you treat the vehicle as just one line item in a broader settlement, you'll miss money. If you treat it like the separate valuation issue it is, you preserve your bargaining power.

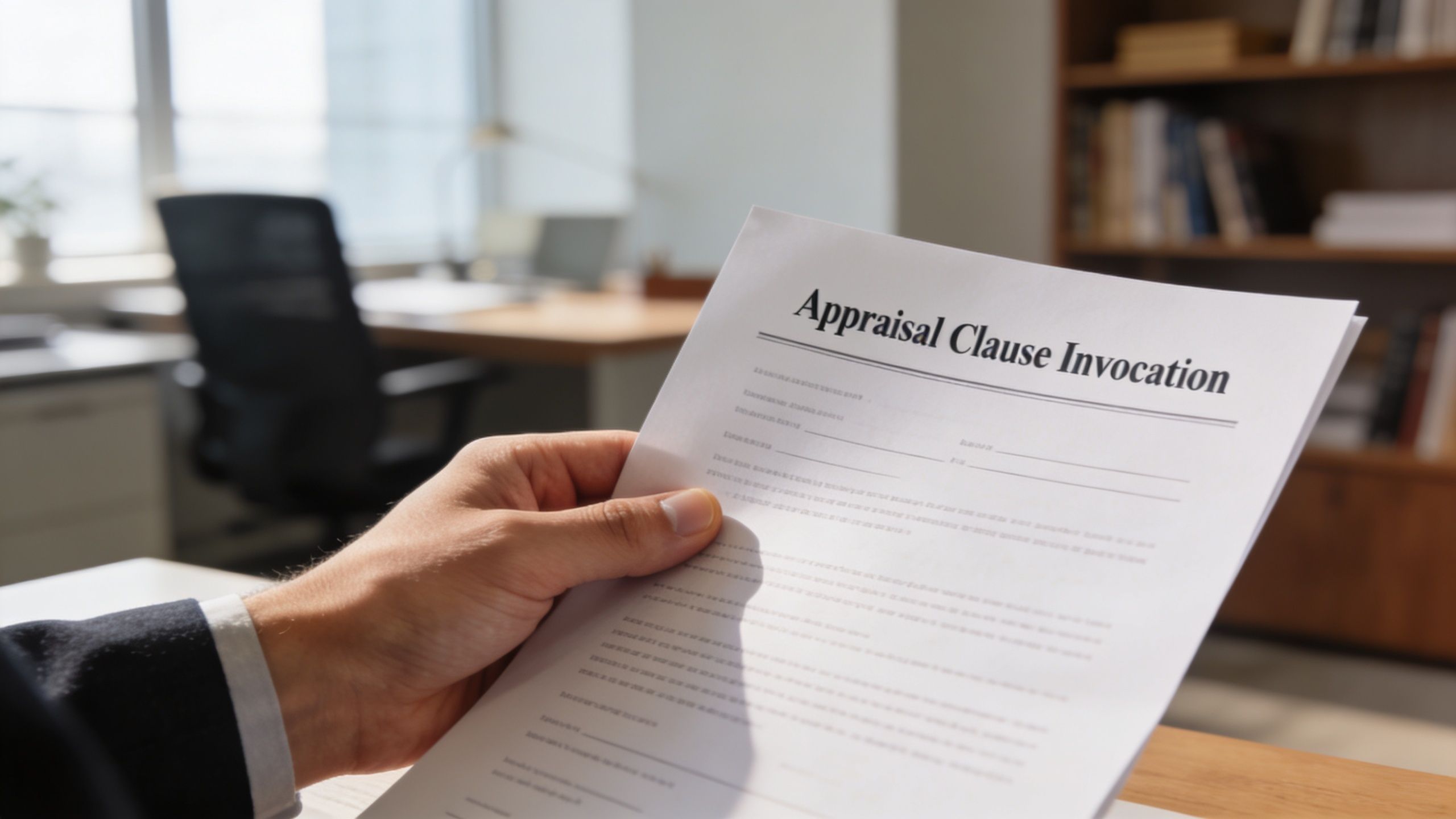

Invoking the Appraisal Clause Before You Sign the Form

If the insurer's number for your vehicle is wrong, the smartest move is often not arguing harder over the same report. It's changing the process.

That's what the Appraisal Clause does.

According to guidance on settlement letters and appraisal strategy, the Appraisal Clause is available in 47 states' policies, and invoking it before signing a release shifts valuation to neutral appraisers, boosting total loss payouts by 18-25% on average. That same source says this matters even more against a projected 22% increase in claims settled via biased insurer software in WA and OR in 2025.

What the clause actually does

Most drivers never look for it. They should.

The Appraisal Clause is usually buried in the policy language. It gives both sides a way to resolve a disagreement about vehicle value through appraisers rather than just accepting the insurer's internal number. It does not mean you've filed a lawsuit. It means you're forcing the valuation question into a more balanced process.

If you want to understand the mechanics, review this explanation of the insurance appraisal clause process.

When to invoke it

The right time is before you sign the car accident settlement form. Not after. The form closes the claim. The clause helps you challenge the vehicle value while the claim is still open.

Use it when:

- The total loss offer doesn't match market reality

- The insurer's comparables are poor matches

- Your car has upgrades, scarcity, or condition advantages

- You suspect valuation software is flattening the true number

The practical sequence

This isn't complicated, but it needs to be done in the right order.

- Read your policy and find the appraisal language.

- Notify the insurer in writing that you dispute the value and are invoking the clause.

- Choose an independent appraiser who understands total loss and diminished value methodology.

- Submit supporting records such as options, condition evidence, service history, and relevant comparables.

- Pause release discussions until the valuation process is finished.

That last point matters. Don't let the insurer separate the paperwork from the valuation dispute if the form will close your property claim.

Why this works better than endless back-and-forth

Adjuster negotiations often circle around the same software report. Appraisal changes the field. It moves the dispute toward market evidence, appraiser judgment, and documented vehicle specifics.

Expert view: If the insurer built the number with its own valuation system, don't assume a phone argument will fix it. Use the policy tool designed for value disputes.

The Appraisal Clause doesn't guarantee perfection. It does something better. It gives you a process with less built-in bias before you sign away your rights.

Your Top Questions About Settlement Forms Answered

Do I always need a lawyer to review a settlement form

No. But you do need someone qualified reviewing the part of the claim that's in dispute.

If your main problem is vehicle value, an independent appraiser is often the critical expert. If your injuries are serious, treatment is ongoing, or the release language is broad, legal review is smart. Don't default to one kind of help for every issue. Match the expert to the risk.

Can I negotiate the wording of the release form itself

Yes, and you should try when the wording is too broad.

A release is a contract. Contracts can be revised. If the form sweeps in claims that haven't been resolved, ask for narrower language or a carveout that preserves the unresolved property issue. Don't assume the insurer's first draft is untouchable.

If the money is negotiable, the wording is negotiable too.

What happens if I refuse to sign the form the adjuster sent

The claim stays open. That's not a failure. It just means the settlement is not complete.

The adjuster may push back or repeat that the form is standard. That doesn't change your rights. If the valuation is wrong or the release is too broad, refusing to sign is often the most financially responsible move you can make.

Should I settle the vehicle claim separately from the injury claim

Sometimes that's appropriate, but only if the paperwork is narrowly drafted and you understand exactly what stays open.

If the insurer sends a broad release and you think you're only settling the car, stop and read every line. The label on the form matters less than the scope of the release.

What if I already signed

Your options may be limited. That's the hard truth.

Still, gather the signed form, payment records, email chain, and valuation documents. Have someone review exactly what was released. People often remember the phone conversation, but the written release controls.

What's the one rule I should follow from here

Don't sign a car accident settlement form until the vehicle value issue is fully resolved.

That rule alone prevents a lot of avoidable damage.

If the insurer is lowballing your total loss or you're worried about giving up a diminished value claim, get expert help before you sign. Total Loss Northwest specializes in diminished value and total loss auto appraisals for Oregon and Washington vehicle owners, and provides diminished value support in all 50 states. They use independent market-based valuation and Appraisal Clause support to challenge biased insurance numbers and help you protect the money your vehicle is worth.