The secret to a successful car accident settlement negotiation doesn't start at the bargaining table. It starts the second the crash happens. Building a rock-solid case means meticulously documenting every piece of evidence you can get your hands on. This is what gives you leverage and justifies the true value of your claim, especially if your vehicle isn't a standard, off-the-lot model.

Build Your Case From the Ground Up

The groundwork for a fair settlement isn't laid in an office—it's laid right there at the scene of the accident. Those first few minutes and hours are your one and only shot to gather the raw, undeniable evidence that proves your side of the story. This is your opportunity to take control of a chaotic situation.

Think of every piece of information you collect as a building block. You're assembling a file that an insurance adjuster simply can't ignore or downplay. For a complete rundown, knowing exactly what to do after a car accident gives you a clear checklist for navigating those crucial first moments.

Document Everything on the Spot

Your phone is your best friend after a wreck. Before any cars are moved, start snapping pictures—and don't be shy. Take dozens of them from every angle imaginable. Get wide shots to capture the whole scene, including road conditions and traffic signs, then move in for close-ups of the damage on every vehicle involved.

Once you've got your photos, it's time to gather information. Your documentation checklist should include:

- Witness Information: If anyone saw what happened, get their name and phone number. A neutral third-party account is incredibly powerful.

- The Official Police Report: Always, always call the police. Their official report is a credible, unbiased record that's very difficult for an insurance company to argue with.

- Photos of Injuries: Take pictures of any visible injuries right away. Keep taking photos in the following days, as bruising and other signs can take time to appear.

Skipping this step is a huge mistake. Without this evidence, your negotiation becomes a "he said, she said" situation, and the insurance company has a lot more experience playing that game.

The better your documentation, the stronger your negotiating position. An adjuster can argue with your memory of events, but they can't argue with a timestamped photo or an official police report.

Get a Handle on Key Valuation Terms Now

For many people, the real fight isn't over who was at fault—it's about what their car was actually worth. This is especially true if you own a classic, customized, or otherwise unique vehicle. Standard "blue book" values just don't cut it.

That’s why you need to understand two key concepts from day one: Total Loss and Diminished Value.

A vehicle is considered a total loss when the repair costs are more than a certain percentage of its value before the accident. Diminished Value is the drop in your car's market price even after it's been perfectly repaired. That accident is now on its record, and it will sell for less.

Knowing these terms right away ensures you're not just asking for repair costs—you're demanding compensation for the full, true financial hit you've taken.

Figuring Out What Your Car Accident Claim is Really Worth

Here's the first rule of negotiating with an insurance company: never let their internal software be the final word on your vehicle's value. Their first offer is almost always just a starting point. It’s a number spit out by an algorithm that cares more about national averages than the reality of your car in your local market.

To get a fair settlement, you have to build your own case for what you're owed. This goes way beyond just the obvious repair estimates. Think of it as putting together a detailed invoice for the entire incident, where every single line item is backed up by solid proof.

Breaking Down Your Claim's Components

The total value of your claim isn't just about parts and labor. It’s a combination of several different types of damages, and each one needs its own documentation. A successful car accident settlement negotiation lives or dies on your ability to prove every component.

Your valuation needs to meticulously account for all of it:

- Vehicle Value (Repairs or Total Loss): This is the heart of your property damage claim. For repairs, get multiple quotes. If your car is a total loss, your job is to establish its actual cash value (ACV) the moment before the crash. Our guide on calculating a total loss vehicle's value walks you through this entire process.

- Diminished Value: Even with flawless repairs, your vehicle is now worth less simply because it has an accident history. This is a real, compensable loss that adjusters often "forget" to mention.

- Medical Expenses: This covers everything—the ER visit, physical therapy, prescriptions, and any future care your doctor says you’ll need.

- Lost Wages: Did you miss work because of your injuries or to deal with the aftermath? Calculate that lost income. Pay stubs or a letter from your boss are crucial here.

- Other Out-of-Pocket Costs: Rental car bills, towing fees, and other incidental costs add up quickly. Make sure they're on your list.

The Power of an Independent Appraisal

So, how do you prove your numbers are right, especially when the insurer’s valuation seems ridiculously low? The single most effective tool you have is an independent appraisal.

An independent appraisal report from a certified expert is the best way to dismantle an insurer’s lowball offer. It replaces their generic, software-generated number with a valuation grounded in your specific vehicle and local market data, giving you undeniable leverage.

A professional appraiser does the legwork. They find comparable vehicles ("comps") that have actually sold recently in your area—not just ones listed for sale. They dig into your vehicle's specific condition, mileage, trim, and any custom work you've had done. The result is a professional, evidence-based document that justifies every penny of your claim.

This step is non-negotiable for owners of classic cars, customized trucks, or high-value vehicles where standard "book values" are completely useless. An appraisal changes the entire conversation, shifting it from their biased numbers to your real-world losses. It forces them to explain exactly why their figure is so much lower than a market-based expert valuation.

To give you some perspective, here are the typical settlement ranges insurers often work from.

Typical Settlement Ranges By Accident Type

This table shows average settlement amounts for common types of car accidents, providing a baseline to understand initial insurance offers. Note how these averages may not reflect the true value of unique or high-value vehicles.

| Accident Type | Average Settlement Range |

|---|---|

| Rear-End Collision | $16,000 – $19,000 |

| Side-Impact (T-Bone) | $25,000 – $50,000 |

| Head-On Collision | $50,000 – $100,000+ |

| Multi-Vehicle Pile-Up | Varies Widely |

While the average U.S. motor vehicle accident settlement is around $37,248, insurers use figures like the ones above to anchor their initial offers low. This becomes a huge problem if your unique vehicle’s value is far higher than these norms. Your goal is to make the negotiation about your car, not some national statistic.

How to Negotiate with an Insurance Adjuster

Stepping into a negotiation with an insurance adjuster isn't just a phone call; it's a strategic engagement. All that time you spent gathering documents and getting an independent appraisal? This is where it all comes together.

The entire car accident settlement negotiation boils down to who controls the story. The adjuster’s primary job is to resolve your claim for as little money as possible, and fast. Your job is to calmly and persistently guide them back to the reality of your documented losses.

Managing the Conversation

When you get that first call from the adjuster, keep one thing in mind: less is more. Stick to the hard facts of the accident and the damages to your vehicle. Don't get emotional, never apologize, and avoid guessing about who was at fault. Anything you say can be noted and used against your claim later.

Keep all your communications professional and grounded in your evidence. If you have a phone call, send a follow-up email that same day recapping the conversation. This simple step creates a paper trail and prevents "misunderstandings." For a deeper dive, check out our guide on how to deal with insurance adjusters for more strategies.

The First Offer Is Just the Beginning

Here’s a rule of thumb I’ve learned over years of doing this: never accept the first offer. It’s almost guaranteed to be a lowball figure spit out by a computer program that knows nothing about your car's true condition, upgrades, or local market value.

When the adjuster gives you that initial number, don't get angry or defensive. A calm, simple, and firm rejection is all you need to signal that the real negotiation is about to start.

Pro Tip: When you get that lowball offer, try saying something like this: "Thanks for getting back to me, but that number isn't in the ballpark of what my documentation shows. My independent appraisal values the vehicle at [Your Number]. Can you walk me through the specific comps you used to get to your figure?"

This response is effective for a few key reasons:

- It politely says "no" while keeping the conversation moving forward.

- It immediately shifts the focus back to your evidence.

- It puts the adjuster on the spot to justify their low valuation with facts, not just a number.

Using Your Evidence as Leverage

Your demand package is your toolkit, and your independent appraisal is the most powerful tool in it. When the adjuster pushes back on your number, don't argue—point to the facts.

Refer them to specific comparable vehicles listed in your appraisal report. Point out the receipts for that new engine or custom paint job. The goal is to keep the conversation centered on your proof. Don't let them drag you into hypotheticals about "typical" claims. This isn't about averages; it's about your car.

By patiently returning to the evidence every single time, you command the negotiation and make them work within your framework. That's how you get a fair settlement.

Countering a Lowball Settlement Offer

So, the insurance adjuster’s first offer is in, and it's a letdown. Maybe even insulting. Before you get frustrated, just remember: this is completely normal. Think of it as the opening bid in an auction, not the final price. This is where the real car accident settlement negotiation begins, and your goal is to calmly and logically dismantle their low number and build an undeniable case for what you're truly owed.

First things first, don't just take their number over the phone. Politely insist that the adjuster send you their complete valuation report in writing. You need to see exactly how they landed on that figure. This report will reveal the comparable vehicles (or "comps") they used, their assessment of your car's condition before the crash, and, most importantly, everything they chose to ignore.

Pinpointing the Weaknesses in Their Offer

With their report in hand, it's time to put on your detective hat. Insurance company valuations are often built on shaky ground, and your job is to find the cracks.

Look for these classic weak spots:

- Bad Vehicle Comps: Did they really compare apples to apples? It’s common for adjusters to use base models with high mileage to bring the average value down. Check that the trim, mileage, and overall condition of their comps truly match your vehicle.

- Wrong Zip Code: Car values are local. If they pulled comps from a cheaper market a few hundred miles away, that’s a major flaw. The value should be based on what your car was worth in your area.

- Missing Diminished Value: If your car is being repaired instead of totaled, its resale value has taken a permanent hit. This is called diminished value, and it's a real, compensable loss that insurers often conveniently forget to include.

- Unjustified Condition Rating: Did they label your well-maintained car as "average" or "fair" with no real basis? This is a quick way for them to shave value off right from the start.

It's the classic dilemma: whether to accept the insurance company's first settlement offer. The short answer is almost always no. That initial figure is a feeler, designed to see if you’ll take a quick and easy payout that saves them money.

This is where your independent appraisal report becomes your most powerful weapon. It's not just your opinion against theirs; it's a certified, market-based valuation that an adjuster can't just wave away.

Constructing Your Written Counteroffer

Never counter their offer with a simple phone call. A formal, written response signals that you're serious and creates a paper trail. Keep it professional, to the point, and packed with evidence.

Start your letter by professionally rejecting their offer. Then, go point by point, explaining why your valuation is the accurate one. For every weak spot you found in their report, present your counter-evidence. If they used shoddy comps, list the better ones from your appraisal. If they ignored your new tires, include the receipt.

Negotiations are more data-driven than ever. The average auto liability claim for property damage is now around $6,551, with bodily injury claims averaging $26,501. Insurers lean on these internal numbers, and many now use automated valuation tools, especially in virtual mediations (which now see an 87% settlement rate). These systems are notorious for undervaluing unique, classic, or heavily upgraded vehicles, often missing thousands of dollars in real-world value. This makes a human-led, independent appraisal absolutely essential.

Wrap up your letter by clearly stating your counteroffer. This is your initial demand, supported by the mountain of evidence you've just presented. Attach your independent appraisal and all your other documentation. Now, the ball is back in their court, and you've forced them to justify their low number against your rock-solid case.

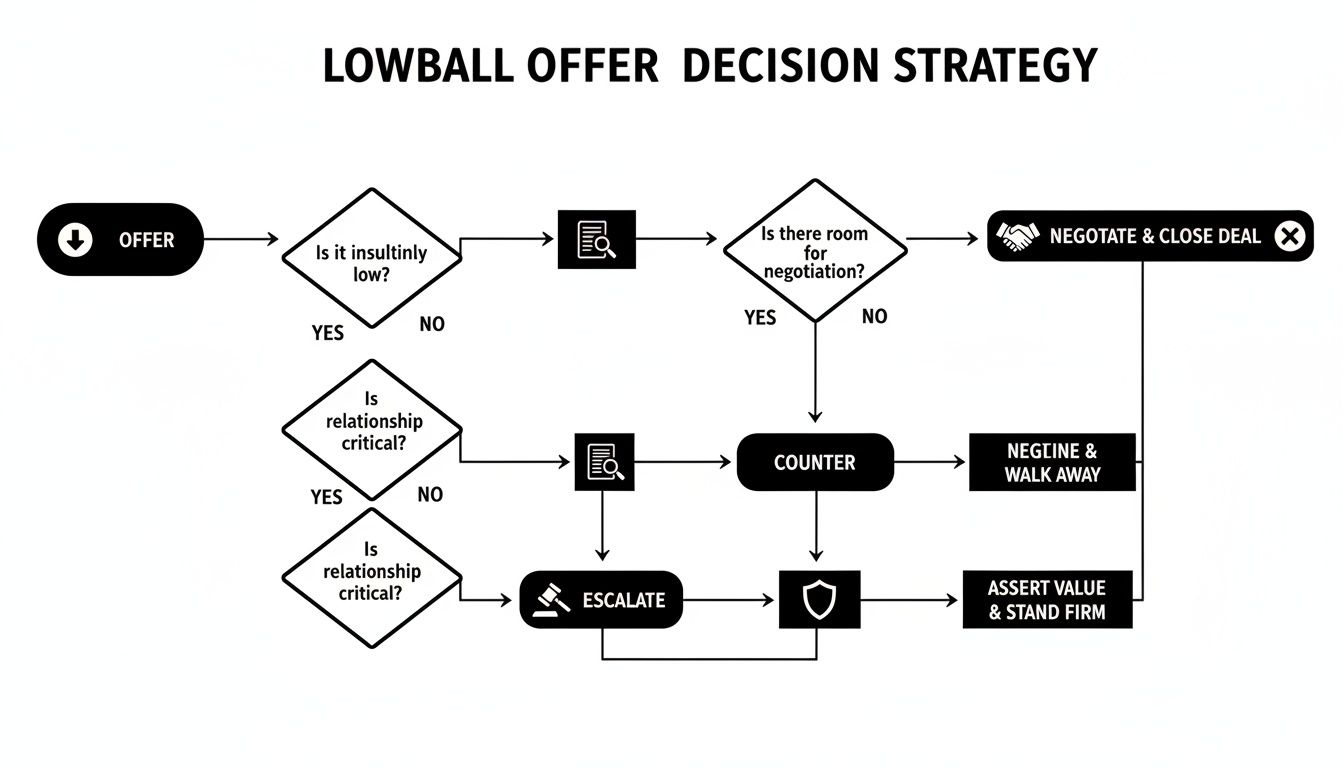

When to Escalate or Finalize Your Settlement

You've laid out all your evidence, made a solid counteroffer, and now you're met with… crickets. Or worse, the adjuster comes back with another laughably low number and utters the dreaded words, "This is our final offer."

This is the make-or-break moment. You have to decide: take what's on the table, or dig in your heels and escalate?

Sometimes, just signaling that you’re ready to take the next step is enough to get them to cough up a better offer. At the end of the day, insurance companies are businesses, and dragging things out costs them time and money they'd rather not spend.

Signs It’s Time to Escalate

If the adjuster is giving you the runaround with stall tactics, refusing to explain their low valuation with actual data, or just won't move from an offer that completely ignores your evidence, it's time to bring out the big guns.

You have a few powerful options here:

- Invoke the Appraisal Clause: This is your ace in the hole. Formally invoking this clause in your policy forces the insurance company to hire their own independent appraiser to hash it out with yours. It effectively removes the stubborn adjuster from the equation.

- File a Complaint with the State: Every state has an insurance commissioner or department that oversees these companies. Filing an official complaint gets a regulator to look at your case, which puts serious pressure on the insurer to play fair.

- Talk to a Lawyer: You don't always have to hire one to file a lawsuit. Often, a single, strongly-worded letter from an attorney is all it takes to make an insurer suddenly see things your way.

This decision tree gives you a clear visual for navigating this exact situation.

As you can see, the path is logical: receive the offer, counter with your proof, and if they still refuse to be reasonable, it's time to escalate.

Knowing When to Shake Hands and Finalize the Deal

So, how do you know when you’ve actually won? A fair offer is one that lines up with the real-world losses you've meticulously documented—your independent appraisal, your diminished value report, everything.

If the adjuster has finally come up to a number that genuinely makes you whole again, it’s probably time to close the deal.

Hold on—don't sign anything just yet. Before your signature touches any paper, demand a copy of the settlement release form. Read every single word. Look for tricky clauses that might release them from future claims or contain confusing language. Once you sign this, it's final.

The truth is, very few car accident cases ever see the inside of a courtroom. In the U.S., a staggering 95.8% of auto claims are resolved through negotiation, not a trial. You can read more about these global settlement negotiation trends to see the bigger picture.

Insurers count on you not knowing this. They build their entire strategy around the assumption that you'll take their first or second lowball offer and go away. Your willingness to push back and escalate is your single greatest piece of leverage.

Once you’re satisfied with the final number and you’re sure the release form is clean, you can sign with confidence and finally close the book on this whole ordeal.

Common Questions About Car Accident Settlement Negotiations

After a car accident, the last thing you want is a confusing, drawn-out battle with an insurance company. You just want straight answers. Let's cut through the noise and tackle some of the most common questions people have when they’re trying to negotiate a fair settlement.

How Long Does a Car Accident Settlement Negotiation Take?

This is the million-dollar question, and the honest answer is: it depends. I’ve seen simple property damage claims get settled in a couple of weeks, but more complicated cases can easily stretch out for months.

So, what causes the delays? A few things usually slow the process down:

- The Severity of the Damage: Fighting over a total loss valuation is a different beast than getting a bumper replaced. The bigger the numbers, the longer it often takes.

- The Quality of Your Paperwork: If you come prepared with an independent appraisal and solid documentation, things move much faster. A claim built on shaky ground gives the adjuster an excuse to drag their feet.

- The Adjuster Themselves: Some are professional and efficient. Others use delay tactics as a core strategy, hoping you'll get frustrated and take a low offer.

The key takeaway here is that patience is your biggest asset. Rushing to an agreement almost always works in the insurance company’s favor, not yours.

Do I Really Need a Lawyer to Negotiate My Settlement?

For a lot of claims involving just property damage or minor injuries, you can absolutely handle the negotiations yourself if you're willing to do the prep work. You don't always need to bring in an attorney. Legal help becomes critical when you're facing serious injuries, complicated questions about who was at fault, or when you suspect the insurance company is acting in bad faith.

But when the fight is purely about your car's value—like a total loss or diminished value claim—your most powerful weapon isn't a lawyer. It's an independent appraiser. A certified appraisal report gives you the hard evidence you need to dismantle the adjuster’s lowball offer, often making a lawyer unnecessary for that specific part of your claim.

Deciding on a lawyer really comes down to the details of your case. For vehicle value disputes, the leverage comes from a solid appraisal. For anything involving significant medical bills, getting legal advice is usually the smartest move.

What Is the Appraisal Clause and When Should I Use It?

The appraisal clause is a tool buried in most auto insurance policies that many people don't even know exists. It's specifically designed to break a deadlock when you and the insurer just can't agree on what your vehicle is worth.

The time to use it is when the adjuster won't move from a ridiculously low offer. Invoking this clause takes the decision out of the adjuster's hands and gives it to impartial experts. Here’s how it works: you hire a certified appraiser, the insurer hires one, and if they can’t agree on a value, a neutral third-party "umpire" steps in to make a final, binding decision. For more answers to common questions, you can check out some further FAQs on settlement negotiations.

At Total Loss Northwest, we provide the certified, independent appraisals that force insurance companies to play fair. If you're in Oregon or Washington and stuck with a lowball offer on a total loss or diminished value claim, we’re here to help. We can invoke the Appraisal Clause for you and fight to get the accurate settlement you're owed. Don't let their software dictate your vehicle's value—contact us today at https://totallossnw.com.